- Baby Care & Accessories

- Libya Baby Diapers and Wipes Market

Libya Baby Diapers and Wipes Market Size, Share, and Growth Forecast, 2026 - 2033

Libya Baby Diapers and Wipes Market by Product Type (Diaper and Wipes), by Age Group (9 to 24 Months, 0 to 5 Months, 5 to 8 Months, Above 24 Months), by Sales Channel (Wholesalers/Distributors, Hypermarkets/Supermarkets, Online Retailers, Specialty Stores, Multi-brand Stores, Convenience Stores, Pharmacy/Drug Stores, and Other Sales Channel), and Regional Analysis for 2026 - 2033

Libya Baby Diapers and Wipes Market Size and Trends Analysis

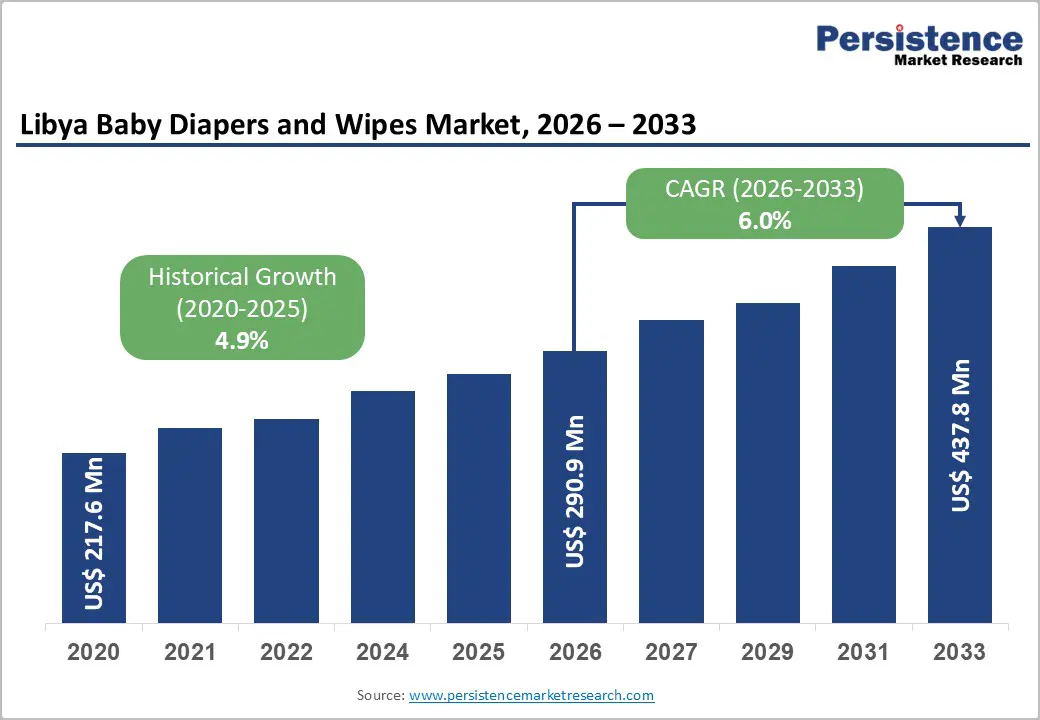

The libya baby diapers and wipes market was valued at US$ 209.4 Million in 2020 and is projected to reach US$ 283.8 Million by 2026, further expanding to US$ 404.9 Million by 2033, growing at a CAGR of 6.0% between 2026 and 2033.

The Libyan market demonstrates sustained growth driven by increasing urbanization, rising household disposable incomes, and expanding awareness of hygiene standards among middle-income families.

The market benefits from North African demographic trends, with Libya's young population (median age approximately 29 years) generating consistent demand for infant care products. Product diversification beyond traditional diapers particularly the rapid expansion of baby wipes reflects evolving consumer preferences and retail channel modernization. This represents a stable, emerging market opportunity with strategic implications for both regional and international players seeking North African market penetration.

