- Beauty & Personal Care

- Women Hygiene Care Product Market

Women Hygiene Care Product Market Size, Share, and Growth Forecast 2026 - 2033

Women Hygiene Care Product Market by Product Type (Sanitary Napkins/Pads, Tampons, Panty Liners, Menstrual Cups, Period Underwear, Feminine Wash, Feminine Wipes, Others), by Material Type (Cotton-Based, Non-Woven Fabric, Super Absorbent Polymer (SAP), Organic Cotton, Bamboo-Based, Biodegradable Materials), by Distribution Channel, by Regional Analysis, 2026 - 2033

Women Hygiene Care Product Market Size and Trend Analysis

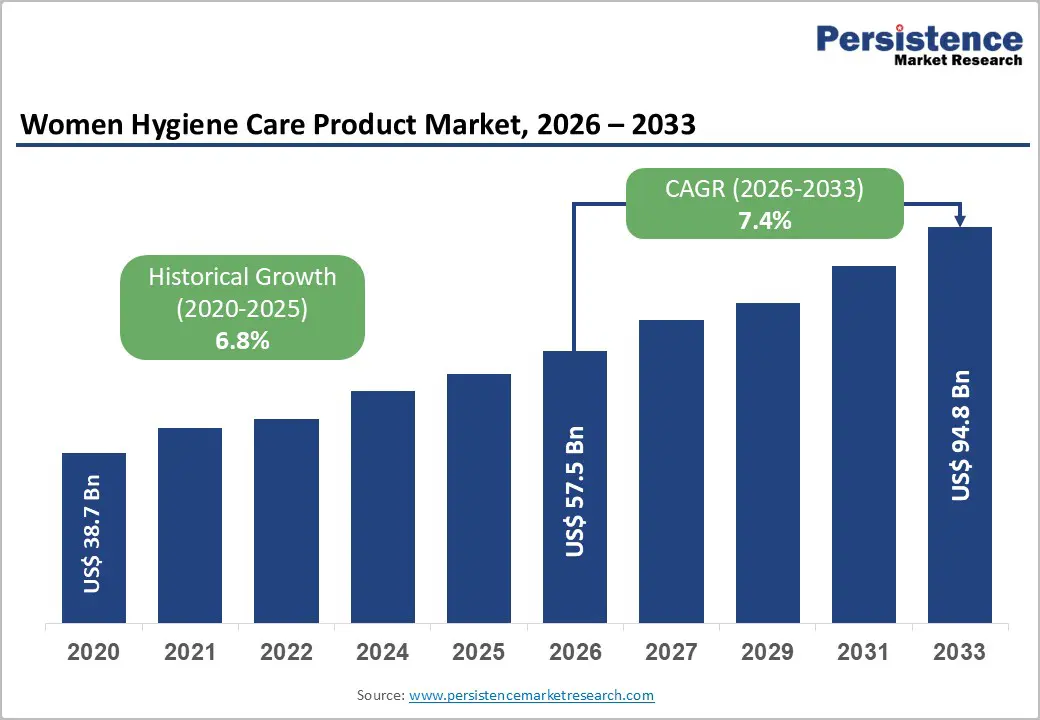

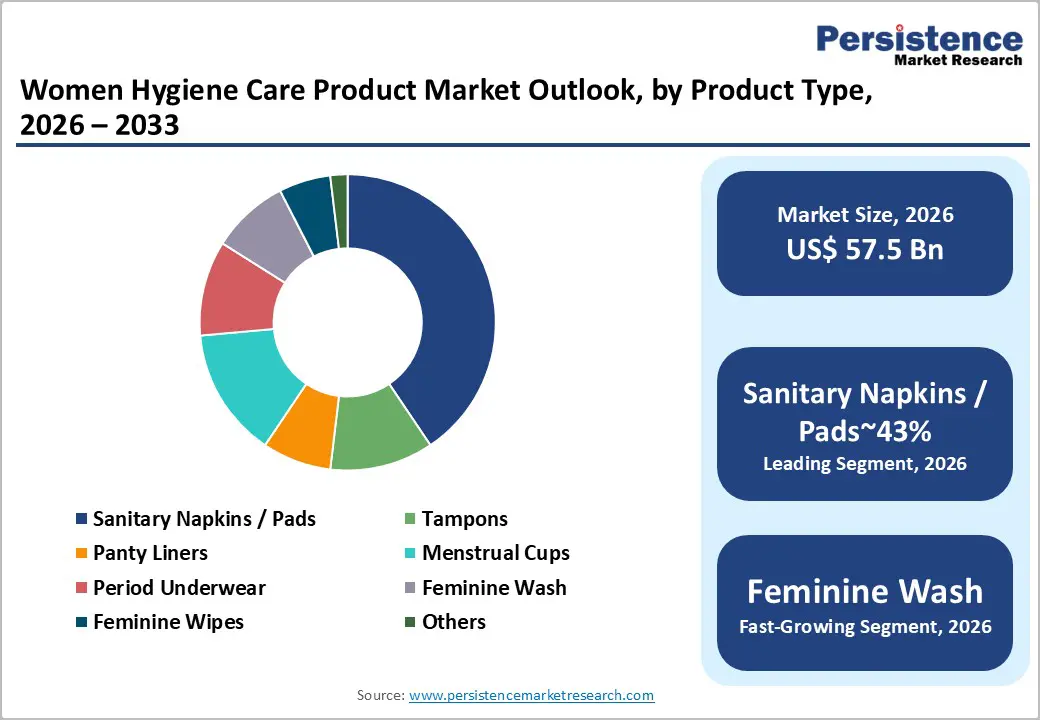

