- Processed Food

- Ready-to-Eat Pureed Baby Foods Market

Ready-to-Eat Pureed Baby Foods Market Size, Share, and Growth Forecast, 2026 - 2033

Ready-to-Eat Pureed Baby Foods Market by Product Type (Fruits, Vegetables, Grains, Meats), Age Group (4-6 Months, 7-9 Months, 10-12 Months), Distribution Channel (Hypermarkets/Supermarkets, Others), and Regional Analysis for 2026 - 2033

Ready-to-Eat Pureed Baby Foods Market Size and Trends Analysis

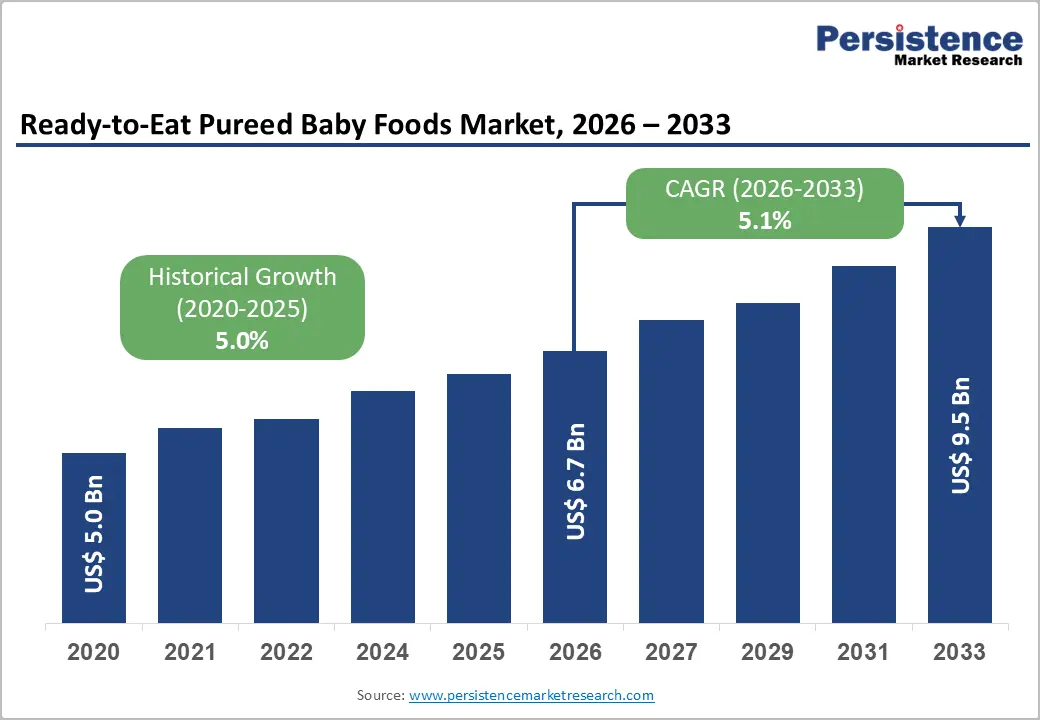

The global ready-to-eat pureed baby foods market size is likely to be valued at US$6.7 billion in 2026 and is expected to reach US$9.5 billion by 2033, growing at a CAGR of 5.1% during the forecast period from 2026 to 2033, driven by increasing demand for convenient, nutritionally balanced options that support infants during the transition from milk to solid foods. Growth in this sector is largely influenced by the rising participation of women in the workforce, which has heightened the need for time-saving feeding solutions, as well as growing parental awareness regarding early-life nutrition, guided by recommendations from organizations such as the World Health Organization (WHO) and UNICEF.

Demographic trends, including urbanization in emerging markets and the expansion of dual-income households, are creating new opportunities for ready-to-eat baby food products. Parents are increasingly seeking products that ensure safety, ingredient transparency, and adherence to nutritional standards, while also valuing organic, clean-label, and allergen-conscious formulations. Continuous product innovation, such as stage-specific formulations, mixed fruit and vegetable blends, and plant-based or fortified options, helps manufacturers address evolving consumer preferences and regulatory requirements.