Key Industry Highlights:

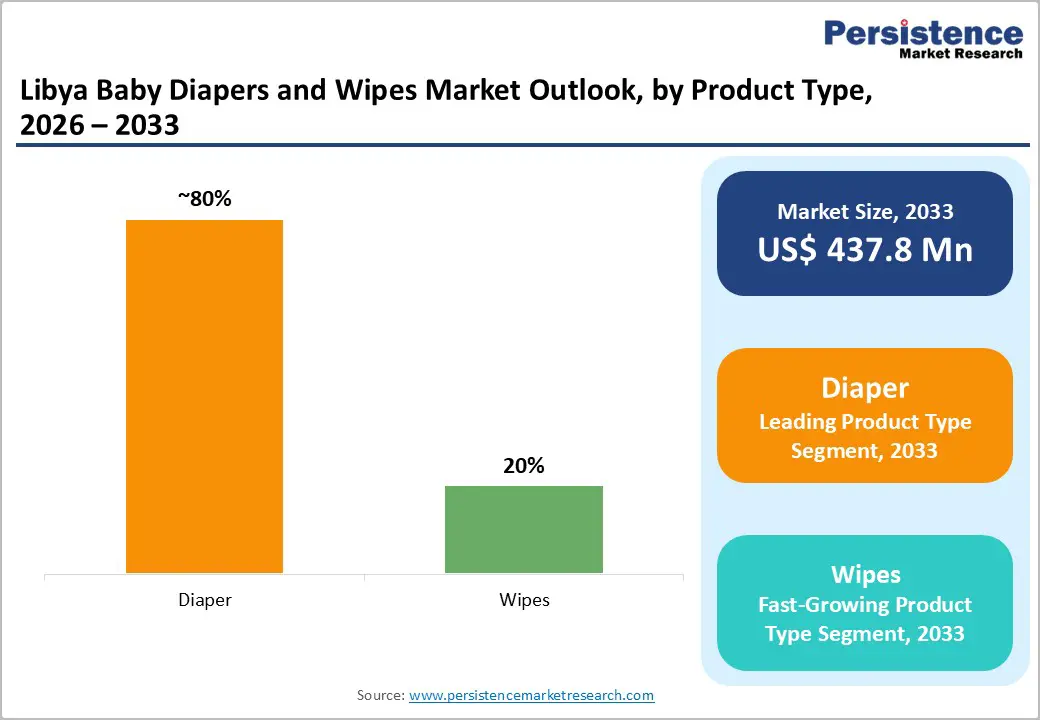

- Product Segment Leadership: Diapers command 60%+ market revenue share as category foundation, while wipes emerge as fastest-growing segment at 6.5% CAGR, reflecting diversifying consumer product portfolios and expanding retail distribution supporting multi-product household penetration.

