- Industrial Machinery

- Additive Manufacturing Market

Additive Manufacturing Market Trends, Size, Share, Growth, and Forecast, 2025 - 2032

Additive Manufacturing Market By Technology (Vat Photopolymerization, Material Jetting, Binder Jetting, Material Extrusion, Powder Bed Fusion, Sheet Lamination, and Directed Energy Deposition) Material (Ceramics, Metals, Polymers, and Miscellaneous) Application (Prototyping, Tooling, and Functional Parts) and Regional Analysis for 2025 - 2032

Additive Manufacturing Market Share and Trends Analysis

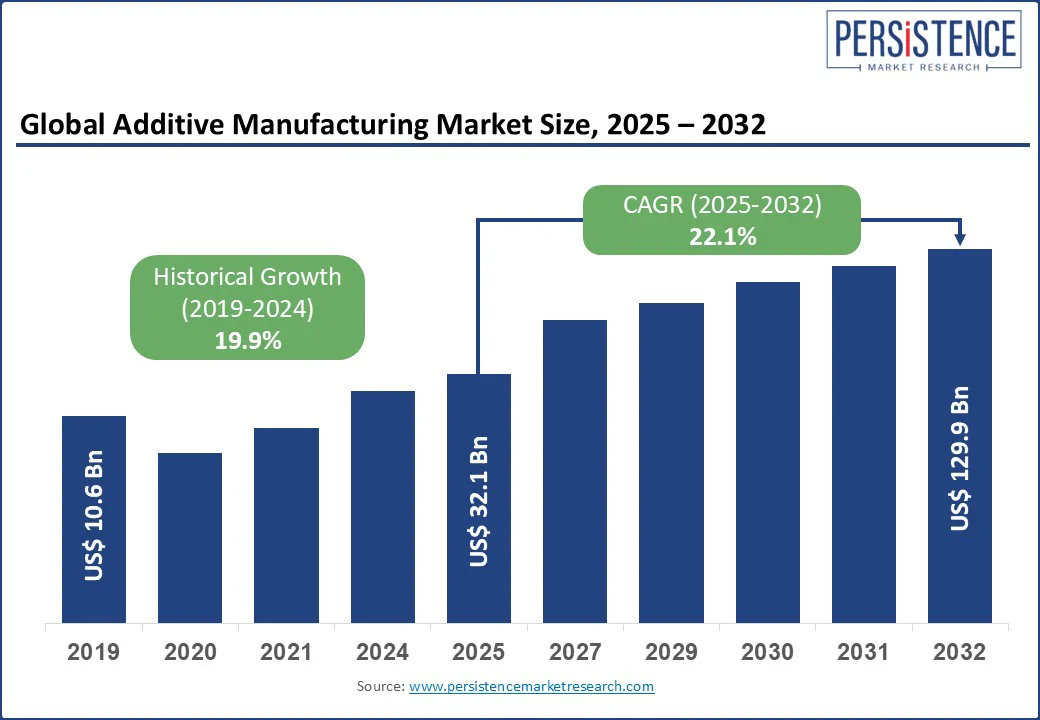

The global additive manufacturing market size is likely to value at US$32.1 Bn and is expected to reach US$ 129.9 Bn by 2032, growing at a CAGR of 22.1% by 2032. The industry has evolved from prototyping to producing functional, end-use components across aerospace, healthcare, energy, and tooling sectors. This growth is supported by rising material options, demand for lightweight parts, and high customization.

The market’s rise aligns with the increasing adoption of 3D printing systems, with global shipments surpassing 4.5 million units in 2024. Entry-level systems under $2.5k witnessed notable growth, while industrial-grade printers showed signs of saturation. Although consumer models have gained traction, industrial applications, such as those for complex aerospace and medical components, continue to drive the core value proposition.

Conceptually, 3D printing works by building layer by layer objects, contrasting with subtractive or formative techniques that cuts or mold materials. This layer-based process allows the production of geometrically intricate parts with reduced waste, optimized weight, and faster design-to-production cycles. Through technologies like SLS and binder jetting, components can now be fabricated using high-strength alloys, polymers, and reinforced composites.

