- Pharmaceuticals

- Precision Oncology Market

Precision Oncology Market Size, Share, Growth, and Regional Forecast, 2026 to 2033

Precision Oncology Market by Treatment Type (Therapeutics and Diagnostics), Cancer Type (Breast cancer, Lung cancer, Hematologic, Colorectal Cancer, Prostate Cancer, Cervical Cancer, and Others), Technology (Next-Generation Sequencing (NGS), Polymerase Chain Reaction (PCR), In Situ Hybridization (ISH/FISH), Immunohistochemistry (IHC), Gene Expression Profiling, and Bioinformatics & AI-based Analytics), Therapy Type (Targeted Therapy, Immunotherapy, Chemotherapy, Hormone Therapy, and Combination Therapy), End-user, and Regional Analysis from 2026 to 2033

Precision Oncology Market Share and Trend Analysis

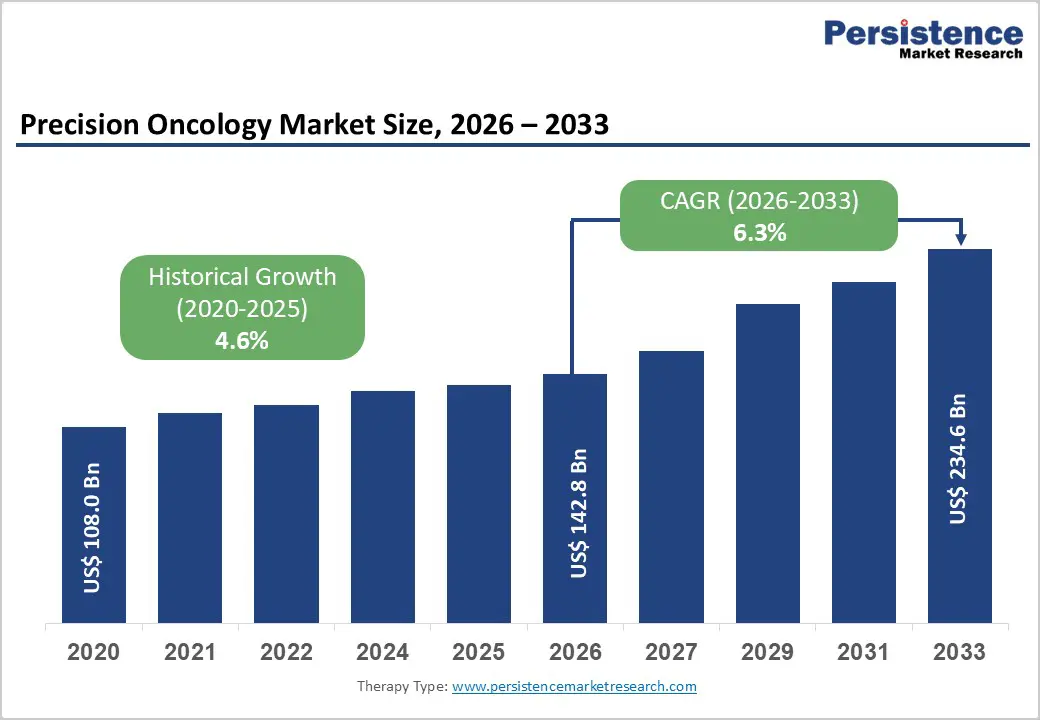

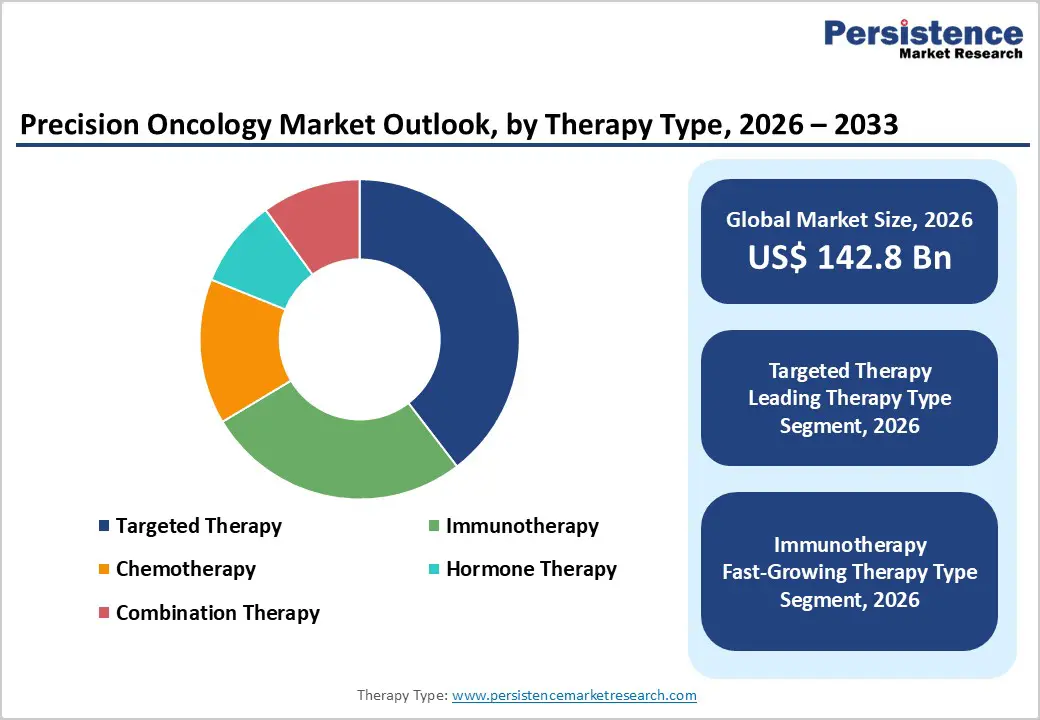

The global precision oncology market size is estimated to grow from US$ 142.8 Bn in 2026 to US$ 234.6 Bn by 2033. The market is projected to record a CAGR of 6.3% during the forecast period from 2026 to 2033.

Incidence of complex cancers and the growing shift toward individualized treatment strategies are significantly accelerating the adoption of precision oncology across global healthcare systems. Instead of relying on conventional one-size-fits-all therapies, clinicians are increasingly utilizing molecular profiling and genomic insights to guide treatment decisions. Technologies such as next-generation sequencing, liquid biopsy, and advanced bioinformatics platforms are enabling accurate identification of tumor-specific mutations, improving therapeutic targeting and patient outcomes. The expanding pipeline of targeted drugs and immunotherapies, along with the parallel development of companion diagnostics, is strengthening clinical adoption. Pharmaceutical and biotechnology firms are actively investing in biomarker-driven drug development, while healthcare providers are integrating precision diagnostics into oncology care pathways.

Additionally, the growing availability of real-world evidence and digital health tools is supporting better disease monitoring and treatment optimization. Emerging economies are also witnessing gradual adoption due to improving healthcare infrastructure and rising awareness of personalized medicine. As a result, precision oncology is transitioning from a niche approach to a mainstream component of cancer management, supported by continuous innovation and strategic collaborations across diagnostics, therapeutics, and data analytics ecosystems.

Key Industry Highlights:

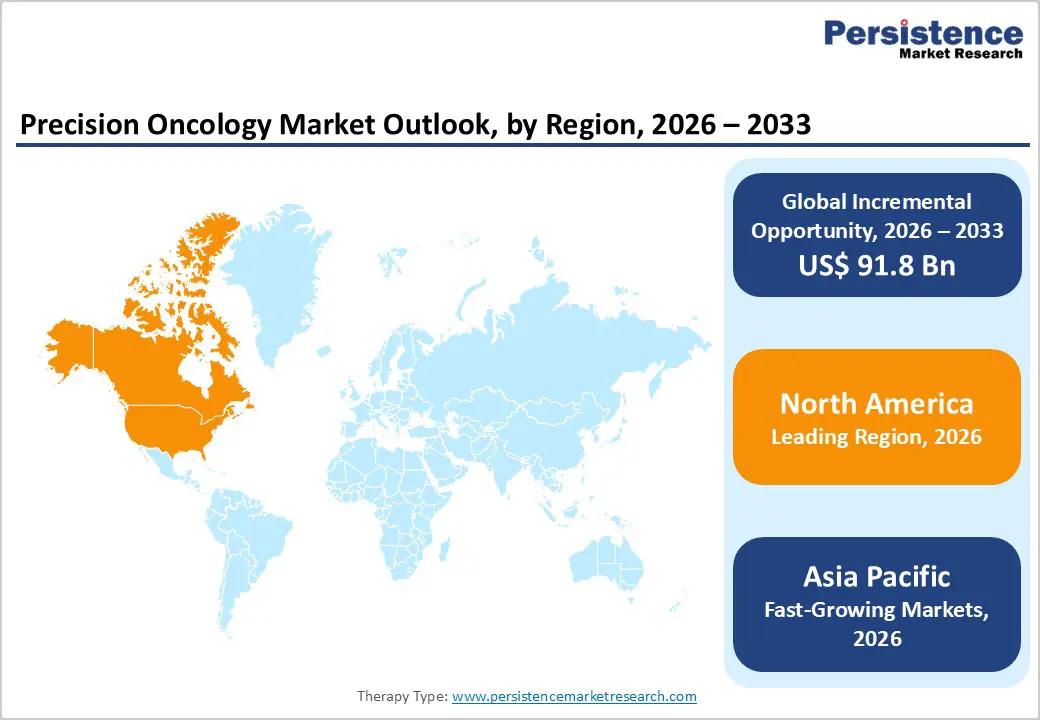

- Leading Region: North America accounts for 46.7% of the global market, supported by strong genomic research capabilities, high adoption of advanced cancer diagnostics, robust reimbursement frameworks, and the presence of leading oncology-focused pharmaceutical and biotechnology companies.

- Fastest-Growing Region: Asia Pacific is registering the fastest expansion, driven by increasing cancer prevalence, improving access to molecular diagnostics, rising healthcare expenditure, and government initiatives promoting precision medicine and genomic research.

- Leading Type Segment: Therapeutics lead with a 56.8% share, attributed to the strong uptake of targeted therapies and immuno-oncology drugs that are increasingly guided by biomarker identification.

- Fastest-Growing Type Segment: Diagnostics are witnessing accelerated growth due to rising demand for early detection tools, liquid biopsy technologies, and comprehensive genomic profiling solutions that support treatment selection..

- Leading Cancer Type Segment: Breast cancer contributes 38.7% of total demand, reflecting high screening rates, extensive biomarker availability (such as HER2 and BRCA), and widespread adoption of targeted treatment approaches.

- Fastest-Growing Cancer Type Segment: Prostate cancer is expanding at a notable pace, supported by increasing use of genomic testing, growing awareness of personalized therapies, and advancements in precision-based treatment protocols.

| Key Insights | Details |

|---|---|

| Precision Oncology Market Size (2026E) | US$ 142.8 Bn |

| Market Value Forecast (2033F) | US$ 234.6 Bn |

| Projected Growth (CAGR 2026 to 2033) | 6.3% |

| Historical Market Growth (CAGR 2020 to 2025) | 4.6% |

Market Dynamics

Driver - Rising Cancer Burden and Accelerating Adoption of Biomarker-Guided Therapies

The increasing global incidence of cancer is fundamentally reshaping treatment paradigms, driving strong demand for precision oncology approaches. As tumor heterogeneity becomes better understood, clinicians are shifting away from generalized chemotherapy toward biomarker-driven therapies that target specific genetic mutations and molecular pathways. Advances in genomic sequencing, particularly next-generation sequencing (NGS), are enabling comprehensive tumor profiling, allowing physicians to identify actionable mutations and tailor treatments accordingly. This has significantly improved treatment efficacy, reduced adverse effects, and enhanced patient outcomes, especially in complex cancers such as lung, breast, and hematologic malignancies.