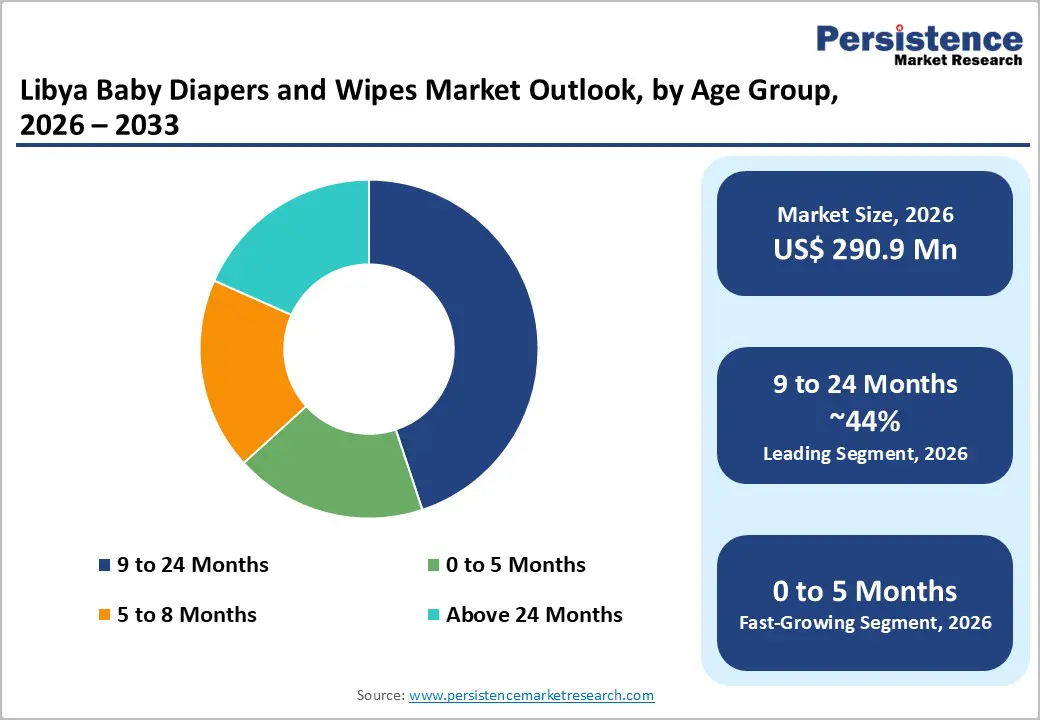

- Age Group Dynamics: 9-24 months segment dominates at b representing peak consumption intensity, while 0-5 months segment accelerates at 6.4% CAGR, driven by premium product adoption and new-parent healthcare consciousness.

- Distribution Channel Evolution: Wholesalers/distributors maintain 40%+ market share representing traditional infrastructure, while hypermarkets/supermarkets demonstrate fastest growth at 6.6% CAGR, signifying structural retail modernization and organized channel expansion.

- Demographic & Economic Drivers: Libya's 32% under-age-10 population and rising middle-class disposable incomes support sustained category demand, with urban concentration enabling efficient distribution supporting penetration expansion in metropolitan markets.

- Market Opportunities & Risk Factors: E-commerce represents <5% current share with 15-18% growth potential, premium product segments enable 35-50% price premiums, and regional supply chain integration reduces cost structures, while economic volatility and import dependencies present constraint considerations requiring strategic risk management.

- Strategic developments emphasize sustainability initiatives, premium product development, geographic expansion into high-growth emerging markets, and digital-native/e-commerce integration; venture capital investment in D2C brands reflects market disruption trends.

| Global Market Attributes | Key Insights |

|---|---|

| Libya Baby Diapers and Wipes Market Size (2026E) | US$ 290.9 Mn |

| Market Value Forecast (2033F) | US$ 437.8 Mn |

| Projected Growth (CAGR 2026 to 2033) | 6.0% |

| Historical Market Growth (CAGR 2020 to 2025) | 4.9% |

Key Growth Drivers

Rising Household Incomes and Consumer Spending Power

Libya's economic recovery trajectory and rising middle-class expansion constitute primary demand catalysts for premium baby care products. Household disposable income growth in urban centers (particularly Tripoli and Benghazi) has increased consumer willingness to purchase branded, premium-quality diapers and wipes over traditional cloth alternatives. Urban middle-income families increasingly adopt convenience-driven purchasing behaviors, viewing disposable baby products as essential childcare investments rather than discretionary items. The shift from traditional cloth diapers to disposable products represents a fundamental consumption pattern change, with penetration rates in major metropolitan areas approaching 35-40% among employed households. Government employment sectors, which constitute a significant portion of formal employment, provide wage stability supporting consistent demand. Market research indicates that households earning above US$ 30,000 annually represent the primary target consumer base, representing approximately 22-25% of Libyan families with infants.