The global Women Hygiene Care Product market size is likely to be valued at US$ 57.5 billion in 2026 and is expected to reach US$ 94.8 billion by 2033, growing at a CAGR of 7.4% during the forecast period from 2026 to 2033. The market's strong and accelerating growth trajectory is driven by rising menstrual hygiene awareness across emerging economies, rapid expansion of women's health policy frameworks, and the progressive shift toward sustainable and organic feminine care products.

Key Industry Highlights:

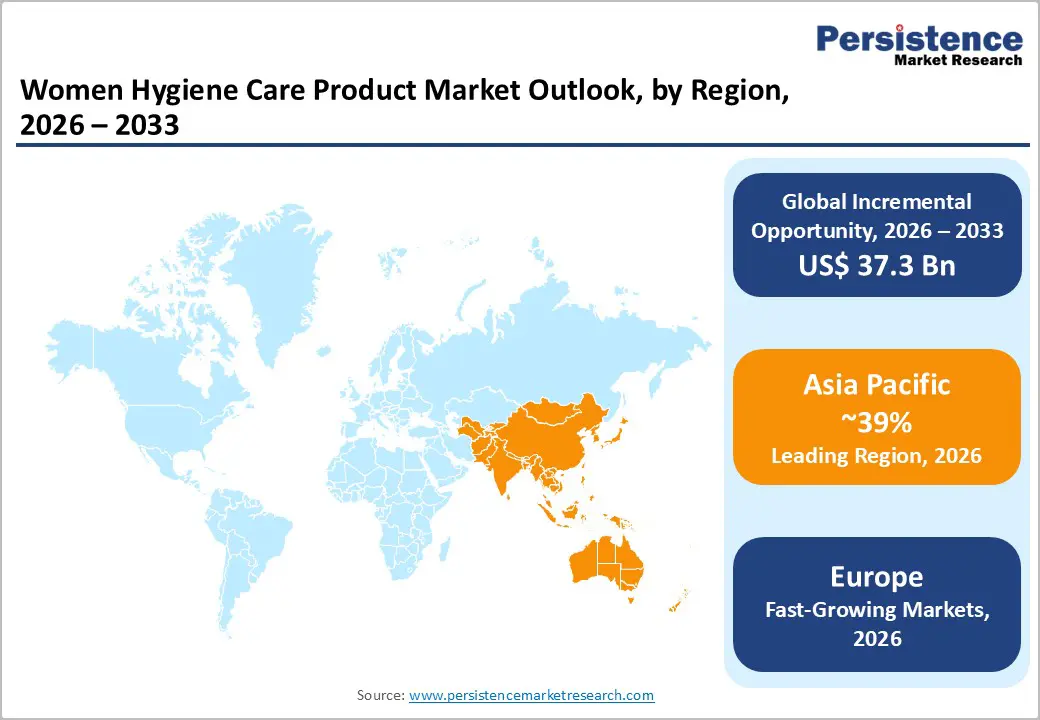

- Leading Region: Asia Pacific leads the global Women Hygiene Care Product market, holding 39% share, driven by population scale, government-backed menstrual hygiene programs in India and Southeast Asia, and the dominant manufacturing and innovation capabilities of Unicharm Corporation and Kao Corporation across the region.

