- Baby Care & Accessories

- Baby Wipes Market

Baby Wipes Market Size, Share, Trends, and Growth Forecast, 2025 - 2032

Baby Wipes Market by Product Type (Wet Wipes, Dry Wipes), Distribution Channel (Online Retail, Offline Retail), and Regional Analysis for 2025 - 2032

Baby Wipes Market Size and Trends Analysis

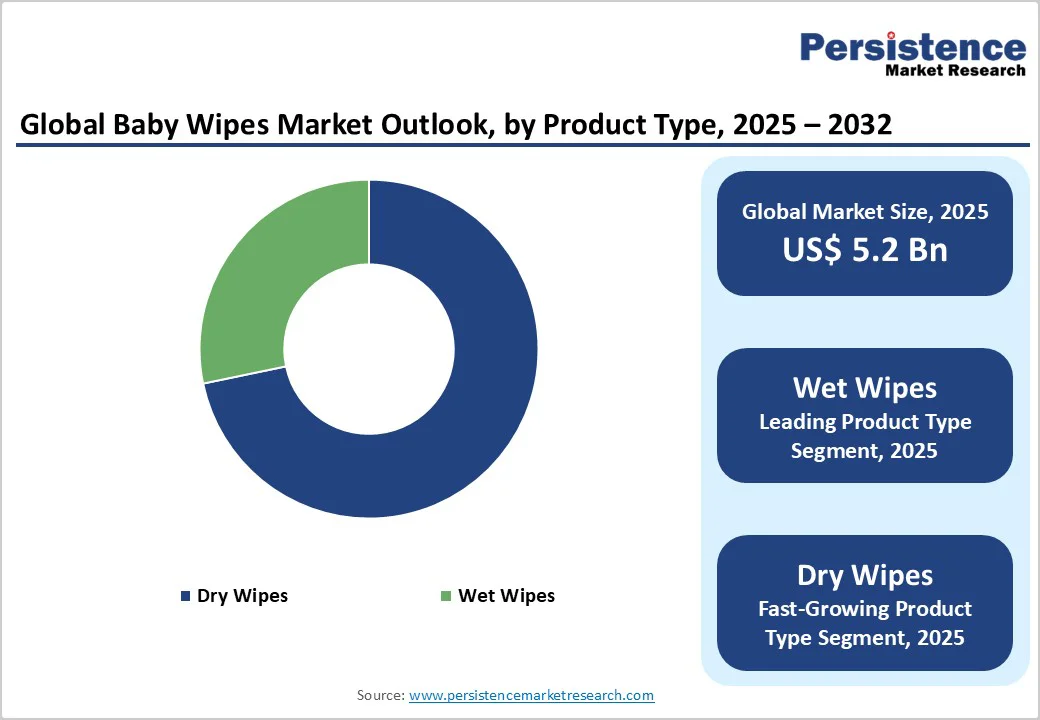

The global baby wipes market size is likely to value at US$ 5.5 billion in 2025 and is projected to reach US$ 8.2 billion by 2032, growing at a CAGR of 5.8% between 2025 and 2032.

This growth trajectory is underpinned by rising parental awareness of infant hygiene, increasing disposable incomes, and demographic shifts in emerging economies, which collectively drive sustained demand for convenient and safe baby care solutions.

The expansion of e-commerce platforms and subscription-based models has also enhanced accessibility and convenience, particularly for time-constrained parents, reinforcing market momentum across both developed and developing regions.

Key Industry Highlights:

- The wet wipes segment is the leading product category, accounting for 86.4% market share in 2025 due to convenience, superior cleansing, and skin-soothing properties.

- Dry wipes are the fastest-growing category, driven by eco-friendly potential, versatility, and longer shelf life.

- The offline retail channel dominates with 73.4% market share, led by hypermarkets and supermarkets, while online retail is the fastest-growing segment due to convenience and subscription models.

