- Baby Care & Accessories

- Baby Powder Market

Baby Powder Market Size, Share, and Growth Forecast, 2026 – 2033

Baby Powder Market by Ingredient Type (Talc-based, Talc-free), Packaging Type (Plastic Bottles, Sustainable/Eco-tins, Sachet/Pouches, Others), Distribution Channel (Offline, Online), and Regional Analysis 2026 – 2033

Baby Powder Market Size and Trends Analysis

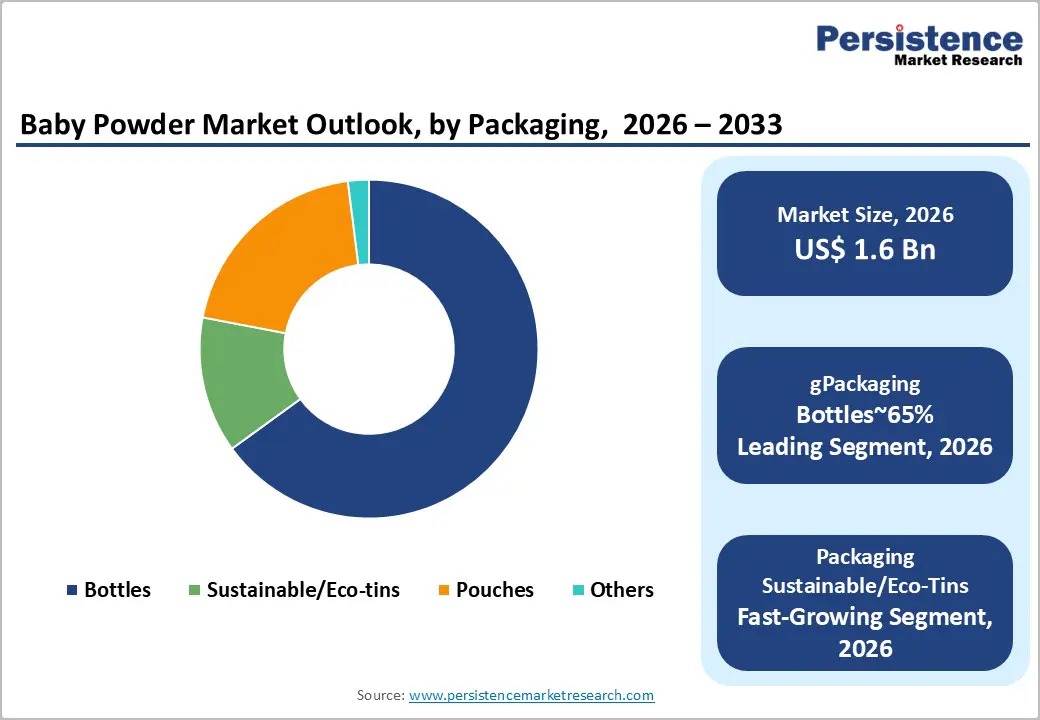

The global baby powder market size is likely to be valued at US$1.6 billion in 2026 and is expected to reach US$2.5 billion by 2033, growing at a CAGR of 6.8% during the forecast period from 2026 to 2033, driven by a global consumer transition toward talc-free and plant-based formulations, spurred by heightened safety awareness and regulatory scrutiny.

Rising disposable incomes and expanding urbanization in emerging economies are significantly increasing the adoption of premium infant skincare products. Demand for natural ingredients and e-commerce expansion support this trajectory, with Asia Pacific leading due to high birth rates. Leading manufacturers are subsequently adapting their portfolios to emphasize clean-label ingredients and sustainable packaging, directly addressing modern parental demands for verifiable safety and eco-conscious product lifecycles.

