- Aerospace & Defense

- Aircraft Ground Support Equipment Market

Aircraft Ground Support Equipment Market Size, Share, and Growth Forecast, 2025 - 2032

Aircraft Ground Support Equipment Market by Equipment (Passenger Service, Airport Service, Cargo Loading, Container Loaders, Belt Loaders, Cargo Transporters), Power (Electric, Non-Electric, Hybrid), Ownership (New Sales, Used Sales, Rental), End-user, and Regional Analysis for 2025 - 2032

Aircraft Ground Support Equipment Market Size and Trends Analysis

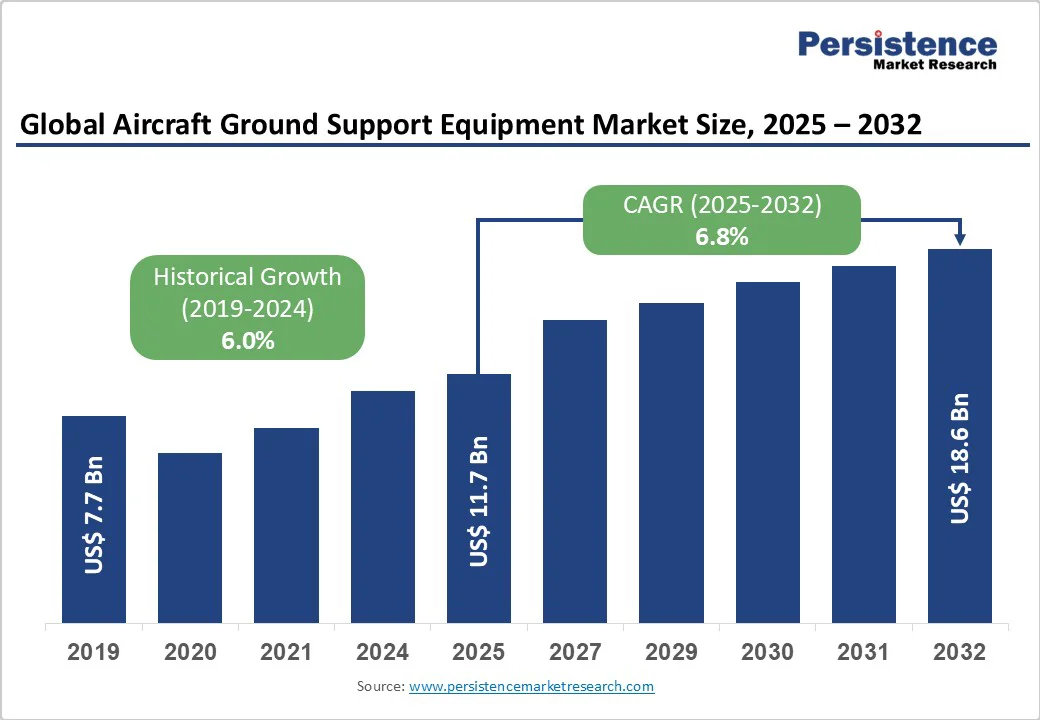

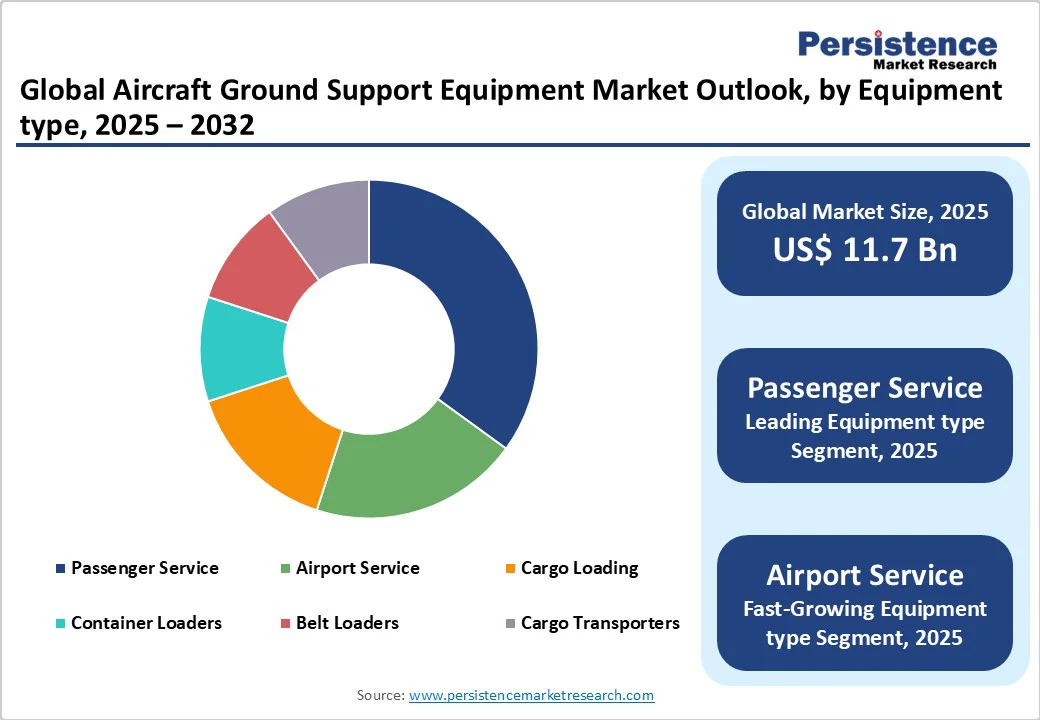

The global aircraft ground support equipment market size is likely to be valued at US$11.7 Bn in 2025 and is projected to reach US$18.6 Bn by 2032, growing at a CAGR of 6.8% between 2025 and 2032. Growth is primarily driven by accelerating airport expansion and modernization worldwide, regulatory pressure to reduce emissions prompting electrification of ground support fleets, and increased air travel volumes post-pandemic, boosting demand for efficient, reliable GSE.

Key Industry Highlights:

- Passenger Service equipment dominates with a 27.7% share in 2025, reflecting strong demand for passenger handling and comfort-focused solutions across major commercial airports.

- Non-Electric GSE leads with a 65.8% share in 2025, highlighting continued reliance on conventional power systems for cost efficiency and operational familiarity.

- New sales account for a 37.6% share in 2025, reflecting consistent investment in fresh fleets by large commercial hubs and private airports.

- Commercial airports accounted for 61.8% of total traffic in 2025, underscoring their position as the primary demand hub due to rising passenger traffic and ongoing terminal expansions.