Key Industry Highlights:

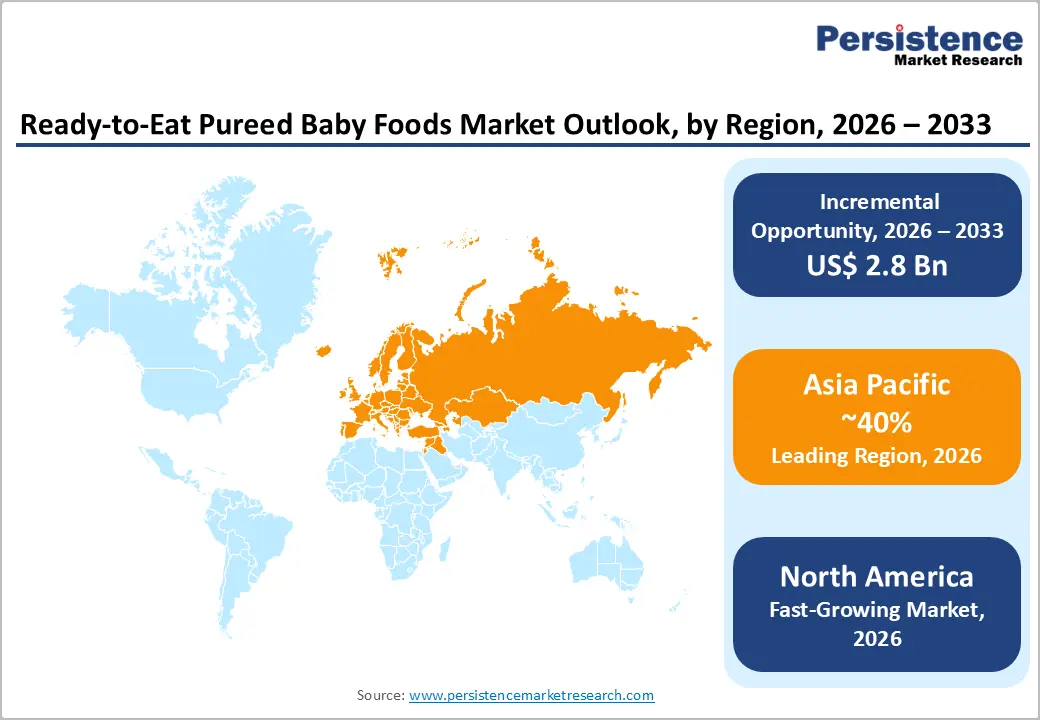

- Leading Region: Asia Pacific is anticipated to be the leading region, accounting for a market share of 40% in 2026, driven by rapid urbanization, rising female workforce participation, increasing middle-class incomes, manufacturing, and export advantages.

- Fastest-growing Region: North America is likely to be the fastest-growing region, supported by U.S. leadership, high parental nutrition awareness, product innovation, and a strong regulatory framework.

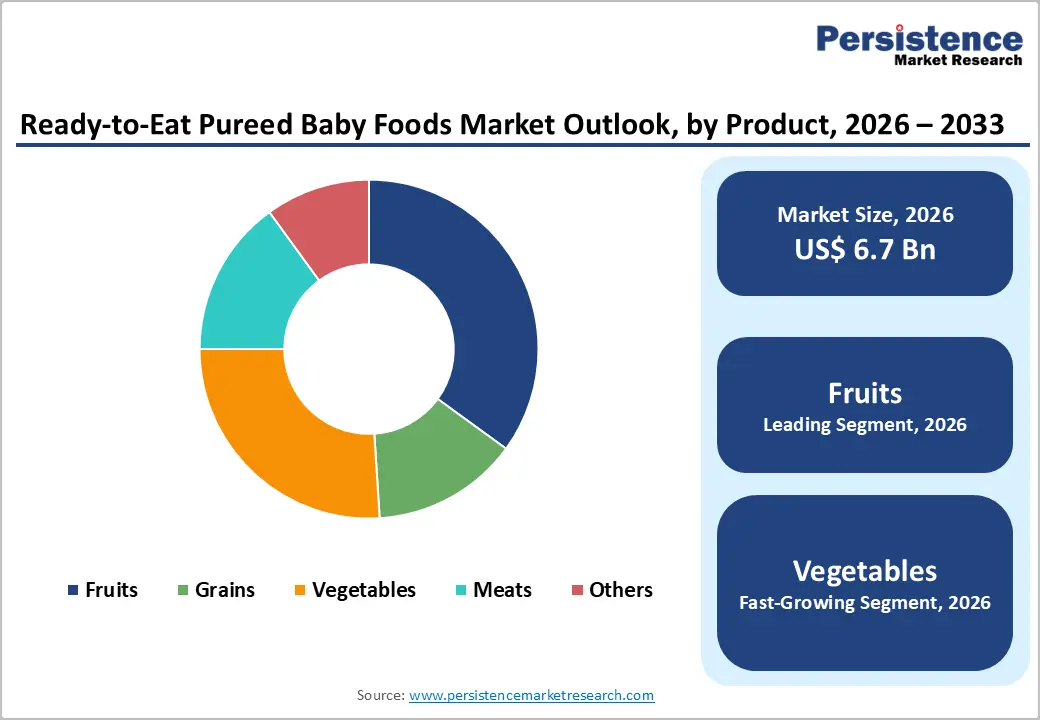

- Leading Product Type: Fruits are projected to represent the leading product type in 2026, accounting for 45% of the revenue share, driven by natural sweetness, high parental familiarity, and ease of early-stage acceptance.

