- Plastics, Polymers & Resins

- Anti-Scratch Additives for Polypropylene Market

Anti-Scratch Additives for Polypropylene Market Size, Share, and Growth Forecast, 2026 - 2033

Anti-Scratch Additives for Polypropylene Market by Product Type (Organic Modified Siloxane, Silicon Oil, Amides, Others), End-Use Industry (Automotive, Consumer goods, Electrical & Electronics, Others), and Regional Analysis for 2026 - 2033

Anti-Scratch Additives for Polypropylene Market Share and Trends Analysis

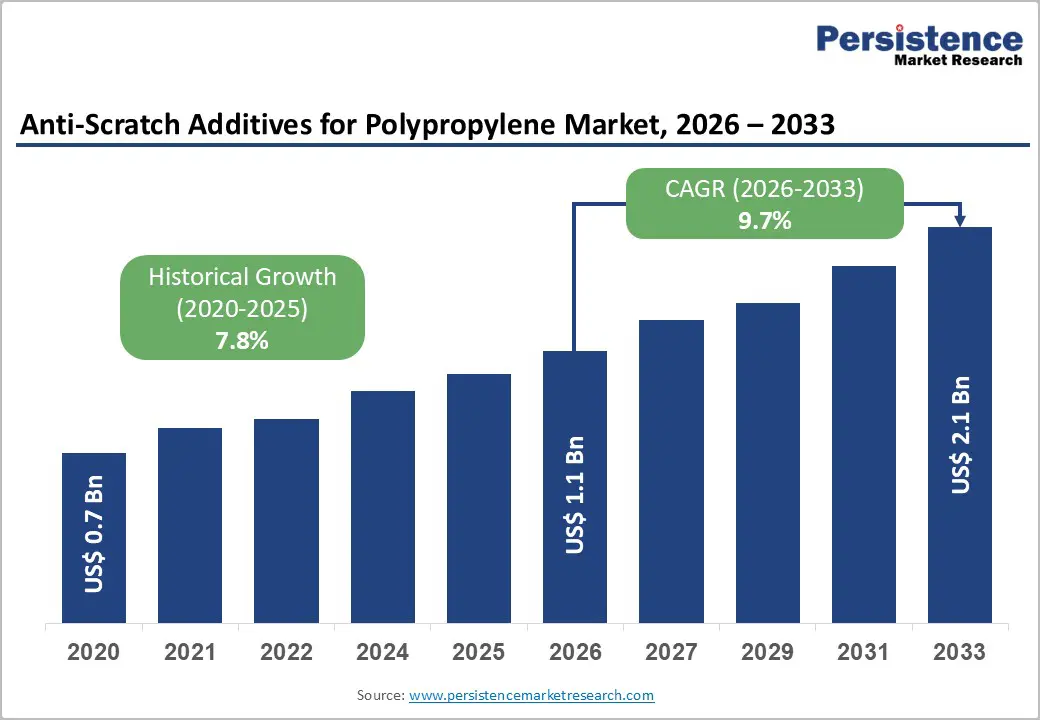

The global anti-scratch additives for polypropylene market size is likely to be valued at US$ 1.1 billion in 2026, and is projected to reach US$ 2.1 billion by 2033, growing at a CAGR of 9.7% during the forecast period of 2026–2033.

Market growth is driven by rising demand for durable, aesthetic polypropylene components in automotive interiors, consumer goods, and electrical applications. Regulatory pressure to extend product lifecycles, combined with original equipment manufacturer (OEM) preference for lightweight polymers over metals, continues to accelerate adoption. Advancements in organic modified siloxane formulations and increasing polypropylene usage in the Asia Pacific further strengthen long-term market expansion.

Key Industry Highlights

- Dominant Additive Types: Organic modified siloxanes are expected to account for 42% of market revenue in 2026 due to their superior durability and polypropylene compatibility

- Fastest-growing Additive Types: Amide additives are projected to grow the fastest, at a 10% CAGR through 2033, driven by cost efficiency and broader adoption across consumer goods.

