- Automotive Components & Materials

- Automotive Occupant Sensing System Market

Automotive Occupant Sensing System Market Size, Share, and Growth Forecast 2026 - 2033

Automotive Occupant Sensing System Market by Product Type (Pressure Sensors, Weight Sensors, Seat Belt Sensors, Airbag Sensors, Cameras, Strain Gauges, Ultrasonic Sensors, and Infrared / Capacitive Sensors), Mounting Location (Driver Side and Passenger Side), Vehicle Type, Sales Channel, and Regional Analysis 2026 - 2033

Automotive Occupant Sensing System Market Size and Share Analysis

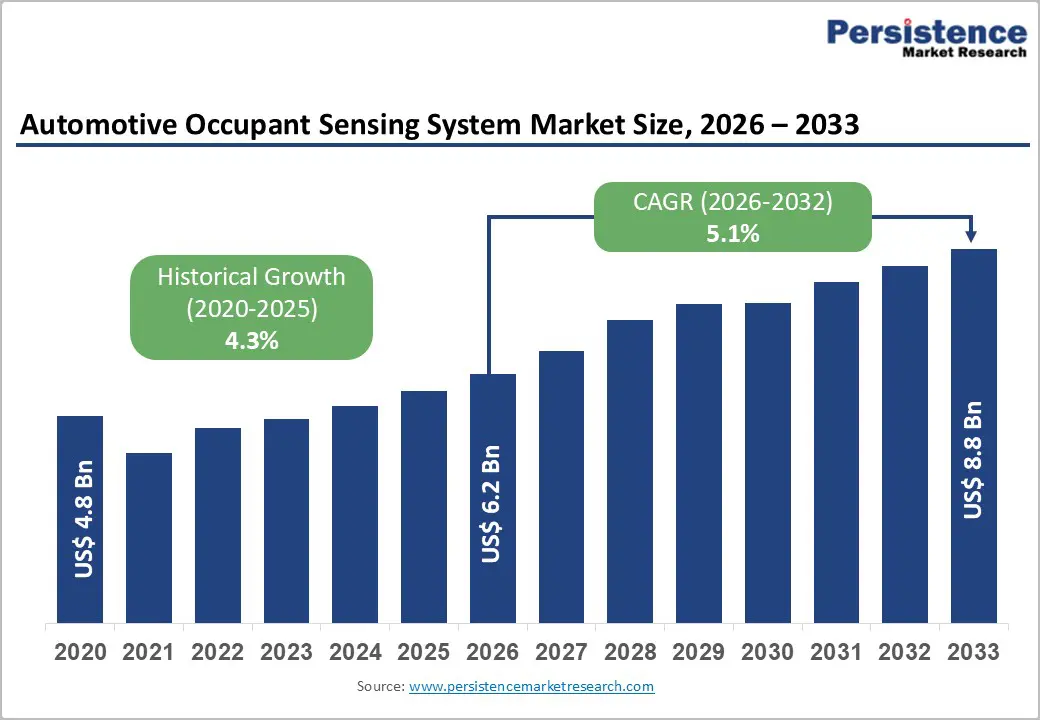

The global Automotive Occupant Sensing System Market size is likely to be valued at US$ 6.2 billion in 2026 and is projected to reach US$ 8.8 billion by 2033, growing at a CAGR of 5.1% between 2026 and 2033.

This growth is primarily driven by stringent vehicle safety regulations mandating advanced occupant detection systems and the accelerating adoption of autonomous and electric vehicles requiring sophisticated sensor integration. Additionally, rising consumer awareness about passenger safety features and insurance premium incentives for vehicles equipped with advanced safety systems is propelling market expansion across developed and emerging economies.