- Leading Age Group: The 4-6 months are anticipated to be the leading age group, accounting for over 40% of the revenue share in 2026, supported by recommendations for the start of complementary feeding and the preference for smooth, single-ingredient purees for digestive readiness.

| Key Insights | Details |

|---|---|

| Ready-to-Eat Pureed Baby Foods Market Size (2026E) | US$6.7 Bn |

| Market Value Forecast (2033F) | US$9.5 Bn |

| Projected Growth (CAGR 2026 to 2033) | 5.1% |

| Historical Market Growth (CAGR 2020 to 2025) | 5.0% |

DRO Analysis

Driver - Rising Participation of Women in the Workforce

The increasing participation of women in the workforce has significantly reshaped infant feeding practices. Busy working mothers seek convenient, ready-to-eat solutions that provide complete nutrition without extensive preparation, making pureed baby foods highly attractive. The demand is strengthened by dual-income households, which prioritize time-efficient and reliable feeding options. Manufacturers respond with products designed for portability, shelf-stability, and easy serving, aligning with modern lifestyle needs.

Growing female employment also encourages early adoption of commercial baby foods, driving brand loyalty and repeat purchases. As awareness of infant nutrition spreads among working mothers, there is a preference for stage-specific and fortified products to support growth milestones. Companies are innovating packaging, portion sizes, and flavors to cater to convenience without compromising nutritional quality. Urban centers and metropolitan areas witness the highest adoption rates, supported by e-commerce availability and home delivery services.

Increased Parental Awareness of Infant Nutrition and Food Safety

Modern parents are increasingly informed about infant nutritional requirements and the importance of safe feeding practices, influencing market growth. Awareness campaigns and guidelines from organizations such as WHO and UNICEF highlight the need for balanced complementary feeding, prompting demand for commercial purees that meet dietary recommendations. Parents prefer products with verified ingredient sourcing, allergen information, and fortified formulations to ensure adequate intake of iron, vitamins, and proteins during critical development stages.

This heightened awareness drives demand for specialty products such as organic, non-GMO, and clean-label purees, with a growing focus on functional nutrition such as probiotics and fortified cereals. Safety considerations, including BPA-free packaging, pasteurization, and adherence to hygiene standards, are decisive purchase factors. Retailers and manufacturers leverage these concerns by highlighting certifications and regulatory compliance.

Restraint - Stringent Regulatory and Safety Compliance Requirements

Compliance with labeling, nutritional standards, and hygiene regulations increases production costs and slows time-to-market for new products. Manufacturers must navigate multiple agencies, such as the FDA in the U.S., FSSAI in India, and EFSA in Europe, ensuring every batch meets rigorous quality parameters. Any deviation can lead to recalls, fines, or loss of consumer confidence, making adherence both critical and resource-intensive. These regulatory demands are particularly challenging for small and medium-sized enterprises entering the market.

Strict compliance affects innovation cycles, as companies must conduct extensive testing for fortification levels, allergen safety, and shelf-life stability before launch. Certification for organic or clean-label products adds procedural requirements. International expansion becomes complex due to differences in import regulations, nutritional labeling, and safety standards. Even minor lapses can impact brand reputation, making risk management a key focus. While regulations enhance consumer trust, they constrain market agility, requiring significant investment in quality assurance, documentation, and production oversight.

Consumer Preference for Homemade or Fresh Alternatives

Many parents still favor homemade or freshly prepared baby foods, perceiving them as healthier, fresher, and free from additives. This preference limits commercial adoption, particularly in regions where traditional feeding practices are deeply ingrained. Homemade purees allow parents to control ingredients, portion sizes, and seasoning, reducing reliance on packaged options. Such behaviors are amplified by social media trends and parenting communities emphasizing DIY feeding and natural nutrition, posing a challenge to market expansion for ready-to-eat products.

The perception that homemade foods are superior also encourages intermittent use of commercial products rather than consistent consumption. Families in rural and semi-urban areas with limited retail access rely primarily on home-prepared foods. Seasonal availability of fresh fruits and vegetables reinforces homemade feeding. Brands must overcome these preferences through educational campaigns, highlighting safety, nutrient fortification, and convenience advantages.