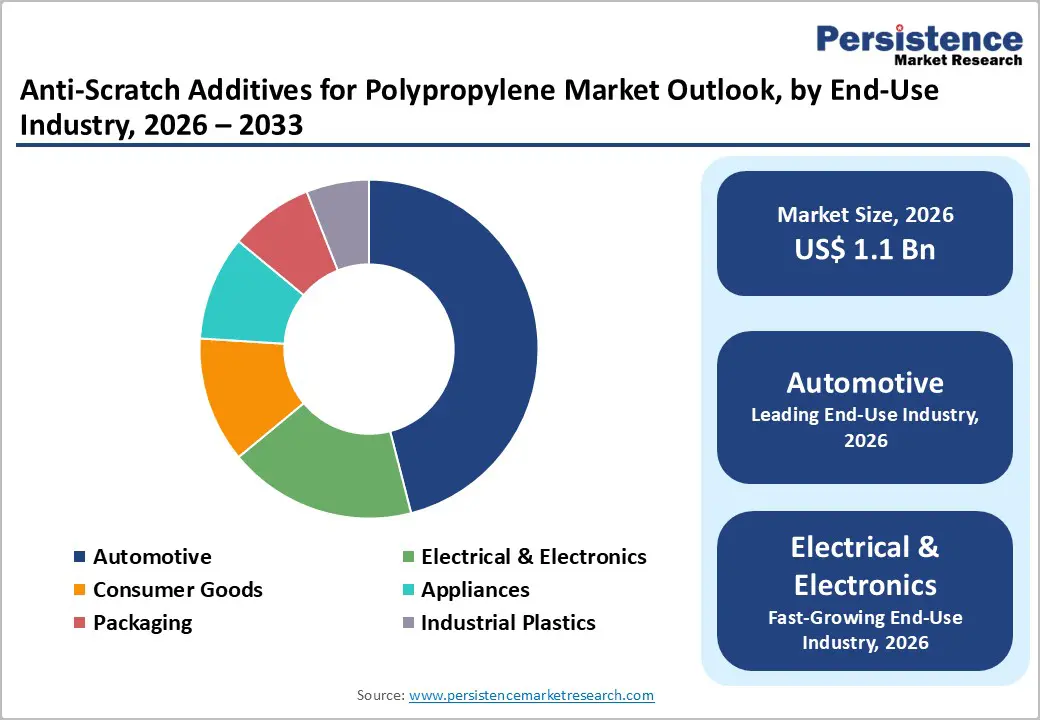

- Leading End-Use Industry: The automotive sector is projected to dominate with about 46% revenue share in 2026, supported by rising polypropylene usage in interior components.

