- Pharmaceuticals

- Bile Duct Cancer Treatment Market

Bile Duct Cancer Treatment Market Size, Share, and Growth Forecast 2026 - 2033

Bile Duct Cancer Treatment Market by Treatment Type (Chemotherapy, Targeted Therapy, Immunotherapy, Surgery, Radiation Therapy), Cancer Type (Intrahepatic bile duct cancer, Extrahepatic bile duct cancer (Perihilar Bile Duct Cancer, Distal Extrahepatic Bile Duct Cancer)), Treatment Provider (Hospitals, Cancer specialty centers, Ambulatory care centers), by Regional Analysis, 2026 - 2033

Bile Duct Cancer Treatment Market Share and Trends Analysis

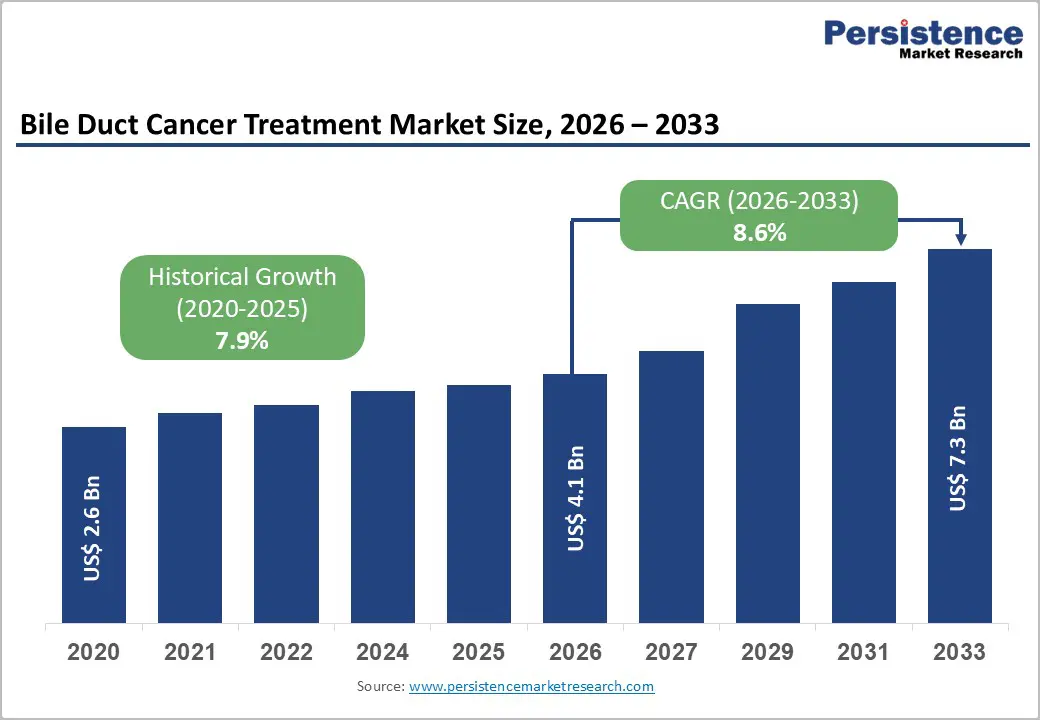

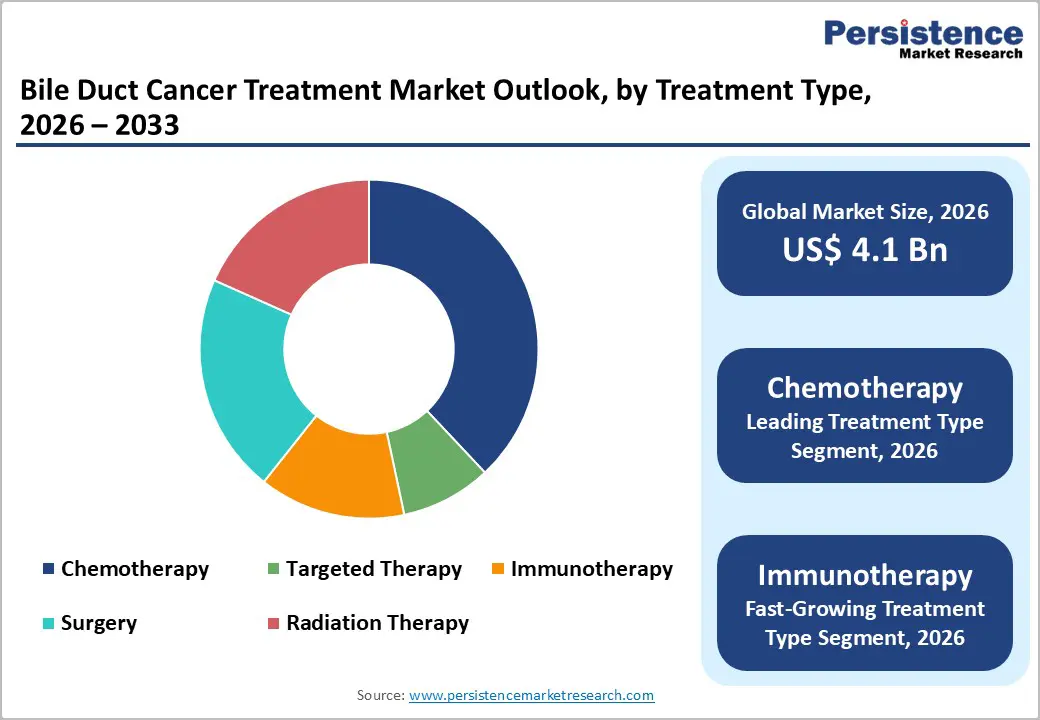

The global bile duct cancer treatment market size is expected to be valued at US$ 4.1 billion in 2026 and projected to reach US$ 7.3 billion by 2033, growing at a CAGR of 8.6% between 2026 and 2033.

The market is expanding as bile duct cancer (cholangiocarcinoma) management shifts from conventional chemotherapy-only paradigms toward precision oncology and immunotherapy-based regimens, significantly improving survival outcomes in advanced disease.

FDA approvals of combination regimens such as pembrolizumab with chemotherapy and durvalumab with gemcitabine-cisplatin have demonstrated meaningful overall survival gains compared with chemotherapy alone in unresectable or metastatic biliary tract cancers, thereby accelerating the adoption of novel systemic therapies in first-line settings.

Key Industry Highlights:

