- Industrial Machinery

- Automatic Distillation Analyzer Market

Automatic Distillation Analyzer Market Size, Share, and Growth Forecast 2025 - 2032

Automatic Distillation Analyzer Market by Product Type (Hydrocarbons Distillation Analyzer, Others), Application (Gasoline, Fuels, Aromatics, Solvents, Hydrocarbons), End-user (Pharmaceutical Industry, Automotive Industry, Others), and Regional Analysis for 2025 - 2032

Automatic Distillation Analyzer Market Size and Trend Analysis

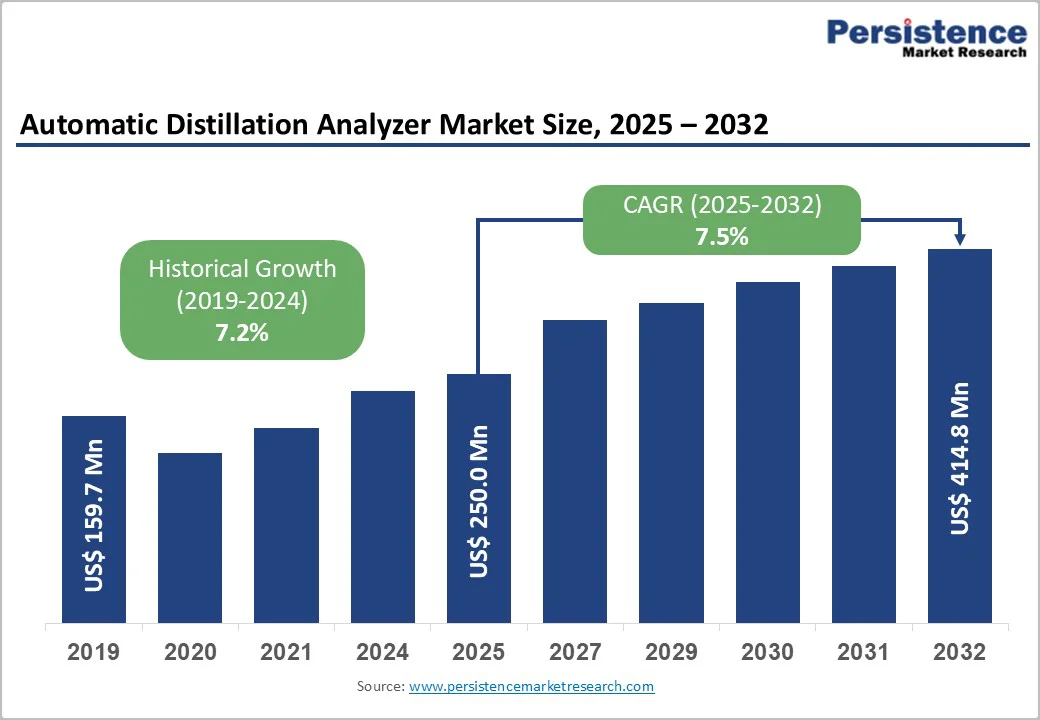

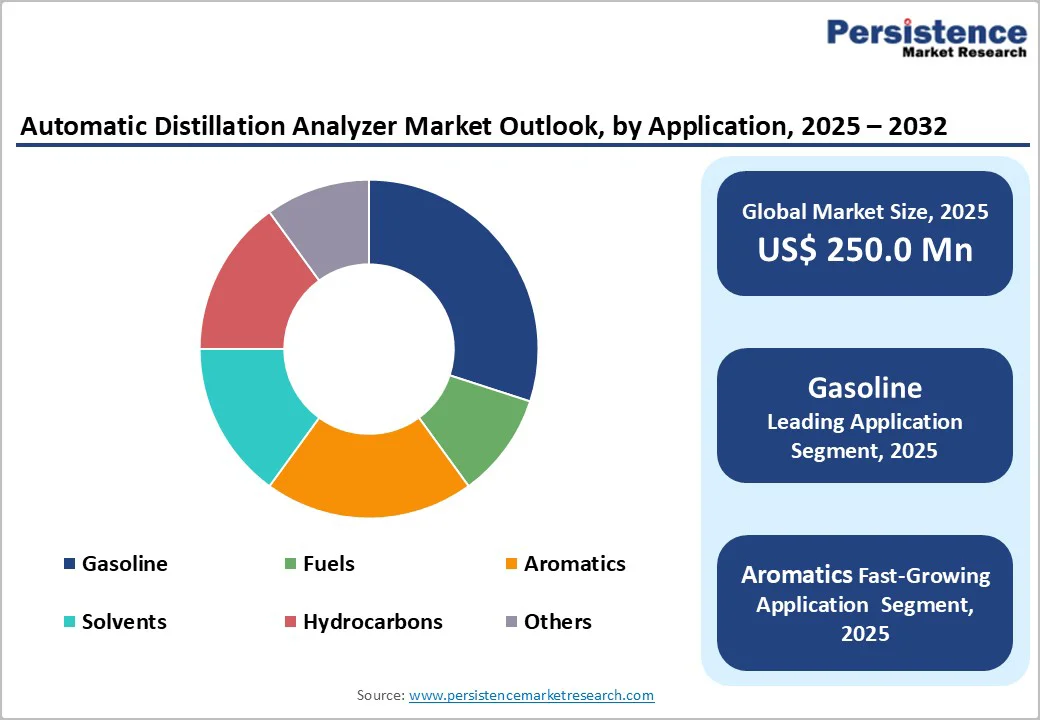

The global automatic distillation Analyzer market size is likely to be valued at US$250.0 million in 2025 and is expected to reach US$414.8 million by 2032, growing at a CAGR of 7.5% during the forecast period from 2025 to 2032, driven by increasing demand for precise quality control and regulatory compliance across industries such as petroleum refining, pharmaceuticals, and chemicals.

