- Industrial Machinery

- Automatic Paper Cutter Market

Automatic Paper Cutter Market Size, Share, and Growth Forecast, 2026 - 2033

Automatic Paper Cutter Market by Product Type (Guillotine, Rotary Trimmers, Stack, Laser), Application (Commercial Printing, Office Use, Industrial Use, Others), Installation (Portable, Stationary), and Regional Analysis for 2026-2033

Automatic Paper Cutter Market Share and Trends Analysis

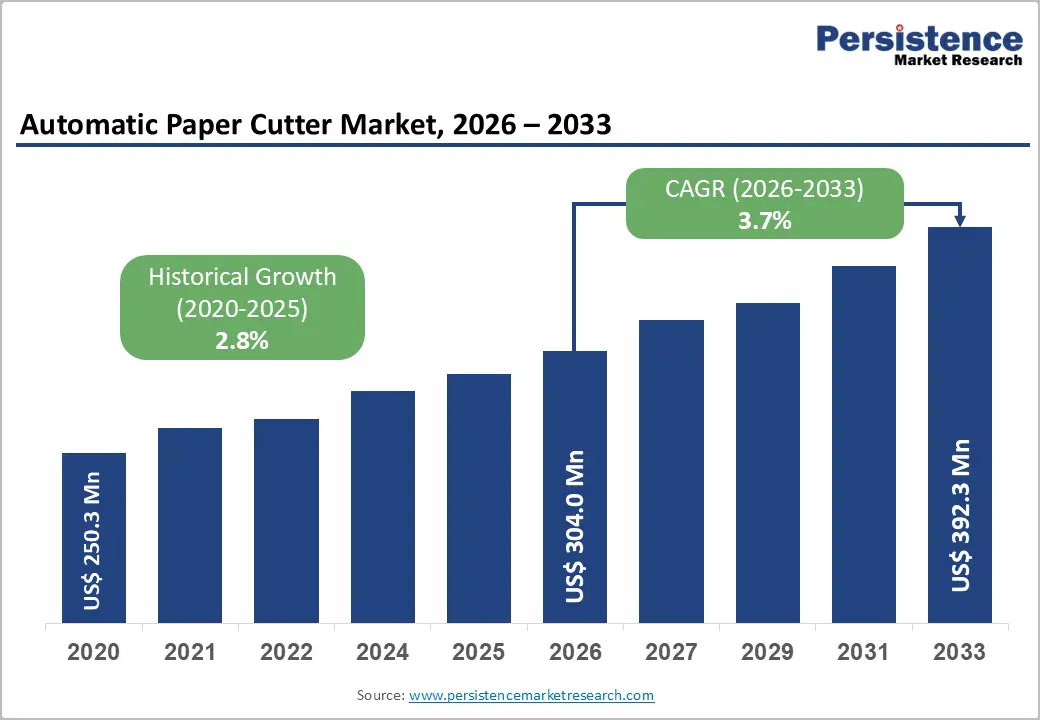

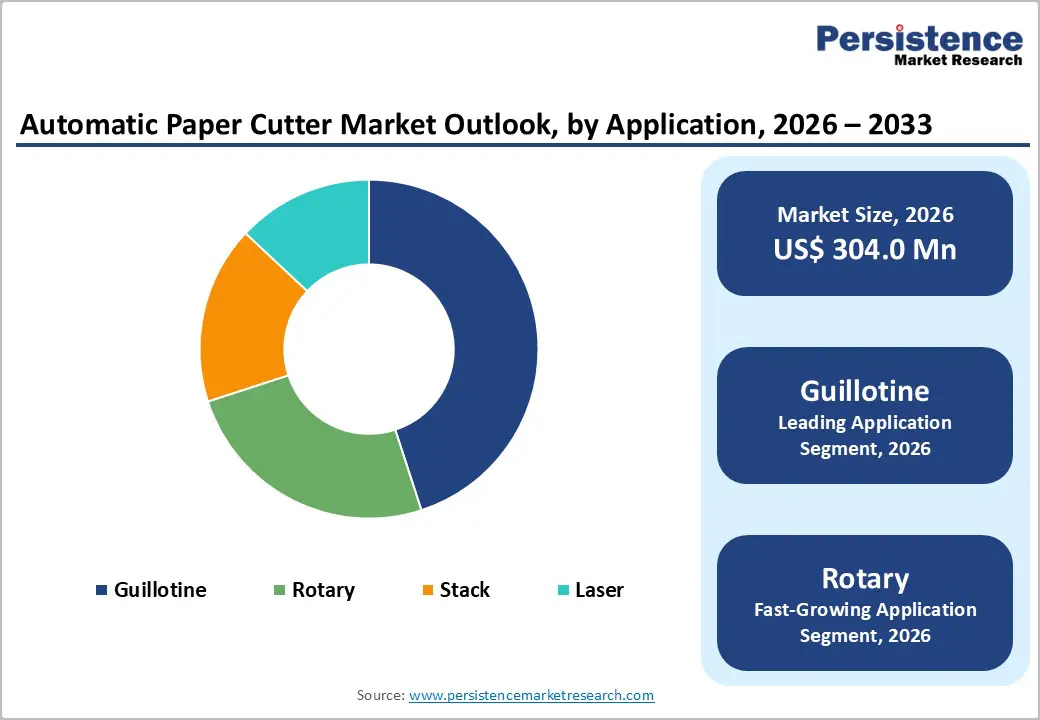

The global automatic paper cutter market size is likely to be valued at US$ 304.0 million in 2026, and is projected to reach US$ 392.3 million by 2033, growing at a CAGR of 3.7% during the forecast period 2026−2033.