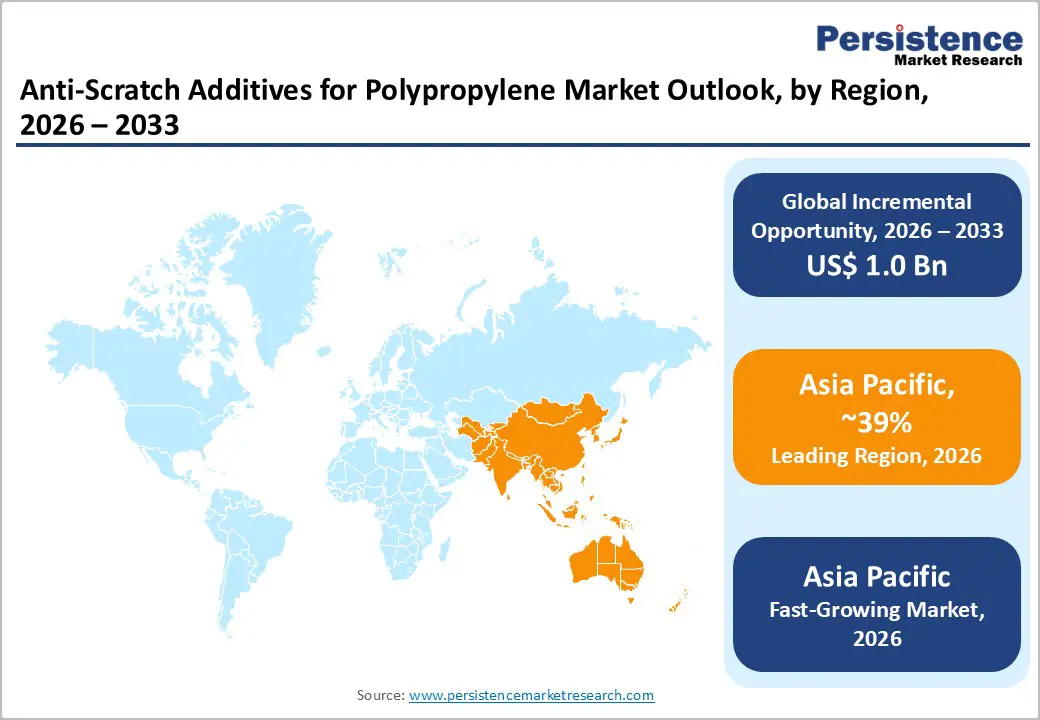

- Regional Leadership: Asia Pacific is poised to lead with over 38% market share in 2026 and remain the fastest-growing market through 2033, fueled by large-scale automotive manufacturing and expanding consumer goods markets.

- Key Drivers: Interior quality requirements for electric vehicles (EVs) and tightening emissions regulations are accelerating innovation in low-migration, high-performance, and REACH-compliant anti-scratch additive formulations.

- Competitive Dynamics: The market is shaped by formulation upgrades, capacity expansions, and strategic OEM-compounder partnerships, with leading players prioritizing automotive interior applications.

| Key Insights | Details |

|---|---|

|

Anti-Scratch Additives for Polypropylene Market Size (2026E) |

US$ 1.1 Bn |

|

Market Value Forecast (2033F) |

US$ 2.1 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

9.7% |

|

Historical Market Growth (CAGR 2020 to 2025) |

7.8% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Automotive Demand for Lightweight, Durable, and High-Quality Polypropylene Applications

Automotive lightweighting mandates and interior durability requirements have made polypropylene a core material for modern vehicle interiors, directly driving demand for anti-scratch additives. Regulatory frameworks such as fleet-level CO-emission limits in Europe, fuel-efficiency standards in North America, and vehicle weight reduction targets in major Asian markets have accelerated the substitution of heavier materials with polypropylene in dashboards, door trims, and center consoles. These components are subject to standardized OEM abrasion and scratch tests during material qualification, where visible surface degradation is not acceptable over long service lifecycles. Anti-scratch additives enable polypropylene to meet these performance thresholds without increasing part thickness or compromising weight targets.

This driver is reinforced by the growth of electric and premium vehicles, where interior quality is critical to customer perception, given reduced engine noise and longer ownership cycles. Automakers increasingly rely on polypropylene-based interior systems that maintain appearance under repeated contact, cleaning, and thermal cycling. To control warranty exposure related to cosmetic wear, Tier-1 suppliers integrate scratch-resistant additives at the compounding stage rather than applying secondary coatings. As interior durability has shifted from a design preference to a material qualification requirement, the adoption of anti-scratch additives in automotive polypropylene applications continues to expand.

Cost Pressure and Regulatory Compliance Risks in Specialty Additive Supply Chains

The adoption of anti-scratch additives for polypropylene is constrained by volatile pricing of silicone derivatives and specialty amides, which are highly sensitive to energy costs and upstream raw material availability. During 2025, restrictions on silicon metal exports from China, the world’s largest producer, tightened global supply and increased input costs for silicone-based additives. This directly affected compounders dependent on imported feedstocks, particularly in Asia and Europe. For small and mid-sized manufacturers, sudden cost escalations reduced margin visibility. They made it difficult to pass increases downstream, limiting adoption in price-sensitive consumer goods and mass-market applications.

