- Clothing, Footwear, & Accessories

- Women Luxury Footwear Market

Women Luxury Footwear Market Size, Share, and Growth Forecast 2026 - 2033

Women Luxury Footwear Market by Product Type (Boots, Heels & Pumps, Sandals & Flats, Sneakers & Sports Shoes), Material Type (Rubber, Leather, Polyester, Velvet, Canvas, Textile, Others), and Regional Analysis, 2026 - 2033

Women Luxury Footwear Market Size and Trend Analysis

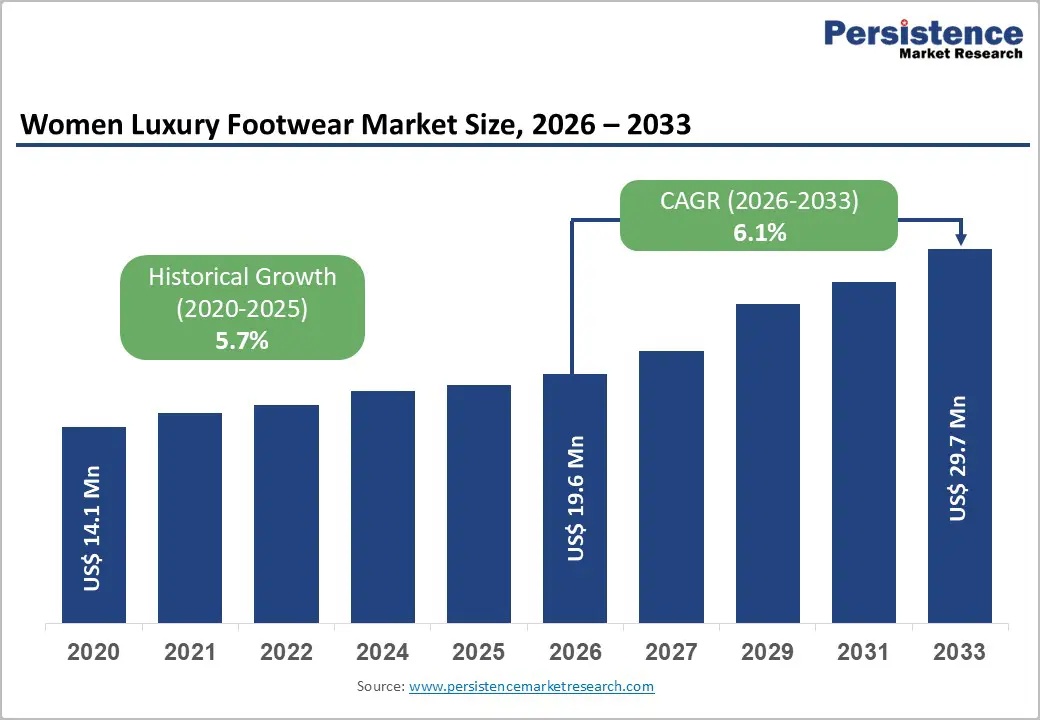

The global women luxury footwear market size is expected to be valued at US$ 19.6 million in 2026 and projected to reach US$ 29.7 million by 2033, growing at a CAGR of 6.1% between 2026 and 2033.

Rising disposable incomes among affluent women worldwide are driving increased spending on premium footwear, with emerging markets showing strong growth as middle-class populations expand. Fashion trends favor versatile luxury items like stylish sneakers and flats, blending comfort with elegance. The rise of e-commerce enables brands to connect with global consumers, offering exclusive online releases that enhance accessibility and boost overall market demand.