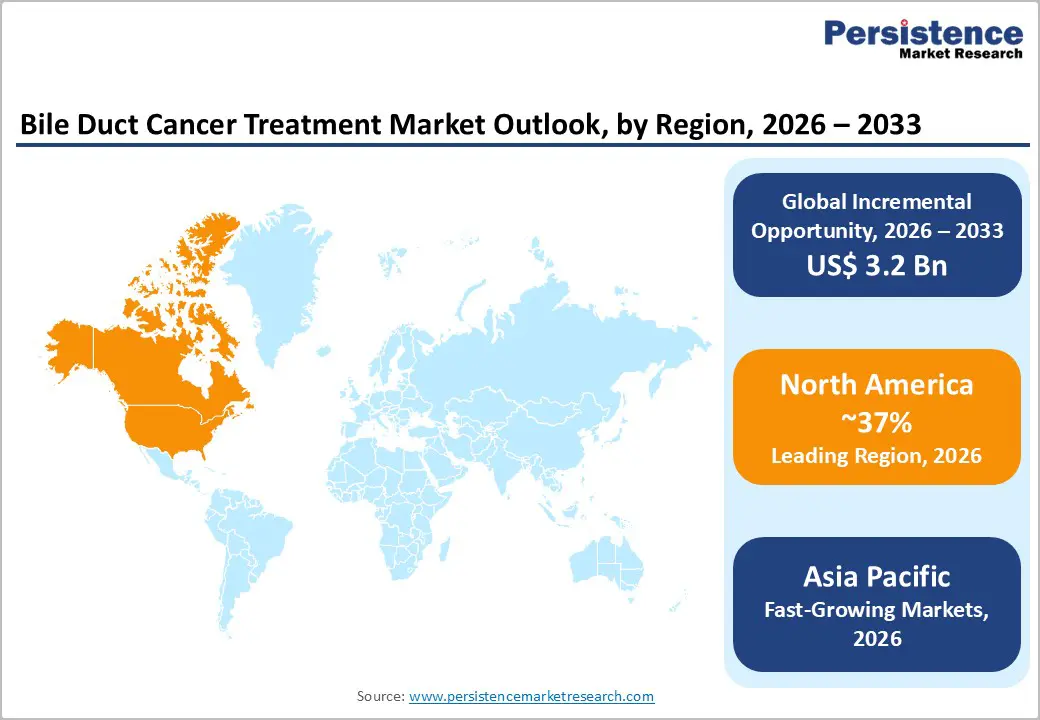

- Leading Region - North America accounts for about 37% of the bile duct cancer treatment market in 2025, supported by strong FDA-driven innovation, high per-capita oncology spending, dense networks of NCI-designated cancer centers, early adoption of molecular profiling, and rapid integration of new targeted and immunotherapy regimens into clinical practice.

- Fastest Growing Region - Asia Pacific is the fastest-growing regional market, underpinned by extremely high cholangiocarcinoma incidence in countries such as Thailand, expanding tertiary oncology infrastructure in China, Japan, and India, rising clinical-trial activity, and progressive access to advanced systemic therapies.

- Dominant Treatment Type: Chemotherapy remains the dominant treatment type with around 38% share in 2025, anchored by gemcitabine-cisplatin regimens validated in ABC-02 and optimized in Japanese trials, wide generic availability, and its role as the universal backbone to which targeted and immunotherapy agents are increasingly added.

- Fastest Growing Treatment Type: Immunotherapy Transformation: Immunotherapy constitutes the fastest-growing segment, propelled by first-line approvals for durvalumab and pembrolizumab, strong OS improvements versus chemotherapy alone, and expanding pipelines exploring dual-checkpoint regimens and combinations with targeted agents, particularly in biomarker-defined subgroups.

- Key Opportunity - Precision Medicine and Biomarker-Driven Care: Precision medicine based on NGS-guided detection of FGFR2, IDH1, HER2, and other actionable alterations in cholangiocarcinoma, collectively present in a substantial minority of patients, creates a scalable opportunity for targeted therapies, companion diagnostics, and personalized combinations that can meaningfully improve outcomes and differentiate offerings.

| Key Insights | Details |

|---|---|

| Bile Duct Cancer Treatment Market Size (2026E) | US$ 4.1 billion |

| Market Value Forecast (2033F) | US$ 7.3 billion |

| Projected Growth CAGR (2026 - 2033) | 8.6% |

| Historical Market Growth (2020 - 2025) | 7.9% |

Market Dynamics

Drivers - Breakthrough Advancements in Targeted Therapies and Precision Oncology

Targeted therapies have become a core growth engine as they address the molecular heterogeneity of cholangiocarcinoma and deliver superior outcomes in biomarker-defined subgroups. FGFR2 fusion-positive intrahepatic cholangiocarcinoma, which occurs in roughly 10-15% of cases, has become a key focus, with agents such as pemigatinib demonstrating objective response rates of about 37% and median progression-free survival (PFS) of about seven months in previously treated patients. Similarly, futibatinib has reported response rates exceeding 40% and a median PFS of nearly 9 months, reinforcing the clinical value of this class. In parallel, IDH1 mutations in approximately 15-20% of intrahepatic tumors have been successfully targeted by ivosidenib, which achieved a roughly 63% reduction in risk of progression or death versus placebo in the ClarIDHy trial. These advances, coupled with the widespread uptake of next-generation sequencing (NGS) at major centers such as Memorial Sloan Kettering Cancer Center and MD Anderson Cancer Center, are embedding molecular profiling into routine practice and structurally expanding demand for biomarker-driven drugs.