Key Industry Highlights:

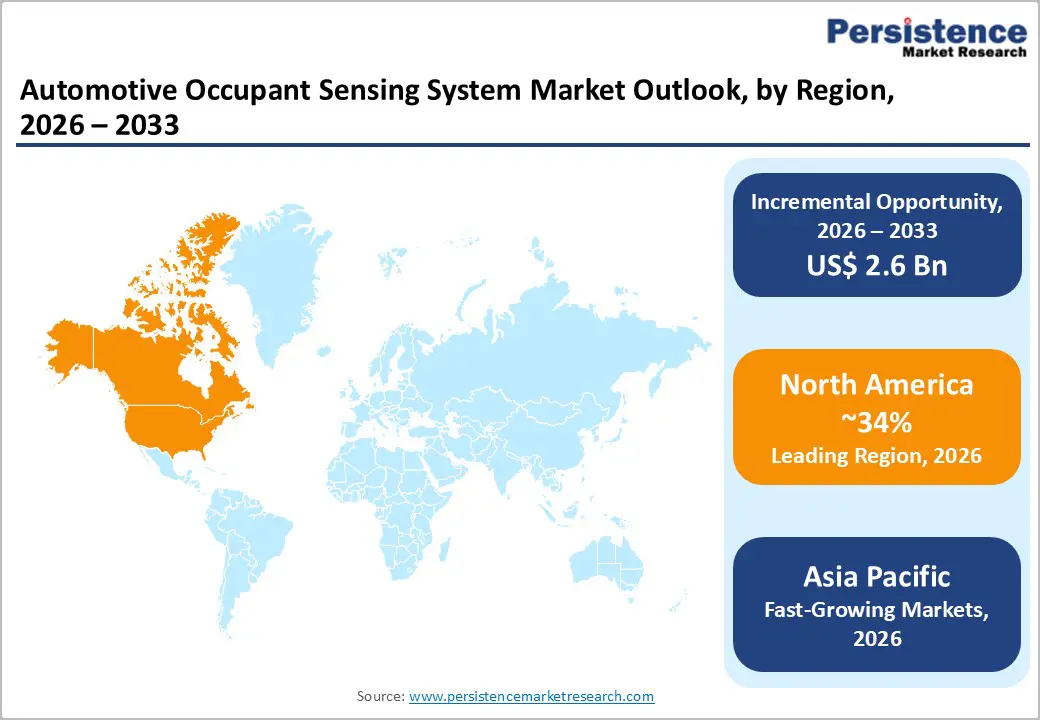

- Leading Region: North America leads the global Automotive Occupant Sensing System Market with approximately 34% market share, driven by stringent FMVSS 208 compliance requirements, mature regulatory frameworks enforced by NHTSA, and strong consumer preference for advanced safety features reflected in IIHS safety ratings and insurance premium structures.

- Growing Region: Asia Pacific represents the fastest-growing regional market with a projected CAGR of 6.3% during 2026-2033, fueled by explosive automotive production growth in China, India, and ASEAN countries, evolving safety regulations mandating occupant protection systems, and increasing consumer safety awareness across emerging middle-class populations.