Opportunity - Innovation in Organic, Allergen-Free, and Functional Purees

Consumers increasingly demand products free from preservatives, artificial colors, and allergens to safeguard infant health. Functional products fortified with vitamins, minerals, probiotics, or plant-based proteins address nutritional gaps and lifestyle concerns, attracting health-conscious parents. Organic certification and clean-label positioning enhance brand credibility, creating premium market segments with high perceived value. Manufacturers can leverage these innovations to differentiate offerings and target specialized consumer needs while aligning with health trends.

Introducing allergen-free and functional purees allows companies to cater to infants with dietary restrictions, enhancing inclusivity and widening the potential consumer base. These products also respond to pediatric recommendations for early-life nutrition, supporting developmental milestones. By integrating natural fortification and plant-based ingredients, brands can offer innovative flavor profiles and textures that appeal to both parents and infants. Expansion into organic and functional lines encourages retail partnerships, premium pricing, and direct-to-consumer channels, presenting sustained revenue potential.

Innovative Flavors and Textures

Innovating flavors and textures represents a major opportunity to drive engagement and adoption in the ready-to-eat pureed baby foods market. Parents seek variety to support taste development and introduce diverse nutrients early in infancy. Companies are experimenting with mixed fruit and vegetable blends, culturally adapted recipes, and stage-specific textures, enabling smooth progression from purees to soft solids.

Flavor innovation aligns with growing exposure to international cuisines and parental willingness to provide varied diets. Textural advancements help address age-specific feeding needs, including soft lumps or finger-friendly consistency, enabling a gradual transition to self-feeding. Manufacturers use sensory appeal and packaging design to complement these innovations, increasing shelf visibility and convenience. Partnerships with pediatricians, nutritionists, and parenting influencers promote trust and trial. By combining taste, texture, and nutritional quality, companies can effectively increase engagement, expand market share, and position products as essential tools for holistic infant development.

Category-wise Analysis

Product Type Insights

Fruits are expected to lead the ready-to-eat pureed baby foods market, accounting for approximately 45% of revenue in 2026, driven by their natural sweetness, high acceptance among infants, and strong parental familiarity during early feeding stages. These products are widely preferred as first foods due to their smooth texture, digestibility, and alignment with pediatric recommendations for introducing single-ingredient purees. For example, apple and banana purees are commonly introduced as initial complementary foods due to their mild flavor and low allergenic risk, supporting widespread adoption.

Vegetable-based purees are likely to represent the fastest-growing segment, supported by increasing emphasis on dietary diversity and reduced sugar exposure in early nutrition. Parents are becoming more conscious of introducing savory flavors early to shape healthier eating habits, aligning with health recommendations. Companies are investing in improving taste profiles and texture to overcome initial resistance among infants, ensuring better acceptance. For example, blends such as carrot and sweet potato or spinach and peas are gaining popularity as they combine nutrition with palatable flavors.

Age Group Insights

The 4-6-month age group is projected to lead the market, capturing around 40% of the revenue share in 2026, supported by its role as the primary stage for introducing complementary feeding alongside milk. At this stage, infants require simple, smooth-textured foods that are easy to digest and free from complex ingredients, making ready-to-eat purees an ideal choice. Distribution channels ensure high availability of these products, particularly in urban markets where awareness is higher. For example, single-ingredient apple or rice purees are commonly introduced at this stage due to their mild taste and low allergenic potential.

The 7-9-month age group is likely to be the fastest-growing age group, driven by the transition toward more complex textures and diverse flavor profiles. At this stage, infants begin developing motor skills and require foods that support chewing and sensory exploration, prompting demand for thicker purees and mixed-ingredient blends. Parents increasingly seek products that provide balanced nutrition, including higher protein and iron content, aligning with developmental milestones. For example, multi-ingredient blends such as vegetable and lentil purees are gaining traction, offering both nutritional value and taste variety.

Regional Insights

North America Ready-to-Eat Pureed Baby Foods Market Trends

North America is likely to be the fastest-growing region, driven by high parental awareness, strong retail infrastructure, and strict regulatory oversight that builds consumer trust. Demand is increasingly shaped by clean-label, organic, and functional formulations, with parents prioritizing transparency, low sugar content, and allergen-safe ingredients. For example, Little Spoon has adopted stricter safety standards aligned with European regulations, reinforcing trust and setting new benchmarks for ingredient transparency and quality in the U.S. market.

