- Animal Health

- Automatic Self Cleaning Cat Litter Box Market

Automatic Self Cleaning Cat Litter Box Market Size, Share, and Growth Forecast 2026 - 2033

Automatic Self Cleaning Cat Litter Box Market by Product Type (Single Cat, Multi Cat), by Distribution Channel (Online, Offline), by Regional Analysis, 2026 - 2033

Automatic Self Cleaning Cat Litter Box Market Size and Trend Analysis

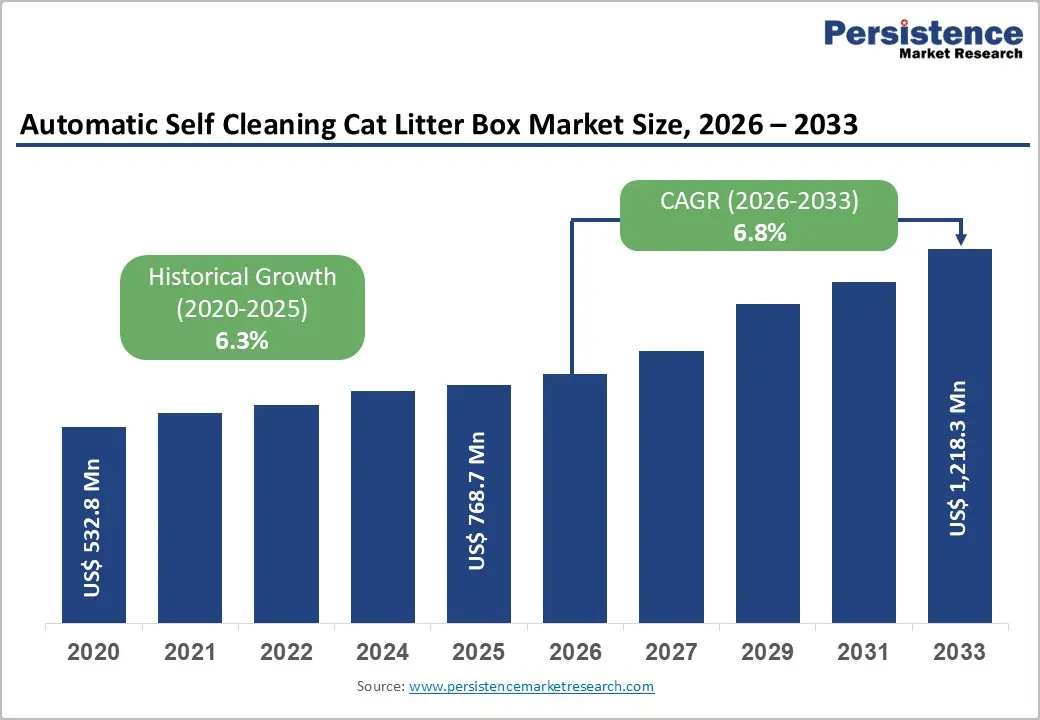

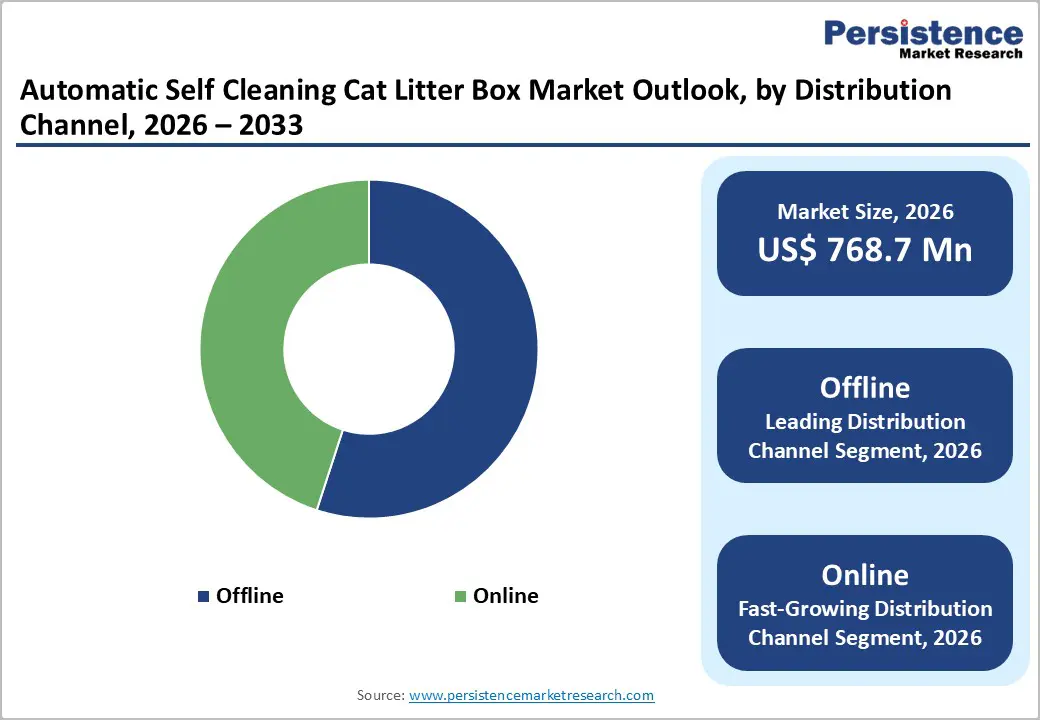

The global automatic self-cleaning cat litter box market size is expected to be valued at US$ 768.7 million in 2026 and projected to reach US$ 1,218.3 million by 2033, growing at a CAGR of 6.8% between 2026 and 2033.

Rising pet ownership, combined with the accelerating adoption of smart home automation technologies, is the primary catalyst driving market expansion. According to recent statistics, approximately 46.5 million households in the United States own cats, while globally there are approximately 74 million domesticated cats in the US, 53 million in China, and 23 million in Russia, reflecting a substantial addressable market opportunity. The convergence of urbanization, dual-income households prioritizing convenience, and millennial consumers with purchasing power represents approximately 33% of pet owners, demonstrating an elevated willingness to invest in premium automation solutions.

Key Industry Highlights:

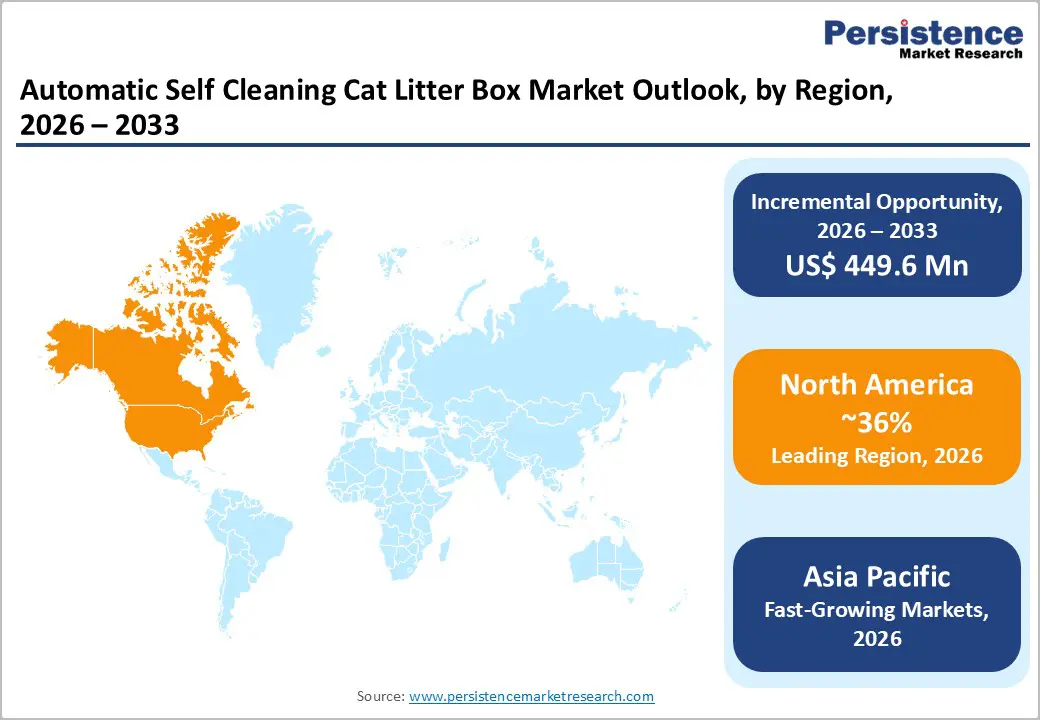

- Leading Region: North America holds the largest regional market share of approximately 36% in 2025, driven by high pet ownership, advanced technology adoption, and strong consumer purchasing power.

- Emerging Region: Asia Pacific represents the fastest-growing regional market, expanding at approximately a 10% CAGR through 2033, propelled by rapid urbanization, rising disposable incomes, the accelerating adoption of Western pet care culture in China, Japan, Singapore, and South Korea, and the explosive development of e-commerce infrastructure, enabling direct-to-consumer sales.

- Dominant Segment: Single-cat automatic self-cleaning litter boxes dominate the product category, commanding approximately 78% market share in 2025, driven by the prevalence of single-cat households, compact, space-efficient designs optimized for urban apartments, lower production costs, and simplified operational requirements compared to multi-cat systems.

- Fastest Growing Segment: Online distribution channels represent the fastest-growing sales segment, expanding at approximately 13% CAGR through 2033, driven by e-commerce acceleration, direct-to-consumer brand establishment and subscription-based consumable delivery models.

- Key Opportunity: Health monitoring and IoT integration represent the key market opportunity, with pet tech firms integrating machine-learning algorithms to analyze pet health patterns, pet owners deploying smart pet devices, and consumers willing to pay premium prices for early disease-detection capabilities.

| Key Insights | Details |

|---|---|

|

Automatic Self-Cleaning Cat Litter Box Market Size (2026E) |

US$ 768.7 million |

|

Market Value Forecast (2033F) |

US$ 1,218.3 million |

|

Projected Growth CAGR(2026-2033) |

6.8% |

|

Historical Market Growth (2020-2025) |

6.3% |

Market Dynamics

Drivers – Rise in Demand for Convenience and Time-Saving Pet Care Solutions

Busy consumer lifestyles and the prevalence of dual-income households have created compelling demand for automated pet care solutions that eliminate time-consuming manual tasks. Automatic self-cleaning litter boxes reclaim valuable time previously devoted to daily scooping and cleaning, with typical cat owners spending approximately 5-10 minutes per day on manual litter box maintenance, representing 25-50 hours annually. Major consumer surveys indicate that over 60% of urban pet owners prefer devices that integrate with mobile apps and smart home systems, enabling remote monitoring and control.

The Litter-Robot brand, operated by Whisker, has achieved market-leading status with over 1.5 million users globally and over 65,000 five-star reviews, demonstrating compelling validation of consumer demand. Consumers are increasingly willing to pay a premium for self-cleaning litter boxes, with average unit prices ranging from $300-600, reflecting a willingness to pay for convenience, odor control, and hygiene benefits. This convergence of demographic shifts, time scarcity, and consumer technology adoption is driving sustained market expansion across consumer segments prioritizing convenience.

Integration of IoT Technologies and Health Monitoring Capabilities

Advanced IoT integration with sensor-based automation and AI analytics is transforming automatic self-cleaning litter boxes from basic cleaning devices into comprehensive pet health monitoring systems. More than 65% of pet owners express interest in AI-driven health monitoring devices for their pets, reflecting strong consumer demand for technology-enabled wellness insights. Modern litter boxes equipped with laser and weight sensors can detect usage patterns and track health trends, which aligns with findings that 53% of pet owners prefer AI-enhanced devices for ongoing health monitoring over traditional methods.