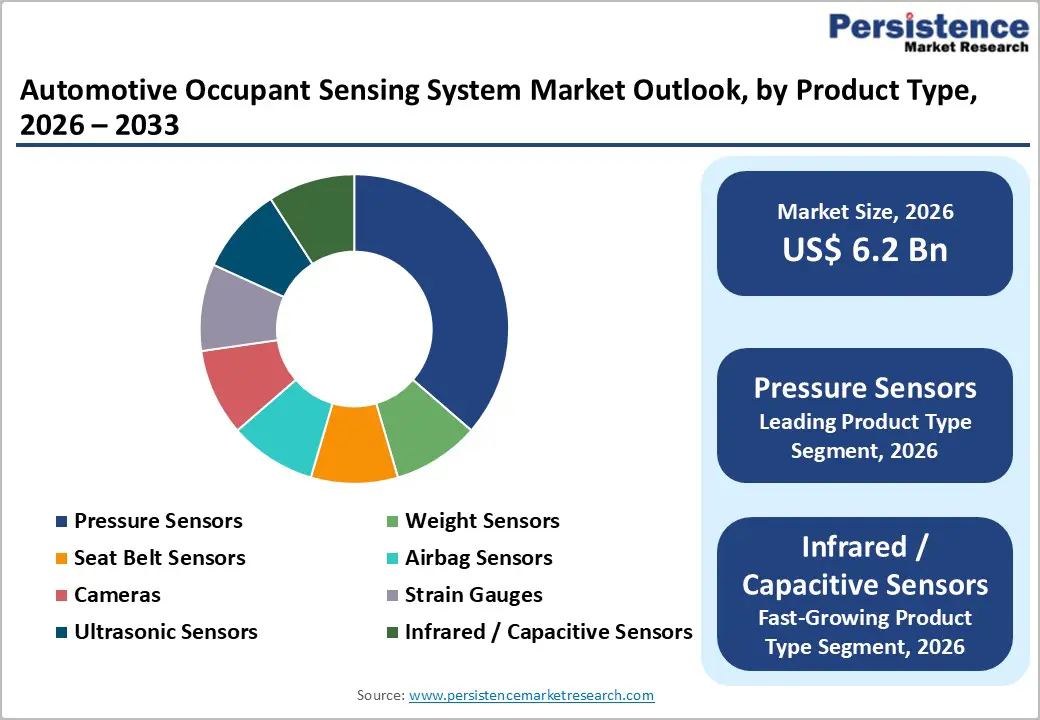

- Dominant Product Type: Pressure sensors dominate the product type category with 32% market share, reflecting widespread adoption in cost-effective occupant classification systems, proven reliability across diverse climatic conditions, and regulatory acceptance as primary sensing technology for airbag deployment decisions across major automotive markets globally.

- Growing Vehicle Type: Electric vehicles emerge as the fastest-growing vehicle type segment with an anticipated CAGR of 8.7% through 2032, driven by sophisticated cabin monitoring requirements for autonomous features, battery management optimization through occupant detection, and premium positioning facilitating advanced sensor integration.

- Key Opportunity: Integration of health monitoring and wellness features represents the most significant market opportunity.

| Key Insights | Details |

|---|---|

|

Global Automotive Occupant Sensing System Market Size (2026E) |

US$ 6.2 Bn |

|

Market Value Forecast (2033F) |

US$ 8.8 Bn |

|

Projected Growth CAGR (2026-2033) |

5.1% |

|

Historical Market Growth (2020-2025) |

4.3% |

Market Dynamics

Drivers - Stringent Global Vehicle Safety Regulations Mandating Occupant Detection Systems

Regulatory frameworks across major automotive markets are compelling manufacturers to integrate advanced occupant sensing technologies. The National Highway Traffic Safety Administration (NHTSA) in the United States enforces Federal Motor Vehicle Safety Standard (FMVSS) 208, which requires advanced airbag systems with occupant classification capabilities to prevent injury from inappropriate airbag deployment. Similarly, the European New Car Assessment Programme (Euro NCAP) has incorporated occupant monitoring systems into its safety rating criteria since 2020, directly influencing consumer purchasing decisions.

In 2023, the Ministry of Road Transport and Highways in India proposed amendments to Automotive Industry Standard (AIS) 145 to mandate seat belt reminders and occupant detection for front seats in all passenger vehicles. These regulatory pressures are driving original equipment manufacturers to invest heavily in sensor integration, with the Insurance Institute for Highway Safety (IIHS) reporting that vehicles equipped with advanced occupant sensing systems demonstrate 35% fewer fatalities in frontal crashes compared to vehicles with basic systems.

Rapid Proliferation of Electric and Autonomous Vehicles Requiring Advanced Sensor Integration

The global transition toward electrification and autonomous driving is fundamentally reshaping occupant sensing requirements. Electric vehicles manufactured by companies like Tesla, BYD, and Volkswagen incorporate sophisticated cabin monitoring systems that integrate weight sensors, cameras, and capacitive sensors to optimize battery management and personalize user experiences. According to the International Energy Agency (IEA), electric vehicle sales reached 14 million units globally in 2023, representing a 35% year-over-year increase. Autonomous vehicle platforms require continuous occupant monitoring to ensure safe handover procedures between automated and manual driving modes, as specified in SAE International's J3016 taxonomy for driving automation.

Continental AG and Robert Bosch have developed multi-modal sensing systems combining pressure sensors, infrared cameras, and machine learning algorithms to detect occupant position, posture, and vital signs. The Society of Automotive Engineers (SAE) projects that by 2030, approximately 60% of new vehicles will feature Level 2+ automation capabilities, necessitating advanced occupant monitoring to comply with emerging safety standards.