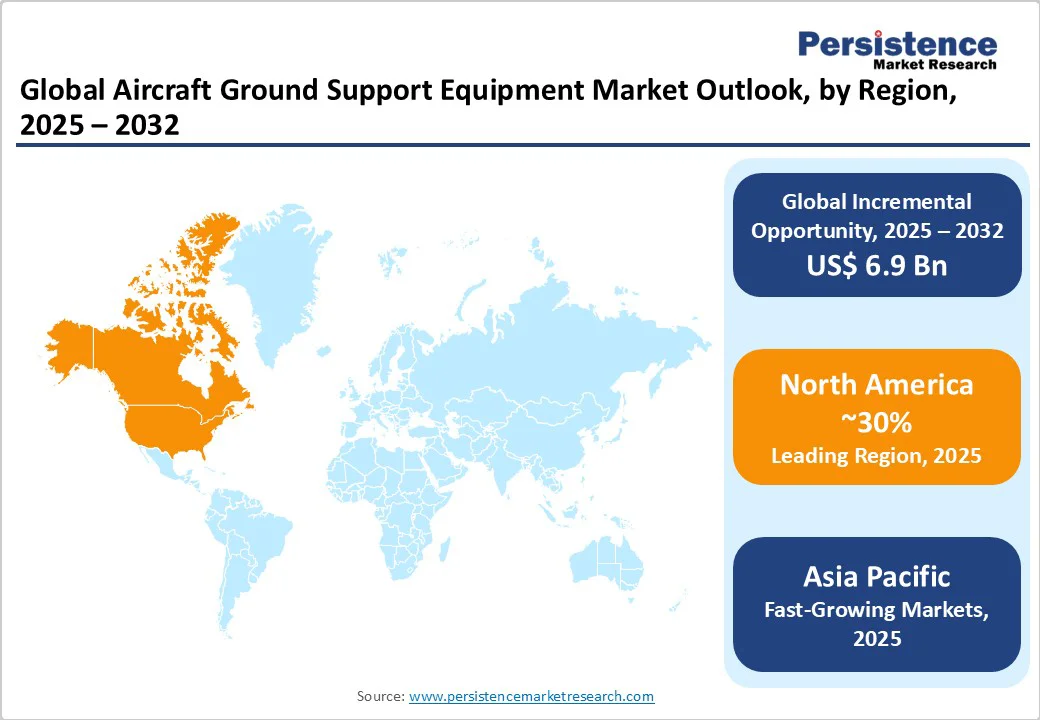

- North America remains a key leader, driven by strong infrastructure upgrades, technology adoption, and sustainability investments. Europe and the Asia Pacific present high growth potential, supported by green airport mandates, next-gen infrastructure programs, and rapid air travel expansion across emerging markets.

- Industry players are accelerating GSE fleet electrification, scaling rental and leasing business models, and forming technology partnerships focused on battery-electric, autonomous, and digital-enabled equipment. These strategies highlight the sector’s pivot toward sustainable operations and service-based revenue growth.

| Key Insights | Details |

|---|---|

|

Aircraft Ground Support Equipment Market Size (2025E) |

US$11.7 Bn |

|

Market Value Forecast (2032F) |

US$18.6 Bn |

|

Projected Growth (CAGR 2025 to 2032) |

6.8% |

|

Historical Market Growth (CAGR 2019 to 2024) |

6.0% |

Market Dynamics

Driver - Technological Innovation and Ownership Model Shifts

Advancements in automation, telematics, remote monitoring, and digital interfaces are enhancing the efficiency and safety of GSE. Airports are investing in smart tracking, predictive maintenance, and autonomous equipment to reduce human error and improve turnaround times. Also, rental and leasing ownership models are gaining traction as airports aim to reduce capex and asset obsolescence risk. Rental ownership appears as the fastest-growing ownership segment (though New Sales dominate currently) because airports can scale usage without large upfront capital. These trends combine to drive demand for newer-generation GSE with high uptime and operational flexibility.

Regulatory Pressure and Sustainability Mandates

Environmental regulations, carbon-emission targets, and airport sustainability goals are driving the shift toward electric and hybrid GSE. Persistence Market Research notes that electric and hybrid categories are the fastest-growing power segments, as non-electric dominated in 2025. Still, airports are increasingly adopting battery-electric GSE to reduce emissions and comply with local and international sustainability norms. Adoption of emission regulations (e.g., regional air quality standards, noise regulations) increases operational costs of diesel/non-electric GSE (fuel, maintenance, emissions penalties), favoring electric equipment. Additionally, cost savings in fuel and maintenance over the life cycle and incentive programs (e.g., grants, tax incentives) support investment in cleaner GSE.

Restraint - High Initial CapEx and Total Cost of Ownership for Advanced/ Electric GSE

A major restraint in the Aircraft Ground Support Equipment (GSE) market is the high initial cost of electric and hybrid units compared to conventional diesel-powered equipment. Significant investment is required for battery systems, charging infrastructure, and specialized maintenance, making adoption challenging for small and mid-sized airports with limited budgets. Uncertainty over long-term cost savings and extended payback periods further discourages procurement. As a result, many operators defer purchases or continue relying on non-electric alternatives, slowing the market penetration of sustainable GSE despite regulatory support and environmental benefits.

Supply Chain Constraints and Component Availability

The aircraft ground support equipment market faces constraints due to global supply chain disruptions and complex certification processes. Shortages of batteries, semiconductors, high-grade metals, and specialized electronics often lead to extended lead times and higher costs for electric or hybrid GSE. Logistics delays and skilled labor shortages further affect timely delivery and equipment quality.

Strict regulatory certifications, safety standards, and airport compatibility requirements (e.g., weight restrictions, power supply) add layers of complexity. These factors slow the replacement of older fleets and hinder large-scale adoption of advanced GSE, restraining overall market growth despite rising demand.

Key Market Opportunities

Growth in Rental/Leasing Models and Military Airport Demand

Rental is the fastest-growing ownership segment. Many airports, particularly in emerging markets, prefer rental/leasing over outright purchase to reduce capital expenditure and manage maintenance risks. This presents opportunities for GSE companies to offer flexible ownership, subscription, or rental models. Additionally, military airports are the fastest-growing end users, spurred by defense modernization, the increasing use of air force bases for dual civilian/military operations, and government budget allocations. Manufacturers can tailor product lines to meet military specifications (ruggedness, durability, interoperability) to capture this high-growth niche.