AI-powered platforms like advanced smart litter boxes now offer mobile app integration that provides real-time alerts and insights, reflecting the broader trend that 40% of pet owners believe AI can help identify health issues before symptoms manifest, showing strong trust in AI-based proactive care. These developments underscore industry confidence in health monitoring as a key growth driver for automatic self-cleaning pet devices.

Restraints - High Product Cost and Premium Pricing Barriers

Automatic self-cleaning litter boxes command premium price points that substantially exceed those of traditional manual litter boxes, creating adoption barriers for price-sensitive consumer segments and lower-income households. Typical self-cleaning litter box prices range from $300-600 per unit, representing significant discretionary spending compared to basic litter boxes costing $10-30, limiting addressable market penetration. Manufacturing complexity, sophisticated sensor technologies, precision motion-control mechanisms, and smart connectivity components substantially increase production costs, which manufacturers pass on to consumers through premium pricing.

The need for proprietary litter formulations optimized for automatic systems and for ongoing consumables, including waste drawer liners and carbon filters, creates additional ownership costs that discourage adoption among budget-conscious consumers. Consumer research indicates price sensitivity remains a significant purchase barrier, with approximately 40-45% of interested consumers deferring purchase decisions due to perceived high costs relative to perceived value proposition.

Noise and Behavioral Concerns Among Cats and Multi-Cat Households

Some cats exhibit anxiety and stress in response to automated cleaning cycles, with noise from rotating mechanisms and unexpected cleaning activation that can startle sensitive animals. Multi-cat households face compounded complications, as conflicting usage patterns may trigger multiple cleaning cycles, resulting in excessive noise and potential equipment wear.

Traditional rake-based litter box mechanisms can create clogging issues if cats experience digestive issues or produce unusually textured waste, necessitating maintenance and cleaning interventions, reducing perceived automation benefits. The Whisker brand reports an adoption rate of over 95% for Litter-Robot units, yet the remaining 5% of cats that demonstrate rejection or behavioral stress represent meaningful adoption friction. Equipment failure rates and maintenance requirements, including motor failures, sensor malfunctions, and software glitches, create reliability concerns among consumers expecting fully automated, zero-intervention operation.

Opportunity - Rapid E-Commerce Expansion and Direct-to-Consumer Distribution Channel Growth

Significant market opportunities exist in expanding e-commerce and direct-to-consumer distribution channels, which represent the fastest-growing distribution segment, with a 12-15% CAGR through 2032. Online retailers, including Chewy.com, Amazon.com, and brand-direct channels, including Whisker.com have captured dominant market positions.

Direct-to-consumer channels enable manufacturers to build brand loyalty, gather detailed customer usage data, and implement subscription-based recurring-revenue models for consumables, such as carbon filter replacement packs and waste drawer liners. The expansion of e-commerce infrastructure, reduced customer acquisition costs through digital marketing, and frictionless payment processing have substantially reduced barriers to market entry for emerging competitors.

Expansion into Emerging Markets and Geographic Markets with Rising Pet Ownership

Exceptional market opportunities exist in the Asia Pacific experiencing rapid urbanization, rising disposable incomes, and accelerating adoption of Western pet care culture. China’s explosive e-commerce infrastructure development and social media-driven consumer adoption demonstrate a substantial market opportunity, with Chinese consumers increasingly demanding technology-rich, AI-enabled litter boxes that provide real-time monitoring and remote tracking capabilities.

India’s rising urban middle class, combined with increasing pet ownership among younger demographics, represents an emerging market opportunity. Japan and South Korea demonstrate particularly strong pet tech adoption, with consumers prioritizing innovative solutions that align with expectations for technological sophistication. Europe’s market expansion, particularly in Germany, the United Kingdom, and France, reflects accelerating premiumization trends, with consumers willingly investing in high-end pet care products emphasizing health monitoring and hygiene.