Restraints - High Integration Costs and Complexity in Legacy Vehicle Platforms

The integration of advanced occupant sensing systems into existing vehicle architecture presents high cost and technical challenges for manufacturers. Retrofitting pressure sensors, weight sensors, and camera-based systems requires substantial modifications to seat frames, electrical harnesses, and electronic control units, with integration costs ranging from $150 to $400 per vehicle, depending on system sophistication. Legacy platform vehicles face compatibility issues with modern sensor protocols, requiring expensive gateway modules and software updates.

Small and mid-sized automotive manufacturers, particularly in price-sensitive markets, struggle to justify these investments given thin profit margins on entry-level vehicle segments. The Center for Automotive Research estimates that 45% of vehicles produced globally still utilize platforms designed before 2015, lacking the electronic infrastructure necessary for seamless sensor integration without significant re-engineering expenses.

Consumer Privacy Concerns Regarding In-Cabin Monitoring Technologies

The deployment of camera-based occupant sensing systems has triggered significant privacy concerns among consumers and regulatory bodies. Organizations like the Electronic Privacy Information Center (EPIC) have raised questions about data collection, storage, and potential misuse of biometric information captured by in-cabin cameras. In 2024, the European Data Protection Board (EDPB) issued guidelines requiring explicit consent for continuous cabin monitoring in non-driving scenarios, complicating system activation protocols for manufacturers.

Many potential vehicle buyers feel uncomfortable with camera-based monitoring systems in cars. They worry that these systems could record them without their knowledge or that their personal data could be hacked or misused. This concern is stronger in countries where people are very conscious about data privacy. Because of this, some customers may hesitate to buy vehicles equipped with such features. To overcome this challenge, manufacturers need to clearly explain how data is collected and used, ensure strong data protection measures, and design secure systems that prevent tampering. Building trust through transparency and strong privacy safeguards will be essential for wider adoption.

Opportunity - Expanding Aftermarket Segment for Retrofit Safety Solutions in Existing Vehicle Fleets

The aftermarket channel presents substantial growth opportunities as millions of older vehicles lack modern occupant sensing capabilities. Independent automotive retailers and service chains are increasingly offering retrofit kits combining seat belt sensors, weight sensors, and basic occupant detection modules compatible with vehicles manufactured after 2010. According to the Automotive Aftermarket Suppliers Association (AASA), the global automotive aftermarket reached $455 billion in 2023, with safety components representing a 12% share and growing at 6.8% annually. Insurance companies in markets like the United States, Germany, and Japan are offering premium discounts of 5% to 15% for vehicles equipped with aftermarket occupant sensing systems, creating financial incentives for consumers to upgrade older vehicles.

Companies such as Key Safety Systems Inc. and Lear Corporation have launched modular retrofit solutions priced between $200 and $600, targeting the estimated 400 million passenger vehicles globally that lack advanced occupant detection. This aftermarket opportunity is particularly significant in emerging economies where vehicle replacement cycles exceed 12 years, and consumers seek cost-effective safety upgrades.

Integration with Health Monitoring and Wellness Features in Premium Vehicle Segments

Automotive manufacturers are exploring occupant sensing systems as platforms for advanced health monitoring and personalized wellness features, particularly in premium and luxury vehicle segments. Volvo has demonstrated prototype systems using strain gauges and capacitive sensors integrated into seats to monitor heart rate, breathing patterns, and stress levels, with plans to commercialize these features by 2026. The Consumer Technology Association (CTA) reports growing consumer interest in vehicle-integrated health monitoring, with 42% of premium vehicle buyers willing to pay additional amounts ranging from $800 to $1,500 for comprehensive wellness monitoring systems.

Texas Instruments and Analog Devices are developing specialized integrated circuits optimized for automotive health sensing applications, enabling real-time vital sign monitoring with medical-grade accuracy. Regulatory developments are also favorable, with the Food and Drug Administration (FDA) establishing guidelines for automotive health monitoring devices in 2024. This convergence of automotive safety and healthcare technology creates opportunities for sensor manufacturers to develop high-value integrated solutions targeting the growing wellness-conscious consumer segment, particularly in markets like North America and Western Europe where premium vehicles command 25% to 35% of total sales.

