- Baby Care & Accessories

- Baby Food Maker Market

Baby Food Maker Market Size, Share, and Growth Forecast 2026–2033

Baby Food Maker Market by Product Type (Food Preparation, Bottle Preparation), by Nature (Organic, Conventional), Distribution Channel (Supermarkets/Hypermarkets, Specialty Stores, Drug Stores, Online Retailers, Others), and Regional Analysis for 2026–2033

Baby Food Maker Market Size and Trend Analysis

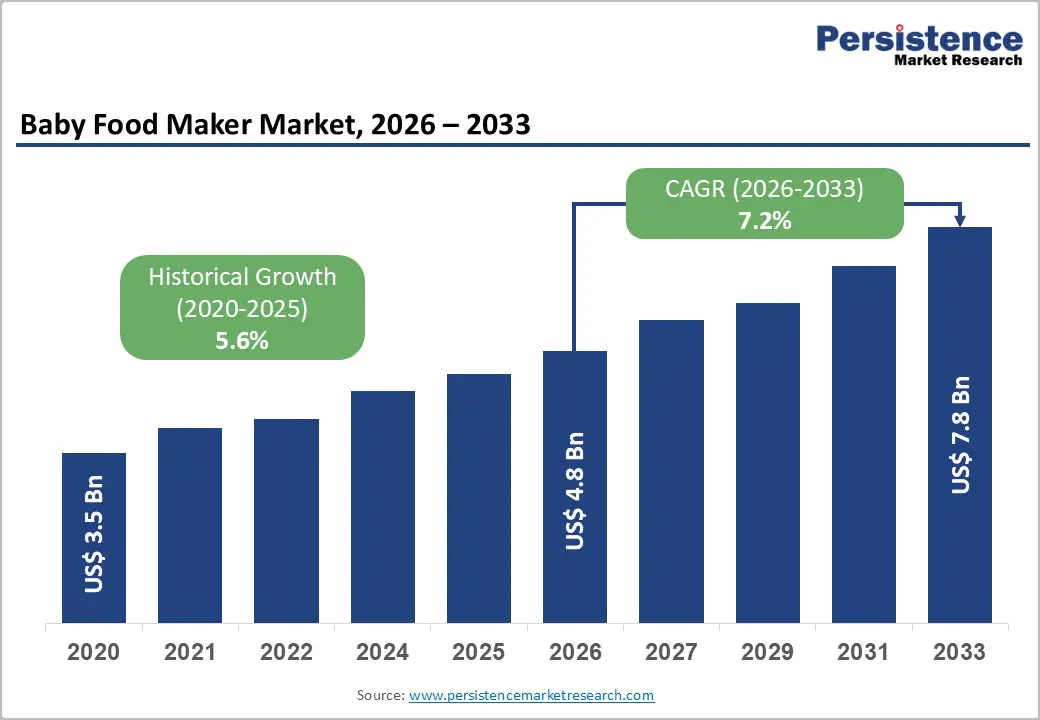

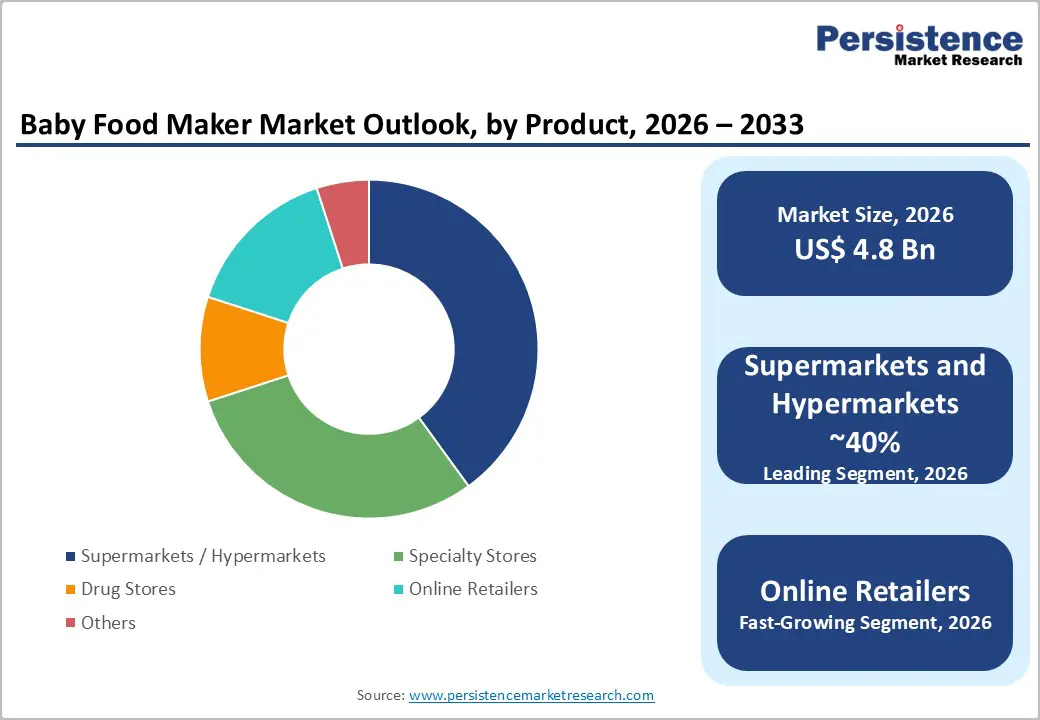

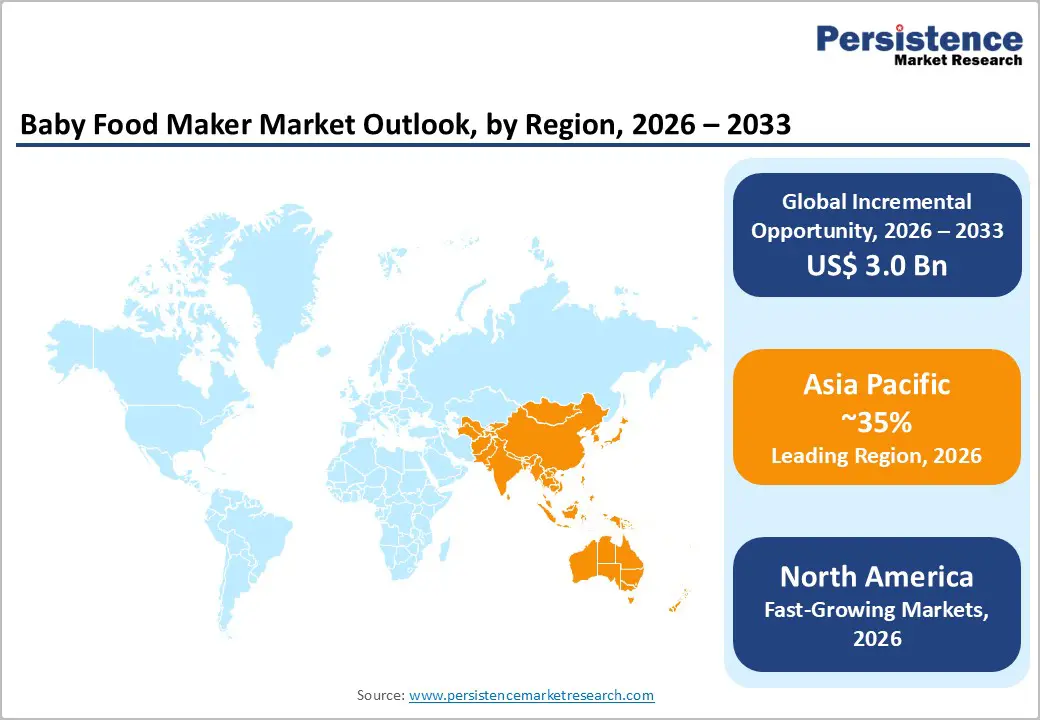

The global Baby Food Maker market size is supposed to be valued at US$ 4.8 billion in 2026 and is projected to reach US$ 7.8 billion by 2033, growing at a CAGR of 7.2% between 2026 and 2033.

