- Plastics, Polymers & Resins

- Additive Masterbatch Market

Additive Masterbatch Market Size, Trends, Share, and Growth Forecast 2026 - 2033

Additive Masterbatch Market by Additive Type (Antioxidant Masterbatch, Flame Retardant Masterbatch, Antimicrobial Masterbatch, UV Stabilizer Masterbatch, Foaming / Blowing Agent Masterbatch, Optical Brightener & Nucleating Agent Masterbatch, Other), End-user (Residential, Commercial, Institutional, Industrial), and Regional Analysis, 2026 - 2033

Additive Masterbatch Market Size and Trend Analysis

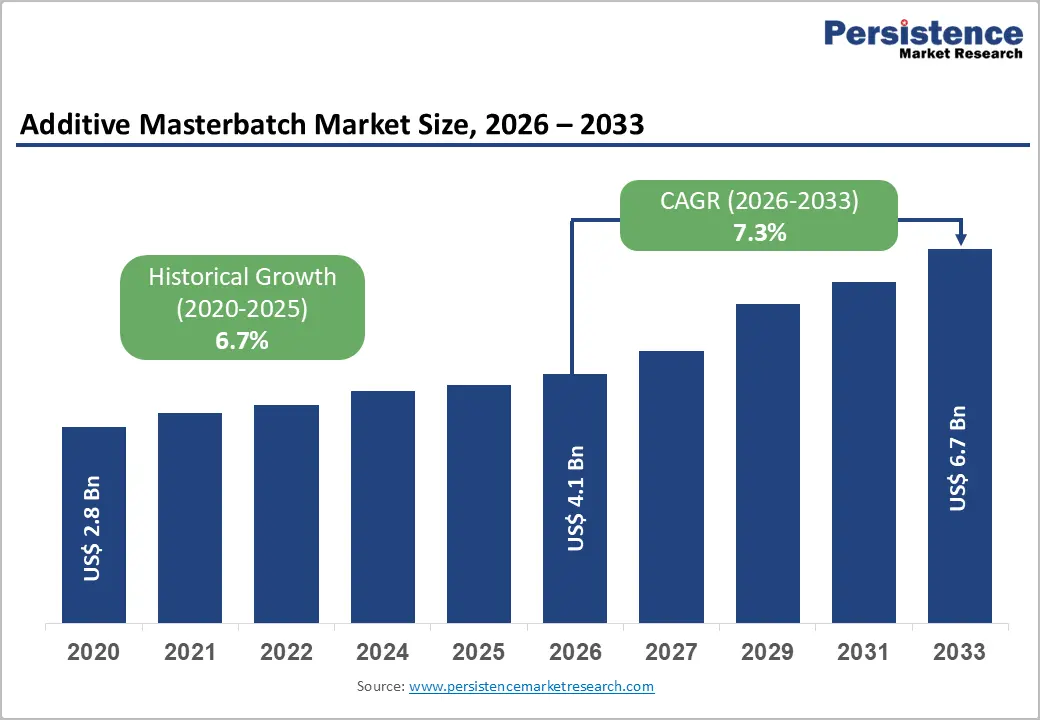

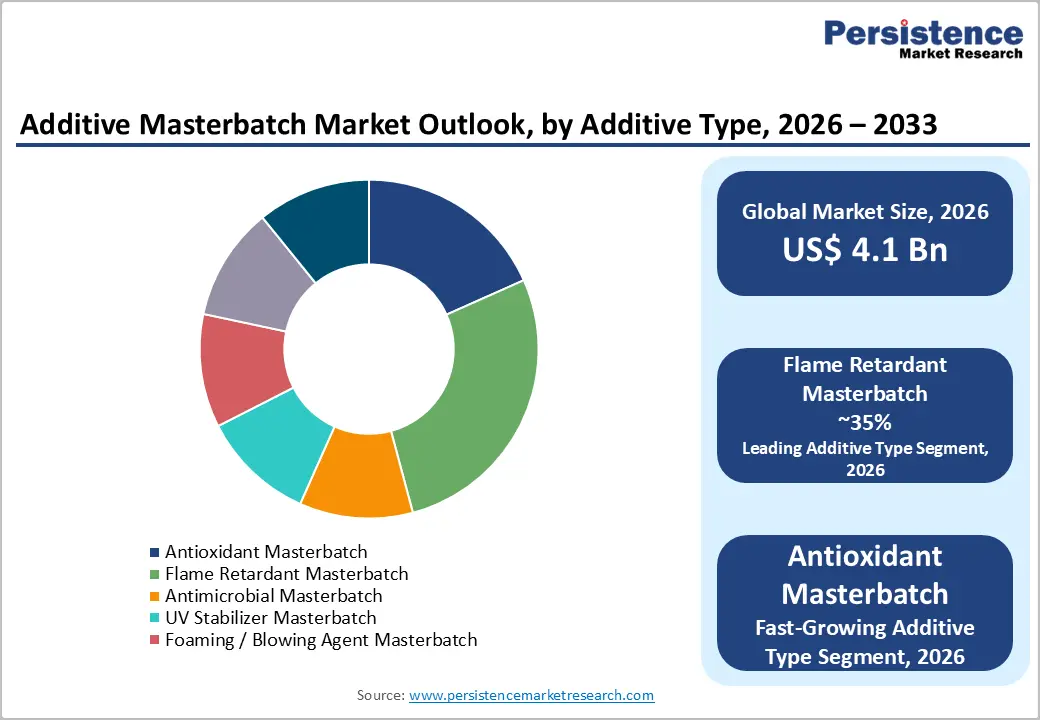

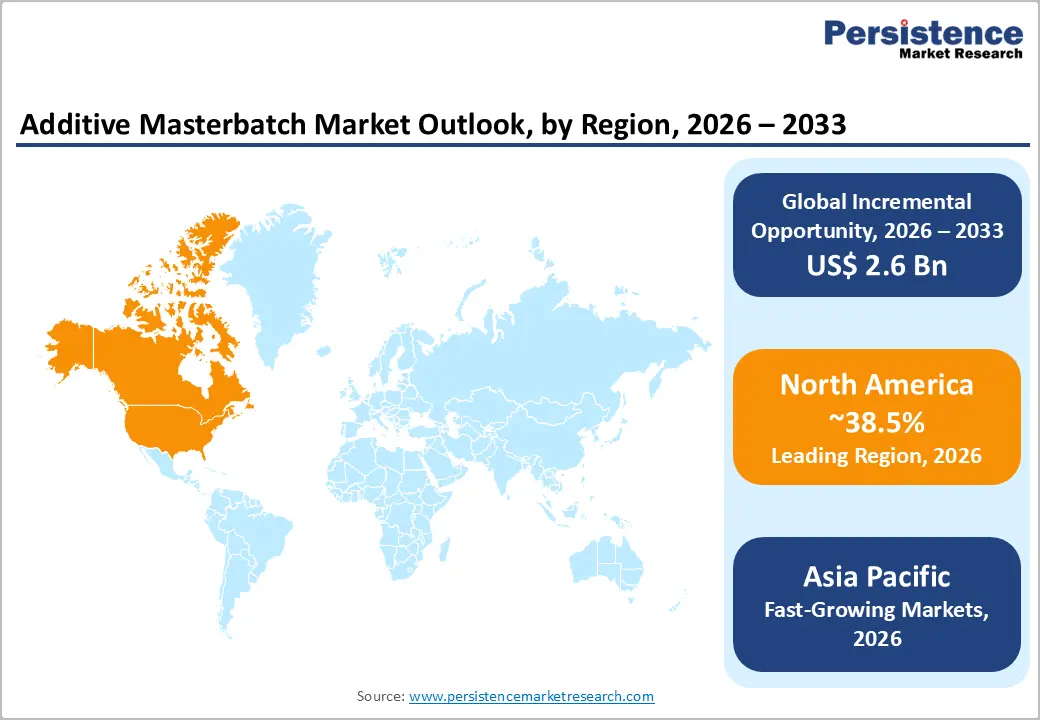

The global additive masterbatch market size is expected to be valued at US$ 4.1 billion in 2026 and projected to reach US$ 6.7 billion by 2033, growing at a CAGR of 7.3% between 2026 and 2033.