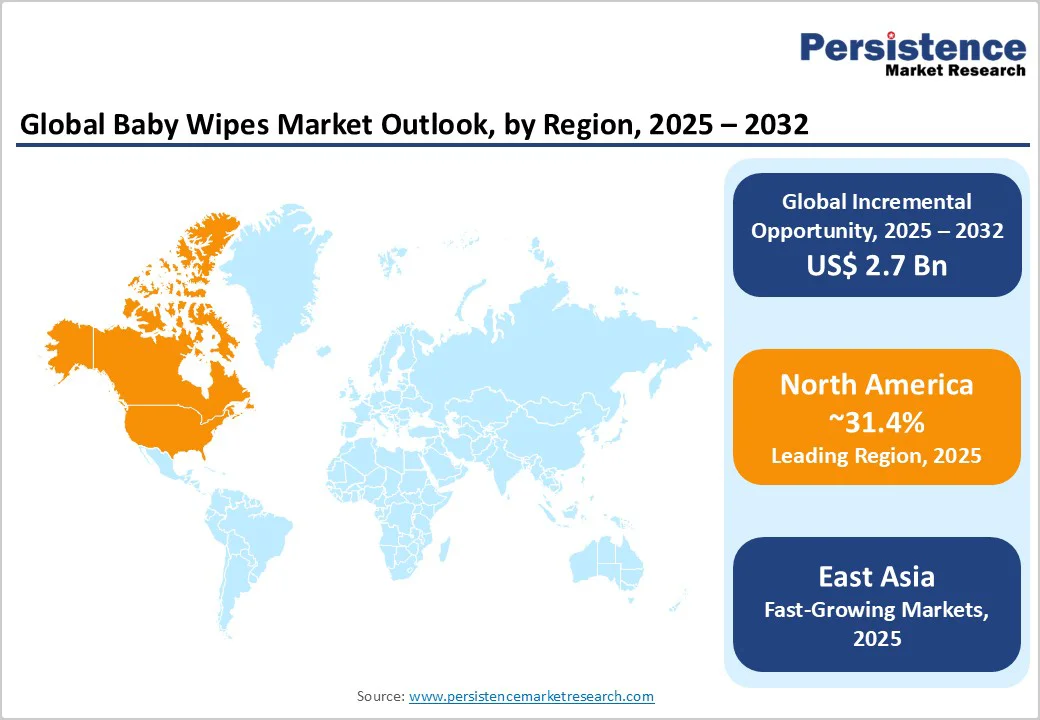

- North America holds the largest regional share at 31.4%, driven by high disposable incomes, premium product demand, and regulatory support for child health.

- Europe accounts for 25.6% of the market, with growth shaped by environmental regulations, high eco-consciousness, and demand for biodegradable wipes.

- East Asia represents 20% of the market, experiencing strong growth from urbanization, rising middle-class income, and expanding e-commerce platforms.

- The global market is oligopolistic, dominated by Johnson & Johnson, Kimberly-Clark, Procter & Gamble, Unicharm, Hengan, and Himalaya, with regional players creating localised competition.

| Key Insights | Details |

|---|---|

| Baby Wipes Market Size (2025E) | US$ 5.5 Bn |

| Market Value Forecast (2032F) | US$ 8.2 Bn |

| Projected Growth (CAGR 2025 to 2032) | 5.8% |

| Historical Market Growth (CAGR 2019 to 2024) | 5.2% |

Market Dynamics

Drivers - Parental Awareness of Infant Hygiene and Health

The heightened focus on infant hygiene and health among modern parents is a pivotal driver of market expansion. Today’s caregivers, particularly millennial and Gen Z parents, actively research product ingredients, favouring formulations free from synthetic chemicals, parabens, sulfates, and fragrances.

This shift is supported by pediatric recommendations and public health campaigns emphasizing the importance of gentle cleansing to prevent skin conditions such as diaper dermatitis, which affects approximately 14.9% of infants in countries like Germany.

The demand for dermatologically tested, hypoallergenic, and alcohol-free wipes has surged, with brands like Johnson’s Baby and Pampers Aqua Pure capitalising on this trend by offering products with 99% water content and natural extracts such as aloe vera and chamomile. This consumer behaviour is not only health-driven but also reflects a broader wellness-oriented parenting philosophy, where product safety and skin compatibility are paramount.