Category-wise Analysis

Product Type Insights

The single-cat automatic self-cleaning litter box segment dominates the market, commanding roughly 78% share in 2025, driven by the larger base of single-cat households and demand for compact, lower-cost automated solutions. These systems use simpler mechanics, require less maintenance, and include smaller waste capacity, enabling faster processing cycles and reduced production costs. Urban consumers living in smaller homes increasingly prefer single-cat units due to space efficiency and favorable price-to-value ratios. Manufacturers continue to prioritize reliability enhancements, odor-control improvements, and quieter operation to maintain segment leadership and reinforce the consumer shift away from traditional manual litter boxes.

Distribution Channel Insights

Offline distribution channels, including pet specialty retailers and veterinary clinics, remain dominant, accounting for approximately 55% of the market in 2025. Consumers prefer in-store demonstrations, immediate product availability, and professional recommendations, which build confidence when purchasing premium automated litter systems. Veterinary endorsements influence adoption among health-aware pet owners, while established retail chains leverage strong distribution networks and bundled service offerings to support upselling strategies and long-term customer engagement.

Regional Insights

North America Automatic Self-Cleaning Cat Litter Box Market Trends and Insights

North America dominates the global automatic self-cleaning cat litter box market, commanding approximately 36-37% market share in 2025, driven by high pet ownership prevalence, advanced technology adoption, and premium consumer purchasing power. The United States represents approximately 72% of the North American market value, supported by approximately 46.5 million households owning cats and 71% of households maintaining pets. American consumers demonstrate elevated willingness to invest in premium pet care automation, with average US pet industry spending reaching approximately $136 billion annually, reflecting robust discretionary spending for pet wellness and convenience products.

Whisker’s Litter-Robot has achieved a market-leading position with 1.5 million users globally and over 65,000 five-star customer reviews, demonstrating exceptional consumer validation in North American markets. The US automatic self-cleaning cat litter box market specifically generated approximately US$ 125.3 million in 2024 and is projected to reach US$ 182.2 million by 2030, expanding at a CAGR of 6.6%. Major retailers, including Chewy.com (capturing 28.66% of the pet supplies search market share), PetSmart, and Petco, maintain substantial distribution capabilities, driving market penetration. Technology adoption, including IoT connectivity and mobile app integration, aligns with North American consumer preferences for smart home integration and remote pet monitoring. Innovation ecosystem strength, venture capital availability, and the presence of technology companies, including Whisker, supporting product development, reinforce regional competitive advantages.

Europe Automatic Self-Cleaning Cat Litter Box Market Trends and Insights

Europe represents approximately 20-22% of global market share in 2025, with market valuation estimated at approximately €500 million (approximately US$ 550 million) in 2023, expanding at approximately 9% CAGR through 2033. Germany dominates the European market, accounting for approximately 25-30% of market value, driven by high cat ownership prevalence, strong environmental consciousness prioritizing sustainable products, and elevated adoption of smart home technologies. The United Kingdom and France represent secondary major markets, with significant cat populations including approximately 11.9 million in the UK and 14.9 million in France.

European consumer emphasis on hygiene, convenience, and pet health creates compelling market drivers, with premiumization trends reflecting willingness to invest in high-end automated pet care solutions. Germany’s industrial manufacturing capabilities support the development of advanced robotics and sensor technologies, and consumers are particularly receptive to AI-enabled health monitoring and automated cleaning cycle optimization. The UK market emphasizes feline urinary health monitoring capabilities, driving adoption of sophisticated litter box systems tracking usage patterns and detecting health anomalies. Spain projects approximately 11.60% CAGR growth through 2032, reflecting accelerating adoption among younger demographics prioritizing convenience. European regulatory frameworks emphasizing data privacy and sustainability drive product development focusing on energy efficiency and ecological responsibility.

