- Home Appliances

- Automatic Milk Frother Market

Automatic Milk Frother Market Size, Share, and Growth Forecast, 2026 - 2033

Automatic Milk Frother Market by Material (Stainless Steel, Plastic, Glass), Application (Residential, Commercial, Hospitality, Others), Sales Channel (Online, Offline), and Regional Analysis for 2026-2033

Automatic Milk Frother Market Share and Trends Analysis

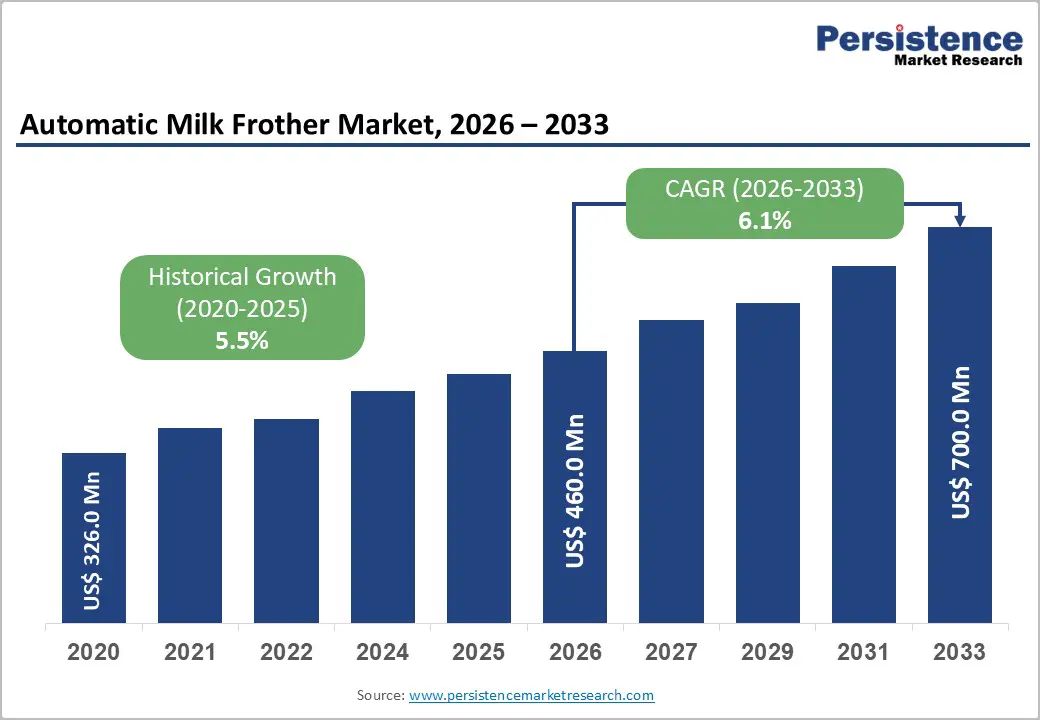

The global automatic milk frother market is projected to grow from US$460.0 million in 2026 to US$700.0 million by 2033, at a CAGR of 6.1%. Growth is driven by rising home coffee consumption, technological improvements in frothers, and the expansion of specialty coffee culture across North America, Europe, and Asia Pacific. Increased disposable incomes, plant-based milk options, and wider e-commerce distribution are further boosting adoption.