Category-wise Analysis

Product Type Insights

Pressure sensors dominate the product type category, accounting for approximately 32% of the market share, driven by their cost-effectiveness, reliability, and widespread adoption in airbag deployment systems. These sensors utilize piezoelectric or piezoresistive technologies to measure force distribution across seat surfaces, enabling accurate occupant classification required by regulations like FMVSS 208. According to the Japan Automobile Manufacturers Association (JAMA), pressure sensor-based systems are deployed in over 85% of new passenger vehicles manufactured in Japan, South Korea, and China due to their proven performance in diverse climatic conditions and ability to function independently without external calibration.

Autoliv Inc. reports that advanced pressure sensor arrays can differentiate between 12 distinct occupant classifications, including child seats, small adults, and large adults, with accuracy exceeding 98%. The integration of machine learning algorithms with pressure sensor data is further enhancing classification accuracy, with Robert Bosch demonstrating systems capable of detecting occupant posture changes and predicting potential out-of-position scenarios 200 milliseconds before airbag deployment decisions.

Vehicle Type Insights

Passenger cars represent the leading segment in the vehicle type category, capturing approximately 68% of the market share, reflecting the segment's dominant global production volumes and regulatory focus on occupant safety. Within passenger cars, SUVs are experiencing the fastest growth, driven by their increasing market penetration and premium positioning that facilitates advanced safety feature integration. The International Organization of Motor Vehicle Manufacturers (OICA) reports that global passenger car production reached 66.8 million units in 2023, with SUVs accounting for 48% of this volume compared to 38% in 2018.

Hatchbacks and sedans continue to maintain substantial market presence, particularly in price-sensitive markets like India, Brazil, and Southeast Asia, where these body styles represent 60% to 70% of passenger vehicle sales. Hyundai Mobis Co., Ltd. has developed cost-optimized occupant sensing solutions specifically for compact passenger cars, utilizing simplified sensor arrays priced 30% to 40% lower than premium SUV systems while maintaining compliance with basic regulatory requirements. The growing adoption of electric vehicles within the passenger car segment is creating additional demand for advanced occupant sensing systems by 2033.

Mounting Location Insights

Driver side occupant sensing systems hold approximately 56% of the market share, reflecting prioritization of driver safety in regulatory frameworks and the higher complexity of driver monitoring requirements in autonomous and semi-autonomous vehicles. However, passenger side systems are experiencing rapid growth, with regulatory bodies increasingly mandating dual-side coverage for comprehensive occupant protection. The NHTSA requires occupant classification systems on both front seats in vehicles sold in the United States, while Euro NCAP awards higher safety ratings to vehicles demonstrating effective passenger-side occupant detection and airbag optimization.

Continental AG reports that integrated dual-side occupant sensing systems, which share electronic control units and calibration data between driver and passenger positions, offer 15% to 20% cost advantages compared to independent single-side solutions. Technical advances in sensor miniaturization are enabling manufacturers to incorporate equivalent sensing capabilities across both seating positions without significant weight or packaging penalties. The Insurance Institute for Highway Safety data indicates that passenger-side occupant sensing systems have contributed to a 22% reduction in passenger fatalities from inappropriate airbag deployments since their widespread adoption in 2015.

Sales Channel Insights

OEM (Original Equipment Manufacturer) channels dominate approximately 87% of the market share, as occupant sensing systems are typically integrated during vehicle manufacturing to ensure proper calibration, certification compliance, and warranty coverage. Major automotive manufacturers, including Volkswagen, Toyota, General Motors, and Stellantis, maintain exclusive partnerships with tier-one suppliers like ZF Friedrichshafen AG, Lear Corporation, and Delphi Automotive PLC for occupant sensing system integration. According to IHS Markit, 94% of vehicles equipped with advanced occupant sensing systems receive these features as factory-installed equipment, reflecting the technical complexity of proper installation and calibration.

The aftermarket channel is demonstrating accelerated growth, particularly in markets with large aging vehicle populations and increasing safety awareness. Companies like Nexus RV LLC and Tiffin Motorhomes Inc. are expanding retrofit solutions for recreational vehicles and commercial applications. The Specialty Equipment Market Association (SEMA) reports that aftermarket occupant sensing systems sales grew 14% annually between 2020 and 2023, driven by insurance incentives and consumer demand for safety upgrades in vehicles lacking factory-installed systems.