The market is driven by rising demand for high-performance plastics across packaging, automotive, and construction sectors, propelled by urbanization and the trend toward lightweight, durable materials. The increasing global plastic production, which reached 400 million tons in 2024, underscores the growing demand for additives that enhance durability, processability, and sustainability. Regulatory mandates for flame retardancy and UV stability further support market expansion worldwide.

Key Industry Highlights:

- Leading Region: Asia Pacific commands 38.5% share in 2025, driven by manufacturing hubs in China and India, boosting plastics demand.

- Fastest-Growing Region: Asia Pacific is the fastest-growing market, supported by low labor costs, urbanization, and infrastructure expansion.

- Leading Additive Type: Flame retardant masterbatch dominates with 35% share in 2025, crucial for safety in construction and electronics.

- Fastest-Growing Additive Type: Multi-functional and antimicrobial masterbatches are emerging as the fastest-growing category, meeting hygiene and high-performance demands.

- Key Opportunity: Sustainable, bio-based masterbatches offer growth potential amid circular-economy initiatives and EU recycling targets for 2030.

| Global Market Attribute | Key Insights |

|---|---|

| Additive Masterbatch Size (2026E) | US$ 4.1 billion |

| Market Value Forecast (2033F) | US$ 6.7 billion |

| Projected Growth CAGR (2026 - 2033) | 7.3% |

| Historical Market Growth (2020 - 2025) | 6.7% |

Market Dynamics

Drivers - Rising Demand for Additive Masterbatches Driven by Packaging Industry Growth and Sustainability Needs

The rapid expansion of the global packaging industry significantly drives the additive masterbatch market, as functional additives such as antimicrobials, UV stabilizers, and antioxidants help extend product shelf life while ensuring compliance with hygiene and safety standards. With plastics accounting for approximately 40% of packaging materials and global demand projected to grow at 4.5% annually through 2025, masterbatches enable tailored solutions for food and consumer goods, enhancing barrier properties and reducing material waste.

E-commerce growth further increases the need for durable and lightweight packaging, while stringent regulations such as EU Food Contact Materials push manufacturers to adopt high-performance additives. This integration ensures compliance, product protection, and improved shelf life, positioning additive masterbatches as a crucial component in modern packaging solutions.

Accelerating Adoption of Additive Masterbatches Due to Automotive Lightweighting and Safety Compliance Initiatives

The automotive sector’s focus on lightweighting and electrification drives the demand for additive masterbatches that enhance plastics with flame retardancy, strength, and durability. Vehicle production reached 90 million units in 2025, with plastics increasingly replacing metals to reduce vehicle weight and improve fuel efficiency by up to 10%, according to OICA data.

Additives in masterbatches also ensure adherence to critical safety standards, such as FMVSS, enabling the manufacture of complex interior and exterior components. As automakers pursue sustainable, energy-efficient designs, additive masterbatches become essential for achieving both performance and regulatory compliance in modern vehicles, supporting long-term market growth.

Restraints - Profitability Challenges Due to Fluctuating Raw Material Prices in the Additive Masterbatch Market

The additive masterbatch industry faces significant challenges from volatile prices of polymers and specialty additives, which directly impact production costs and profitability. In 2024, resin prices surged by 15-20% due to supply chain disruptions, geopolitical tensions, and fluctuations in petrochemical feedstock availability, according to industry reports. Manufacturers heavily reliant on polyethylene carriers are particularly affected, as rising costs squeeze margins and reduce operational flexibility.

Global supply chain dependencies further exacerbate price volatility, making procurement unpredictable and hindering the ability to scale production efficiently. In price-sensitive markets, sudden cost increases may limit adoption, delay orders, or force manufacturers to pass costs onto customers, affecting competitiveness. Such instability remains a key restraint on market expansion in both developed and emerging regions.