The steady upward trajectory of the market is underpinned by the rising demand for precision cutting equipment across commercial printing, publishing, packaging, and office automation sectors. Automation adoption in manufacturing facilities has accelerated following post-pandemic supply chain restructuring, increasing capital expenditure on time-saving, high-throughput equipment. Growing e-commerce activity is simultaneously driving the demand for customized packaging, which requires accurate paper and board cutting solutions.

Key Industry Highlights

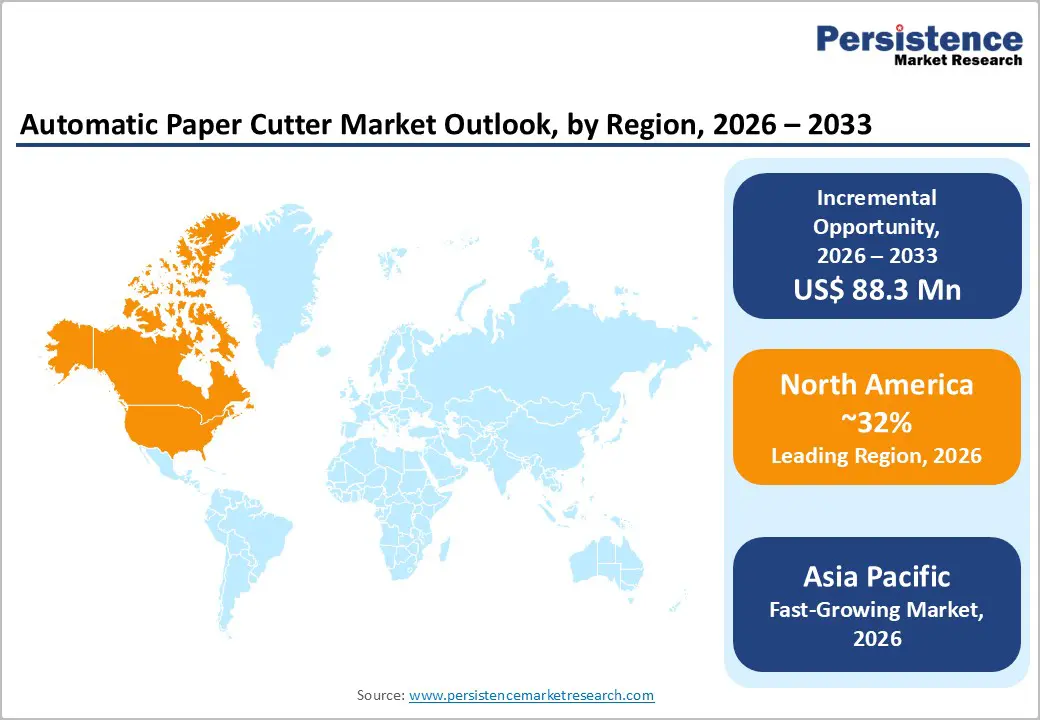

- Dominant Region: North America is expected to command about 32% market share in 2026, fueled by a well-established printing and publishing industry.