Key Industry Highlights:

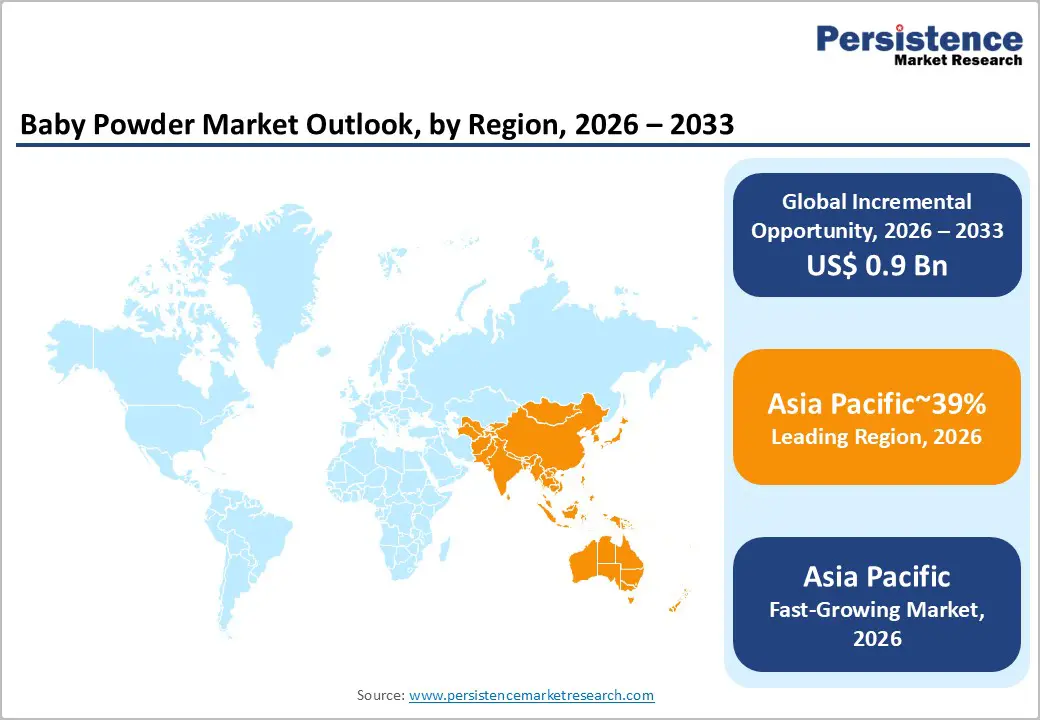

- Leading Region: Asia Pacific is projected to lead due to high birth rates, growing middle-class populations, and strong distribution networks, accounting for approximately 39% share.

- Fastest-Growing Region: Asia Pacific is anticipated to grow the fastest due to increasing urbanization, rising healthcare awareness, and expanding e-commerce penetration.

- Leading Ingredient Type: Talc-free/Cornstarch is expected to lead, accounting for approximately 76%, driven by regulatory compliance, consumer trust, and high adoption in infant skincare routines.

- Leading Packaging Type: Plastic bottles are projected to lead with approximately 65%, supported by convenience, ease of handling, and established manufacturing supply chains.

| Key Insights | Details |

|---|---|

| Baby Powder Market Size (2026E) | US$ 1.6 Bn |

| Market Value Forecast (2033F) | US$ 2.5 Bn |

| Projected Growth (CAGR 2026 to 2033) | 6.8% |

| Historical Market Growth (CAGR 2020 to 2025) | 5.4% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Growth Analysis – Surge in Demand for Talc-Free and Plant-Based Alternatives

The baby powder market is structurally benefiting from a pronounced consumer shift toward talc-free formulations, prompted by regulatory scrutiny and high-profile litigation over traditional talc safety. Rising parental concern over ingredient safety is increasingly influencing purchasing decisions, with a focus on dermatologically tested, hypoallergenic, and clean-label products. In response, manufacturers are reformulating flagship product lines using natural alternatives such as cornstarch, arrowroot, and tapioca powder to align with regulatory standards and consumer expectations. This shift necessitates greater transparency in sourcing, specialized processing methods, and robust quality control systems to ensure products maintain performance while adhering to safety certifications. Growth in the premium segment is particularly notable, as parents demonstrate a readiness to pay higher prices for offerings that meet health-conscious and ethical criteria.

These trends are driving investments in traceability systems, organic certifications, and tailored manufacturing capabilities. Regulatory frameworks continue to encourage innovation focused on safety, influencing cost structures and margins associated with talc substitutes. Simultaneously, plant-based formulations are broadening product differentiation, allowing brands that successfully integrate consumer-driven, non-talc alternatives to enhance competitiveness across both mainstream and niche segments of the baby care market.