Additionally, regulatory agencies are increasingly approving targeted therapies and companion diagnostics in tandem, accelerating the integration of precision medicine into clinical workflows. The expansion of liquid biopsy technologies is further supporting early detection, disease monitoring, and therapy selection through minimally invasive methods. Additionally, growing investments from pharmaceutical and biotechnology companies in precision drug development are strengthening the therapeutic pipeline. With healthcare systems prioritizing personalized treatment strategies and value-based care models, the adoption of biomarker-guided therapies is expected to expand rapidly, positioning precision oncology as a central pillar in modern cancer management.

Restraints - High Cost of Genomic Testing and Limited Accessibility Across Healthcare Systems

Despite strong clinical potential, the widespread adoption of precision oncology is constrained by the high cost associated with genomic testing, targeted therapies, and advanced diagnostic platforms. Comprehensive genomic profiling, which is essential for identifying actionable mutations, often requires sophisticated sequencing technologies, specialized laboratory infrastructure, and skilled personnel, resulting in significant cost burdens. In many low- and middle-income regions, limited reimbursement frameworks and inadequate healthcare funding further restrict patient access to these advanced diagnostics and therapies.

Additionally, the complexity of interpreting genomic data presents operational challenges. Clinicians require specialized training and decision-support systems to translate molecular insights into effective treatment strategies. Variability in regulatory pathways across countries also complicates the approval and commercialization of companion diagnostics and targeted therapies, leading to delays in market access. Furthermore, integration of genomic data into existing healthcare IT systems remains fragmented, limiting real-time clinical application. Concerns regarding data privacy, storage, and interoperability add another layer of complexity. These economic, infrastructural, and regulatory barriers collectively hinder the broader penetration of precision oncology, particularly in resource-constrained healthcare environments.

Opportunity - Expansion of Multi-Omics Integration and AI-Driven Clinical Decision Support

The convergence of multi-omics technologies and artificial intelligence is unlocking transformative opportunities in precision oncology. Beyond genomics, the integration of transcriptomics, proteomics, and metabolomics is enabling a more comprehensive understanding of tumor biology, leading to highly personalized treatment strategies. These multi-dimensional datasets provide deeper insights into disease progression, drug resistance mechanisms, and patient-specific therapeutic responses. Artificial intelligence and machine learning algorithms are increasingly being deployed to analyze complex biological data, identify novel biomarkers, and optimize treatment selection. AI-powered clinical decision support systems are helping oncologists interpret vast genomic datasets and match patients with the most effective targeted therapies or clinical trials.

Moreover, advancements in real-world evidence generation and digital health platforms are enhancing longitudinal patient monitoring and treatment optimization. The growing adoption of precision oncology in emerging applications such as immuno-oncology, cell and gene therapies, and early cancer detection further expands its market potential. Strategic collaborations between pharmaceutical companies, diagnostic firms, and technology providers are accelerating innovation and commercialization. As healthcare systems continue to embrace data-driven medicine, the integration of multi-omics and AI is expected to significantly enhance the scalability, accuracy, and clinical impact of precision oncology solutions.

Category-wise Analysis

By Treatment Type

Therapeutics are projected to remain the dominant product category in the global precision oncology market in 2026, representing 61.4% of total revenue. Their leadership stems from the rapid clinical adoption of molecularly targeted agents, checkpoint inhibitors, antibody-drug conjugates, and cell & gene therapies tailored to individual tumor biology. Oncologists increasingly prefer therapeutics that are guided by companion diagnostic results, enabling precise patient selection and significantly improved response rates compared to conventional chemotherapy. The growing number of FDA and EMA approvals for biomarker-driven drugs continues to expand the addressable patient population. Advances in multi-omics profiling and real-world evidence generation have further strengthened the clinical and commercial case for precision therapeutics. As pharmaceutical companies deepen investment in oncology pipelines and accelerate the co-development of drugs alongside diagnostic partners, therapeutics are expected to maintain commanding revenue leadership throughout the forecast period.