Rising requirements for accurate fuel testing, solvent purification, and product standardization in manufacturing processes are fueling the adoption. Expanding industrialization, the growing need for efficient process monitoring, and advancements in automated and portable analyzer technologies are further supporting market expansion.

Key Industry Highlights

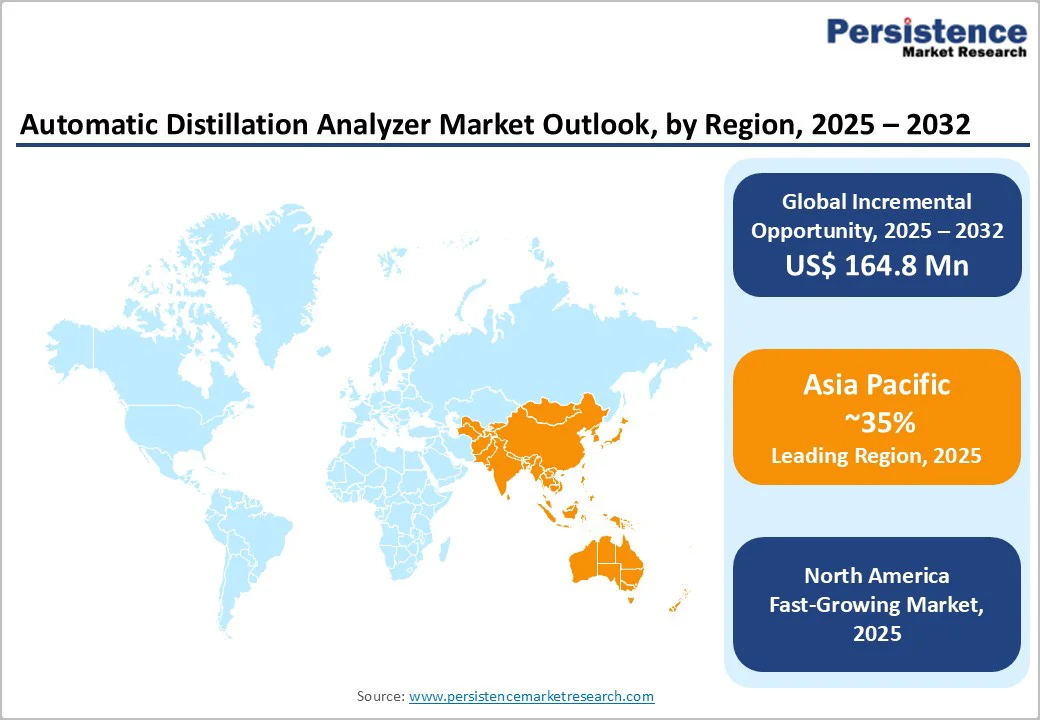

- Leading Region: Asia Pacific leads the market with over 35% share, driven by rapid industrialization, rising FDI, and expanding petroleum and pharmaceutical sectors.

- Fastest-Growing Region: North America emerges as the fastest-growing region, with strict EPA and FDA regulations, strong petrochemical and pharmaceutical industries, and ongoing innovation in automated quality compliance technologies.

- Leading Product Type: Hydrocarbons distillation analyzers lead the market with about 45% revenue share, driven by strong demand from the petroleum refining sector.

- Leading Application: Gasoline applications lead the market with about 35% revenue share, supported by strict quality standards in the automotive and fuel industries.