Regulatory compliance requirements further compound these cost pressures by increasing development complexity and time-to-market. The updates under the Registration, Evaluation, Authorisation and Restriction of Chemicals (REACH) framework of the European Union (EU) deepened the scrutiny on additive migration and long-term environmental persistence, requiring additional testing for certain silicone oils and amide-based formulations used in polymers. These requirements increased the need for toxicological assessments and reformulation efforts, extending product approval timelines and raising compliance costs. Thus, new product launches slowed, and entry barriers increased, particularly for smaller players with limited regulatory resources, constraining near-term market expansion despite underlying demand growth.

Rising Demand for Sustainable Polypropylene Solutions for EVs

The convergence of electric mobility, smart interior design, and expanding consumer markets is creating significant growth opportunities for anti-scratch additives in polypropylene. As engine noise decreases in electric vehicles, surface imperfections become more noticeable, making scratch resistance a critical quality parameter. This trend is reflected in recent EV models, where automakers have updated interior material specifications to enhance abrasion and scratch resistance in dashboards and door trims. Polypropylene, with its lightweight and cost benefits, is increasingly used in these applications, driving the adoption of additives that ensure durability in soft-touch and matte finishes. This evolution supports higher penetration of advanced additive solutions across both premium and mainstream electric vehicles.

The industrialization and rising disposable incomes in the Asia Pacific are boosting demand for durable consumer goods with improved aesthetics. Policies such as India’s Production Linked Incentive (PLI) program for specialty polymers encourage local manufacturing of high-performance polypropylene compounds, including scratch-resistant formulations. Regional initiatives in China and Southeast Asia similarly support domestic additive production, helping manufacturers meet rising demand for long-lasting, visually resilient products. Combined with growing regulatory and consumer focus on sustainability and low-migration materials, these trends offer a substantial multi-regional opportunity for advanced anti-scratch additives in polypropylene applications.

Category-wise Analysis

Product Type Insights

Organic-modified siloxanes are expected to account for approximately 42% of market revenue in 2026, making them the leading additive due to their superior compatibility with polypropylene and long-lasting surface performance. These additives enhance scratch and mar resistance in high-touch surfaces without affecting gloss or texture, critical for automotive interiors and premium consumer goods. In 2025, silicone-based masterbatches meeting VW PV3952 and GM GMW14688 standards demonstrated high durability in dashboards and door trims, reinforcing adoption of siloxanes. Established supply networks in Europe and North America support consistent quality and wide adoption. These additives remain the preferred choice where visual quality and longevity are key, particularly in applications requiring premium finishes.

Amide-based additives are projected to grow at a CAGR of about 10% from 2026 to 2033, driven by cost-effectiveness and suitability for high-volume applications. Their balanced slip-scratch performance makes them ideal for consumer goods and appliance housings where durability must align with price constraints. In 2025, amide-integrated polypropylene compounds demonstrated improved abrasion resistance in medium-duty plastics for appliance panels and storage shells, meeting rising expectations in the Asia Pacific. Expanding polymer compounding hubs in Southeast Asia enable localized production and faster adoption. The combination of affordability, performance, and accessibility positions amides as the fastest-growing additive segment.

End-Use Industry Insights

Automotive applications are likely to account for 46% of the anti-scratch additives for polypropylene in 2026, making the sector the largest end-user. Polypropylene is widely used in dashboards, door trims, center consoles, and instrument panels to reduce weight while maintaining aesthetics. The transparent polypropylene granules combined with silicone masterbatch systems passed high-end interior durability tests, showing enhanced surface hardness and scratch resistance. Germany, Japan, and the U.S. lead consumption due to mature automotive manufacturing and strict OEM quality protocols. EV interior standard updates and premiumization trends further drive additive integration. These factors reinforce the automotive segment’s market share leadership.