Market Restraining Factors

Limited Local Manufacturing and Import Dependencies

Libya lacks significant domestic diaper and wipes manufacturing capacity, creating supply chain vulnerabilities and cost inefficiencies. Approximately 95% of baby diaper products are imported, primarily from Egypt, Tunisia, and international suppliers, rendering the market susceptible to supply disruptions and tariff changes. Customs procedures and regulatory certifications for imported baby products occasionally extend product lead times to 6-8 weeks, disrupting inventory management and creating stock-out risks during peak demand periods. Import licensing complexities and occasional regulatory delays have historically constrained new entrant market access, creating barriers for international brands seeking market entry. The absence of local manufacturing infrastructure prevents cost optimization through local production, limiting price competitiveness versus established regional producers. Transportation and logistics costs for imported products inflate final retail prices by 15-22%, directly impacting consumer affordability and market penetration rates among price-sensitive segments.

Libya Baby Diapers and Wipes Market Trends and Opportunities

E-Commerce Channel Development and Digital Retail Expansion

E-commerce penetration in Libya remains below regional averages, representing significant expansion potential as digital payment infrastructure and logistics networks mature. Current online retail channels represent less than 5% of market share, yet regional benchmarks suggest mature markets achieve 15-25% online channel penetration.

Expanding smartphone adoption (43% of population), improving internet infrastructure, and growing consumer familiarity with online shopping create foundational conditions for rapid e-commerce growth. Online channels enable premium brand positioning and direct-to-consumer relationships, reducing distribution cost structures and improving brand margins by 8-12%. Digital marketing capabilities provide targeted reach to affluent urban consumers with higher brand loyalty and purchasing frequency. Market sizing indicates that achieving 12% e-commerce penetration by 2033 would generate approximately US$ 48-52 Million in incremental market value, representing significant growth optionality.

Libya Baby Diapers and Wipes Market Insights and Trends

Product Type Insights

Diapers Dominate Today While Baby Wipes Accelerate Growth Across Infant Care Market

The diaper segment continues to anchor the market, holding a dominant position with over 60% of total revenue and forming the foundation of category demand. In 2026, diapers are estimated to generate approximately US$ 170-175 million in revenue, supported by widespread consumer adoption across income groups. High replacement frequency, averaging six to eight diapers per infant per day, ensures stable and recurring revenue streams. Standard disposable diapers account for nearly 75-80% of segment sales, while specialty variants such as training and overnight diapers contribute the remaining share. Urban penetration exceeds 40%, whereas rural and lower-income adoption remains comparatively low, creating long-term expansion opportunities. Overall, the diaper segment is projected to grow steadily at a CAGR of 5.5-5.8% between 2026 and 2033, driven by rising middle-income consumption and premiumization trends.

In contrast, baby wipes represent the fastest-growing product category, expanding at a CAGR of around 6.5% over the same period. Currently contributing 35-40% of market revenue, wipes benefit from multifunctional use, convenience, and alignment with modern hygiene-focused parenting. Premium formulations command significant price premiums, enhancing margins, while broader retail availability and awareness campaigns are expected to push wipes toward nearly 45% market share by 2033.

Age Group Insights

Infant Diaper Market Age Segmentation Reveals Dominance, Growth, and Transition Dynamics

The age-group analysis highlights clear consumption and growth differences across infant diaper categories. The 9-24 months segment emerges as the dominant consumer cohort, accounting for over 45% of total market revenue and maintaining steady growth. This age range represents peak diaper usage, as infants develop stable feeding habits and mobility patterns, leading to consistent consumption of 5-8 diapers per day. Market revenue from this segment is estimated at US$ 128-135 million in the 2026 baseline year, reflecting the largest installed consumer base. Strong brand loyalty, high retail visibility, and sustained promotional focus further reinforce its leadership, while a 5.8-6.0% CAGR reflects demographic stability and expanding penetration in secondary markets.

The 0-5 months segment is the fastest-growing cohort, recording a projected CAGR of 6.4% from 2026 to 2033. Currently contributing 20-22% of market revenue, this segment benefits from rising demand for premium newborn-specific products, including hypoallergenic and ultra-soft variants. Higher parental health awareness and medical recommendations are accelerating adoption, with the segment expected to reach 25-28% revenue share by 2033.