The region’s growth is supported by continuous product innovation and premiumization strategies targeting health-conscious parents. Companies are expanding portfolios with plant-based, fortified, and stage-specific purees to meet evolving nutritional needs. Supermarkets and online platforms remain dominant distribution channels, offering a wide product variety and promotional accessibility. The presence of established multinational brands alongside emerging startups fosters a competitive environment focused on differentiation through quality, safety, and convenience.

Europe Ready-to-Eat Pureed Baby Foods Market Trends

Europe is likely to be a significant market for ready-to-eat pureed baby foods, due to stringent food safety standards and a well-established culture of organic consumption. Parents prioritize certified organic, non-GMO, and minimally processed baby foods, aligning with regional policies that promote clean-label and sustainable production. Packaging sustainability and traceability are critical purchase factors, with brands emphasizing eco-friendly materials and transparent sourcing.

Innovation in Europe is centered around premium organic formulations, diverse flavor profiles, and nutritional fortification tailored to developmental stages. Companies are increasingly introducing culturally adapted recipes and plant-based options to meet evolving dietary preferences. For example, HiPP GmbH & Co. Vertrieb KG, known for its extensive organic baby food portfolio and strict adherence to European quality standards, has strengthened its leadership in the region.

Asia Pacific Ready-to-Eat Pureed Baby Foods Market Trends

The Asia Pacific region is anticipated to be the leading region, accounting for a market share of 40% in 2026, driven by rising birth rates, urbanization, and increasing disposable incomes in countries such as China and India. The expanding middle-class population and growing participation of women in the workforce are significantly boosting demand for convenient baby food solutions. Parents are becoming more aware of infant nutrition, leading to increased adoption of packaged purees that meet safety and quality standards. The region also benefits from the rapid expansion of modern retail channels and e-commerce platforms, improving accessibility in both urban and semi-urban areas.

Market players are actively investing in manufacturing capabilities, supply chain efficiency, and product innovation to capture growth opportunities in this region. Affordable product variants and smaller pack sizes are introduced to cater to price-sensitive consumers, while premium segments focus on organic and fortified offerings. For example, Nestlé S.A., which has expanded its infant nutrition portfolio across Asia by localizing products and strengthening distribution networks to meet diverse consumer needs.

Competitive Landscape

The global ready-to-eat pureed baby foods market exhibits a moderately fragmented structure, driven by the presence of numerous multinational corporations and regional players competing across product quality, innovation, pricing, and distribution reach. The market is characterized by strong brand-driven competition, where established companies leverage extensive portfolios and supply chains, while emerging players focus on niche segments such as organic and clean-label offerings.

With key leaders including major food and nutrition companies alongside specialized organic brands, the market reflects a dynamic mix of scale and specialization. These players compete through product innovation, premiumization strategies, and expansion of distribution channels, including e-commerce and direct-to-consumer models. Companies emphasize ingredient transparency, diverse flavor portfolios, and convenient packaging formats such as pouches to enhance consumer appeal.

Key Industry Developments:

- In March 2026, Nestlé S.A. launched Compleat Paediatric Oral Blends, a ready-to-consume, fruit-based nutrition pouch designed for children with special dietary needs, featuring over 50% fruit content along with plant proteins, vitamins, and minerals, and introduced across multiple European markets to meet rising demand for convenient, on-the-go pediatric nutrition solutions.

- In November 2025, Nestlé S.A. announced the acceleration of its global strategy to eliminate added sugars in infant nutrition products, aiming to offer no-added-sugar options across all markets while enhancing product localization and micronutrient fortification to align with global health guidelines and improve early childhood nutrition.

Companies Covered in Ready-to-Eat Pureed Baby Foods Market

- Danone S.A.

- Hain Celestial Group, Inc.

- Hero Group

- Kraft Heinz Company

- Abbott Laboratories

- Plum Organics

- Sprout Foods, Inc.

- Beech-Nut Nutrition Corporation

- Ella's Kitchen (Brands) Limited

- Gerber Products Company

- Earth's Best

- Happy Family Organics

- Nurture, Inc.

- Little Spoon

- Once Upon a Farm

Frequently Asked Questions

The global ready-to-eat pureed baby foods market is projected to reach US$6.7 billion in 2026.

The ready-to-eat pureed baby foods market is driven by rising demand for convenient, nutritionally balanced infant feeding solutions supported by increasing working parents and growing awareness of early-life nutrition.

The ready-to-eat pureed baby foods market is expected to grow at a CAGR of 5.1% from 2026 to 2033.

Key market opportunities include expansion in emerging economies, increasing demand for organic and clean-label products, innovation in flavors and formulations, and growth of e-commerce distribution channels.

Danone S.A., Hain Celestial Group, Inc., Hero Group, Kraft Heinz Company, and Abbott Laboratories are the leading players.