Key Industry Highlights

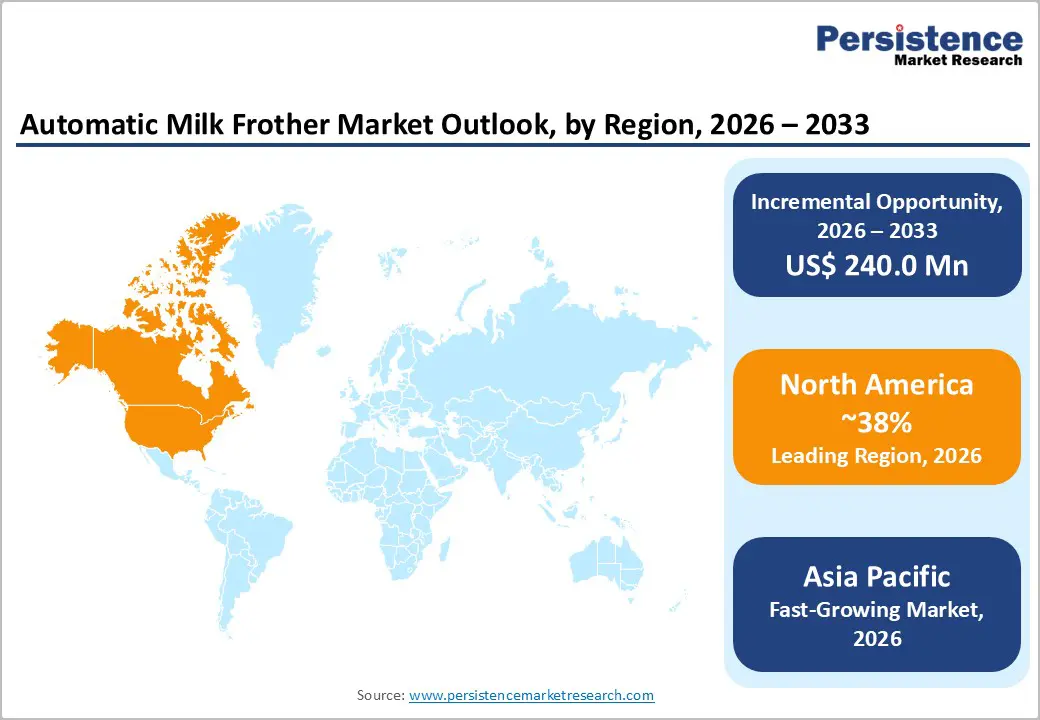

- Dominant Region: North America is expected to command about 38% of the market share in 2026, supported by demand through robust coffee culture and widespread specialty beverage consumption.

- Fastest-growing Market: Asia Pacific is likely to emerge as the fastest-growing market due to rapid urbanization and rising disposable incomes among middle-class households.