Rapid Electrification (Electric GSE) as a High-Potential Avenue

The power segment, dominated by non-electric devices in 2025, presents a significant opportunity for electric GSE to gain ground. Regulatory push toward carbon neutrality, incentive schemes, and airport sustainability mandates (both governmental and airport-authority-led) provide tailwinds. Forecasts suggest that electric GSE will be the fastest-growing power source segment, as airports replace traditional diesel units. Suppliers that develop reliable, rugged electric models and support infrastructure (e.g., chargers, battery swap or charging stations) can secure premium contracts and recurring service revenue.

Category-wise Analysis

Equipment Type Insights - Passenger Service Leads, Cargo Loading Expands Fastest

The Passenger Service equipment segment held a 27.7% share in 2025, driven by boarding bridges, ground power units, and pushback tugs, all essential for passenger handling. Growth is supported by post-COVID traffic recovery and terminal capacity expansions, as airports prioritize tighter turnaround times and improved passenger experiences.

Cargo loading equipment is projected to record the fastest CAGR through 2032, fueled by booming global air freight volumes, e-commerce, and cross-border trade. Increasing adoption of container loaders, cargo transporters, and heavy-duty systems underscores operators’ focus on efficiency, throughput capacity, and cost optimization in cargo operations. Together, these segments highlight evolving airport priorities across passenger and cargo domains.

Power Insights Non-Electric Dominates, Electric Accelerates Rapidly

In 2025, non-electric GSE accounts for nearly 65.8% of the market, supported by diesel and mechanical systems that benefit from existing infrastructure, lower capital costs, and easier maintenance. Many large airports and cargo hubs continue to rely on these units, even though electric charging infrastructure is underdeveloped or retrofit costs are prohibitive.

The Electric GSE segment is projected to grow at the fastest CAGR through 2032, driven by regulatory mandates to reduce emissions, airport sustainability initiatives, and government subsidies. Innovations in battery energy density, charging efficiency, and lifecycle performance, alongside favorable total cost of ownership, are significantly boosting the adoption of electric belt loaders, tugs, and other zero-emission ground-handling equipment.

Ownership Insights - New Sales Lead, Rental Emerges as Fastest Growing

In 2025, new sales represent 37.6% of GSE market revenues, as airports and ground handling companies prioritize acquiring brand-new equipment with advanced features, warranty coverage, and higher efficiency to handle rising passenger volumes and stricter regulatory standards. New purchases also allow for tailored specifications, including power type, automation, and safety upgrades, making them attractive despite higher upfront costs.

Conversely, the Rental model is projected to be the fastest-growing ownership segment through 2032. Airports, especially in emerging markets, increasingly adopt leasing or shared ownership to minimize capital expenditure, reduce maintenance risks, and maintain operational flexibility. Rental providers offer scalable fleets, service contracts, and rapid access to newer technology, ensuring operators can respond quickly to seasonal peaks and evolving operational needs.

End-user Insights- New Sales Dominate, Rental Drives Future Growth

In the airport end-user, commercial airports hold a commanding 61.8% share, reflecting their central role in global air traffic, passenger handling, and cargo operations. The dominance is supported by large-scale infrastructure, rising international connectivity, and continuous investments in modernization and expansion projects. Commercial hubs prioritize safety, efficiency, and passenger experience, driving consistent demand for advanced systems and services.

The private airport segment is emerging as a key growth driver, fueled by rising business aviation, the growing number of high-net-worth individuals, and the demand for personalized, flexible air travel. Private airports are also investing in advanced technologies, sustainability measures, and luxury facilities to cater to elite clientele. This shift indicates strong future growth potential, even as commercial airports maintain market leadership.

Regional Insights and Trends

North America: Strong Market Share with Sustainability-Driven Modernization

North America represents a major share of the global GSE market in 2025, supported by a strong recovery in both domestic and international air travel, well-financed airport infrastructure, and stringent environmental regulations. The U.S. and Canada are investing heavily in electric and hybrid GSE as operators face pressure to cut carbon emissions, with clean-air regulations and incentive programs accelerating adoption. The presence of leading manufacturers, established service networks, and robust capital access for modernization projects strengthens the region’s competitive edge.

U.S. airlines operated 28,000 flights to over 800 airports across roughly 80 countries, facilitating the movement of around 2.5 million passengers and transporting 28,000 tons of cargo daily.