The market impact of this trend is evident in the premiumization of product lines, with companies launching eco-conscious and organic variants to capture value-seeking, health-aware segments. For instance, Cugo launched biodegradable wipes made from 100% plant-based materials in May 2024, while Ginni Filaments introduced “paaniwipes” in India, featuring 99.9% water and aloe vera for maximum skin gentleness.

These innovations command higher price points and margins, contributing to overall market growth. Moreover, digital platforms and social media have amplified consumer education, enabling brands to engage directly with parents through influencer marketing and virtual parenting communities, thereby reinforcing trust and brand loyalty.

Demographic Growth in Emerging Economies

The expanding infant population in developing regions is a significant driver of demand for baby wipes. Countries in the Asia-Pacific, Latin America, and Africa are experiencing urbanisation and rising middle-class populations, which correlate with increased spending on infant care products.

In India, for example, despite a slight decline in birth rate to 16.55 per 1,000 population in 2025, the absolute number of births remains substantial, supporting sustained demand for hygiene essentials. In these regions, access to clean water and sanitation can be inconsistent, making disposable wipes a practical and hygienic alternative for daily infant care.

The growing participation of women in the workforce has led to dual-income households with less time for traditional cleaning routines, further boosting the appeal of convenient, on-the-go solutions like baby wipes. This demographic shift is compounded by rising disposable incomes and improved retail infrastructure, enabling greater product penetration.

Governments and NGOs in countries such as India and Brazil are also promoting child health initiatives, indirectly supporting market growth. For instance, the U.S. Child Care and Development Block Grant allocated USD 8.3 billion in subsidies in 2019, enhancing the affordability of childcare products.

Multinational and local manufacturers are expanding production and distribution networks in these high-growth markets. Kimberly-Clark’s USD 25 million investment in its Singapore facility in 2019 to double export capacity exemplifies this strategic focus on emerging economies.

Restraint - Environmental Concerns Over Non-Biodegradable Wipes

A major structural challenge facing the market is the environmental impact of conventional baby wipes, which are predominantly made from synthetic polymers like polyethene and polypropylene that do not degrade in landfills. It is estimated that over 100 billion non-biodegradable wipes enter municipal waste streams annually, contributing to microplastic pollution and long-term ecological damage.

Regulatory bodies in Europe and North America have responded with stricter guidelines on single-use plastics, increasing compliance costs and reputational risks for manufacturers. For example, the UK’s ban on plastic-containing wet wipes took effect in 2025, compelling brands to reformulate products with biodegradable materials.

This regulatory pressure, combined with growing consumer activism, limits the scalability of traditional wipe formulations and necessitates costly R&D investments in sustainable alternatives.

The financial risk is twofold: first, biodegradable wipes are more expensive to produce, which can deter price-sensitive consumers, particularly in developing markets. Second, greenwashing allegations can damage brand credibility if claims are not substantiated, leading to consumer distrust and potential legal repercussions.

As a result, companies face a delicate balance between innovation, cost management, and environmental responsibility, which constrains profit margins and slows market penetration in eco-conscious segments.

Opportunity - Development of Biodegradable and Sustainable Wipe Formulations

The transition toward sustainable materials presents a transformative opportunity for market leaders. Consumers, especially in North America and Europe, are increasingly demanding eco-friendly alternatives, creating a fast-growing niche for wipes made from bamboo, organic cotton, and wood pulp. These materials decompose within months, significantly reducing environmental impact.

Market research indicates that the biodegradable wipes segment is expanding at a significant CAGR, outpacing the overall market. Companies like Suominen Corporation have introduced plant-based non-woven materials such as Biolace Bamboo, enabling brands to develop fully compostable wipes. This innovation not only meets regulatory requirements but also strengthens brand's positioning as environmentally responsible.

Expansion of E-Commerce and Subscription Models

The digital transformation of retail offers a powerful growth lever, particularly through e-commerce platforms and subscription services. Online channels provide unparalleled convenience, allowing parents to purchase wipes in bulk, compare products, read reviews, and receive doorstep delivery-critical for time-pressed caregivers.