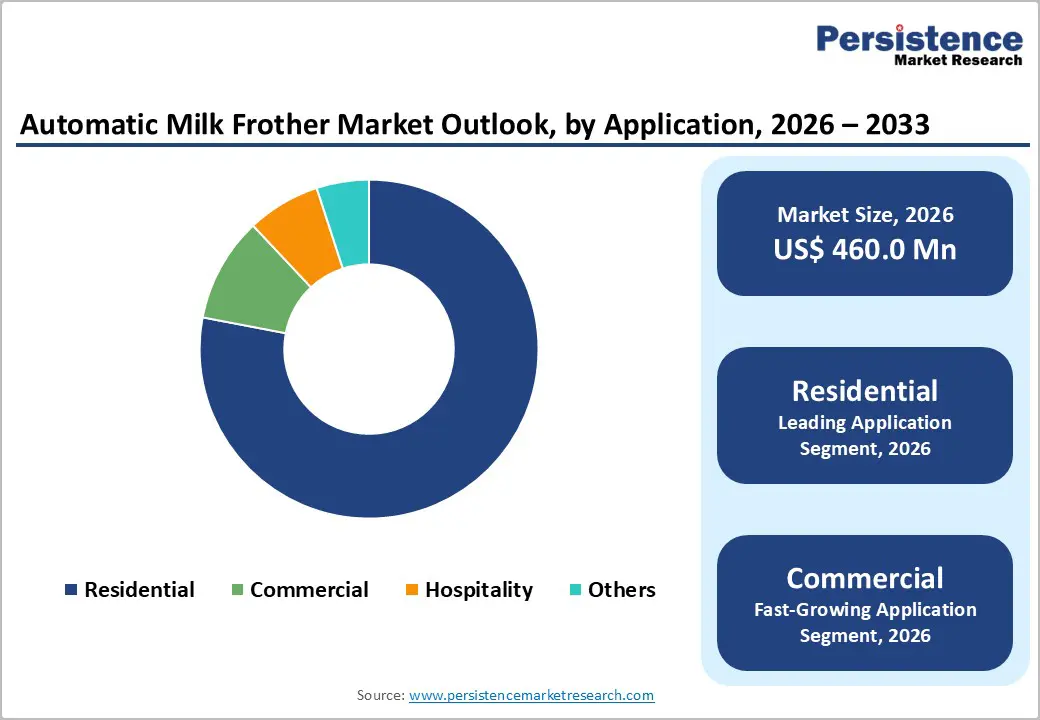

- Leading & Fastest-growing Application: Residential applications are slated to hold roughly 78% revenue share in 2026, while commercial applications are expected to grow the fastest during the 2026-2033 forecast period.

- Sales Channel Dominance: Online retail is set to dominate with an approximate 55% revenue share in 2026, with offline channels exhibiting the highest 2026-2033 CAGR.

- Key Developments: Nespresso launched the NanoFoamer, a cordless, rechargeable handheld milk frother designed for creating superfine, fine, or standard cold foam on iced coffees, cappuccinos, and lattes.

| Key Insights | Details |

|---|---|

|

Automatic Milk Frother Market Size (2026E) |

US$ 460.0 Mn |

|

Market Value Forecast (2033F) |

US$ 700.0 Mn |

|

Projected Growth (CAGR 2026 to 2033) |

6.1% |

|

Historical Market Growth (CAGR 2020 to 2025) |

5.5% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Technological Innovation in Product Design

Manufacturers are integrating advanced induction heating systems into automatic milk frothers to deliver precise temperature control within narrow tolerances of approximately + 2 degrees Celsius. This level of accuracy is improving milk texture consistency and foam stability across different beverage types. Smart connectivity features are allowing users to manage settings through mobile applications and programmable interfaces, which is aligning with growing demand for connected kitchen appliances. These capabilities are supporting customization of froth density and temperature preferences. Energy-efficient engineering is reducing electricity consumption compared with conventional heating elements, and this improvement is helping brands comply with regulatory standards in regions such as the European Union (EU). Companies that are embedding digital controls and thermal precision are enhancing product differentiation while meeting sustainability objectives.

Material innovation is also strengthening product appeal and safety performance. Manufacturers are incorporating Bisphenol A free components and non-stick interior coatings to address consumer health concerns. Self-cleaning mechanisms and detachable parts are improving hygiene and reducing maintenance effort. These advancements are shortening preparation time relative to manual frothing techniques and are improving daily usability. Premium feature integration is enabling brands to justify higher price positioning in competitive retail environments. Firms that are prioritizing durability testing, energy certification compliance, and intuitive design are positioning themselves to attract quality-focused buyers. Strategic investment in technology enhancement and user-centric design is supporting long-term competitiveness in an increasingly mature automatic milk frother market.

Product Durability and Maintenance Concerns

Consumer reviews highlight significant concerns about the average lifespan of automatic milk frothers. Users frequently report functionality issues that emerge over time due to demanding daily use. Heating element failures and motor wear from regular operation shorten replacement cycles beyond consumer expectations. These recurring problems erode overall product reliability for households seeking dependable kitchen appliances. Maintenance tasks, such as regular descaling and thorough cleaning, further discourage buyers who prioritize convenience and minimal upkeep. Limited warranties covering only basic periods amplify perceived risks around long-term value, leaving customers vulnerable to unexpected costs.

Component breakdowns often force full unit replacement instead of simple repairs, creating substantial environmental challenges through accelerated waste generation. Customers endure additional expenses and repeated inconvenience from frequent repurchasing. Brands experience weakened loyalty as dissatisfied users hesitate to repurchase or recommend products. Companies must address these durability gaps through robust engineering upgrades and extended support frameworks. Such proactive strategies not only enhance customer retention but also align with growing sustainability demands. Ultimately, they position brands for sustained market expansion while fostering stronger consumer relationships in a competitive landscape.