Regional Trends

North America Automotive Occupant Sensing System Market Trends

The United States maintains market leadership in North America, driven by rigorous enforcement of FMVSS 208 and the region's early adoption of advanced safety technologies. The NHTSA has mandated advanced airbag systems with occupant classification since 2006, establishing a mature regulatory framework that continues to evolve with emerging technologies. In November 2023, NHTSA proposed updates to occupant protection standards requiring enhanced detection capabilities for rear-seat occupants and integration with automated driving systems by 2027. This regulatory progression is driving significant investment in next-generation sensing technologies by suppliers operating in the region.

The North American market benefits from a robust innovation ecosystem, with companies like Autoliv Inc., Lear Corporation, and Key Safety Systems Inc. maintaining advanced research facilities focused on sensor fusion technologies. According to the Automotive Safety Council, approximately $2.3 billion was invested in occupant safety research and development across North America in 2023. The Insurance Institute for Highway Safety continues to incorporate occupant sensing system performance into its crashworthiness ratings, with Top Safety Pick+ awards requiring demonstration of advanced occupant detection capabilities across multiple crash scenarios.

Europe Automotive Occupant Sensing System Market Trends

Europe maintains a leadership position in occupant sensing system innovation, with Germany, France, the United Kingdom, and Spain driving technological advancement and regulatory harmonization through Euro NCAP and European Commission directives. The European Union's General Safety Regulation (GSR), which became mandatory in July 2024, requires advanced occupant monitoring systems in all new vehicle type approvals, significantly expanding market coverage beyond previous voluntary adoption patterns. Germany, as Europe's largest automotive market, accounts for approximately 28% of the region's occupant sensing system demand, with manufacturers like Robert Bosch, Continental AG, and ZF Friedrichshafen AG headquartered in the country and maintaining substantial market influence.

Euro NCAP protocols introduced in 2023 assign 15% of the overall safety rating to occupant monitoring and protection systems, incentivizing manufacturers to deploy advanced multi-sensor solutions. The European Automobile Manufacturers' Association (ACEA) reports that 89% of passenger vehicles sold in Western Europe during 2023 featured advanced occupant sensing systems, compared to 67% in 2019. France has implemented additional incentives through its Bonus-Malus system, offering financial benefits to consumers purchasing vehicles with comprehensive safety features, including advanced occupant detection. The United Kingdom, despite Brexit, maintains alignment with EU safety standards through its Vehicle Certification Agency, ensuring continued technology harmonization. Spain's growing automotive manufacturing sector, which produced 2.45 million vehicles in 2023 according to ANFAC (Spanish Association of Automobile and Truck Manufacturers), is increasingly focused on integrating advanced occupant sensing systems to maintain competitiveness in premium export markets.

Asia Pacific Automotive Occupant Sensing System Market Trends

Asia Pacific represents the fastest-growing regional market, driven by massive automotive production volumes in China, Japan, South Korea, and emerging manufacturing hubs in India and ASEAN countries. China, as the world's largest automotive market, produced 30.2 million vehicles in 2023 according to the China Association of Automobile Manufacturers (CAAM), with occupant sensing system penetration increasing from 52% in 2020 to 71% in 2023 as domestic manufacturers upgrade safety specifications to compete with international brands. The Ministry of Industry and Information Technology (MIIT) in China has proposed new technical standards for intelligent vehicle safety systems, including mandatory occupant monitoring for vehicles with Level 2+ autonomous capabilities by 2026.

Japan maintains technological leadership in sensor miniaturization and integration, with companies like Takata Corporation (now operating under Joyson Safety Systems) and Denso Corporation developing next-generation capacitive and ultrasonic sensing solutions. The Japan Automobile Standards Internationalization Center (JASIC) collaborates with ISO to develop global standards for occupant sensing system performance. India's automotive market is experiencing rapid safety regulation evolution, with the Ministry of Road Transport and Highways mandating six airbags in passenger vehicles from October 2023, driving increased demand for occupant classification systems. ASEAN countries, including Thailand, Indonesia, and Vietnam are harmonizing safety standards through the ASEAN New Car Assessment Programme (NCAP), which incorporates occupant protection ratings similar to Euro NCAP. Manufacturing cost advantages in the region are enabling Asia Pacific suppliers to compete aggressively in global markets, with China and India emerging as significant exporters of automotive safety components to Europe and North America.