Adoption Limitations Imposed by Stringent Environmental and Regulatory Compliance Requirements

Stringent environmental regulations, particularly concerning halogenated flame retardants, pose a significant restraint on the additive masterbatch market. The EU REACH framework has restricted over 20 halogen-based compounds since 2023, forcing manufacturers to transition toward non-halogenated alternatives. This shift increases production costs by 10-15% and demands extensive R&D to maintain performance standards, particularly for electronics, automotive, and construction applications.

Smaller players face heightened compliance burdens, including testing, documentation, and certification requirements, which may restrict their ability to compete. These regulatory pressures can slow market adoption, drive consolidation among manufacturers, and increase reliance on technologically advanced firms capable of developing sustainable and compliant formulations, limiting flexibility in certain regional markets.

Opportunity - Expanding Opportunities Through Bio-Based and Sustainable Additive Masterbatch Formulations

The rising emphasis on sustainability and circular economy initiatives presents significant growth opportunities for bio-based additive masterbatches. With the EU targeting 25% recycled plastics by 2030, manufacturers are increasingly developing plant-derived antioxidants and biodegradable additives that improve environmental performance while maintaining functionality. Studies indicate that these bio-based solutions can enhance degradability by up to 20%, supporting regulatory compliance and eco-conscious product positioning.

The post-pandemic surge in hygiene awareness has accelerated demand for antimicrobial masterbatches, particularly in packaging applications. Asia Pacific leads investments in this segment, reflecting both rapid urbanization and growing consumer preference for safe, sustainable products. These trends position bio-based and sustainable masterbatches as a key driver for long-term market expansion and innovation.

Growth Potential Driven by Advancements in Multi-Functional Additive Masterbatches

Multi-functional masterbatches, which integrate properties such as UV stabilization, flame retardancy, and foaming capabilities, are gaining traction across industrial applications. China’s manufacturing expansion, responsible for nearly 30% of global plastics output, along with initiatives like Made in China 2025, fuels the development and adoption of these innovative solutions.

By combining multiple functionalities in a single masterbatch, processing steps can be reduced by up to 15%, delivering cost savings and efficiency gains. High-volume sectors such as construction, automotive, and packaging benefit from simplified manufacturing workflows, making multi-functional masterbatches a strategic opportunity for producers targeting industrial-scale applications.

Category-wise Analysis

Additive Type Insights

Flame retardant masterbatches led the market in 2025 with a 35% share, driven by stringent safety regulations in electronics, construction, and automotive sectors. UL 94 compliance mandates their use in approximately 70% of wire cables, where additives like antimony trioxide suppress fire through gas-phase radical trapping. Extensive application in polyolefins for automotive interiors and exteriors further reinforces their leading position in the additive type segment.

Alongside flame retardants, multi-functional and non-halogenated additive masterbatches are emerging as the fastest-growing category. These combine properties such as UV stabilization, antimicrobial activity, and processing aids, catering to industrial and consumer demands for high-performance, sustainable, and versatile plastics. Their adoption is accelerating in sectors seeking cost-efficient, all-in-one solutions for complex polymer applications.

End-user Insights

The industrial segment held a commanding 45% market share in 2025, primarily driven by construction and automotive demands for durable, high-performance plastics. Global infrastructure projects consumed over 200 million tons of plastics in 2025, with additive masterbatches enhancing thermal stability, flame resistance, and processability. Manufacturing hubs heavily rely on these solutions to meet quality and safety standards, reinforcing the industrial segment’s leadership in end-use adoption.

The fastest-growing end-use areas include consumer goods, healthcare, and packaging sectors, where hygiene, aesthetics, and sustainability are becoming critical. Additive masterbatches in these applications enhance barrier properties, antimicrobial protection, and UV resistance, meeting evolving regulatory and market expectations while supporting innovation in emerging industrial and commercial products.

Regional Insights

North America Additive Masterbatch Market Trends and Insights

North America holds a significant ~34.1% share of the global additive masterbatch market in 2025, led by the U.S., which benefits from a robust innovation ecosystem. Stringent EPA regulations mandate flame retardants in construction plastics, while automotive lightweighting initiatives, aligned with NHTSA standards, drive growth in specialty additives. Product innovations like Avient’s non-PFAS mold releases enhance high-temperature polymer performance.