The 5-8 months and above 24 months segments together account for roughly 30-35% of revenue. These stages reflect transitional and declining usage patterns, respectively, though innovation in training and transition products offers moderate growth opportunities.

Sales Channel Insights

Traditional and Modern Retail Channels Shape Market Reach, Growth, and Competitive Dynamics

Wholesalers and distributors continue to dominate the sales channel landscape, accounting for over 40% of total market revenue due to their well-established distribution infrastructure and long-standing retail relationships. This channel serves as the primary supply route for independent retailers, pharmacies, and convenience stores, handling an estimated US$113-120 million in annual market volume as of the 2026 baseline. Strong inventory management systems, loyalty programs, and geographic reach particularly in secondary and rural markets support its strategic relevance. However, margin pressure has intensified as distributor margins declined from 12-15% to nearly 10-12%, while growth has moderated to a 5.5-5.8% CAGR amid rising competition from modern retail formats.

Hypermarkets and supermarkets represent the fastest-growing channel, expanding at a 6.6% CAGR from 2026 to 2033. Currently holding around 25-28% market share, this segment benefits from organized retail expansion, one-stop shopping convenience, and strong promotional capabilities. Higher gross margins of 18-22% enable investments in category development, premium brand visibility, and consumer education, accelerating growth across urban and secondary markets.

Additional channels including specialty baby stores, online platforms, and pharmacy or drug stores collectively contribute 28-32% of market revenue. Specialty stores appeal to affluent consumers through expert guidance and premium assortments, while online retail, though under 5% share, shows strong long-term potential with 15-18% CAGR. Pharmacies offer trusted recommendations, and convenience formats support stable, need-based purchases, underscoring the importance of differentiated, multi-channel strategies.

Libya Baby Diapers and Wipes Market Competitive Landscape

Libya's Baby Diapers and Wipes Market demonstrates moderate fragmentation, with no single player commanding greater than 18-22% market share. The top five manufacturers control approximately 50-55% of total market revenue, indicating moderate consolidation with competitive opportunities for challenger brands and niche players. Market structure characteristics include established regional players commanding 30-35% collective share, international brands holding 35-40% share, and emerging/local manufacturers comprising 25-30%. Egyptian and Tunisian manufacturers dominate regional supply through established distribution relationships and competitive cost structures.

International brands (primarily European and Asian manufacturers) maintain premium positioning focused on affluent urban consumers. Market concentration demonstrates healthy competitive dynamics, preventing monopolistic pricing practices while enabling category growth investments from established players. New entrant barriers remain moderate, with distribution access and brand awareness representing primary challenges rather than insurmountable structural barriers. Private label penetration remains limited at 3-5%, indicating retail channel development opportunities.

Key Industry Developments

- In 2025, the Libyan Export Promotion Centre announced that Aseel Company for the Manufacture of Diapers and Tissue Paper-part of the Al-Sahel Holding Group successfully fulfilled an additional export shipment to sub-Saharan African markets, marking a notable expansion in the company’s international trade activities.

Companies Covered in Libya Baby Diapers and Wipes Market

- AL rabeea

- Lilas

- Peaudouce

- Ontex

- ABA group

- Baby Lino

- Bumble

- Hayat Kimya

- Johnson

- CHICCO

- Remy Industries

- Other Market Players

Frequently Asked Questions

The Libya Baby Diapers and Wipes Market is estimated to be valued at US$ 290.9 Mn in 2026.

The key demand driver for the Libya Baby Diapers and Wipes Market is the combination of high birth rates and rising urbanization, which is steadily increasing the consumption of convenient infant hygiene products across the country.

Among product types, Diaper have the highest preference, capturing beyond 80% of the market revenue share in 2026, surpassing other product types.

AL rabeea, Lilas, Peaudouce, Ontex, ABA group, and Baby Lino. There are a few leading players in the Libya Baby Diapers and Wipes Market.