Sustainability-Focused Product Innovation in Europe

Sustainability regulations established by the European Union are influencing purchasing decisions across the region. Consumers are seeking eco-designed automatic milk frothers that manufacturers are producing with recycled metals and certified plastics. Energy-efficient operation is reducing electricity consumption during daily use, which is aligning with household carbon reduction targets. Modular and repairable construction is extending product lifespan and supporting circular economy objectives promoted by European policy frameworks. Brands that are adopting carbon-neutral manufacturing practices are strengthening environmental credentials and are appealing to environmentally conscious buyers. Biodegradable or recyclable packaging is lowering waste at the point of sale. Product take-back initiatives are enabling structured end-of-life recycling and are enhancing corporate responsibility perception.

Firms are differentiating themselves in competitive Western European markets by targeting consumers with established green purchasing behavior. Early integration of sustainable design principles is allowing manufacturers to command premium pricing while creating barriers to entry for competitors that lack similar capabilities. Alignment with circular economy strategies is reinforcing customer loyalty and improving reputational capital. Organizations that are managing sustainability across the entire value chain from raw material sourcing to disposal programs are strengthening operational resilience. Reduced energy use and material optimization are lowering long-term production costs, while transparent reporting is enhancing investor confidence. Strategic commitment to environmental performance is therefore supporting both revenue expansion and durable profitability for players in the market for automatic milk frothers.

Category-wise Analysis

Material Insights

Stainless steel is slated to maintain a dominant position, with an estimated 60% of the automatic milk frother market revenue share in 2026. Consumers value stainless steel automatic milk frothers for their exceptional durability that withstands daily intensive use. The material resists rust and corrosion even with frequent milk exposure and cleaning. Superior heat conduction ensures even temperature distribution for consistent foam quality. Its polished, professional appearance elevates kitchen aesthetics and matches commercial-grade standards. This combination of longevity and performance establishes stainless steel's leadership across premium market segments. Households and businesses alike trust it for reliable operation over extended periods.

Plastic is likely to be the fastest-growing segment during the 2026-2033 forecast period. Budget-conscious consumers actively choose plastic automatic milk frothers due to their attractive affordability compared to premium materials. The lightweight construction enhances portability for travel, dorm living, or small kitchen spaces. Vibrant color options appeal to younger demographics and coordinate with modern kitchen aesthetics. These attributes perfectly suit casual home brewing routines rather than intensive commercial demands. Recent advancements in heat-resistant plastics significantly broaden market accessibility. Enhanced formulations withstand repeated thermal cycles without deformation or safety risks. Manufacturers achieve cost efficiencies through high-volume production capabilities.

Application Insights

Residential is expected to hold the highest revenue share, estimated to reach 78% in 2026. The residential segment significantly drives market expansion as home brewing gains popularity. Consumers increasingly seek high-quality coffee experiences without leaving their homes. Demand surges for electric milk frothers that deliver professional-grade foam quality. This market attracts diverse users, from casual coffee drinkers to dedicated home baristas. Enthusiastic consumers willingly invest in premium kitchen appliances to elevate their daily routines and achieve barista-level results. The rise of remote working arrangements and the subsequent reduction in visits to coffee shops have further bolstered the demand for automatic milk frothers.

Commercial application is expected to be the fastest-growing segment between 2026 and 2033. This segment serves cafés, restaurants, hotels, and other hospitality venues that need dependable frothing solutions. Commercial operations prioritize durability, consistent performance, and high-volume capacity while maintaining milk quality. As the food service sector recovers from pandemic disruptions, businesses emphasize superior customer experiences. This focus accelerates adoption of advanced electric milk frothers to meet rising service standards.