The rise of social commerce, influencer endorsements, and targeted digital advertising has further amplified product discovery and conversion rates. Subscription models, offered by brands like The Honest Company and Amazon Family, ensure recurring revenue and customer retention by automating replenishment.

This shift is especially impactful in urban centres across Asia-Pacific and Latin America, where e-commerce penetration is rising rapidly. Platforms like FirstCry in India and JD.com in China have become key distribution channels, enabling both global and local brands to scale efficiently. The data-driven nature of online retail also allows for personalised marketing, dynamic pricing, and inventory optimisation, enhancing operational efficiency and profitability.

Category-wise Analysis

Product Type Insights

The wet wipes segment is the dominant category, accounting for approximately 86.4% of the market share in 2025. This leadership is attributed to their immediate usability, superior cleansing efficacy, and ability to hydrate and soothe sensitive infant skin.

Enriched with ingredients such as aloe vera, vitamin E, and chamomile, wet wipes provide a spa-like cleaning experience that dry alternatives cannot replicate. Their pre-moistened format ensures consistent performance, making them the preferred choice for diaper changes, mealtime clean-ups, and travel.

Major brands such as Pampers and Huggies have reinforced this dominance through continuous innovation in texture, thickness, and formulation, including the launch of Pampers Pure Protection and Huggies Natural Care lines.

The dry wipes segment is the fastest-growing, driven by their versatility, longer shelf life, and eco-friendly potential [user-provided data]. Dry wipes can be used with water or cleansing solutions, reducing plastic and liquid waste, and are increasingly marketed as sustainable alternatives.

Distribution Channel Insights

The offline retail segment, particularly hypermarkets and supermarkets, holds a leading 73.4% market share in 2025. This dominance stems from the one-stop shopping convenience, in-store product visibility, and the ability to physically assess quality and packaging. Supermarkets frequently offer promotions, bundle deals, and loyalty programs that incentivise bulk purchases, a common behaviour among parents stocking up on essential baby care items.

The presence of well-known brands in high-traffic retail environments builds consumer trust and drives impulse buying. Pharmacies and drugstores serve as trusted points of sale, especially for hypoallergenic and medicated wipes recommended by healthcare professionals.

The online retail channel is the fastest-growing segment, fueled by the convenience of home delivery, 24/7 availability, and access to a wider product range, including niche and international brands. E-commerce platforms enable detailed product comparisons, customer reviews, and subscription services that enhance user experience and retention.

Regional Insights and Trends

North America Baby Wipes Market Trends

North America holds a 31.4% share of the global baby wipes market, the largest regional segment, driven by high disposable incomes, advanced retail infrastructure, and strong consumer awareness of infant hygiene.

The U.S. market, in particular, is characterised by a preference for premium, natural, and organic products, with brands like The Honest Company and WaterWipes gaining traction. Government support through childcare subsidies, such as the USD 8.3 billion allocated by the CCDBG in 2019, enhances affordability and market access.

The region’s regulatory environment, including FDA guidelines and state-level plastic bans, pushes manufacturers toward safer, biodegradable formulations.

The competitive landscape is oligopolistic, dominated by Procter & Gamble, Kimberly-Clark, and Johnson & Johnson, which leverage extensive R&D and marketing budgets to maintain leadership. Investment trends show a focus on sustainable packaging and digital engagement, with brands launching refillable pouches and virtual parenting communities.

Europe Baby Wipes Market Trends

Europe accounts for 25.6% of the global market, with growth shaped by stringent chemical regulations and high environmental consciousness. The EU’s REACH and CLP regulations restrict the use of hazardous substances in baby care products, compelling manufacturers to adopt natural, fragrance-free, and dermatologically tested formulations.

Countries such as Germany, the UK, and France lead in demand for biodegradable wipes, supported by public awareness campaigns and eco-labelling schemes.

The market is highly competitive, with local players such as Beiersdorf AG and Codi Group challenging global giants through innovation and regional marketing. In 2020, WaterWipes launched the Early Day Club, a virtual parent education platform, to strengthen brand loyalty.