The United States aviation sector is well-established, with substantial government investment in maintaining and expanding airport infrastructure and in military aviation. The country has around 19,000 airports. Consequently, the need for ground support equipment is projected to surge at these airports to upgrade their current infrastructure.

Europe: Sustainability Mandates Driving Electric GSE Adoption

Europe commands a significant share of the global GSE market, with growth closely tied to ambitious sustainability and emission-reduction targets. Airports across Germany, the U.K., France, and Spain are expanding terminals, modernizing fleets, and adopting stricter emission and noise standards. EU-level regulatory harmonization simplifies certification, enabling faster deployment of equipment across member states. European manufacturers benefit from government subsidies, clean transport funding, and R&D programs focused on battery technology, lightweight materials, and green power sources.

Germany leads in adopting hybrid and electric GSE, while the U.K. emphasizes operational efficiency, and France and Spain invest in modernization. Future opportunities include deploying electric GSE at regional airports, retrofitting older fleets, and embedding automation and digital monitoring into day-to-day ground operations.

Asia Pacific: Rapid Airport Expansion and Strong GSE Growth Potential

Asia Pacific is emerging as the fastest-growing region in the global GSE market, driven by surging air travel and large-scale airport expansions across China, India, and Southeast Asia. Strong government investments in aviation infrastructure, new passenger terminals, and cargo facilities are fueling demand. While adoption of electric and hybrid GSE is still in its early stages, sustainability regulations and policy incentives are accelerating the shift from conventional equipment.

Local manufacturing hubs, cost advantages, and growing domestic OEMs enhance production capacity and competitiveness. ASEAN nations such as Thailand, Vietnam, and Indonesia are rising markets with expanding cargo and regional airport operations. Key challenges include limited charging infrastructure and financing barriers for rentals, yet opportunities in joint ventures, technology partnerships, and localized production remain substantial.

Competitive Landscape

The global aircraft ground support equipment market is moderately consolidated. Leading players such as TLD NV, JBT Corporation, Goldhofer, BEUMER Group, Textron, COBUS Industries, Tronair, AERO Specialties, among others, hold significant shares. Still, none dominate overwhelmingly; market share tends to be spread across the top 5-10 players.

The rest includes regional specialists and smaller innovators, especially those focusing on electric/hybrid GSE or automation/digital components. Competition is intense around product reliability, uptime, service & maintenance support, charging infrastructure for electric models, and total cost of ownership.

Key Industry Developments:

- In March 2024, Toyota Material Handling Europe, based in Sweden, invested USD 33.7 million in its most significant production project to enhance manufacturing capacity in Mjölby, Sweden.

- In May 2024, Dnata, a prominent global air and travel services provider, secured major agreements with top manufacturers, establishing five-year global framework contracts for new Ground Support Equipment (GSE) at the Dubai Airport Show. These contracts are valued at over USD 210 million throughout their duration.

- In January 2024, Shenzhen-based China International Marine Containers (Group) Co. Ltd. inaugurated the First Blue Sky Series Low-Carbon Energy Station, SL1500. The SL1500 has an estimated generating capacity of 1,200 kWh and a yearly carbon-reduction potential of 8,048 tons per unit.

Companies Covered in Aircraft Ground Support Equipment Market

- ITW GSE

- Textron GSE

- Wilcox GSE

- Air+MAK Industries

- TLD Group

- CLYDE Machines

- Wollard International

- MULAG

- Tiger GSE

- Iscar GSE

- Oshkosh Aerotec

- Tronair (Eagle)

- Other Market Players

Frequently Asked Questions

The Aircraft Ground Support Equipment market is estimated to be valued at US$ 11.7 Bn in 2025.

The key demand driver for the Aircraft Ground Support Equipment (GSE) market is the expansion and modernization of global airport infrastructure, driven by rising passenger and cargo traffic.

In 2025, the North America region will dominate the market with an exceeding 30% revenue share in the global Aircraft Ground Support Equipment market.

Among the Equipment Type, Passenger Service Equipment holds the highest preference, capturing beyond 27.7% of the market revenue share in 2025, surpassing other parts.

The key players in the Aircraft Ground Support Equipment market are ITW GSE, Textron GSE, Wilcox GSE, Air+MAK Industries, and TLD Group