Key Industry Highlights:

- Aerospace and automotive sectors drive demand for lightweight, geometrically complex 3D-printed components.

- Smart factory integration accelerates additive manufacturing’s role in digital, end-to-end production workflows.

- AI and generative design tools reshape how components are conceptualized, optimized, and customized.

- High initial costs and unclear ROI continue to limit adoption among small and mid-sized manufacturers.

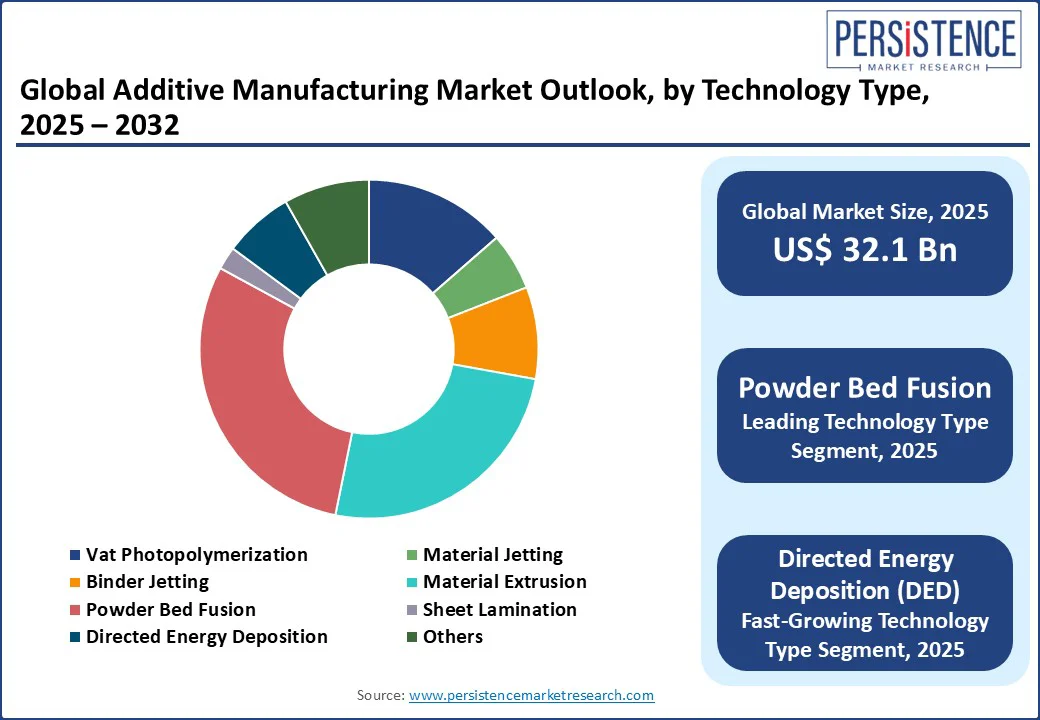

- Powder Bed Fusion leads in technology share, accounting for 29.8% of the global market due to high strength and precision.

- Prototyping dominates applications, holding a 39.8% market share by enabling faster design validation and cost savings.