Investment is focused on sustainable materials and circular economy models, such as compostable packaging and take-back programs. Despite slower growth compared to Asia-Pacific, Europe remains a high-value market due to premium pricing and brand loyalty..

East Asia Baby Wipes Market Trends

East Asia represents 20% of the global market, with robust growth driven by urbanisation, rising middle-class incomes, and increasing awareness of infant hygiene in countries like China, Japan, and India. China’s expanding e-commerce ecosystem, led by platforms like JD.com and Alibaba, has revolutionized distribution, enabling rapid market penetration.

Local innovations, such as Ginni Filaments’ “paaniwipes,” cater to the demand for ultra-gentle, minimal-ingredient products. Regulatory frameworks are evolving, with India’s Bureau of Indian Standards (BIS) developing safety norms for baby care products.

The competitive landscape is fragmented, with both multinational brands and regional players vying for share through localised marketing and affordable pricing. Investment is flowing into manufacturing capacity and digital marketing, positioning East Asia as a key growth engine for the global market.

Competitive Landscape

The global Baby Wipes market is characterised by strong competition among leading players such as Johnson & Johnson, Kimberly-Clark (Huggies), Procter & Gamble (Pampers), Unicharm, Hengan, and Himalaya.

These companies dominate the market through well-established brands, extensive distribution networks, and large-scale production capabilities. Private label and regional players add competitive pressure by offering affordable alternatives tailored to local preferences.

Product innovation is a key focus area, with major brands emphasising natural ingredients, skin-friendly formulations, and sustainable packaging solutions to appeal to environmentally conscious consumers.

The market structure is broadly oligopolistic, with a few global companies holding substantial market shares, though regional fragmentation persists due to localised demand patterns. Overall, competition is driven by brand differentiation, pricing strategies, and product innovation aimed at both premium and mass-market segments.

Key Industry Developments:

- In August 2025, Novel Tissues Pvt. Ltd., an emerging Indian hygiene manufacturer, strengthened its position in the baby wipes market with its dermatologist-tested, ISO and GMP-certified product range. The company introduced India’s first Goat Milk Baby Wipes alongside Aloe Vera with Chamomile and 99% Pure Water variants, catering to diverse skin needs. With manufacturing units in Mysuru and Manesar, Novel has built one of India’s largest baby hygiene production ecosystems, emphasising safety, purity, and affordability.

- In December 2024, 3i Group plc announced a €145 million investment in WaterWipes UC, a premium wet wipes brand known for its 99.9% water-based products made from only two natural ingredients. The investment supports WaterWipes’ global growth, leveraging its differentiation in skin safety, healthcare endorsements, and allergy accreditations. Founder Edward McCloskey retains a significant minority stake, while the existing leadership, led by CEO Paul Heeringa, continues to reinvest and partner with 3i.

Companies Covered in Baby Wipes Market

- Johnson & Johnson Services, Inc.

- Kimberly-Clark (Huggies)

- Procter & Gamble (Pampers)

- Unicharm Corporation

- Hengan International Group

- Pigeon Corporation

- Himalaya Wellness Company

- Cotton Babies, Inc.

- Farlin-Global

- BABISIL

Frequently Asked Questions

The global baby wipes market is projected to be valued at US$ 5.5 Bn in 2025.

The wet wipes segment is expected to hold around 86.4% market share by product type in 2025, driven by rising demand for convenient, hygienic, and dermatologically tested baby care products.

The baby wipes market is expected to witness a CAGR of 5.8% from 2025 to 2032.

The baby wipes market is driven by rising parental awareness of infant hygiene, demand for safe and premium products, and demographic growth in emerging economies.

Key market opportunities in the Baby Wipes market include the development of biodegradable, sustainable formulations and the expansion of e-commerce and subscription-based sales channels.

The key market players in the Baby Wipes market include Johnson & Johnson Services, Inc., Kimberly-Clark (Huggies), Procter & Gamble (Pampers), Unicharm Corporation, and Hengan International Group.