Urbanization and Rising Disposable Incomes in Emerging Markets

Rapid urbanization and expanding middle-class populations in emerging markets are structurally amplifying demand for baby powder products, driven by shifts in lifestyle and hygiene consciousness. Rising disposable incomes are increasing per capita expenditure on personal care products, supporting demand for premium and differentiated offerings. Retail expansion across urban centers through modern trade channels, e-commerce platforms, and organized retail networks has strengthened product accessibility and brand visibility in the baby hygiene segment. These demographic and economic developments are reinforcing sustained market momentum, prompting adjustments across distribution systems, marketing frameworks, and formulation strategies.

Companies are recalibrating value chains to align with evolving consumer expectations, emphasizing product quality, safety assurance, and enhanced convenience. Urban population growth is simultaneously reshaping purchasing behavior, with families prioritizing convenience-oriented, dermatologically tested, and safety-validated solutions. Supply chains are adapting to manage higher transaction volumes and increased regional logistics complexity, while pricing architectures balance affordability with premium positioning strategies. The combined effects of income expansion, urban concentration, and retail modernization are structurally reinforcing market growth, driving investment in manufacturing scalability, localized sourcing capabilities, and diversified product portfolios across emerging Asia Pacific economies.

Barrier Analysis – Stringent Regulatory Scrutiny and Litigation Risks

The baby powder market faces structural constraints from intensifying regulatory oversight targeting legacy ingredient safety concerns. Regulatory bodies are enforcing stringent contaminant detection standards, increasing compliance complexity across manufacturing and sourcing functions. Expanded testing obligations necessitate sophisticated laboratory capabilities, independent certifications, and continuous quality verification mechanisms, all of which elevate operational costs and prolong product development and approval cycles. At the same time, ongoing litigation tied to legacy formulations sustains reputational exposure within the category. Heightened consumer skepticism further intensifies scrutiny, compelling companies to strengthen transparency measures, refine labeling accuracy, and implement comprehensive risk management protocols to maintain credibility and market access.

Tighter regulation reallocates cost structures toward compliance, insurance coverage, and legal contingencies. Smaller producers experience disproportionate pressure due to constrained capital reserves and limited access to advanced certification infrastructure. Margin compression becomes more pronounced as firms attempt to offset reformulation and compliance expenses while serving price-sensitive segments. Retailers and distribution partners increasingly enforce rigorous supplier qualification criteria, positioning regulatory adherence as a baseline competitive requirement. Together, legal liabilities and regulatory escalation establish structural financial barriers that temper industry expansion and raise entry thresholds.

High Production Costs for Organic Alternatives

The transition toward organic and plant-based baby powder formulations is structurally increasing production cost intensity across the value chain. Procuring natural alternatives such as cornstarch increases raw material costs by roughly twenty to twenty-five percent, driven by premium agricultural sourcing and certification obligations. Organic cultivation requires regulated farming conditions, documented traceability, and independent verification, adding multiple compliance layers to supply chains. These requirements heighten input price volatility and expand working capital needs, particularly where sustainability benchmarks are strictly enforced.

In parallel, manufacturing processes must be modified to address moisture sensitivity and contamination control, leading to additional investments in processing technology and quality assurance systems. Higher input expenditures place sustained pressure on gross margins, particularly in price-sensitive emerging markets. Producers encounter limited latitude to transfer costs to consumers, who weigh safety considerations against affordability constraints. Retailers often resist substantial price adjustments, intensifying margin compression across both branded and private-label categories. Cost escalation also reshapes inventory management practices, as organic materials demand controlled storage and faster turnover cycles.

Opportunity Analysis – Integration of Advanced Organic and Therapeutic Ingredients

The baby powder market presents a structural opportunity through the integration of advanced organic and therapeutic botanical ingredients. Consumer preferences are shifting toward multifunctional formulations that extend beyond basic moisture absorption and odor control. Incorporating extracts such as chamomile, calendula, and colloidal oatmeal enhances anti-inflammatory and dermal soothing performance. This functional convergence aligns baby powder with broader natural skincare positioning within regulated infant care frameworks. Certification of organic inputs and validated dermatological testing strengthen differentiation across premium segments. Such formulation upgrades reconfigure research and development priorities, emphasizing efficacy validation and ingredient traceability.