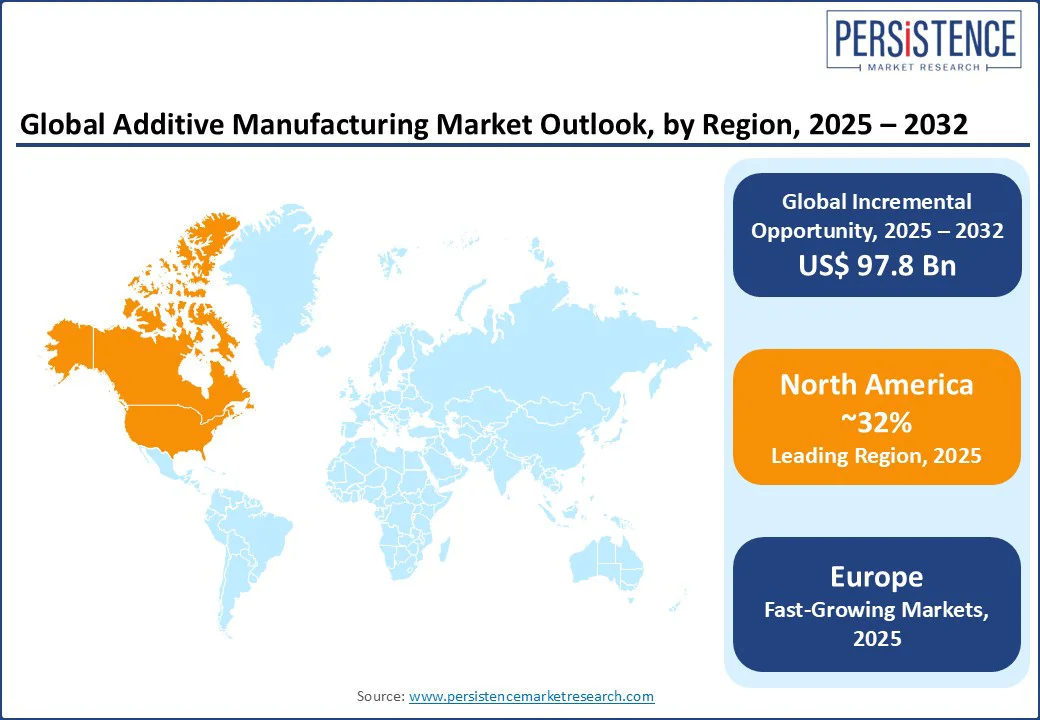

- North America commands 32.1% market share in 2025, supported by material innovation and defense-led industrial demand.

- Europe drives adoption through R&D and public-private initiatives, with Germany, Italy, and the U.K. leading usage.

- Entry-level printer shipments grow globally, especially for units priced under $2.5k, as accessibility improves.

- Industrial-grade printer deployment slows, with Q4 2024 showing a 6% dip, indicating cautious investment.

|

Global Market Attribute |

Details |

|

Additive Manufacturing (AM) Market Size (2024A) |

US$ 26.3 Bn |

|

Estimated Market Size (2025E) |

US$ 32.1 Bn |

|

Projected Market Value (2032F) |

US$ 129.9 Bn |

|

Value CAGR (2025 to 2032) |

22.1% |

|

Historical Market Growth (CAGR 2019 to 2024) |

19.9% |

Market Dynamics

Driver - Rising Demand for Lightweight and Complex Components

Aerospace and defense continue to push the boundaries of additive manufacturing by prioritizing the need for lightweight, geometrically complex components. On June 3, 2025, 3D Systems, in collaboration with NASA Glenn Research Center and two major universities, developed titanium radiators with embedded heat pipes and deployable nitinol structures. These components reduced weight by 50% while achieving a sixfold increase in the deployed-to-stowed area ratio proof of how AM enables intricate designs that traditional methods can’t deliver.

Automotive and industrial applications echo this trend. Rennscot MFG adopted the EOS M 300-4 system to build highly detailed metal parts with 10× higher productivity and 50% lower cost per part. From thermal-resistant components in 3D Systems' Figure 4 platform to the 75 AI-generated 3D-printed parts in HP’s custom-built EV, manufacturers meet performance goals without adding weight. As industries demand more efficiency, AM rises by transforming design constraints into functional, optimized outcomes.

Restraint - High Initial Setup Costs and ROI Uncertainty

Additive manufacturing requires an initial investment is required before production even begins. Metal 3D printing systems do not work alone; they need supporting equipment such as inert gas chambers, powder handling units, post-processing machines, and high-precision inspection tools. Building this complete setup costs, a lot, which makes it difficult for many manufacturers, especially mid-sized companies, to start using the technology.

Even after setting up, the path to profit is not easy. The cost of materials changes often, machines need regular maintenance, and skilled operators are expensive. These factors reduce the expected savings and make it hard for companies to recover their investment.