This growth trajectory is driven primarily by the global rise in health-conscious parenting, increasing dual-income households, and growing awareness of the nutritional benefits of freshly prepared infant food over commercially processed alternatives. According to the World Health Organization (WHO), appropriate complementary feeding starting at 6 months is critical for infant development, and parents are increasingly investing in purpose-built food preparation appliances that offer steaming, blending, and warming functions in a single device.

Key Industry Highlights:

- Leading Region – Asia Pacific holds approximately 35% of the global baby food maker market in 2025, led by China's expanding middle-income group population.

- Fastest Growing Region – North America is likely to register approximately 28% of the global baby food maker market in 2026, supported by high disposable income levels, a well-established specialty baby retail ecosystem, and strong awareness of paediatric nutrition guidelines promoted by the American Academy of Paediatrics (AAP) and CDC's infant feeding programs.

- Dominant Segment – Food Preparation appliances command approximately 72% of the market in 2026, driven by WHO and AAP complementary feeding guidelines that recommend fresh, home-prepared steamed and pureed infant foods from 6 months of age.

- Fast - Growing Distribution Channel – Online retailers are the fast-growing distribution channel, fueled by millennial parents' digital-native purchasing behaviour, Amazon and Tmall ecosystem dominance, and influencer-driven parenting content that converts awareness to purchase within mobile shopping environments globally.

- Key Opportunity – Manufacturers that align baby food maker products with certified organic ingredient ecosystems, BPA-free material claims, and direct-to-consumer digital strategies bundling recipe apps and paediatric nutrition content can command 15–20% price premiums and build brand loyalty in the premium parenting segment.

DRO Analysis

Drivers - Rising Health-Conscious Parenting and Demand for Fresh, Additive-Free Infant Nutrition

A fundamental shift in parenting philosophy is reshaping the baby food appliance landscape. A 2023 survey by the International Food Information Council (IFIC) found that over 70% of parents prioritize ingredient transparency and minimal processing when selecting food for infants. The WHO and UNICEF jointly advocate for fresh complementary foods as the nutritional gold standard for infants aged 6–24 months, citing risks of excess sodium, sugar, and preservatives in commercial jarred alternatives.

Baby food makers address this demand directly enabling home preparation of steam-cooked, blended, and portioned meals without additives. This behavioural shift is most pronounced in North America and Western Europe, where parents' willingness to pay a premium for food safety and quality control is driving unit value growth across the food preparation product segment.

Dual-Income Households and Time-Saving Appliance Adoption Among Millennial Parents

The global increase in dual-income households is a powerful driver for baby food maker adoption. According to the International Labour Organization (ILO), female labor force participation has steadily grown across both developed and emerging economies, with working mothers seeking time-efficient solutions for infant nutrition management. Modern baby food makers offering all-in-one steam, blend, defrost, and reheat functions within 15–20 minutes directly address this time constraint without compromising nutritional quality.

Millennial and Gen Z parents, who now constitute the dominant parenting demographic, exhibit strong affinity for smart home appliances. The growing availability of Wi-Fi-enabled and app-connected baby food makers from brands such as BEABA and Babymoov is further broadening the addressable market, especially in high-smartphone-penetration markets across Asia Pacific and North America.

Restraints - High Product Cost Limiting Penetration in Price-Sensitive Emerging Markets

Premium baby food makers from established brands are priced between USD 80 and USD 250, placing them out of reach for a significant proportion of households in lower-middle-income economies. The World Bank estimates that over 3 billion people live on less than USD 6.85 per daya threshold at which discretionary spending on specialty infant appliances is severely constrained.

In high-growth markets such as India, Sub-Saharan Africa, and parts of Southeast Asia, traditional food preparation methods or low-cost blenders remain the default choice, restricting formal baby food maker market penetration and limiting the total addressable volume for branded appliance manufacturers.