The medical packaging segment is also expanding, with antimicrobial masterbatches aligning with FDA guidelines amid increasing healthcare plastics use. Combined regulatory support, technological innovation, and adoption of sustainable, high-performance additives reinforce North America’s leadership position and steady market expansion.

Europe Additive Masterbatch Market Trends and Insights

Europe’s additive masterbatch market is expected to grow at a CAGR of ~4.5% between 2026 and 2033. Germany leads in automotive applications, benefiting from REACH harmonization and reduced halogen usage, while the U.K. and France focus on sustainable packaging driven by the EU Circular Economy initiatives. Spain’s construction sector further boosts demand for UV-stabilized plastics.

Innovation and regulatory alignment encourage cross-border trade, exemplified by patents such as Clariant’s oxygen scavenger for PET. Technological advancements, combined with stringent safety and sustainability standards, ensure Europe maintains steady growth and a competitive position in the global market.

Asia Pacific Additive Masterbatch Market Trends and Insights

Asia Pacific commands the largest regional share at 38.5% of the global market in 2025, driven by China’s manufacturing scale and India’s urbanization-led growth. ASEAN countries benefit from foreign investment in electronics manufacturing, while Japan’s green technology initiatives support high-performance and sustainable masterbatches.

Low labor costs and efficient production infrastructure enhance regional competitiveness, making the Asia Pacific the fastest-growing additive masterbatch market. Rising industrial demand, supportive policies, and technological adoption continue to attract investment, reinforcing the region’s dominant role in global production and innovation.

Competitive Landscape

The global additive masterbatch market is moderately consolidated, with leading players collectively holding a dominating market share. Companies focus on strengthening their position through extensive R&D, acquisitions, and strategic partnerships, aiming to enhance product portfolios and address evolving industry demands. Emphasis on sustainable and high-performance formulations allows differentiation in a competitive environment.

Emerging strategies include the development of multi-functional additives that combine properties such as flame retardancy, UV stabilization, and antimicrobial performance. Additionally, adoption of digital dosing and precision manufacturing systems enhances process efficiency, reduces waste, and supports high-quality, cost-effective production, giving companies a competitive edge in key regional markets.

Key Developments

- In July 2024, Avient Corporation introduced a non-PFAS mold release additive for high-temperature polymers, enhancing injection molding efficiency, improving product quality, and reducing cycle times, supporting high-performance applications in automotive, packaging, and industrial plastics.

- In October 2023, Clariant AG patented the Cesa ProTect oxygen scavenger masterbatch for PET packaging, expanding its portfolio of active solutions, improving shelf life of packaged goods, and strengthening its presence in sustainable and high-performance food and beverage packaging applications.

- In October 2025, Ampacet Corporation acquired Liad, a specialist in weighing and dosing systems, entering auxiliary equipment markets to enhance dosing precision, improve manufacturing efficiency, and support consistent quality in additive and color masterbatch production processes.

Companies Covered in Additive Masterbatch Market

- Avient Corporation

- Ampacet Corporation

- Clariant AG

- LyondellBasell Industries

- Dow

- RTP Company

- Tosaf Compounds Ltd.

- Americhem, Inc.

- Cabot Corporation

- Plastiblends India Ltd.

- Plastika Kritis S.A.

- Gabriel-Chemie Group

- Dainichiseika Color & Chemicals Mfg. Co., Ltd.

- Hubron International

- Alok Masterbatches Pvt. Ltd.

Frequently Asked Questions

The additive masterbatch market is expected to reach US$ 4.1 billion in 2026, driven by packaging and automotive demands.

Rising packaging sector needs for antimicrobials, UV stabilizers, and flame retardants, with plastics demand growing globally.

Asia Pacific with 38.5% share in 2025, led by manufacturing hubs in China and India.

Sustainable bio-based formulations supporting circular economy initiatives and EU recycling targets by 2030.

Leading firms include Avient Corporation, Ampacet Corporation, Clariant AG, LyondellBasell Industries, and Dow, focusing on innovations.