Key Industry Highlights:

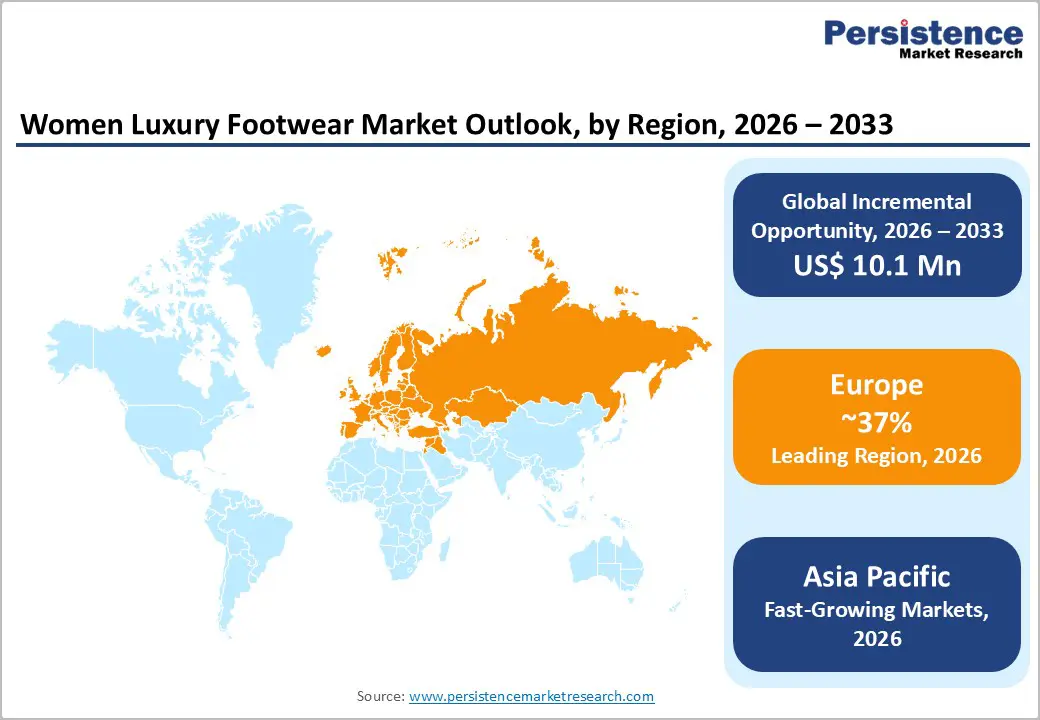

- Leading Region: Europe leads the Women's Luxury Footwear market with a 37% share in 2025, supported by artisanal heritage and affluent consumer demand.

- Fastest-Growing Region: Asia Pacific is the fastest-growing region with a 31% share in 2025, driven by urbanization, rising middle-class income, and expanding luxury consumption.