- Leading End-user: The pharmaceutical industry leads the market with nearly 40% revenue share in 2025, driven by strict quality and safety standards requiring accurate distillation data.

| Key Insights | Details |

|---|---|

|

Automatic Distillation Analyzer Market Size (2025E) |

US$250.0 Mn |

|

Market Value Forecast (2032F) |

US$414.8 Mn |

|

Projected Growth CAGR (2025-2032) |

7.5% |

|

Historical Market Growth (2019-2024) |

7.2% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Stringent Regulatory Standards across Industries

The demand for distillation analyzers is being propelled by stringent regulatory standards across multiple industries. Agencies such as the U.S. Environmental Protection Agency (EPA), the European Chemicals Agency (ECHA), and the Food and Drug Administration (FDA) enforce rigorous quality, purity, and safety norms across the petroleum, pharmaceutical, and food processing sectors. These regulations mandate precise measurement and documentation of volatile compounds, fuel composition, and product distillation ranges to ensure compliance and reduce environmental impact. The growing emphasis on sustainability and reducing industrial waste requires more accurate and automated distillation monitoring, driving the adoption of advanced analyzers. Manufacturers are increasingly investing in analyzers capable of integrating with digital data systems to maintain regulatory records efficiently.

The tightening of environmental emission norms and consumer safety regulations has significantly increased the pressure on industries to modernize testing and quality control infrastructure. Within the petrochemical and automotive sectors, standards for gasoline, diesel, and solvents demand real-time distillation analysis to ensure optimal performance and lower carbon emissions. In pharmaceuticals and food processing, regulators emphasize solvent purity and contamination control, driving continuous technological advancements in analyzer design. The rise in complex fuel blends and innovative pharmaceutical formulations requires analyzers with higher precision, reliability, and faster throughput, making them essential for maintaining competitive advantage in these markets.

High Initial Investments and Maintenance Costs

High initial investments and maintenance costs present a significant restraint to the widespread adoption of distillation analyzers across industries. These analyzers incorporate advanced automation, precision sensors, and digital control systems that ensure accurate and repeatable measurements, but at a considerable upfront cost. For many SMEs, particularly in emerging markets, the high cost of purchasing and installing such equipment remains prohibitive. The integration of analyzers with laboratory information management systems (LIMS) or automated production lines can increase setup complexity and capital requirements, further limiting adoption among smaller operators.

Beyond installation, ongoing maintenance and operational costs also pose challenges. Distillation analyzers require frequent calibration, component replacement, and specialized technical expertise to ensure consistent performance and compliance with quality standards. Software updates and spare parts can add to long-term expenditures, making it difficult for smaller facilities to sustain operations efficiently. Industries dealing with high-throughput processes, such as petrochemical refining and pharmaceuticals, face increased operational pressures, as any downtime for maintenance can disrupt production and impact profitability, further restraining widespread adoption.

Adoption of Portable and Fixed Analyzer Innovations

Industries increasingly prioritize flexibility, accuracy, and efficiency in quality control. Modern distillation analyzers are being developed with advanced automation, compact designs, and digital connectivity features. Portable analyzers, in particular, enable on-site testing in remote or field environments, reducing turnaround time and operational costs. Fixed analyzers provide high-throughput, continuous monitoring capabilities for laboratory and production line applications, supporting large-scale operations with consistent precision.

These technological advancements align with the push toward smarter, more efficient industrial operations. The combination of portability and automation allows companies to meet stringent regulatory standards while maintaining cost efficiency and operational agility. The rising demand from sectors such as petrochemicals, pharmaceuticals, and food processing, where real-time analysis and quality consistency are critical, further accelerates adoption. The integration of analyzers with Industry systems and predictive maintenance tools enhances process optimization, positioning portable and fixed analyzers as essential solutions in modern industrial quality control workflows.

Category-wise Insights

Product Type Analysis

Hydrocarbons distillation analyzers lead the market, accounting for approximately 45% revenue share in 2025. Their dominance is primarily attributed to extensive use in the petroleum and petrochemical industries, where accurate distillation profiling is critical for refining processes, fuel formulation, and regulatory compliance. These analyzers play an essential role in determining the boiling point distribution of hydrocarbons. For example, devices such as the Anton Paar PetroOxy and Metrohm 870 KF Titrino are widely used for laboratory-based hydrocarbon analysis in refineries and chemical plants. The rising demand for high-precision analyzers in applications such as gasoline, diesel, and lubricants testing further strengthens this segment.