- Fastest-growing Regional Market: The Asia Pacific market is slated to record the fastest growth during the 2026-2033 forecast period, aided by the rapid expansion of the printing industry in China and India.

- Leading & Fastest-growing Product Type: Guillotine cutters are likely secure an estimated 45% revenue share in 2026, whereas rotary cutters are set to be the fastest-growing segment through 2033.

- Leading & Fastest-growing Application: Commercial printing is expected to capture approximately 75% revenue share in 2026, with industrial use poised to grow the fastest over the 2026-2033 forecast period.

| Key Insights | Details |

|---|---|

| Automatic Paper Cutter Market Size (2026E) | US$ 304.0 Mn |

| Market Value Forecast (2033F) | US$ 392.3 Mn |

| Projected Growth (CAGR 2026 to 2033) | 3.7% |

| Historical Market Growth (CAGR 2020 to 2025) | 3.2% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Accelerating Automation in the Print and Packaging Industry

The print and packaging industry is redirecting capital toward automation to improve production efficiency and manage rising labor expenses. Firms are investing in advanced finishing equipment as throughput requirements are increasing across commercial printing operations. The Printing Industries of America (PIA) is monitoring this transition as manufacturers modernize post-press workflows. Automatic paper cutters, including programmable guillotine systems and rotary cutting machines, are supporting these upgrades by delivering accurate and high-speed processing. Printing companies in Asia Pacific and North America are replacing aging finishing lines with automated systems that integrate easily into digital production environments.

Automation is improving operational stability across modern print facilities. Automated cutting systems are reducing reliance on manual handling while increasing precision and output consistency. Programmable guillotine cutters are supporting flexible job management across varying print runs, while rotary machines are handling large-scale production tasks efficiently. Packaging manufacturers are strengthening demand for dependable cutting technologies as product volumes expand globally. Companies that are adopting these systems are improving workflow reliability and minimizing production errors. Strategic investment in automation is therefore enabling print houses to develop scalable operations that align with rising market demand and evolving production standards.

Smart Manufacturing and Industry 4.0 Integration

Government policies are accelerating the adoption of Industry 4.0 technologies across the paper and printing sectors. Initiatives such as the European Union (EU) Digital Decade Policy Programme and the U.S. Advanced Manufacturing National Program are providing financial support for industrial modernization. Printing and packaging facilities are using these incentives to upgrade production infrastructure and integrate digital technologies. Automatic paper cutters equipped with Internet of Things (IoT) sensors are gaining attention because they enable real-time performance monitoring and operational data capture. Predictive maintenance algorithms are identifying potential mechanical faults before system failure occurs. Integration with manufacturing execution systems (MES) is also linking cutting equipment with wider factory management platforms.

The demand for intelligent cutting systems is rising, fed by the transition of manufacturers toward digitally connected production environments. Network-enabled machines are improving workflow coordination and reducing operational interruptions. IoT functionality is supporting optimized scheduling while minimizing unexpected downtime. Predictive maintenance tools are extending equipment lifespan and lowering repair costs. MES connectivity is aligning cutter performance with broader plant efficiency targets. Forward-looking manufacturers are prioritizing equipment that supports scalable and interoperable operations within smart factory frameworks. Early investment in these technologies can bolster operational resilience and position firms to benefit from the broader shift toward digitally integrated manufacturing.