- Fastest Growing Region: Europe is the fastest growing region and a sustainability-focused market for women's hygiene care products, with a strong presence in Germany, the United Kingdom, France, Spain, and the Nordic countries.

- Dominant Segment: Sanitary Napkins/Pads dominate the Women Hygiene Care Product market with approximately 43% revenue share, driven by universal consumer familiarity, widest price accessibility, active government procurement programs, and portfolio leadership by Procter & Gamble Co., Kimberly-Clark, and Unicharm.

- Fastest Growing Segment: Biodegradable Materials is the fastest growing material type segment, propelled by the EU Single-Use Plastics Directive, rising sustainability consciousness among consumers in North America and Europe, and strategic product launches by brands such as Unicharm, Essity, and Procter & Gamble in organic and compostable hygiene product lines.

- Key Market Opportunity: The convergence of D2C e-commerce subscription models and organic/sustainable product innovation presents the most significant growth opportunity, enabling manufacturers to engage directly with digitally active consumers, command premium pricing, and build high-retention recurring revenue streams, particularly among millennial and Gen Z women in Asia Pacific, North America, and Europe.

| Key Insights | Details |

|---|---|

|

Women Hygiene Care Product Market Size (2026E) |

US$ 57.5 Billion |

|

Market Value Forecast (2033F) |

US$ 94.8 Billion |

|

Projected Growth CAGR (2026–2033) |

7.4% |

|

Historical Market Growth (2020–2025) |

6.8% |

Market Dynamics

Drivers - Rising Menstrual Hygiene Awareness and Government Policy Initiatives Driving Market Expansion

Government initiatives and NGO-led programs focused on improving menstrual hygiene management (MHM) are significantly increasing demand for women hygiene care products across developing and emerging economies. The United Nations observes Menstrual Hygiene Day on May 28, supported by more than 900 partner organizations across 60+ countries, encouraging stronger public health investments in menstrual care.

In India, schemes such as Pradhan Mantri Jan Arogya Yojana and the Suvidha sanitary napkin initiative have expanded product access by distributing subsidized pads through Jan Aushadhi centers at just INR 1 per pad. Meanwhile, the WHO and UNICEF Joint Monitoring Programme reports that only 59% of schools globally have adequate menstrual hygiene facilities, highlighting a major institutional supply opportunity. These policy-driven efforts are steadily increasing product adoption and boosting demand for sanitary napkins, panty liners, and feminine wipes across South Asia, Sub-Saharan Africa, and Southeast Asia.

Urbanization and Rising Female Workforce Participation Accelerating Premium Product Adoption

Rapid urbanization across Asia Pacific, Latin America, and the Middle East is expanding the consumer base for premium women hygiene products, including organic cotton pads, menstrual cups, period underwear, and feminine wash. According to the International Labour Organization, global female labor force participation reached 47.4% in 2024, with strong growth in South and Southeast Asia as more women enter formal employment.

Urban working women typically show higher product awareness, stronger brand loyalty, and greater willingness to pay for safe and chemical-free hygiene solutions. In the European Union, the removal of VAT on menstrual products following the 2022 EU VAT Directive amendment improved affordability and supported measurable sales growth. These combined socioeconomic trends are driving premiumization while also strengthening overall category demand across both value and high-end product segments globally.