The electrical & electronics segment is projected to grow at a CAGR of roughly 11% due to the rising use of polypropylene in casings for consumer electronics and smart appliances. The EU Ecodesign Directive introduced minimum durability criteria for electronics housings, including scratch and abrasion resistance, prompting OEMs to specify polypropylene compounds with integrated anti-scratch additives. Lightweight, cost-effective, and design-flexible polypropylene is well-suited for these applications. High demand is concentrated in East Asia and North America, where electronics manufacturing is strong. Enhanced additive adoption is becoming a key differentiator for product longevity and consumer satisfaction.

Regional Market Insights

North America Anti-Scratch Additives for Polypropylene Market Trends

North America has been experiencing robust demand for anti-scratch additives, primarily fueled by the automotive and consumer goods industries within the United States. The automotive sector has been accelerating the adoption of these additives in polypropylene compounds for lightweight, durable interior components such as dashboards and door trims, supported by incentives under the Inflation Reduction Act that promote electric vehicle production and domestic manufacturing of advanced materials. Consumer appliances and smart devices have been incorporating higher volumes of polypropylene to satisfy expectations for enhanced surface resilience. Reshoring initiatives for plastics compounding and advanced recycling facilities in regions such as Texas and Ontario have been fortifying supply chain reliability while drawing substantial capital investments.

Regulatory frameworks have been favoring low-migration additives that align with stringent environmental and safety standards, particularly in applications demanding both durability and compliance. OEMs) and additive suppliers have been deepening collaborations to benchmark material performance across interior and exterior components. While expansion rates trail those in Asia Pacific, North America's emphasis on premium automotive interiors, electronics integration, and innovation ecosystems has been sustaining market leadership. Stakeholders prioritizing compliant formulations and regional production capabilities will have captured disproportionate value as electrification and sustainability imperatives reshape material specifications.

Europe Anti-Scratch Additives for Polypropylene Market Trends

The European anti-scratch additives for polypropylene market growth prospects have been strengthening across Germany, France, and the United Kingdom, with automotive programs and premium consumer goods driving most volumes. Harmonized REACH requirements have been steering formulators toward compliant, low-risk chemistries for applications with strict safety and environmental thresholds. In 2025, the European Parliament adopted circular economy rules that require minimum recycled plastic content in vehicle parts and stronger material traceability, pushing OEMs to refine polypropylene compounds and additive packages to protect surfaces while meeting sustainability targets. These shifts have accelerated the integration of anti-scratch solutions into interior modules and consumer products, where durability and compliance must move in tandem.

Automotive interior upgrades have continued to support steady expansion, and German manufacturers have prioritized recyclability and long service life as key design criteria. EU funding programs have supported sustainable materials and bio-based additive innovation, thereby improving the long-term differentiation potential for suppliers that can validate performance in recycled PP streams. France and the UK have been advancing partnerships to scale high-performance formulations that align with circularity expectations, while also tightening supplier qualification around documentation and traceability readiness. To win share in this environment, additive suppliers have benefited most when they pair regulatory readiness with application engineering, and they will further strengthen their competitiveness by building OEM-aligned test protocols and recycling-compatible performance claims.

Asia Pacific Anti-Scratch Additives for Polypropylene Market Trends

Asia Pacific is expected to dominate in 2026, with around 39% of the anti-scratch additives for polypropylene market share, and is also projected to be the fastest-growing market through 2033, driven by expansive automotive production, electronics manufacturing, and consumer goods demand. China alone accounts for nearly 45% of regional demand due to its scale in automotive and appliance production. Government policies aligned with broader industrial modernization, including plastics manufacturing strategies that emphasize domestic value addition and improved recycling systems, are reinforcing substrate growth. National targets to reduce plastic leakage and enhance recycling infrastructure across Southeast Asia improve material circularity and support additive adoption. Furthermore, regional workshops under the Asia-Pacific Economic Cooperation (APEC) forum have fostered collaboration on plastic recycling technologies and policy frameworks, enhancing technical capacity and cross-border cooperation.