Therapeutic positioning supports premium pricing architecture and improved contribution margins. Suppliers of certified botanical extracts gain strategic importance within sourcing networks, emphasizing sustainability and transparency. Manufacturing processes adapt to preserve bioactive stability, increasing formulation sophistication and quality assurance rigor. Retail channels leverage premiumization narratives to enhance category segmentation and shelf positioning. The organic baby care segment demonstrates disproportionate revenue momentum, reinforcing investment in holistic infant dermal health solutions. Collectively, therapeutic ingredient integration structurally expands value capture across regulated and premium baby hygiene ecosystems.

Sustainable packaging innovations

Sustainable packaging innovations are reshaping product design and supply chain strategies across consumer goods industries. Manufacturers are increasingly adopting biodegradable materials, recycled polymers, and reduced-weight formats to minimize environmental impact and comply with evolving regulatory standards. These initiatives require redesigning packaging architectures, recalibrating supplier networks, and investing in material science research to maintain durability, barrier protection, and shelf stability. Lifecycle assessments and carbon footprint measurements are becoming integral to development processes, embedding environmental metrics into cost and performance evaluations.

Transitioning to sustainable formats introduces operational and financial complexities. Alternative materials often involve higher procurement costs, limited supplier availability, and performance trade-offs that necessitate additional testing and certification. Capital expenditure increases initially as production lines adapt to alternative molding and filling technologies. Long-term cost efficiencies may emerge through material optimization and regulatory risk mitigation. Logistics frameworks may also require adjustment due to differences in weight, strength, or storage characteristics. Despite these constraints, sustainable packaging supports brand differentiation, regulatory alignment, and long-term risk mitigation, positioning it as a strategic lever rather than a purely compliance-driven adjustment within competitive markets.

Category–wise Analysis

Ingredient Type

The talc-free segment is expected to dominate the market segment, accounting for approximately 76% share in 2026, reflecting entrenched consumer realignment toward plant-derived safety profiles. This dominance stems from sustained health controversies surrounding talc, which accelerated reformulation cycles and portfolio withdrawals across legacy brands. Market incumbents, including Johnson & Johnson and Pigeon Corporation, have transitioned toward cornstarch-based formulations to preserve brand equity and maintain retail shelf presence amid shifting safety perceptions. This strategic repositioning is grounded in pediatric endorsement, reduced respiratory risk profiles, and reliable moisture-absorption performance across mass retail and pharmacy distribution channels. Consumer research from Nielsen reflects sustained preference for naturally-derived bases, supporting continued replacement demand and repeat purchasing behavior. Scale advantages in agricultural procurement and standardized processing capabilities enhance cost stability and supply consistency, reinforcing the segment’s entrenched leadership within conventional baby hygiene consumption patterns.

The talc-free segment is expected to be the fastest-growing segment, driven by accelerating clean-label penetration and certification-backed differentiation strategies. Growth is catalyzed by demand for traceable botanical inputs aligned with holistic infant skincare positioning. Brands incorporating certifications such as the USDA Organic strengthen premium shelf placement and digital visibility within specialty retail channels. Companies, including The Honest Company and Earth Mama Organics, utilize certified ingredient positioning to reinforce brand loyalty and increase switching barriers among health-oriented millennial parents. Additional emphasis on dermatological testing and small-batch sourcing frameworks enhances perceptions of product efficacy and controlled quality, while supporting exclusivity narratives. As premiumization increasingly defines purchasing behavior in baby care, certified organic talc-free formulations are structurally positioned to grow at a pace exceeding the broader category trajectory.

Packaging Type

Plastic bottles are anticipated lead, accounting for approximately 65% share in 2026, supported by entrenched manufacturing scale and retail compatibility advantages. Their market leadership is supported by structural durability, effective moisture barrier properties, and controlled dispensing systems aligned with frequent infant care usage. Companies such as Johnson & Johnson and Himalaya Wellness Company utilize rigid plastic packaging to maintain tamper evidence, logistical resilience, and shelf stability across large-scale retail networks. Economies of scale derived from cost-efficient molding technologies and standardized filling operations reinforce competitive unit economics compared with alternative packaging materials. Extensive penetration in offline retail channels further entrenches plastic bottle formats within established distribution infrastructures, sustaining operational consistency and supply chain efficiencies.