Digital Substitution and the Structural Decline of Print Media

Digital communication channels are expanding rapidly across media, marketing, and commerce. This shift is creating structural pressure on the automatic paper cutter market. Publishers are reducing print volumes as readers rely more on online platforms. Businesses are prioritizing digital marketing campaigns rather than printed brochures or catalogues. Newspapers and magazines are lowering physical circulation as digital distribution expands. As a result, traditional printing facilities are experiencing declining production activity, with print service providers facing shrinking client bases, which is reducing equipment purchases from legacy operations.

Manufacturers are responding by repositioning products toward packaging and specialty material applications. Equipment suppliers are targeting demand generated by e-commerce packaging, custom labeling, and short-run production formats. This shift requires investment in research 7 development (R&D) to redesign cutting systems that handle thicker substrates and varied material dimensions. Companies are entering competitive segments that already include established packaging machinery providers. Transition costs are therefore increasing while returns are emerging gradually. Firms are strengthening sales capabilities to serve a wider customer base and expanding service networks that support diverse industrial uses.

Supply Chain Fragility and Raw Material Volatility in Precision Component Manufacturing

Advanced automatic paper cutters, including high-specification guillotine systems and computer numerical control (CNC) servo machines, rely on tightly coordinated supply chains. These machines incorporate precision components such as hardened steel blades, servo motors, linear guides, and embedded control electronics. Manufacturers source these parts from specialized global suppliers to maintain performance reliability and meet demanding production standards. Disruptions within this network are affecting assembly schedules and delaying equipment delivery. Firms are therefore reassessing procurement strategies to strengthen supply resilience as global material flows remain uncertain.

Supply chain exposure is placing additional pressure on original equipment manufacturers (OEMs). Many critical components originate from concentrated production hubs such as Japan, Germany, and China, which increases vulnerability to trade policy changes and logistical disruptions. Fluctuating input costs for items such as precision bearings and motors are also influencing production planning. OEMs operating with narrow margins are facing difficulty absorbing sudden cost increases within a capital equipment sector that features long sales cycles and price-sensitive customers. Institutional buyers are demanding stronger supply reliability, which is encouraging manufacturers to diversify sourcing channels and maintain strategic component inventories to reduce operational risk.

Integration of AI and Digital Connectivity

The integration of artificial intelligence (AI) vision systems, cloud-based monitoring dashboards, and predictive analytics is creating new opportunities for innovation in automatic paper cutters. Equipment manufacturers are embedding these technologies to improve optical registration accuracy and monitor blade conditions in real time. These capabilities are enabling operators to maintain precise alignment and optimize cutting performance across multiple paper grades and packaging materials. Cloud connectivity is allowing remote diagnostics and operational visibility, supporting faster decision making and improved production control.

Suppliers are using this technology convergence to develop premium equipment for high-volume commercial printing and packaging facilities. AI algorithms are predicting maintenance requirements and adjusting machine parameters automatically, strengthening reliability in demanding production environments. Vendors are also investing in scalable platforms designed to integrate with existing factory infrastructure and digital manufacturing networks. User-focused interface design and strong cybersecurity frameworks are becoming critical differentiators as buyers seek dependable connected equipment. Manufacturers that align advanced analytics with practical operational needs are strengthening competitive positioning and building long-term customer loyalty in increasingly data-driven production environments.

Sustainability-Driven Equipment Upgrades

Corporate supply chains are focused on meeting their environmental, social, and governance (ESG) commitments, prompting print and packaging operators to modernize equipment fleets. New automatic paper cutters are incorporating programmable backstops that improve alignment accuracy and reduce setup errors across different material thicknesses. These systems are enabling operators to achieve higher material utilization compared with older semi-automatic machines that generate excess waste during production. Regulatory frameworks such as the EU Green Deal and climate disclosure requirements issued by the U.S. Securities and Exchange Commission (SEC) are increasing transparency on environmental performance, which is accelerating equipment modernization in regulated markets.