Low Awareness and Cultural Preferences for Traditional Infant Feeding Practices

In many regions particularly across South Asia, Sub-Saharan Africa, and the Middle East deeply entrenched cultural practices around infant feeding, including extended breastfeeding and family-pot food sharing, reduce the perceived need for dedicated baby food preparation appliances. The WHO's Global Breastfeeding Scorecard documents that over 44% of infants globally are exclusively breastfed to 6 months, after which traditional household-cooked foods predominate.

Limited product awareness, insufficient retail distribution, and the absence of paediatric nutritionist endorsements in these markets collectively restrict category growth beyond affluent urban consumer segments.

Opportunities - Online Retail Expansion and Direct-to-Consumer Channels Unlocking New Consumer Cohorts

E-commerce is the fastest-growing distribution channel for baby food makers, driven by the convergence of parenting content consumption and digital purchasing behaviour among millennial and Gen Z parents. Amazon, Tmall, Flipkart, and Lazada have emerged as dominant retail touchpoints, enabling global brands to reach consumers in markets where physical specialty retail is underdeveloped.

The International Trade Centre (ITC) estimates that online retail penetration for baby and maternity products has grown at a double-digit CAGR since 2020 across Southeast Asia. Direct-to-consumer (DTC) models where manufacturers sell via owned websites with bundled content (weaning guides, recipe apps, paediatric nutrition consultations) are allowing premium brands to build loyalty, command higher average order values, and collect first-party data for product development.

Organic Baby Food Maker Segment: Premium Positioning Aligned with Health Megatrend

The organic segment within baby food makers represents a compelling growth opportunity, as parents increasingly seek appliances specifically designed Forand marketed with organic ingredient preparation. The Organic Trade Association (OTA) reports that U.S. organic baby food sales have consistently outpaced total baby food market growth, with parents demonstrating a 15–20% willingness-to-pay premium for certified organic infant food products.

This behavioural trait extends to appliance choices: organic-positioned baby food makers bundled with organic ingredient starter kits, BPA-free certifications, and partnerships with organic baby food brands (such as Serenity Kids and Little Spoon) are commanding higher average selling prices and stronger brand loyalty. As EU Organic Regulation (2018/848) and similar national frameworks elevate organic food standards globally, manufacturers that credibly align their appliance branding with organic nutrition positioning will access growing premium consumer segment.

Category-wise Analysis

Product Type Insights

Food preparation appliances represent the dominant segment within the Product Type category, accounting for approximately 72% market share in 2026. This leadership reflects the core consumer use case: parents of infants aged 6–18 months require reliable steaming and blending functionality to prepare pureed vegetables, fruits, and proteins as part of structured complementary feeding regimens endorsed by the WHO and American Academy of Paediatrics (AAP).

Leading food preparation models such as the BEABA Babycook Neo and Philips Avent 4-in-1 Healthy Baby Food Maker offer steaming, blending, defrosting, and reheating in a single unit, reducing kitchen clutter and preparation time. The segment benefits from strong repurchase intent as parents progress through different feeding stages, driving accessory and replacement blade sales that extend product lifetime value.

Nature Insights

Conventional baby food makers hold the dominant position in the nature category, representing approximately 68% market share in 2026, owing to broader price accessibility and wider retail availability. However, the organic segment is the fastest-growing sub-category, fueled by the health-premium parenting trend. Manufacturers are responding by obtaining certifications such as OEKO-TEX Standard 100 for food-contact materials and partnering with organic ingredient subscription services, positioning organic baby food maker lines as premium lifestyle purchases with strong gifting appeal among health-conscious parent communities.

Distribution Channel Insights

Supermarkets and hypermarkets remain the leading distribution channel for baby food makers, capturing approximately 38% share in 2026. Established retail chains such as Walmart, Carrefour, Target, and Tesco provide high physical visibility, trial-enabling shelf placement, and trusted purchase environments that are particularly valued by first-time parents making a considered appliance investment.

Online retailers represent the fast-growing channel, driven by competitive pricing, product review ecosystems, and the ability to offer broader assortments than physical shelf space permits. The Global E-commerce Index by UNCTAD confirms that baby and childcare product categories are among the highest e-commerce conversion segments globally, with parenting forums and Instagram/YouTube influencer content driving purchase intent and brand discovery among millennial parents across all geographies.