Some manufacturers, such as Rennscot MFG, have adopted advanced systems like the EOS M 300-4 to improve productivity and reduce part costs. Partnerships such as 3D Systems and Precision Resource also aim to integrate advanced technologies and machining systems for better efficiency. But even with these efforts, most companies still struggle to achieve a clear return on investment.

Metal additive manufacturing works best for small batches of complex parts, which limits large-scale production. This makes it harder for companies to scale up and recover costs quickly. Without a clear and predictable ROI, many businesses remain cautious about adopting this technology fully.

Opportunity - Integration into Smart Factories and Industry 4.0 Initiatives

Additive manufacturing’s compatibility with digital manufacturing ecosystems positions it at the centre of the smart factory revolution. The July 8, 2024, partnership between 3D Systems and Precision Resource integrates metal 3D printing with 5-axis machining and advanced inspection, forming a seamless, end-to-end manufacturing loop inside AS9100-certified facilities. This model enhances supply chain resilience while enabling fast turnaround for high-criticality components in aerospace and automotive.

EOS complements this trend by launching the Additive Minds Academy Center in Michigan, a 14,600 sq. ft. facility aimed at upskilling engineers to work within digital-first workflows. Its collaboration with Automation Alley and Project DIAMOnD supports the rapid scaling of distributed 3D printing networks. These developments highly include relevance for additive manufacturing; they embed it deeply into the future of industrial production, where intelligence, connectivity, and adaptability are non-negotiable.

Category-wise Analysis

Technology Insights

Powder bed fusion captures approximately 29.8% of the global market in 2025 due to its ability to produce detailed, durable parts for demanding industries. Its widespread use in aerospace, healthcare, and automotive is supported by the precision it offers and compatibility with metals and polymers. The launch of EOS NickelAlloy IN718 API and EOS Nickel NiCP showcases how this method is meeting tough requirements in oil and gas applications, where strength and corrosion resistance are essential.

This segment is gaining from strategic developments that improve material access and application variety. The acquisition of Covestro’s materials business by Stratasys added around 60 material types and significantly broadened support for Powder Bed Fusion use cases. These materials are advancing real-world adoption across healthcare, consumer products, and industrial tools. Powder Bed Fusion continues to gain preference as manufacturers focus on part quality, strength, and complex geometries that other processes struggle to match.

Application Insights

Prototyping holds the largest market share in 2025, estimated at 39.8%, driven by demand for faster design validation and shorter product cycles. Companies across sectors like automotive, aerospace, and industrial equipment are leaning on 3D technologies to cut down development time and cost. This shift is fueled by innovations like Stratasys’ F770 printer, which supports large-format prototyping with high build volume and automated workflows, helping engineers turn ideas into testable designs more quickly.

The industry is benefiting from major investments in dedicated printing centers. For instance, 3E EOS set up a facility equipped with 15 advanced Stratasys systems, cutting lead times by up to 45 days and achieving 40% cost savings. This has allowed teams in Aerospace & Defense to quickly test parts such as air ducts and fuel adapters before committing to full production, streamlining the entire product development timeline while improving sustainability through reduced waste.

Such advancements make prototyping not just a design aid but a strategic function. Companies such as ArcelorMittal are using systems like the F370 and GrabCAD software to cut part validation costs drastically from €2,000 to under €200 while gaining flexibility in design changes. These real-world benefits explain why prototyping continues to command a dominant role across industries, blending speed, accuracy, and cost-efficiency into everyday operations.

Regional Insights

North America Market Trend

North America holds an estimated 32.1% share of the global 3D printing market in 2025, backed by a strong industrial foundation and ongoing advancements in materials. A key highlight includes HP’s introduction of halogen-free PA 12 FR, developed with Evonik. The material meets UL94 V0 safety standards, offers 60% reusability, lowers ownership costs by 20%, and reduces carbon output by 10% signaling progress in both performance and environmental responsibility.

In the U.S. and Canada, adoption trends vary by user segment. Entry-level printer shipments grew during 2024, though the pace has slowed from previous years.

Industrial system deployments fell by 6% in Q4, suggesting more measured investment cycles. Despite this, the region continues to build momentum in digital manufacturing, promoting flexible, localized production with minimal waste. Sectors such as automotive, defense, and consumer products are increasingly embracing these advancements, reinforcing North America's leadership in next-generation production.