Expansion of Immunotherapy in First-Line and Biomarker-Defined Settings

Immunotherapy is rapidly reshaping first-line standards and unlocking new growth pools by improving survival beyond benchmarks set by chemotherapy in advanced biliary tract cancers. The pivotal TOPAZ-1 trial showed that adding durvalumab to gemcitabine-cisplatin significantly improved overall survival (OS) versus chemotherapy alone, with a hazard ratio of about 0.80 and 24-month OS rates almost doubled in some subgroups, leading to FDA approval for unresectable or metastatic disease. Subsequently, KEYNOTE 966 established pembrolizumab plus gemcitabine and cisplatin as another first-line standard; OS increased from about 10.9 months with chemotherapy to approximately 12.7 months with the combination, corresponding to a hazard ratio around 0.83 in a population of more than 1,000 patients. Further momentum came from zanidatamab, a bispecific HER2-targeted antibody, which received FDA approval for HER2-positive biliary tract cancers after phase II data showed objective response rates above 40% and durable responses beyond 12 months in a heavily pretreated cohort. As multiple checkpoint inhibitors and immunotherapy combinations advance through late-stage trials, their expanding use across lines of therapy will materially lift market value.

Restraints - High Cost of Novel Agents and Affordability Gaps in Endemic Regions

The premium pricing of targeted therapies and immuno-oncology agents significantly constrains real-world uptake, especially in low- and middle-income countries where bile duct cancer burden is highest. Annual therapy costs for many oral targeted agents and checkpoint inhibitors in oncology routinely exceed US$ 150,000-200,000 per patient in markets such as the United States, straining payer budgets and limiting reimbursement in less affluent settings. Regions with extreme cholangiocarcinoma incidence, such as northeastern Thailand, where reported rates can reach about 60 per 100,000 population and parts of China with millions infected by liver flukes, face structural underinsurance and constrained public healthcare budgets. In addition, access to NGS and advanced imaging is uneven; comprehensive molecular profiling can cost several thousand US dollars per test and is often concentrated in tertiary centers, thus excluding rural or lower-income patients from precision medicine pathways. These affordability and access gaps temper the speed and breadth of diffusion of innovative therapies, especially in the very markets with the highest disease burden.

Opportunity - Acceleration of Immunotherapy and Rational Combination Strategies

The immunotherapy segment offers substantial headroom as checkpoint inhibitors move from niche to central components of bile duct cancer treatment algorithms. Following first-line approvals for durvalumab and pembrolizumab, numerous phase II and III studies are evaluating dual checkpoint regimens (for example, PD 1/PDL1 plus CTLA-4 blockade) and combinations with targeted therapies such as FGFR2 inhibitors to deepen responses and delay resistance. Early data from precision therapy-oriented trials show that integrating immunotherapy with molecularly targeted agents can generate additive or synergistic benefits in subsets of patients with specific genomic alterations or immune signatures. The approval of zanidatamab for HER2-positive biliary tract cancer, based on objective response rates above 40% and durable responses in a historically refractory population, validates the opportunity in biomarker-selected immunotherapy. In parallel, emerging platforms such as cancer vaccines, adoptive T-cell therapies, and tumor microenvironment modulators are entering early-phase trials in cholangiocarcinoma. As clinical guidelines are progressively updated and real-world evidence accumulates, immunotherapy’s share of treated patients is expected to expand rapidly, making it the fastest-growing modality.