Sales Channel Insights

Online retail is poised to lead with an approximate 55% of the automatic milk frother market share in 2026, led by Amazon, Alibaba, and brand websites. E-commerce enables competitive pricing through reduced overhead, extensive product comparisons, and user review access influencing purchase decisions. Subscription models offering replacement frothing discs and cleaning solutions generate recurring revenue streams. Digital marketing strategies utilizing social media influencers and video demonstrations effectively reach target demographics. COVID-19 permanently shifted consumer purchasing patterns toward online channels. This ease of access and the ability to browse a wide selection of products from the comfort of one's home have made online retail a preferred choice for many consumers.

The offline retail segment, on the other hand, is anticipated to be the fastest-growing over the 2026-2033 forecast period. These channels attract impulse buyers through in-store promotions and immediate product availability. Physical stores enable manufacturers to demonstrate cutting-edge innovations and foster brand loyalty via direct consumer interactions. Even with online retail's rapid expansion, brick-and-mortar locations maintain essential roles. These outlets strengthen the overall distribution strategy for electric milk frothers and ensure broad market accessibility.

Regional Insights

North America Automatic Milk Frother Market Trends

North America is set to command a significant portion of the automatic milk frother market share at approximately 38% in 2026. The United States leads regional demand through robust coffee culture and widespread specialty beverage consumption. Strong e-commerce infrastructure enables seamless product distribution to households. Regulatory bodies enforce stringent safety certifications, such as those from Underwriters Laboratories (UL) and the Food and Drug Administration (FDA). Innovation hubs in key states accelerate product development cycles. Major retailers maintain extensive distribution networks across physical and digital channels. Affluent consumers favor premium models that integrate with smart home ecosystems.

Market dynamics in Canada mirror the trends in the United States, buttressed by highly similar coffee consumption patterns. Businesses prioritize replacement demand over initial adoption in this mature landscape. Competitive pressures intensify from private label offerings and direct-to-consumer brands. Investment flows toward sustainable manufacturing practices and design differentiation. Companies can succeed through omnichannel strategies that blend online convenience with physical store experiences, while manufacturers should target premiumization opportunities among tech-savvy households. Strategic focus on connected appliances can unlock a large untapped growth potential in established markets. Leaders who balance innovation with regulatory compliance capture sustained regional dominance.

Europe Automatic Milk Frother Market Trends

Europe is anticipated to retain its strong presence in the global market for automatic milk frothers through 2033. Deeply rooted coffee traditions fuel consistent demand across diverse countries. Germany leads regional performance through consumers' expectations for engineering excellence and thoughtful design. The United Kingdom experiences steady growth from expanding specialty coffee culture and rising at-home consumption patterns. France adapts traditional café experiences to residential settings. Spain demonstrates accelerating demand among expanding middle-class households. EU regulatory frameworks standardize product requirements through CE marking and Restriction of Hazardous Substances (RoHS) compliance. Energy efficiency directives under Energy-related Products (ErP) regulations push manufacturers toward innovative designs.

Competitive dynamics blend established local brands with international competitors. German companies emphasize precision engineering while Italian firms leverage espresso heritage advantages. Consumers show strong preference for sustainable and energy-efficient appliances. Investment opportunities emerge in smart connectivity features and eco-design innovations. Eastern European markets offer expansion potential through rapidly developing coffee cultures. Brexit creates supply chain challenges through tariff adjustments and regulatory differences in the United Kingdom market. Scandinavian countries approach market maturity, requiring manufacturers to focus on replacement demand and product upgrades. Companies should prioritize regulatory alignment and sustainability positioning to capture premium pricing across diverse regional preferences.

Asia Pacific Automatic Milk Frother Market Trends

Asia Pacific is poised to emerge as the fastest-growing market for automatic milk frothers from 2026 to 2033. China spearheads expansion through rapid urbanization and rising disposable incomes among middle-class households. Urban consumers embrace Western coffee lifestyles alongside expanding coffee shop chains. Japan maintains mature market dynamics with emphasis on technological sophistication and space-efficient designs for compact living environments. India demonstrates exceptional growth potential fueled by youthful demographics and proliferating cafés across major cities. The ASEAN market, headlined by Indonesia, Thailand, and Vietnam, benefits from young populations and tourism-driven consumption patterns. Regional manufacturing hubs produce cost-competitive products that supply global demand.