The portable automatic distillation analyzer segment is the fastest growing, driven by the rising need for on-site testing and field-based quality verification in oil exploration, refining, and chemical manufacturing. Portable analyzers provide real-time results with high accuracy, enabling faster decision-making and reduced downtime in remote operations. Their compact design, ease of transportation, and minimal setup requirements make them ideal for decentralized testing environments. Examples include the AMETEK Process Instruments Auto Distillation Analyzer and Buchi Distillation System B-811, which are used in field testing and decentralized laboratories.

Application Type Analysis

The gasoline application segment leads the distillation analyzer market, with 35% of revenue share in 2025, driven by strict quality control standards in the automotive and fuel industries, where accurate distillation data is essential for optimizing fuel performance, meeting emission norms, and ensuring regulatory compliance. Distillation analyzers assess gasoline’s volatility, blending, and combustion quality, directly influencing engine efficiency and emissions. For example, refineries and fuel testing laboratories widely use automated analyzers such as PAC OptiDist and Herzog HDA series to comply with ASTM D86 and ISO standards. The growing adoption of cleaner fuel blends and tighter emission regulations reinforces the dominance of this segment, prompting refiners to invest in advanced, automated distillation solutions.

The aromatics application segment is witnessing the fastest growth, driven by rising demand from chemical manufacturing, solvent production, and specialty applications such as coatings and adhesives. Advanced distillation analyzers enable precise boiling point measurement and compositional control of aromatics such as benzene, toluene, and xylene (BTX). Growing investments in high-purity chemical production and process automation have accelerated the adoption. Producers of high-purity solvents commonly use automated distillation systems, including Anton Paar units, to maintain consistent quality standards. Increasing investments in specialty chemicals and the ongoing automation of chemical processing facilities are further driving adoption.

End-user Type Analysis

The pharmaceutical industry leads the distillation analyzer market, accounting for nearly 40% of revenue share in 2025, driven by the sector’s strict regulatory standards and the need for precise distillation data to ensure product purity, stability, and compliance with international quality norms such as the FDA and EMA guidelines. Distillation analyzers are extensively used in API manufacturing, solvent recovery, and formulation testing to verify boiling ranges and solvent quality. For example, ethanol, acetone, and methanol distillation testing are critical in injectable and oral drug production. Major pharmaceutical manufacturers and contract manufacturing organizations increasingly adopt automatic ASTM-compliant distillation analyzers to support GMP documentation, batch validation, and audit readiness.

The food processing industry represents the fastest-growing end-user segment, and increasing emphasis on product quality, flavor consistency, and consumer safety is encouraging food manufacturers to adopt automated analyzers for precise solvent and ingredient distillation. Distillation analyzers are used for alcohol content analysis in spirits and beverages, as well as testing flavor extracts, edible solvents, and food additives. For example, breweries, distilleries, and flavor houses rely on automated distillation systems to ensure consistency in ethanol concentration and aroma compounds. The rising demand for processed and packaged foods, along with stricter regulations from authorities such as the FDA and EFSA, is accelerating the adoption of reliable, automated distillation analysis solutions across the food industry.

Regional Insights

North America Automatic Distillation Analyzer Market Trends

North America is the fastest-growing region, driven by its advanced industrial infrastructure and stringent regulatory environment. The U.S. leads the market, accounting for a significant share due to widespread adoption across the petroleum, chemical, and pharmaceutical industries. Regulatory authorities, including the U.S. Environmental Protection Agency (EPA) and the Food and Drug Administration (FDA), require rigorous testing and quality verification, boosting demand for precise, automated distillation systems. Companies such as PAC (Petroleum Analyzer Company) play a crucial role by providing advanced distillation analyzers extensively used in fuel laboratories and refineries throughout North America.

Technological innovation continues to be a key growth driver in the region. Leading manufacturers are increasingly integrating digital monitoring, AI-driven data analytics, and IoT-enabled systems into analyzer designs to enhance accuracy and enable real-time performance tracking. The region also benefits from robust R&D investment and comprehensive aftermarket service networks. For instance, AMETEK Grabner Instruments supplies highly automated distillation analyzers for gasoline, diesel, and solvent testing, further solidifying North America’s position as a leader in high-precision analytical instrumentation.

Europe Automatic Distillation Analyzer Market Trends

Europe maintains a strong position in the automatic distillation analyzer market, supported by strict environmental regulations, advanced industrial standards, and a well-established chemical and energy sector. The region’s focus on fuel efficiency, emission reduction, and sustainable production practices has driven the adoption of precise, automated distillation analysis systems. Regulations such as REACH and EEA directives enforce rigorous fuel and chemical testing requirements, increasing demand for high-performance analyzers. Companies such as Anton Paar are widely used across Europe for fuel and solvent testing, ensuring compliance with EN and ASTM standards.