Category-wise Analysis

Treatment Type Insights

Chemotherapy remains the leading treatment type, accounting for about 38 share in 2025, underpinned by its universal role as the backbone of systemic therapy in biliary tract cancers. The landmark ABC2 trial established gemcitabine plus cisplatin as the standard of care, improving median OS from roughly 8.1 months with gemcitabine alone to 11.7 months with the doublet and reducing the risk of death by around 36%. Subsequent studies, such as the Japanese KHBO1401MITSUBA phase III trial, demonstrated that adding S1 to gemcitabine-cisplatin further extended median OS to approximately 13.5 months with response rates above 40%, reinforcing chemotherapy’s centrality. The widespread availability of generic cytotoxics and established administration infrastructure in both high-income and resource-limited settings sustain its leading share. However, immunotherapy is the fastest-growing segment as combinations with chemotherapy become first-line standards following TOPAZ1 and KEYNOTE966, and checkpoint inhibitors expand into adjuvant and second-line indications.

Treatment Provider Insights

Hospitals represent the dominant treatment provider category, accounting for approximately 54% share in 2025, reflecting the need for multidisciplinary, high-acuity care in bile duct cancer. Leading comprehensive cancer centers such as Memorial Sloan Kettering Cancer Center, Mayo Clinic, and MD Anderson Cancer Center manage hundreds of liver and bile duct cancer cases annually and offer integrated services spanning complex hepatobiliary surgery, interventional radiology, advanced radiation therapy, systemic oncology, and palliative care. These institutions also routinely perform NGS-based profiling and enroll patients into cutting-edge clinical trials, strengthening the hospital channel’s role in the uptake of novel therapies. Cancer specialty centers form the fastest-growing provider segment as dedicated hepatobiliary programs emerge in both Western and Asia-Pacific markets, leveraging high case volumes and protocol-driven care to improve outcomes versus community hospitals. Ambulatory care centers participate mainly through chemotherapy infusion and follow-up services, but their share remains smaller due to the need for complex diagnostics, intensive monitoring, and surgical or interventional procedures that are largely hospital-based.

Regional Insights

North America Bile Duct Cancer Treatment Market Trends and Insights

North America represents a leading region in the bile duct cancer treatment market due to its advanced healthcare infrastructure, strong oncology research ecosystem, and early adoption of innovative therapies. The region benefits from high awareness levels, widespread access to diagnostic imaging, and routine use of molecular profiling, enabling timely treatment initiation and personalized therapy selection. Chemotherapy remains the treatment backbone; however, North America is at the forefront of integrating targeted therapies and immunotherapies into standard care, supported by favorable regulatory pathways and rapid clinical trial translation. Strong presence of specialty cancer centers and academic hospitals further accelerates the uptake of novel treatments and combination regimens. Additionally, higher healthcare spending and broader insurance coverage compared to other regions improve patient access to advanced therapies. Ongoing clinical trials, real-world evidence generation, and physician familiarity with precision oncology continue to shape treatment practices, positioning North America as a key driver of innovation, revenue contribution, and clinical advancement in the global bile duct cancer treatment market.

Asia Pacific Bile Duct Cancer Treatment Market Trends and Insights

Asia Pacific is emerging as a high-growth region in the bile duct cancer treatment market, driven by a rising disease burden, expanding healthcare infrastructure, and improving access to oncology care. The region has a comparatively higher prevalence of bile duct cancer, particularly in countries with elevated rates of liver disease, hepatitis infections, and parasitic exposure. Increasing investments in hospital expansion, cancer specialty centers, and diagnostic capabilities are improving early detection and treatment access. While chemotherapy remains the most commonly used treatment due to affordability and availability, adoption of targeted therapy and immunotherapy is gradually increasing in urban and tertiary care settings. Growing participation in clinical trials and partnerships with global pharmaceutical companies are accelerating the introduction of novel therapies. Additionally, government initiatives to strengthen cancer care programs and expand insurance coverage are supporting market growth. Despite ongoing challenges related to reimbursement and rural healthcare access, Asia Pacific is expected to witness strong treatment demand and rapid market expansion over the forecast period.