Competitive Landscape

The automotive occupant sensing system market exhibits moderate consolidation, characterized by a mix of established tier-one automotive suppliers and specialized sensor technology companies. The top five players, including Autoliv Inc., Robert Bosch, Continental AG, ZF Friedrichshafen AG, and Lear Corporation, collectively account for approximately 62% of the global market share, reflecting significant barriers to entry related to regulatory certification, automotive qualification processes, and intellectual property portfolios. However, the market maintains competitive dynamics through continuous technology evolution, with companies investing 8% to 12% of revenue in research and development focused on sensor fusion, artificial intelligence integration, and miniaturization.

Key differentiators employed by market leaders include proprietary algorithms for occupant classification, integration capabilities across multiple vehicle platforms, and established relationships with major automotive OEMs spanning decades. Emerging business model trends include software-as-a-service offerings for over-the-air calibration updates, outcome-based pricing tied to safety performance improvements, and strategic partnerships between traditional automotive suppliers and technology companies specializing in computer vision and machine learning. Regional players in Asia Pacific markets are gaining market share through cost-competitive solutions optimized for high-volume segments, while established European and North American suppliers maintain premium positioning through advanced feature sets and proven reliability records.

Key Market Developments

- In September 2024, ZF Friedrichshafen AG received a $400 million contract from a leading Chinese electric vehicle manufacturer to supply integrated occupant sensing and airbag control systems for a new platform launching in 2025, marking the company's largest single occupant safety system contract in the Asia Pacific region.

- In March 2024, Continental AG unveiled its next-generation multi-modal occupant sensing platform integrating pressure sensors, infrared cameras, and radar technology at the Geneva International Motor Show, demonstrating 99.2% classification accuracy across 15 distinct occupant scenarios and achieving ISO 26262 ASIL-D functional safety certification.

- In January 2024, Autoliv Inc. announced a strategic partnership with NVIDIA to develop AI-powered occupant monitoring systems utilizing advanced computer vision algorithms capable of detecting occupant attention levels, drowsiness indicators, and medical emergencies in real-time, with initial deployment planned for 2026 model year vehicles from multiple OEM partners.

Companies Covered in Automotive Occupant Sensing System Market

- Takata Corporation

- Autoliv Inc.

- Robert Bosch

- Continental AG

- Delphi Automotive PLC

- Hyundai Mobis Co., Ltd.

- Key Safety Systems Inc.

- Lear Corporation

- ZF Friedrichshafen AG

- Volvo

- Lutron Electronics

- Leviton Manufacturing Company

- Texas Instruments

- Nexus RV LLC

- Tiffin Motorhomes Inc.

- Denso Corporation

Frequently Asked Questions

The global Automotive Occupant Sensing System Market is projected to reach US$ 8.8 Bn by 2033, growing from US$ 6.2 Bn in 2026 at a CAGR of 5.1% during the forecast period, driven by stringent safety regulations, increasing vehicle production, and growing adoption of advanced driver assistance systems across global automotive markets.

The market is primarily driven by mandatory safety regulations such as FMVSS 208 in the United States and Euro NCAP requirements in Europe, which require advanced occupant classification for optimized airbag deployment.

Pressure sensors lead the product type category with approximately 32% market share, attributed to their cost-effectiveness, proven reliability in diverse operating conditions, widespread regulatory acceptance, and capability to accurately classify occupants for airbag deployment decisions.

North America maintains market leadership with approximately 34% global market share, driven by stringent regulatory enforcement through NHTSA's FMVSS 208 standards, mature safety rating systems from IIHS influencing consumer choices, robust innovation ecosystem with major suppliers like Autoliv and Lear Corporation.

The integration of health monitoring and wellness features in premium vehicle segments represents the most significant opportunity, with manufacturers like Volvo developing systems combining occupant sensing with vital sign monitoring, stress detection, and personalized comfort optimization.

Key market players include Autoliv Inc., Robert Bosch GmbH, Continental AG, ZF Friedrichshafen AG, and Lear Corporation, which collectively control approximately 62% of the global market.