Local brands are seeking to capture price-sensitive segments through aggressive pricing strategies compared to international competitors. Regulatory frameworks differ across markets, with developed economies enforcing strict safety standards while emerging markets are developing modern, technology-led compliance systems. E-commerce platforms dominate urban distribution channels and are accelerating market penetration in the region. Investment priorities are presently centered on local partnerships, expanded distribution networks, and product adaptations for regional taste preferences. Companies should prioritize localization strategies that address diverse consumer palates and space constraints.

Competitive Landscape

The global automatic milk frother market structure is a moderately concentrated one, with Breville Group, Nestlé Nespresso, Groupe SEB, De'Longhi Appliances, and Aerolatte collectively controlling between 40% and 45% of the total revenues. These established brands are leveraging strong distribution networks, product innovation capabilities, and global brand recognition to sustain market leadership. Demand is increasing as consumers are seeking café-quality beverages within home environments. Advanced temperature-controlled frothing systems are improving foam density and consistency across beverage formats such as cappuccino and latte. Buyers are also prioritizing higher-capacity units that deliver reliable performance for multiple servings. Competitive positioning is increasingly depending on product reliability, ease of cleaning, and compatibility with broader coffee appliance ecosystems.

Premium brands are leading across electric countertop devices, portable battery-operated units, and manual frothing tools to address different consumer budgets and usage patterns. Smart automatic frothers are gaining adoption as they integrate with coffee machines and support digital interfaces, programmable settings, and precise thermal management. Manufacturers are embedding sensor-based control systems to maintain stable froth texture and prevent overheating. Sustainability considerations are influencing product development strategies, and companies are incorporating energy-efficient components and recyclable materials into appliance design. As competitive intensity is increasing, firms that are combining technology integration with strong after-sales support are positioning themselves for sustained growth in this expanding household appliance category.

Key Industry Developments

- In November 2025, Heylo, an induction-heated espresso equipment maker, launched Milky, a compact, standalone automated milk frother for cafés at HostMilano 2025. The machine aerates dairy and plant-based milks across 25+ foam settings, dispenses them hot or cold with precise temperature control, and features automatic milk return to coolers.

- In August 2025, De'Longhi launched the LatteMix Cold and Hot Frother in the U.S., a kettle-style electric device that creates both hot and cold foams for dairy and plant-based milks used in lattes, iced coffees, and matcha.

- In August 2025, Smeg launched the Mini Milk Frother (MFF02), a compact, affordable cylinder-shaped device available in classic colors such as cream, black, pastel green, baby blue, and red. The 180ml-capacity unit produces hot/cold froth and warm milk for cappuccinos, iced matcha, or protein shakes using a ceramic non-stick lining for effortless, non-toxic cleaning.

Companies Covered in Automatic Milk Frother Market

- Breville Group Limited

- Nestlé Nespresso SA

- Groupe SEB

- De'Longhi Appliances S.r.l.

- Secura

- Aerolatte Ltd.

- Capresso

- Cuisinart

- Melitta Group

- Bodum

- Bialetti Industrie S.p.A.

- Smeg S.p.A.

- Xiaomi Corporation

- Lavazza Group

Frequently Asked Questions

The global automatic milk frother market is projected to reach US$ 460.0 million in 2026.

Rising home café-style beverage demand, smart technology integration, and sustainability preferences are propelling market growth.

The market is poised to witness a CAGR of 6.1% from 2026 to 2033.

Premiumization through IoT-connected features, expansion into emerging Asia-Pacific coffee cultures, and eco-friendly material innovations offer substantial growth potential.

Breville Group Limited, Nestlé Nespresso SA, Groupe SEB, De'Longhi Appliances S.r.l., and Aerolatte Ltd. are some of the key players in the market.