Sustainability priorities are therefore strengthening demand for advanced cutting technologies. Print facilities are replacing legacy equipment to improve energy efficiency and fulfil ESG reporting standards. Manufacturers are designing cutting machines that incorporate energy-efficient components and recyclable structural materials to address environmental expectations. Early adoption is helping operators avoid compliance risks associated with outdated machinery while improving operational metrics measured in sustainability audits. Equipment suppliers are also developing solutions that demonstrate measurable reductions in material waste and energy use. These capabilities are strengthening long-term supplier relationships as buyers seek equipment that supports both operational performance and corporate sustainability objectives.

Category-wise Analysis

Product Type Insights

Among product types, guillotine cutters are expected to lead in 2026, accounting for about 45% of the automatic paper cutter market revenue share. Their dominance reflects dependable performance when processing large paper stacks in commercial and industrial printing facilities. These machines rely on mechanically driven blade systems that deliver accurate and smooth cuts with limited operator effort. Print operators are selecting them for consistent output and straightforward machine control in high-throughput environments. Durable structural components are also extending service life, which is reinforcing demand among facilities that prioritize stable and efficient paper handling operations.

Rotary cutters are projected to register the fastest growth from 2026 to 2033. Their circular blade mechanism enables curved and detailed cuts that support specialized printing tasks and creative production work. Professionals working in environments such as art studios and photographic processing labs are using these machines to manage delicate materials with greater control. This capability is supporting steady adoption within niche segments that require precision and flexibility. Manufacturers are introducing enhanced safety features and improved blade control systems, which are strengthening product reliability and expanding rotary cutter applications across evolving print and design markets.

Application Insights

Commercial printing is poised to dominate applications, capturing an estimated 75% of the automatic paper cutter market share in 2026. Automatic paper cutters are supporting modern printing facilities that handle large production volumes and complex job specifications. Print operators are relying on programmable controls and fast cutting cycles to maintain precision while meeting tight delivery schedules. These machines are ensuring accurate processing of large paper stacks and varied formats required for customized print orders. As commercial printing companies are expanding digital and short-run production capabilities, demand for advanced cutting equipment is strengthening across global markets.

Industrial applications are projected to register the highest growth trajectory during the 2026-2033 forecast period. Packaging production and paper processing facilities are requiring highly precise and consistent cutting performance to prepare materials for finished goods. These machines are supporting large-scale manufacturing environments that operate under continuous production schedules in sectors such as consumer goods and logistics. Manufacturers are valuing their reliability, speed, and ability to integrate smoothly with automated assembly lines. As industrial packaging demand increases worldwide, automatic cutters are becoming essential components of efficient and scalable manufacturing workflows.

Regional Insights

North America Automatic Paper Cutter Market Trends

North America is anticipated to account for about 32% of the automatic paper cutter market value in 2026. The regional market benefits from a well-developed printing and publishing ecosystem that includes commercial print houses, corporate production units, and specialty packaging facilities across the U.S. and Canada. Established industry players are maintaining high equipment performance standards, which is sustaining demand for guillotine and rotary cutting systems capable of processing varied paper grades with consistent precision. Businesses are prioritizing machines equipped with programmable controls and strong safety mechanisms to support high-volume production of marketing materials, books, and branded packaging.

Automation is strengthening adoption across regional production facilities. Printing companies are upgrading legacy equipment with servo-driven systems to address labor constraints and improve operational efficiency. These modern machines are reducing downtime and increasing throughput in fast-paced printing environments. Corporate offices are also installing compact cutting systems designed for in-house document finishing and promotional material preparation. Technology leadership in North America is encouraging equipment innovation, with manufacturers introducing IoT-enabled monitoring dashboards and predictive maintenance tools that support data-driven equipment management. These capabilities are aligning with regional preferences for reliability, operational transparency, and advanced analytics.

Europe Automatic Paper Cutter Market Trends

Europe holds a stable position in the market for automatic paper cutters, aided by a strong printing and publishing heritage across Germany, France, and the U.K. Printing companies in the region are maintaining strict quality standards for books, magazines, and premium printed materials. As a result, demand remains strong for guillotine and rotary cutting systems equipped with servo precision and programmable controls that deliver clean and accurate edges. Commercial printers are prioritizing equipment that reduces production defects and supports short-run printing with high customization, which aligns with Europe’s emphasis on refined finishing quality in competitive global markets.