Technological innovation and sustainability are key drivers in the European market. Leading manufacturers in Germany, the U.K., and France are incorporating IoT-enabled monitoring, AI-powered analytics, and energy-efficient components to improve operational performance. Collaborative initiatives between research institutions and industrial players are accelerating the development of next-generation analyzers with enhanced accuracy and automation. For instance, Herzog (a PAC company) produces advanced automatic distillation analyzers in Germany, extensively used in European laboratories for petroleum and chemical analysis, further reinforcing Europe’s leadership in precision instrumentation.

Asia Pacific Automatic Distillation Analyzer Market Trends

Asia Pacific is the leading region in the automatic distillation analyzer market, accounting for approximately 35% of the global share. This is supported by a robust industrial base, expanding refining capacity, and a strong presence in the pharmaceuticals and food processing sectors. Key contributors include China and India, where rapid industrialization and government initiatives promoting advanced quality control technologies are driving market growth. Stricter fuel quality and emission regulations across the region have increased the demand for accurate distillation testing in the petrochemical and automotive industries. Companies such as Tanaka Scientific (Japan) and Labtronics India supply distillation analyzers widely to refineries, fuel testing laboratories, and pharmaceutical manufacturers throughout the region.

The region benefits from cost-effective manufacturing, rising foreign investment, and a skilled technical workforce, establishing it as a hub for analytical instrument production. Major international players are expanding operations and forming partnerships to capitalize on local demand and export opportunities. The growing automotive and petrochemical sectors further drive demand, as stricter fuel quality and emission standards push industries toward precise and automated distillation systems. For example, PAC and Anton Paar have strengthened their presence in China and Southeast Asia through strategic partnerships and regional facilities.

Competitive Landscape

The global automatic distillation analyzer market is moderately fragmented, characterized by the presence of established international manufacturers alongside agile regional players. Advances in automation, digital connectivity, and stringent regulatory compliance have lowered entry barriers, enabling new and specialized companies to compete with traditional market leaders. Strong demand from the petroleum refining, pharmaceutical, chemical, and food processing industries continues to drive innovation.

Key market leaders include Anton Paar, PAC (Petroleum Analyzer Company), AMETEK Grabner Instruments, Herzog (a PAC company), and Metrohm. These companies leverage strong brand recognition, deep technical expertise, and extensive global service networks. Competition centers on continuous R&D, product upgrades, and expansion of aftermarket support. Strategic partnerships with regional distributors and service providers help broaden market reach. Differentiation is achieved through energy-efficient designs, digital integration, and superior customer support, while competitive pricing and modular system configurations allow regional players to gain market traction.

Key Industry Developments:

- In October 2025, Koehler Instrument Company introduced its Automatic Distillation Analyzer Series 5000, designed for precise distillation analysis of gasolines, fuels, solvents, aromatics, naphthas, kerosenes, and other volatile products. The system fully automates testing, data processing, and reporting in compliance with ASTM D86, ASTM D850, and ISO standards. It supports distillation groups 0–4, enables networking of up to 32 units, and features programmable receiver chamber control up to 60°C, offering high efficiency and flexibility for quality control laboratories.

- In March 2025, PAC LP (USA) introduced OptiDist 2, a next-generation automatic distillation analyzer designed to meet and exceed current industry standards. The system supports ASTM D86 and related ASTM, ISO, and IP test methods, offering high precision, advanced automation, and improved ease of use for fuel and chemical testing laboratories.

Companies Covered in Automatic Distillation Analyzer Market

- PAC LP (AMETEK Inc.)

- Koehler Instrument Company, Inc.

- Grabner Instruments (AMETEK)

- Tanaka Scientific Ltd.

- LabTech S.r.l.

Frequently Asked Questions

The automatic distillation analyzer market is valued at US$250 million in 2025 and expected to reach US$414.8 million by 2032, reflecting robust growth.

The primary demand drivers for the automatic distillation analyzer market include strict regulatory standards, increasing focus on process optimization and industrial expansion, government investments in quality infrastructure, and advancements in sensor technology and automation for enhanced quality control.

Hydrocarbons distillation analyzers lead with a 45% share, due to widespread demand in petroleum refining.

Asia Pacific dominates the automatic distillation analyzer market, holding over 35% of the global share, driven by rapid industrialization, expanding refining capacity, and strong growth in the pharmaceuticals and food processing sectors.

Opportunities exist in emerging economies, the development of portable analyzer variants, and the integration of AI and IoT for advanced analytics.