Competitive Landscape

The global bile duct cancer treatment market competition landscape is characterized by a mix of well-established oncology players and emerging biopharmaceutical innovators focused on advancing treatment options. Competition centers on developing therapies that improve survival, demonstrate tolerability, and target specific molecular pathways. While traditional chemotherapy remains widely used, late-stage clinical progress in targeted and immune-based therapies has intensified competitive dynamics. Companies are investing in clinical trials, combination regimens, and precision medicine approaches to gain differentiation. Additionally, strategic collaborations, licensing deals, and regional market expansions are shaping competitive positioning, with stakeholders striving to balance clinical efficacy, safety, and cost-effectiveness amid evolving treatment guidelines.

Key Developments:

- In January 2025, Coherus BioSciences' Phase 2 clinical trial showed a 38% total response rate in unresectable hepatocellular carcinoma patients, supporting continued evaluation of casdozokitug with other therapies.

- In December 2024, Nivolumab was under clinical development by Bristol-Myers Squibb and was in Phase II for Bile Duct Cancer (Cholangiocarcinoma). The Phase II drugs for Bile Duct Cancer (Cholangiocarcinoma) had a 30% phase transition success rate (PTSR) indication benchmark for progressing into Phase III.

- In December 2024, Teva Pharmaceuticals and Sanofi announced that the Phase 2b RELIEVE UCCD study, which investigated duvakitug, a human IgG1-λ2 monoclonal antibody targeting TL1A, had met its primary endpoints in treating ulcerative colitis and Crohn's disease.

- In November 2024, Jazz Pharmaceuticals received FDA approval for Ziihera, a dual HER2-targeted bispecific antibody, for treating adults with HER2-positive biliary tract cancer. The drug has shown efficacy in 62 patients and is currently in a Phase 3 trial.

Companies Covered in Bile Duct Cancer Treatment Market

- Merck & Co., Inc.

- AstraZeneca PLC

- Incyte Corporation

- Taiho Pharmaceutical

- F. Hoffmann-La Roche Ltd

- Eisai Co., Ltd

- Pfizer Inc.

- Bristol-Myers Squibb

- Servier Pharmaceuticals

- Agios Pharmaceuticals

- Zymeworks Inc.

- BeiGene, Ltd.

- Eli Lilly and Company

- Novartis AG

- Celgene Corporation

Frequently Asked Questions

The global bile duct cancer treatment market is expected to be valued at US$ 4.1 billion in 2026, and is projected to reach about US$ 7.3 billion by 2033, reflecting a robust 8.6% CAGR during 2026 - 2033.

Key growth drivers include breakthroughs in precision oncology, such as FGFR2 and IDH1-targeted therapies with meaningful response and PFS benefits, and expanding immunotherapy use, where regimens like durvalumab or pembrolizumab plus chemotherapy have demonstrated statistically significant OS improvements over chemotherapy alone in large phase III trials.

North America currently leads holding roughly 37% share, supported by high oncology spending, rapid incorporation of FDA-approved targeted and immunotherapeutic agents, widespread availability of NGS-based profiling, and treatment concentration in NCI-designated comprehensive cancer centers.

The most significant opportunity lies in expanding precision medicine and immunotherapy, including biomarker-guided combinations targeting FGFR2, IDH1, and HER2, wider adoption of NGS across regions, and deeper penetration of immuno-oncology regimens into first-line, adjuvant, and subsequent treatment settings as evidence and access continue to improve.

Major players include Merck & Co., Inc., AstraZeneca PLC, Incyte Corporation, Taiho Pharmaceutical, F. Hoffmann-La Roche Ltd., Eisai Co., Ltd., Pfizer Inc., Bristol-Myers Squibb, Servier Pharmaceuticals, Agios Pharmaceuticals, Zymeworks Inc., and BeiGene, Ltd., along with other global and regional companies focusing on targeted and immuno-oncology strategies in cholangiocarcinoma.