Printing companies are investing in advanced cutting equipment to strengthen operational efficiency and maintain industry leadership. Modern machines are incorporating features such as optical registration and IoT connectivity to streamline production workflows and improve equipment monitoring. Educational institutions and design academies are also contributing to demand by installing reliable cutting machines in training laboratories that prepare skilled printing professionals. Regulatory frameworks, including the EU Machinery Directive, are enforcing strict safety and efficiency requirements for industrial equipment, pushing operators to replace older systems with energy-efficient models that comply with sustainability objectives and evolving manufacturing regulations.

Asia Pacific Automatic Paper Cutter Market Trends

The Asia Pacific market is expected to register the fastest growth through 2033. Rapid industrial development and expansion of the printing sector are driving demand across major economies such as China and India. Manufacturing hubs in these countries are increasing production capacity to meet rising domestic consumption and export requirements. Printing and packaging companies are upgrading legacy finishing systems to process growing volumes of paper packaging and promotional materials. Automated cutting equipment is therefore becoming a core component of modern production workflows that prioritize efficiency and scalability.

Public policy support is further accelerating market expansion. Governments are encouraging technology adoption through industrial incentives, infrastructure investment, and modernization programs that support advanced manufacturing equipment. China is leveraging its strong position in global paper production and e-commerce logistics, where automated guillotine and rotary cutting machines are ensuring consistent processing in applications such as corrugated board trimming and label production. India is experiencing similar momentum as its commercial printing sector expands to serve growing consumer markets and hybrid digital printing formats. These developments are strengthening regional demand for precision cutting equipment designed for high-volume and flexible production environments.

Competitive Landscape

The global automatic paper cutter market exhibits a moderately consolidated structure led by companies such as POLAR Mohr, Perfecta Schneider, Wohlenberg, Challenge Machinery, and MBM Corporation. These manufacturers collectively account for about 35 to 40 percent of total market share. Their leadership reflects strong engineering capabilities, global distribution networks, and consistent investment in product innovation. Leading suppliers are expanding equipment portfolios by integrating technologies such as AI-driven precision control and IoT-enabled monitoring systems. These capabilities are supporting commercial printing facilities, industrial production units, and office environments that require reliable and high-precision cutting solutions.

Competitive intensity is increasing as new entrants introduce cost-efficient machines and niche cutting technologies. This pressure is encouraging established manufacturers to strengthen research and development (R&D) programs and respond quickly to evolving customer requirements and regulatory expectations. Companies are differentiating products through durable construction, enhanced operator safety mechanisms, and compatibility with automated production systems. In a fragmented supplier landscape, firms that combine technological innovation with operational reliability are strengthening customer retention and securing long-term market positioning.

Key Industry Developments

In January 2026, Maark Automation introduced hydraulic digital paper cutters designed for digital print shops that require compact and reliable finishing equipment. These machines feature programmable cutting, safety sensors, and touchscreen interfaces to improve precision, efficiency, and operational safety during paper processing.

Companies Covered in Automatic Paper Cutter Market

- POLAR Mohr GmbH & Co. KG

- Perfecta Schneider GmbH

- Wohlenberg GmbH

- Challenge Machinery Company

- MBM Corporation

- Formax Inc.

- Duplo International

- Morgana Systems

- Baumgarten Schneider

- ITOTEC Co., Ltd.

- Horizon International Inc.

- Graphic Whizard

- Renz Group

- Krug & Priester

Frequently Asked Questions

The global automatic paper cutter market is projected to reach US$ 304.0 million in 2026.

Automation in printing, packaging, and publishing, powered by a robust demand for precision, efficiency, and reduced labor costs are driving the market.

The market is poised to witness a CAGR of 3.7% from 2026 to 2033.

Major opportunities lie in emerging tech such as laser/servo systems, and sustainable models that offer growth in commercial and industrial segments.

OLAR Mohr, Perfecta Schneider, Wohlenberg, Challenge Machinery, and MBM Corporation are some of the key players in the market.