Rising middle-class consumption in India, ASEAN, and Japan underpins demand for durable polypropylene products requiring scratch resistance. India’s “Make in India” push for specialty materials, coupled with the expansion of compounding hubs in Indonesia and Vietnam, strengthens local manufacturing capabilities and attracts global additive suppliers. China’s efforts to scale production of high-performance materials for automotive interiors, appliances, and electronics further bolster market momentum. With high economic growth, expanding manufacturing bases, and supportive policy ecosystems, the Asia Pacific is projected to maintain the fastest regional growth trajectory, making it a strategic priority for market expansion and innovation investment.

Competitive Landscape

The global anti-scratch additives for polypropylene market structure is moderately consolidated, with leading vendors, including Wacker Chemie AG, Evonik Industries, Dow Chemical, and Momentive, together accounting for a significant share of the market. These established players leverage long-standing relationships with automotive OEMs, appliance manufacturers, and polymer compounders, alongside regulatory expertise and technical support for low-migration, compliant formulations. They invest heavily in R&D to develop next-generation additives with improved scratch resistance, thermal stability, and compatibility with recycled polypropylene.

Regional and niche competitors, such as Siltech Corporation and Zhejiang Xinhui Chemical, are focusing on specialized segments like mid-tier consumer appliances and electronics housings or targeting emerging markets in Asia Pacific. Barriers such as raw material volatility, regulatory compliance, and complex compounding requirements limit new entrants. However, growing demand for high-performance, sustainable polypropylene applications and innovation in bio-based or low-migration additives is enabling smaller companies to capture specialized opportunities and differentiate through product performance and local manufacturing capabilities.

Key Industry Developments

- In November 2025, Clariant completed a CHF 100 million expansion at its Daya Bay facility in China, bringing a second production line fully online. The expansion increased capacity for halogen-free flame retardants and durable polymer additives used in e-mobility and electrical & electronics applications. This investment strengthens Clariant’s Asian supply chain, supports growing EV component demand, and reduces reliance on volatile antimony-based materials, reinforcing its position in sustainable, high-performance polymer solutions.

- In June 2025, Xiamen Xiangxi New Material Co., Ltd. announced a long-term R&D program (2025–2028) focused on next-generation silicone masterbatches for automotive and high-end industrial polypropylene applications. Earlier, in April 2025, the company showcased its enhanced anti-scratch agents at CHINAPLAS 2025, demonstrating scratch resistance improvements from ~50% to up to 90% in automotive interiors. The material system also achieves ultra-low formaldehyde emissions (<50 μg/g), aligning with updated environmental standards and increasing adoption in performance-driven PP applications.

Companies Covered in Anti-Scratch Additives for Polypropylene Market

- BASF SE

- Dow Inc.

- Evonik Industries

- Momentive Performance Materials

- Wacker Chemie AG

- Shin-Etsu Chemical

- BYK-Chemie

- Clariant AG

- Croda International

- Arkema

- Solvay SA

- Adeka Corporation

Frequently Asked Questions

The global anti-scratch additives for polypropylene market is projected to reach US$ 1.1 billion in 2026.

Key growth drivers include the increasing use of polypropylene in high-touch applications, rising durability and aesthetic expectations, lightweight material adoption in automotive and electronics, and growing focus on surface longevity and reduced warranty claims.

The market is poised to witness a CAGR of 9.7% from 2026 to 2033.

Major opportunities lie in electric vehicles, smart appliances, and premium consumer products, along with the development of low-migration, sustainable, and high-performance additive solutions.

Leading companies include Clariant, BYK (ALTANA Group), Evonik Industries, Dow, Ampacet, BASF, and Xiamen Xiangxi New Material, among others.