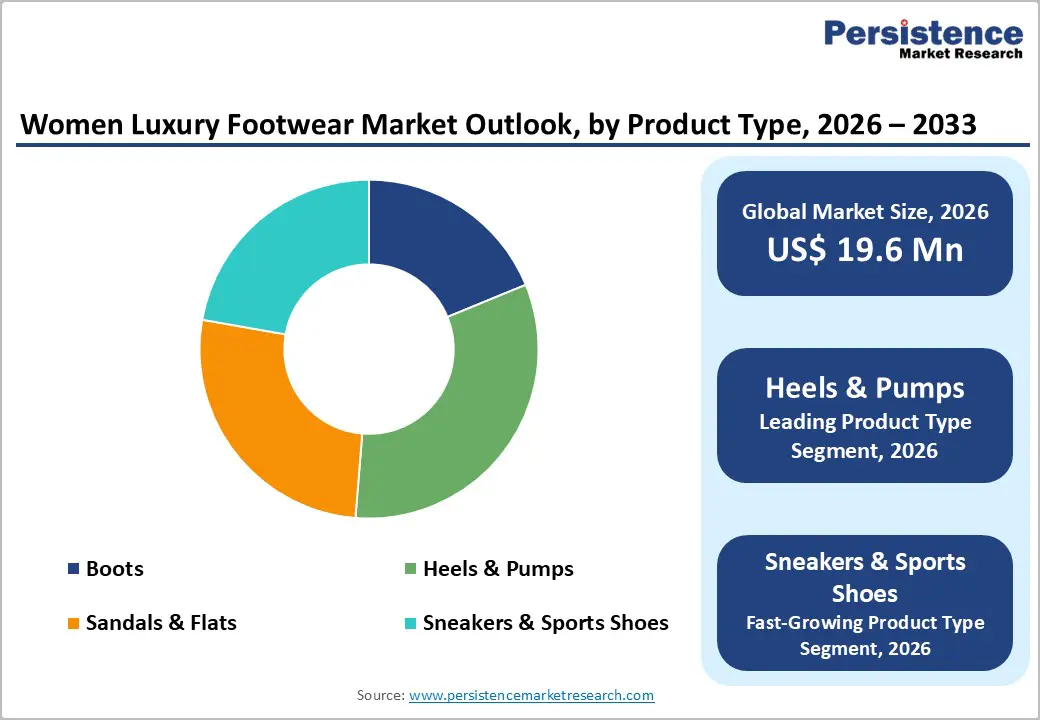

- Leading Product Type: Heels & Pumps dominate the product type segment with a 35% share in 2025, valued for elegance, status, and celebrity appeal.

- Fastest-Growing Product Type: Luxury Sneakers are the fastest-growing segment, blending comfort with high-end fashion trends and capturing younger, style-conscious consumers.

- Key Opportunity: Sustainable innovations appeal to 70% of eco-conscious luxury consumers, offering significant revenue potential through environmentally friendly and trend-driven footwear.

| Key Insights | Details |

|---|---|

|

Women's Luxury Footwear Size (2026E) |

US$ 19.6 million |

|

Market Value Forecast (2033F) |

US$ 29.7 million |

|

Projected Growth CAGR(2026-2033) |

6.1% |

|

Historical Market Growth (2020-2025) |

5.7% |

Market Dynamics

Drivers - Rising Disposable Incomes and Growing Preference for Premium Luxury Footwear

Increasing disposable incomes among urban women worldwide are fueling higher demand for luxury footwear as symbols of status, style, and sophistication. Post-2023 data shows affluent female consumers spending over 20% more on luxury items in key markets. This trend encourages premiumization, with buyers favoring artisanal, high-quality shoes over mass-produced alternatives, while brands offer limited-edition collections and entry-level luxury lines to attract younger consumers without diluting exclusivity.

Luxury brands capitalize on this growing purchasing power by enhancing product craftsmanship and storytelling, driving higher average transaction values. The strategy strengthens brand loyalty while expanding the market, as consumers increasingly see luxury footwear as an investment in both style and personal identity, supporting long-term market growth globally.

Shift in Fashion Preferences Toward Comfortable and Versatile Luxury Footwear

The evolving fashion landscape is driving demand for comfortable yet stylish footwear, such as luxury sneakers and flats, which aligns with the rise of wellness, athleisure, and hybrid work culture. Luxury sneakers now hold approximately 32% of the broader women’s luxury footwear segment, with consumers prioritizing shoes that transition easily between work, leisure, and social occasions, reflecting a preference for practical luxury.

Celebrity endorsements and runway showcases further normalize high-end casual footwear, making it aspirational yet accessible. Seasonal collections blending trendiness with everyday wear broaden the consumer base beyond formal occasions. This convergence of comfort, versatility, and style sustains consistent demand, encouraging brands to innovate while maintaining exclusivity, thus driving steady growth in the women’s luxury footwear market.

Restraints - High Production Costs and Premium Pricing Limiting Broader Market Adoption

Rising production costs, driven by premium materials such as fine leather and handcrafted details, pose a barrier to the wider adoption of women’s luxury footwear. Authentic sources indicate that luxury shoes are priced 5–10 times higher than standard footwear due to sourcing, artisanal labor, and quality control, restricting affordability for middle-income consumers in price-sensitive regions.

Economic pressures, including inflation and discretionary spending cuts, further limit purchase frequency. While exclusivity maintains brand prestige, it also constrains volume sales, particularly among emerging markets. Consumers often hesitate to invest in non-essential luxury items, making high production costs a significant restraint on overall market growth despite strong aspirational demand.

Counterfeiting and Brand Dilution Affecting Consumer Trust and Sales

Widespread counterfeiting poses a major challenge to women’s luxury footwear, with global reports estimating annual losses of over $30 billion across the luxury segment due to counterfeit products. Imitations undermine perceptions of authenticity and quality, discouraging consumers concerned with durability, craftsmanship, and resale value, while legal efforts to combat counterfeits divert brand resources.