Regional Insights

North America Baby Food Maker Market Trends & Analysis

North America holds approximately 28% of the global baby food maker market in 2026, supported by high disposable income levels, a well-established specialty baby retail ecosystem, and strong awareness of paediatric nutrition guidelines promoted by the American Academy of Paediatrics (AAP) and CDC's infant feeding programs. The region's high smartphone penetration drives adoption of app-connected smart baby food makers, while the organic parenting trend sustains premium-tier demand.

U.S. Baby Food Maker Market Size

The U.S. Baby Food Maker market is estimated at approximately US$ 1.1 billion in 2026, representing roughly 82% of North American demand. High average unit selling prices (USD 90–220 for premium models), strong online retail penetration via Amazon, and the 4 million annual U.S. births reported by the CDC collectively sustain a robust replacement and new-parent buyer cycle, with gifting through baby registries at Buy Buy Baby and Target forming a critical demand channel.

Europe Baby Food Maker Market Trends, Drivers, & Insights

Europe accounts for approximately 24% of the global baby food maker market share in 2026. Strong EU food safety and materials regulations, including EU Regulation 10/2011 on plastic food-contact materials, drive consumer preference for certified, premium appliances. Parental leave policies across Scandinavian and Western European countries support extended home food preparation periods, sustaining above-average adoption of multi-function baby food preparation systems.

Germany Baby Food Maker Market Size

Germany represents the largest European market for baby food makers, estimated at approximately US$ 240 million in 2025. Germany's high-income households, stringent DIN/EN quality standards culture, and strong domestic preference for established European brands such as BEABA (France) and Babymoov position it as both a volume leader and a premium-tier benchmark market, contributing approximately 35% of European revenues.

U.K. Baby Food Maker Market Size

The U.K. Baby Food Maker market is estimated at approximately US$ 140–160 million in 2025. The NHS Start for Life campaign and Public Health England's complementary feeding guidelines actively support fresh home-cooked infant food, reinforcing appliance adoption. UK-specific brands such as Tommee Tippee and the strong retail presence of Mothercare and Boots drive category visibility among new parents.

France Baby Food Maker Market Size

France is estimated at approximately US$ 130 million in 2025 and holds a significant position as the home market of BEABA, the global category pioneer. France's PMI (Protection Maternelle et Infantile) public health framework emphasizes fresh food preparation for infants, and the French parenting culture's strong culinary identity translates into above-average baby food maker penetration relative to birth rates across comparable European economies.

Asia Pacific Baby Food Maker Market Drivers & Analysis

Asia Pacific is the leading region with approximately 35% of the global Baby Food Maker market share in 2025. China, driven by its post-one-child-policy birth rate recovery, expanding middle class, and intense parental investment in child development, is the single largest national market in the region. Rising urbanization, increasing female workforce participation, and rapid e-commerce penetration across Tmall, JD.com, and Shopee collectively amplify demand for premium baby food preparation appliances.

China Baby Food Maker Market Size

China's Baby Food Maker market is estimated at approximately US$ 520 million in 2026, representing approximately 42% of the demand in the Asia Pacific. Post-three-child policy (2021) incentives and heightened food safety consciousness, following historical infant formula deceptions, have created a huge demand for home food preparation appliances. Domestic brands such as Bear Electric and Joyoung compete with global entrants through competitive pricing and Tmall ecosystem integration.

India Baby Food Maker Market Size

India's Baby Food Maker market is estimated at approximately US$ 160 million in 2026, supported by India's annual birth cohort of approximately 25 million per the Office of the Registrar General & Census Commissioner of India. Rising middle-class aspirations in Tier-1 and Tier-2 cities, growing awareness through pediatrician networks, and expanding online retail via Flipkart and Amazon India are accelerating category introduction and repeat purchases among urban parents.