Europe Market Trend

Europe commands 27.8% of the global additive manufacturing market in 2025, underpinned by innovation-led economies and growing adoption across industrial clusters. Germany, long regarded as the continent’s engineering nucleus, maintains strong adoption at 7%, driven by industrial equipment, automotive, and aerospace prototyping. Italy and Spain, aligning near the EU average of 5%, benefit from well-established manufacturing bases but show more gradual integration of 3D technologies. The U.K., backed by an active advanced manufacturing ecosystem and focused R&D investments, sustains growth in healthcare and aerospace printing solutions.

France remain cautious in adoption, reporting 4% usage, yet push forward through targeted innovation. 3DCeram’s CERIA system, launched in May 2025, signals France’s ambition to lead in AI-driven ceramic 3D printing, especially for medical and aerospace components. Russia and Türkiye, while outside the EU metrics, reflect rising strategic interest in energy and defense segments, and Türkiye in automotive and consumer product tooling, indicating shifting priorities toward digital production. The rest of Europe, spanning the Nordics and Central Europe, contributes meaningfully through localized centers of excellence and small-scale industry digitization programs.

Competitive Landscape

The global additive manufacturing market is consolidated, led by a core group of innovation-focused companies scaling technology across materials, software, and production systems. 3D Systems is shaping full-stack industrial workflows. its works with NASA and Precision Resource boosts space and aerospace applications, while new SLA and DMP platforms expand its high-mix, low-volume production capabilities.

Stratasys focuses on polymer innovation and production efficiency, seen in its partnerships with 3E EOS and ArcelorMittal, and its acquisition of Covestro AG’s materials arm that strengthens its R&D pipeline.

GE Additive, now Colibrium Additive, pushes advancements in aerospace-grade metal printing with blue-laser technology and academic ties. EOS GmbH refines its laser powder bed systems and materials portfolio while investing in talent development through its Additive Minds Academy. HP Inc. blends AI tools and reusability-focused materials for mass customization, while Shapeways supports cost-effective sourcing through its MFG Materials platform. Each player moves with intent, focusing on production readiness, material flexibility, and sector-specific value.

Key Developments

- On June 3, 2025, 3D Systems collaborated with Penn State University, Arizona State University, and NASA Glenn Research Center to develop advanced thermal management solutions using Direct Metal Printing (DMP). The project delivered lightweight titanium and nitinol-based radiators for space, achieving a 50% weight reduction and a 6× improvement in deployed-to-stowed area ratio.

- On April 4, 2025, Stratasys Ltd. launched the Neo800+™ stereolithography printer and PolyJet ToughONE™ material at RAPID + TCT 2025. Targeting Aerospace, Automotive, and medical sectors, the launch enhances production-grade AM with better mechanical strength, thermal performance, and electrostatic discharge safety.

Companies Covered in Additive Manufacturing Market

- Stratasys Ltd.

- 3D Systems, Inc.

- GE Additive

- EOS GmbH

- HP Inc.

- Materialise NV

- Autodesk, Inc.

- EnvisionTec, Inc.

- Voxeljet AG

- ExOne

- Arcam AB

- Proto Labs, Inc.

- Canon Inc.

- Dassault Systèmes

- Optomec, Inc.

- 3DCeram

- Organovo Holdings Inc.

- Shapeways, Inc.

Frequently Asked Questions

The global Additive Manufacturing (AM) market is projected to be valued at US$ 32.1 Bn in 2025.

Powder Fusion Bed dominates the market with a 29.8% driven by its high precision, material efficiency, and suitability for complex metal part production across aerospace, automotive, and medical sectors.

The additive manufacturing (AM) market is poised to witness a CAGR 21.2% from 2025 to 2032.

Rising demand for lightweight, geometrically complex components across aerospace, automotive, and industrial sectors drives the growth of additive manufacturing.

Integration of additive manufacturing into smart factories and Industry 4.0 ecosystems offers significant opportunities for digital, connected, and scalable production.