Sustainable/Eco-tins are expected to be the fastest-growing segment, by accelerating environmental consciousness and tightening waste management mandates. Consumer preferences are shifting toward recyclable metal tins and biodegradable packaging formats that align with broader sustainability commitments. Companies such as The Honest Company and Earth Mama Organics are incorporating environmentally conscious materials to strengthen premium positioning and sharpen competitive differentiation. Regulatory developments, including policy directives issued by the European Union, are intensifying oversight of single-use plastics and accelerating material substitution across consumer goods categories. As a result, packaging innovation is influencing upstream procurement decisions, supplier selection criteria, and lifecycle accountability standards within the evolving baby care value chain.

Regional Insights

Asia Pacific Baby Powder Market Trends

Asia Pacific is expected to remain both the leading and fastest growing regional market with approximately 39% share of the global market in 2026, supported by demographic scale and manufacturing depth. The region is projected to retain structural leadership, supported by elevated birth rates, rapid urbanization, and rising middle-class consumption. Baby powder usage is increasingly shifting from discretionary application to a routine hygiene staple within expanding urban households. Economies of scale in producing cornstarch and tapioca-based substitutes are expected to enhance supply-side scalability and maintain price competitiveness. Concurrently, regulatory alignment toward stricter safety protocols is anticipated to strengthen consumer trust and formalize branded participation in historically fragmented markets.

India is anticipated to function as a critical regional anchor, shaping affordability dynamics, herbal formulation positioning, and digital commerce acceleration. Domestic manufacturers such as Himalaya Wellness Company are likely to intensify competition through talc-free, Ayurveda-inspired variants distributed via digital marketplaces and local pharmacy networks. Heightened policy enforcement around ingredient integrity is expected to elevate compliance standards, increasing emphasis on traceability and validated quality assurance. Capital allocation is projected to favor localized agricultural sourcing, sachet-oriented packaging formats, and scalable rural distribution frameworks, reinforcing the region’s position as the primary volume and growth driver within the global baby powder industry.

North America Baby Powder Market Trends

North America is expected to remain a mature and structurally stable market within the global baby powder industry, anchored by deep enterprise penetration and advanced retail integration. Demand is projected to be sustained by category premiumization rather than volume expansion, as consumers prioritize organic, dermatologist-tested, and clean-label formulations. The region’s progression toward a fully talc-free product environment is expected to institutionalize safety-centric formulation design and greater transparency in ingredient sourcing. Expansion of technology-enabled retail models, including direct-to-consumer platforms and data-driven personalization systems, is likely to enhance customer retention metrics and margin optimization. Competitive dynamics are anticipated to concentrate on clinical substantiation, sustainable packaging development, and the incorporation of multifunctional botanical ingredients.

Capital allocation trends suggest sustained investment in formulation science and advanced moisture-barrier performance, particularly within increasingly stringent consumer protection frameworks that elevate compliance thresholds. The U.S. is projected to serve as the regional benchmark, influencing innovation pace, regulatory interpretation, and brand positioning. Oversight bodies such as the U.S. Food and Drug Administration are expected to maintain rigorous safety validation requirements, embedding compliance expenditures into development cycles and reinforcing entry barriers. Established players, including Johnson & Johnson and natural-focused brands such as Burt's Bees, are likely to compete through botanical differentiation and eco-conscious packaging, while e-commerce channels intensify price transparency and niche brand scalability.

Europe Baby Powder Market Trends

Europe is expected to remain a mature and structurally stable market within the global baby powder industry, anchored by harmonized regulatory architecture and advanced consumer safety standards. Harmonized cosmetic safety regulations are likely to reinforce stringent ingredient disclosure, contaminant monitoring, and certification-based differentiation across member states. Consumer demand remains closely aligned with standards such as ECOCERT and COSMOS-standard, embedding traceability and disciplined botanical sourcing into procurement systems. Sustainability mandates are accelerating the shift toward recyclable metal tins and biodegradable refill solutions, altering packaging procurement models and strengthening lifecycle accountability. Competitive focus is expected to concentrate on dermo-cosmetic validation, pharmacy-centric distribution channels, and zero-waste product configurations.