The rise of online marketplaces exacerbates the problem, as replicas proliferate across digital platforms and social media, making it difficult for consumers to distinguish genuine products. This erosion of trust affects brand equity, discourages repeat purchases, and slows market expansion, presenting a persistent restraint on luxury footwear growth globally.

Opportunity - Innovation in Sustainable and Eco-Friendly Materials Driving Market Potential

The growing consumer focus on sustainability presents significant opportunities for women’s luxury footwear by enabling the use of recycled, plant-based, and eco-friendly materials. Surveys indicate that nearly 70% of luxury buyers consider sustainability a key purchase factor. Initiatives like ocean-plastic soles and algae-based foams have diverted millions of waste units while complying with green regulations, enhancing brand appeal.

Fastest-growing categories, particularly luxury sneakers, integrate these innovations to attract environmentally conscious Gen-Z and millennial consumers. These demographics are driving 5–7% higher growth in sustainable luxury lines through 2033, enabling brands to expand product offerings, improve brand image, and capitalize on both environmental trends and premium pricing opportunities in global markets.

E-commerce Growth and Personalized Experiences Expanding Market Reach

Digital channels present a major growth opportunity for women’s luxury footwear, as e-commerce increasingly captures market share through AR try-ons, direct-to-consumer models, and exclusive online drops. Reports show online luxury footwear sales growing by 40% post-2024, supported by flexible return policies and seamless shopping experiences, particularly in tech-savvy regions like Asia Pacific.

AI-driven personalization, including custom sizing, monogramming, and style recommendations for sneakers and heels, strengthens consumer loyalty. By offering tailored experiences and leveraging cross-border shopping trends, brands can drive significant revenue growth while reaching younger, digitally engaged luxury buyers, thereby positioning themselves competitively in an increasingly connected global marketplace.

Category-wise Analysis

Product Type Insights

Heels and pumps lead the Women Luxury Footwear product type segment with an estimated 35% market share in 2025, reflecting their enduring status as symbols of elegance and sophistication. Iconic designs from brands like Christian Louboutin and Jimmy Choo dominate red-carpet appearances and professional settings, while over 51% of luxury footwear consumers favor refined silhouettes. Celebrity endorsements and superior craftsmanship continue to sustain their premium appeal globally.

Meanwhile, the fastest-growing product type is luxury sneakers, which combine comfort with high-end fashion appeal. Blending casual versatility with luxury branding, these sneakers cater to hybrid work and leisure trends, attracting younger consumers. Their integration into seasonal collections and collaborations with designers allows brands to innovate, expand their customer base, and merge style with practical everyday wear.

Material Type Insights

Leather leads the material type segment in 2025 with around 38% market share, valued for its durability, premium tactile quality, and association with authenticity in women's luxury footwear. Full-grain and exotic leathers are highly sought for high-end boots, heels, and formal shoes, with brands emphasizing ethical tanning practices to justify premium pricing while reinforcing craftsmanship and exclusivity in global markets.

The fastest-growing material type is sustainable and alternative materials, including recycled, plant-based, and eco-friendly textiles. These innovations are particularly popular in luxury sneakers and casual footwear, appealing to environmentally conscious consumers. By integrating sustainability into design without compromising style, brands can attract Gen Z and millennial buyers, expand product offerings, and enhance their brand image in the evolving luxury footwear landscape.

Regional Insights

North America Women Luxury Footwear Market Trends and Insights

North America is led by the U.S., supported by strong retail networks and innovation hubs. Regulatory frameworks such as EPA-mandated sustainable sourcing push brands toward eco-friendly materials, aligning with consumer expectations for ethical luxury products. Fashion weeks, celebrity influence, and high disposable incomes amplify market activity, fostering a dynamic luxury ecosystem.

The region is projected to achieve a CAGR of 6.4%, driven by direct-to-consumer and omnichannel retail strategies. Consumers increasingly favor versatile luxury footwear that blends style with comfort, while e-commerce adoption ensures accessibility across urban and suburban markets, supporting steady market expansion.