Asia Pacific Automatic Self-Cleaning Cat Litter Box Market Trends and Insights

Asia Pacific represents the fastest-growing regional market, projected to expand at approximately 9-10% CAGR through 2032, driven by rapid urbanization, rising disposable incomes, and accelerating adoption of Western pet care culture. China represents the largest single Asia Pacific country market, with approximately 53 million pet cats and an explosive e-commerce infrastructure development, creating substantial distribution opportunities. Chinese consumers show strong demand for technology-rich, AI-enabled litter boxes that provide real-time monitoring and remote tracking, aligning with national smart home adoption trends.

Japan represents a significant mature market with strong pet tech adoption, high internet penetration, and consumer willingness to invest in premium pricing for innovative pet solutions. Singapore projects the fastest growth rate at approximately 14.90% CAGR through 2032, reflecting expectations for technological sophistication and prioritization of urbanization-driven convenience. South Korea demonstrates exceptional smart home and pet tech adoption, with domestic firms and startups actively innovating for tech-aware consumers. India’s rapidly urbanizing middle class and increasing pet ownership among younger demographics creates emerging market opportunity. The region’s manufacturing advantages and cost-effective production capabilities position Asia Pacific suppliers for competitive expansion into global markets through value-based product offerings.

Competitive Landscape

The automatic self-cleaning cat litter box market features a moderately fragmented structure with a mix of established pet care brands and emerging innovators competing for share. Market leaders benefit from extensive retail distribution, strong brand equity, and sustained investment in product R&D, while newer entrants differentiate through advanced automation features and targeted digital marketing. Competitive strategies increasingly prioritize integration of IoT connectivity, real-time monitoring capabilities, and mobile app ecosystems that enable data-driven pet health insights.

Subscription and recurring consumable revenue models are gaining traction as vendors seek predictable income streams and stronger customer retention. Consolidation trends are emerging as larger pet-technology companies pursue acquisitions or strategic partnerships to expand product portfolios and accelerate entry into automated pet care. Meanwhile, price-competitive products with simplified feature sets are targeting cost-sensitive consumers, intensifying competition across product tiers and driving continuous innovation in design, odor management, and user experience.

Key Market Developments

- May 2022: Whisker introduced the Litter-Robot 4, a fourth-generation automatic self-cleaning litter box incorporating enhanced litter-sifting technology, real-time tracking of usage and health data, QuietSift technology minimizing motor noise, and mobile app integration for seamless user experience and pet health monitoring capabilities.

- October 2025: Whisker launched AI-powered Litter-Robot 5 Pro litter boxes featuring facial recognition cameras, weight tracking, and illness detection for monitoring cat health and well-being.

- November 2025: Petlibro launched Luma Smart Litter Box featuring AI-powered visual detection, multi-cat recognition, waste analysis, auto-cleaning, and app-based health alerts to revolutionize effortless cat care and monitoring.

- July 2025: PETKIT has announced the pre-launch of the Purobot Crystal Duo, the world's first open-top AI-powered automatic litter box. It uses camera monitoring and pH-activated litter to detect cat health risks like UTIs early, sending app alerts, with up to 30 days of hands-free operation.

Companies Covered in Automatic Self Cleaning Cat Litter Box Market

- Lalahome

- Litter-Robot (Whisker)

- PetNovations Inc

- Pet Safe

- Spectrum Brands (LitterMaid)

- Catit

- Petree Litter Box

- OmegaPaw

- Themeowpetshop

- Whisker

- Petco

- Smarty Pear

- Cuddle

- Cosmic Pet

- Chewy

- Cat Genie

- Van Ness

- Modkat

- PetFusion

- Iris USA Inc.

Frequently Asked Questions

The market is expected to reach about US$ 768.7 million in 2026, rising to roughly US$ 1.22 billion by 2033.

Demand is fueled by rising pet ownership, convenience needs, urban living constraints, and adoption of smart and health-monitoring pet technologies.

North America is expected to lead with about 36% share due to high pet ownership and strong technology adoption.

Opportunities include rapid e-commerce expansion, Asia Pacific growth at around 9–10% CAGR, and integration of AI-enabled health monitoring.

Key players include Whisker (Litter-Robot), Pet Safe, PetSmart, Petco, etc.