By Therapy Type

The targeted therapy segment is expected to account for the largest share of the precision oncology market in 2026, contributing 39.6% of overall revenue. Unlike broad-spectrum chemotherapy, targeted agents act on specific genetic alterations, such as EGFR mutations, HER2 amplification, ALK fusions, BRAF V600E, and KRAS G12C identified through genomic profiling, making therapy selection data-driven rather than empirical. The pipeline of next-generation tyrosine kinase inhibitors, PARP inhibitors, and bispecific antibodies continues to expand, creating new treatment options across lung, breast, colorectal, and prostate cancers. Regulatory agencies have fast-tracked approvals for several tumor-agnostic indications, extending the reach of targeted agents beyond single cancer types. Growing clinician awareness of molecular subtyping, combined with declining NGS costs, has accelerated biomarker testing uptake in community oncology settings. As treatment guidelines increasingly mandate genomic profiling prior to therapy initiation, demand for targeted therapies is set to grow consistently across both developed and emerging healthcare markets.

By End-user Insights

Hospitals are expected to represent the largest end-user group in 2026, capturing 68.3% of total market revenue. As the primary site of cancer diagnosis, multidisciplinary tumor board deliberation, and treatment administration, hospitals are uniquely positioned to deploy the full spectrum of precision oncology capabilities from NGS-based tumor profiling and liquid biopsy to targeted drug infusion and immunotherapy monitoring. Large academic medical centers and comprehensive cancer centers invest heavily in sequencing infrastructure, digital pathology platforms, and AI-assisted clinical decision support tools, enabling seamless integration of molecular insights into treatment protocols. Established relationships with diagnostic laboratories and pharmaceutical companies further enable hospitals to access companion diagnostics and investigational therapies through clinical trial networks. As reimbursement frameworks for genomic testing improve across major markets and precision oncology becomes standard of care across more cancer types, hospitals will continue to anchor end-user demand, consolidating their dominance over outpatient clinics and standalone diagnostic centers.

Region-wise Insights

North America Precision Oncology Market Trends

North America is anticipated to hold the largest share of the global precision oncology market in 2026, accounting for 46.7% of total market value, with the United States serving as the primary growth engine. The region's dominance is underpinned by a highly developed oncology ecosystem comprising world-class cancer research institutions, extensive clinical trial networks, and a robust regulatory framework that actively encourages biomarker-driven drug development. The FDA's accelerated approval pathway and breakthrough therapy designation have enabled rapid commercialization of targeted therapies and companion diagnostics, giving the U.S. a significant first-mover advantage in translating genomic discoveries into approved treatments.

Private and public investment in precision medicine infrastructure, including national genomic databases and hospital-based sequencing programs, continues to rise. Major pharmaceutical and diagnostic companies headquartered in the region maintain significant R&D pipelines focused on next-generation sequencing, liquid biopsy, and AI-powered oncology platforms. Favorable reimbursement policies for molecular testing and strong physician adoption of biomarker-guided therapy protocols further reinforce North America's commanding position in the global market.

Europe Precision Oncology Market Trends

Europe represents a well-established and steadily evolving precision oncology market, shaped by rigorous regulatory standards, a strong academic research base, and growing cross-border collaboration in cancer genomics. Key markets including Germany, the United Kingdom, France, Italy, and the Netherlands are driving regional demand through their advanced hospital systems, specialized oncology centers, and proactive national cancer genomics initiatives such as the UK's 100,000 Genomes Project and France's Plan Cancer. European regulators have made significant strides in harmonizing companion diagnostic approval pathways alongside therapeutic authorizations, reducing time-to-market for precision medicine combinations. Regional biotechnology firms and academic consortia are actively engaged in biomarker discovery, clinical validation, and real-world evidence generation, enriching the pipeline of precision oncology innovations.

Additionally, Europe's emphasis on health data interoperability and pan-European research networks including the Innovative Medicines Initiative supports large-scale molecular epidemiology studies that inform treatment guideline updates. Sustained government funding and expanding patient access programs are expected to maintain steady long-term growth across the region.

Asia Pacific Precision Oncology Market Trends

Asia Pacific is projected to be the fastest-growing regional market for precision oncology, expected to expand at a CAGR of approximately 8.5% between 2026 and 2033, driven by a confluence of epidemiological, economic, and policy-level forces. The region carries a disproportionately high cancer burden particularly lung, gastric, liver, and colorectal cancers creating an urgent clinical need for more precise and effective treatment strategies. China, India, Japan, and South Korea are at the forefront of regional growth, each investing aggressively in genomic medicine infrastructure, local NGS manufacturing capabilities, and hospital-based molecular pathology networks. Governments across the region have launched national precision medicine initiatives including China's Precision Medicine Initiative and South Korea's national genomics program that are accelerating biomarker research and clinical integration.