The region is expected to maintain demand primarily through compliance-oriented reformulation and premium organic substitution rather than volume-driven growth. Germany is projected to anchor regional standards, influencing formulation protocols, packaging innovation, and supplier qualification criteria. Enforcement of European regulatory directives sustains strict impurity limits and organic compliance thresholds, reinforcing elevated entry barriers. Market participants such as Beiersdorf and botanical-focused brands such as Weleda compete through clinically supported plant integration and localized sustainable production. Capital deployment is anticipated to prioritize recyclable materials, refill infrastructure, and regionally sourced calendula and chamomile supply ecosystems.

Competitive Landscape

The global baby powder market is moderately consolidated, with leadership concentrated among multinational consumer goods companies such as Johnson & Johnson and Procter & Gamble. These firms shape category standards through large-scale procurement networks, embedded dermatological validation protocols, and extensive pharmacy, supermarket, and e-commerce distribution coverage. Their scale facilitates rapid reformulation toward talc-free platforms, reinforcing safety compliance as a baseline requirement. Nevertheless, consolidation at the top coexists with fragmentation in regional and premium tiers, particularly in Asia, where local brands compete through botanical positioning, ingredient transparency, and sustainability-led differentiation strategies that target emerging middle-class and health-conscious consumer segments.

Key Industry Developments:

- In October 2025, Remark HB Limited launched Bangladesh’s first 100% safe cornstarch baby powder. This product provides a natural, hypoallergenic, and chemical-free alternative specifically designed for sensitive infant skin in an emerging market.

- In August 2025, Pigeon Corporation launched a new specialized product line, including the silicone Paladai, designed for babies requiring expert care, such as those with low birth weight, in India. This expansion broadens the company's reach into the medical and specialist infant care segment of a high-growth region.

- In January 2025, Unicharm Corp (MamyPoko Pants) launched the 'HarBabyKaPehlaDiaper' campaign featuring redesigned absorption technology. This marketing push emphasizes technological innovation in newborn care to maintain market share against increasingly specialized competitors.

Companies Covered in Baby Powder Market

- Johnson & Johnson

- Procter & Gamble

- Kimberly-Clark Corporation

- Unilever

- Beiersdorf AG

- Pigeon Corporation

- The Himalaya Drug Company

- Burt's Bees

- The Honest Company

- Chicco

- Sebapharma GmbH & Co. KG

- Dabur India Limited

- Church & Dwight

- PZ Cussons

- Goodbaby International

- California Baby

Frequently Asked Questions

The global baby powder market is projected to be valued at US$1.6 billion in 2026 and is expected to reach US$2.5 billion by 2033, supported by the rising demand for talc-free, plant-based formulations and expanding urban consumption in emerging economies.

Heightened regulatory scrutiny and consumer safety awareness have accelerated the transition toward cornstarch and botanical-based alternatives. Parents increasingly prioritize dermatologically tested, hypoallergenic, and clean-label products, prompting manufacturers to reformulate portfolios and invest in traceable, certified ingredient sourcing frameworks.

The baby powder market is forecast to grow at a CAGR of 6.8% from 2026 to 2033, reflecting sustained premiumization, regulatory-driven reformulation, and expanding e-commerce penetration across high-birth-rate regions.

Asia Pacific is anticipated to lead the market, accounting for approximately 39% share in 2026, driven by high birth rates, rapid urbanization, manufacturing scale advantages in plant-based inputs, and strengthening retail and digital distribution networks.

The baby powder market is moderately consolidated, with key players including Johnson & Johnson, Procter & Gamble, Kimberly-Clark Corporation, Unilever, Beiersdorf AG, Pigeon Corporation, The Himalaya Drug Company, Burt’s Bees, and The Honest Company. Competition centres on talc-free reformulation, botanical differentiation, sustainable packaging integration, and multi-channel retail expansion.