Europe Women Luxury Footwear Market Trends and Insights

Europe holds the leading regional share at 37% in 2025, driven by its deep-rooted heritage in artisanal footwear production. Italy and France anchor the market with iconic luxury brands and precision craftsmanship, while Germany accounts for 25% of the regional leather segment. The UK and France drive 18–14% of sales through fashion capitals, sustaining Europe’s dominance in high-end women’s footwear globally.

Cross-border trade is strengthened by EU regulatory harmonization and sustainability mandates, enabling brands to emphasize both heritage and green practices. Seasonal fashion weeks, celebrity influence, and design innovation sustain consumer interest. Heritage-focused brands capitalize on these trends, combining artisanal techniques with modern luxury consumer expectations to reinforce Europe’s position as a global benchmark.

Asia Pacific Women Luxury Footwear Market Trends and Insights

Asia Pacific is the fastest-growing region, posting strong growth through urbanization and rising affluence, with a 31% market share in 2025. China leads with rapid urban wealth, India expands through middle-class consumption, and Japan benefits from tourism-driven luxury demand. ASEAN countries leverage manufacturing cost advantages, enabling competitive exports and supporting regional expansion.

Consumers are increasingly adopting versatile luxury footwear, such as sneakers and flats, driven by hybrid work and lifestyle trends. E-commerce penetration enhances accessibility, allowing brands to reach younger, tech-savvy consumers. Innovation in materials and design tailored to local tastes further accelerates adoption, positioning Asia-Pacific as a key driver of global growth in women’s luxury footwear.

Competitive Landscape

The women’s luxury footwear market is highly consolidated, dominated by major global players leveraging strong brand portfolios and extensive distribution networks. Companies focus on differentiation through artisanal craftsmanship, premium materials, and exclusive designs, maintaining brand prestige while appealing to high-end consumers. Celebrity endorsements and fashion collaborations further strengthen brand positioning and influence purchase behavior across key markets.

Innovation and digitalization are becoming central to competition, with initiatives in sustainable materials, personalized offerings, and direct-to-consumer e-commerce gaining prominence. Emerging trends such as resale platforms, authentication technologies, and tech-driven experiences cater to younger, tech-savvy consumers, enhancing engagement and driving long-term market growth.

Key Developments:

- In February 2024, Prada introduced its Re-Nylon sustainable footwear line, crafted from recycled materials. This launch marked a significant step toward eco-friendly luxury, combining high-end design with environmental responsibility, appealing to conscious consumers while supporting the brand’s sustainability commitments in the competitive women’s luxury footwear market.

- In October 2024, LVMH partnered as a Formula 1 Global Partner starting in 2025, elevating the visibility of its luxury footwear portfolio. The collaboration leveraged international sports marketing to position the brand at high-profile global events, enhance brand awareness, and strengthen its premium positioning among affluent consumers.

- In March 2023, Prada Group expanded its Italian production capacity by recruiting over 400 skilled artisans. The initiative aimed to strengthen craftsmanship in luxury footwear, enhance product quality, and reinforce the brand’s heritage, ensuring high-end offerings continue to appeal to discerning global consumers.

Companies Covered in Women Luxury Footwear Market

- Christian Louboutin

- Jimmy Choo

- Gucci

- Prada

- Salvatore Ferragamo

- Chanel

- Hermès

- Bottega Veneta

- Balenciaga

- Alexander McQueen

- Valentino Garavani

- Miu Miu

- Stuart Weitzman

- Roger Vivier

- Aquazzura

Frequently Asked Questions

The global women luxury footwear market is expected to reach US$ 19.6 million in 2026.

Rising disposable incomes and comfort-focused fashion trends like luxury sneakers drive demand among affluent women.

Europe leads with 37% share in 2025, driven by artisanal heritage, craftsmanship, and high-end consumer demand.

Sustainable innovations target 70% eco-conscious consumers, offering strong growth potential globally.

Leading players include Christian Louboutin, Jimmy Choo, Gucci, Prada, and Salvatore Ferragamo.