The rapid expansion of private oncology hospital chains and diagnostic laboratory networks in India and Southeast Asia is further broadening patient access to molecular testing. Strategic partnerships between global pharmaceutical companies and regional healthcare providers are enabling faster technology transfer and clinical trial execution, positioning Asia Pacific as the most dynamic and high-potential growth market in global precision oncology.

Market Competitive Landscape

The global precision oncology market is highly competitive, with strong participation from Thermo Fisher Scientific Inc., Svar Life Science AB, F. Hoffmann-La Roche Ltd., Foundation Medicine, Inc., and Illumina, Inc. These companies leverage advanced genomic profiling technologies, large-scale sequencing capabilities, and global diagnostic distribution networks to strengthen their market presence while enhancing biomarker discovery, companion diagnostic development, and targeted therapy performance.

Growing demand for personalized cancer treatment, liquid biopsy solutions, and AI-powered diagnostics is accelerating product innovation. Manufacturers are focusing on expanding NGS capacity, improving bioinformatics capabilities, strengthening regulatory compliance, and forming strategic collaborations while increasing R&D investments to develop high-value companion diagnostics, multi-cancer early detection tests, and specialty precision oncology platforms.

Key Industry Developments:

- In March 2026, IDEAYA Biosciences, Inc. announced upcoming poster presentations at the American Association for Cancer Research Annual Meeting. The presentations will showcase preclinical data from three pipeline candidates IDE034 (bi-specific TOP1 ADC), IDE574 (KAT6/7 inhibitor), and IDE892 (PRMT5 inhibitor). All three are currently in Phase 1 trials evaluating safety, pharmacokinetics, and efficacy across multiple solid tumors.

- In March 2026, precision oncology company Lucence, in collaboration with Diagnostics Development Hub, Agency for Science, Technology and Research, and National Cancer Centre Singapore, launched UNITED 2.0, a S$6 million initiative focused on developing a next-generation, clinical-grade cancer profiling test to advance precision diagnostics.

- In September 2025, Illumina Inc. partnered with multiple global pharmaceutical firms to develop companion diagnostics using its TruSight™ Oncology (TSO) comprehensive genomic profiling platform. The initiative emphasizes expanding tumor-agnostic CDx claims and improving global access to standardized precision oncology testing, with a particular focus on detecting KRAS mutations associated with cancer progression.

Companies Covered in Precision Oncology Market

- Thermo Fisher Scientific Inc.

- Svar Life Science AB

- F. Hoffmann-La Roche Ltd.

- Foundation Medicine, Inc.

- Illumina, Inc.

- Guardant Health, Inc.

- QIAGEN N.V.

- Natera, Inc.

- Myriad Genetics, Inc.

- Exact Sciences Corporation

- NeoGenomics, Inc.

- Tempus AI, Inc.

- Caris Life Sciences

- Agilent Technologies, Inc.

- Bio-Rad Laboratories, Inc.

- Others

Frequently Asked Questions

The global precision oncology market is projected to be valued at US$ 142.8 Bn in 2026.

Rising cancer prevalence, expanding biomarker-driven therapies, falling NGS costs, growing companion diagnostics adoption, and increasing regulatory support for targeted and immuno-oncology treatments.

The global precision oncology market is poised to witness a CAGR of 6.3 % between 2026 and 2033.

Liquid biopsy expansion, multi-cancer early detection (MCED) tests, AI-powered diagnostics, tumor-agnostic drug approvals, and rapid precision oncology infrastructure growth across Asia Pacific and other emerging markets.

Thermo Fisher Scientific Inc., Svar Life Science AB, F. Hoffmann-La Roche Ltd., Foundation Medicine, Inc., and Illumina, Inc., are some of the key players in the precision oncology market.