Japan Baby Food Maker Market Size

Japan's Baby Food Maker market is estimated at approximately US$ 110 million in 2025. Despite Japan's declining birth rate of 729,000 births in 2023 per the Ministry of Health, Labour and Welfare (MHLW), Japan's market sustains value through ultra-premium product positioning, advanced technology features (precise temperature control, smart connectivity), and high per-unit spending by Japanese parents who rank infant nutrition investment among the highest globally.

Competitive Landscape

The global baby food maker market is moderately fragmented, with a mix of dedicated infant appliance specialists and large consumer electronics and small-appliance conglomerates. BEABA, Babymoov, Philips Avent, and NUK lead through brand heritage, pediatrician endorsement networks, and continuous product innovation, including smart connectivity and multi-function integration.

Key differentiators include BPA-free material certifications, EU food safety compliance, and bundled app ecosystems for recipe guidance. Emerging business model trends include subscription-based organic ingredient partnerships, DTC digital sales strategies, and co-branding with paediatric nutrition authorities. Asian manufacturers Bear Electric and Joyoung are intensifying competition through aggressive pricing and rapid e-commerce channel penetration across the Asia Pacific.

Key Developments:

- In July 2025, Danone announced the completion of its acquisition of a majority stake in Kate Farms, a U.S.-based provider of plant-based, organic nutrition products for both medical and everyday needs. Founded in 2012 in Santa Barbara, California, Kate Farms was established by Richard and Michelle Laver to address their daughter Kate's medical feeding needs.

- In March 2025, BEABA launched the Babycook Neo Connected, a Wi-Fi-enabled all-in-one baby food maker with an integrated nutrition app offering age-specific weaning recipes, digital steaming presets, and paediatric dietitian-curated meal plans for infants aged 4–24 months.

Global Baby Food Maker Market – Key Insights & Details

| Key Insights | Details |

|---|---|

|

Historical Market Value (2020) |

US$ 3.5 Bn |

|

Current Market Value (2026) |

US$ 4.8 Bn |

|

Projected Market Value (2033) |

US$ 7.8 Bn |

|

CAGR (2026-2033) |

7.2% |

|

Leading Region |

Asia Pacific, 35% share |

|

Dominant Application |

Food Preparation, 72% share |

|

Top-ranking Product |

Conventional baby food, 68% |

|

Incremental Opportunity |

US$ 3.0 Bn |

Companies Covered in Baby Food Maker Market

- BEABA (SAS BEABA)

- Philips Avent (Koninklijke Philips N.V.)

- Babymoov

- NUK (MAPA GmbH)

- Cuisinart (Conair LLC)

- Baby Brezza

- Infantino

- Tommee Tippee (Jackel International)

- Chicco (Artsana Group)

- Nutribullet Baby (NutriBullet LLC)

- Hamilton Beach Brands

- Kiinde

- Bear Electric (Bear Home Appliances Co., Ltd.)

- Joyoung Co., Ltd

- UFI Filters

Frequently Asked Questions

The global baby food maker market is estimated at approximately US$ 4.8 billion in 2026, growing at a CAGR of 7.2% through 2033, driven by health-conscious parenting trends, rising dual-income households, WHO complementary feeding guidelines, and expanding e-commerce distribution channels globally.

Primary demand drivers include the global rise in health-conscious parenting, with over 70% of parents (IFIC 2023) prioritizing fresh, additive-free infant food, combined with growing dual-income households seeking time-saving all-in-one appliances, and the millennial generation's strong affinity for smart, app-connected kitchen devices that align with digital-native parenting lifestyles.

Food preparation appliances hold the leading position with approximately 72% market share in 2026. This dominance is driven by WHO and American Academy of Paediatrics recommendations for fresh home-prepared complementary foods from 6 months, and the widespread adoption of multi-function steam-and-blend units from brands such as BEABA, Philips Avent, and Babymoov across developed markets.

Asia Pacific leads with approximately 35% share in 2026, anchored by China's post-three-child-policy parenting investment trends.

The leading companies include BEABA (France), the category pioneer with 50+ country distribution; Philips Avent (Netherlands), leveraging Philips' global clinical brand equity; and Babymoov (France), a European premium innovator.