Restraints - Persistent Social Stigma and Cultural Taboos Constraining Market Penetration in Rural Areas

Despite growing global awareness, strong social stigma and cultural taboos surrounding menstruation continue to limit product adoption in rural areas of South Asia, Sub-Saharan Africa, and parts of Latin America. According to UNICEF, nearly one in three girls in South Asia are unaware of menstruation before their first cycle, highlighting major gaps in reproductive health education. This lack of awareness reduces informed purchasing decisions and slows branded product penetration in rural communities. Cultural discomfort around discussing menstruation also discourages open retail purchasing, especially in smaller towns and villages. As a result, many women continue relying on traditional and unhygienic alternatives. These barriers restrict the geographic expansion of organized brands beyond urban centers, limiting overall market penetration rates in regions that otherwise offer significant untapped demand potential for women hygiene care products.

Environmental Concerns and Regulatory Pressure on Plastic-Based Disposable Products

Environmental concerns related to plastic waste are creating regulatory challenges for conventional disposable sanitary products. Most sanitary napkins and tampons contain plastic components such as polyethylene backings and synthetic superabsorbent polymers, which contribute to non-biodegradable waste. The European Environment Agency identifies single-use hygiene products as a major source of plastic litter on European beaches. In response, governments are introducing stricter regulations, including the EU Single-Use Plastics Directive, which imposes labeling requirements and extended producer responsibility obligations on manufacturers. These compliance standards increase operational and reformulation costs, especially for companies relying on traditional materials. While sustainability creates long-term innovation opportunities, the short-term impact includes higher production expenses and potential margin pressure across the conventional disposable product segment, particularly in highly regulated European markets.

Opportunity - Rapid Growth of Sustainable, Organic, and Reusable Women Hygiene Products as a High-Value Segment

The strong consumer shift toward sustainable, organic, and reusable feminine hygiene products presents one of the most attractive growth opportunities in the market. Products such as menstrual cups, period underwear, biodegradable pads, and organic cotton tampons are expanding rapidly, driven by environmentally conscious millennial and Gen Z consumers seeking low-waste alternatives. According to the Soil Association’s Organic Market Report 2024, organic personal care categories are growing faster than conventional segments in the UK and Germany. Major companies such as Johnson & Johnson and Kimberly-Clark Corporation have expanded their organic and biodegradable product lines to capture this trend. Supportive policies, including the UK Treasury’s zero-VAT rating for period underwear from January 2023, further strengthen the commercial case for reusable formats, creating long-term value opportunities for manufacturers investing in sustainability-driven innovation.

E-Commerce, D2C Channels, and Subscription-Based Models Unlocking New Revenue Architectures

The rapid growth of e-commerce platforms and Direct-to-Consumer (D2C) models is transforming revenue generation in the women hygiene care market. Online channels allow brands to directly engage consumers, provide product education, and promote ingredient transparency while addressing privacy concerns. The UNCTAD B2C E-Commerce Index 2023 highlights strong growth in online personal care purchases across India, Brazil, Indonesia, and Southeast Asia. Digital-native brands such as Bodywise (UK) Limited have successfully used subscription models to build recurring revenue streams and higher customer lifetime value. Large multinational players, including Procter & Gamble Co. and Unicharm Corporation, are investing heavily in D2C infrastructure and subscription capabilities. As digital adoption accelerates globally, online retail and subscription-based purchasing are becoming key strategic priorities for long-term competitive advantage.

Category-wise Analysis

By Product Type Insights

Sanitary Napkins/Pads are the leading product segment in the global women hygiene care product market, contributing approximately 43% of total revenue. Their dominance is driven by strong consumer familiarity, a wide price range that includes affordable institutional options and premium organic ultra-thin variants, and extensive retail availability across all distribution formats worldwide. The World Health Organization (WHO) and UNICEF consistently identify sanitary napkins as the most widely used menstrual hygiene product across income groups, with usage rates exceeding 80% among urban women in Asia and Latin America. Major manufacturers such as Procter & Gamble Co. (Always), Kimberly-Clark Corporation (Kotex), and Unicharm Corporation (Sofy) maintain leadership through diversified portfolios that include ultra-thin, overnight, maternity, and organic products. Government procurement programs in countries such as India, Bangladesh, Kenya, and Nigeria further strengthen the segment by ensuring large institutional volumes alongside strong consumer retail demand.

By Material Type Insights

Non-Woven Fabric is the leading material segment in the women hygiene care product market, accounting for around 36% of total revenue. It is widely used as the primary topsheet and backsheet material in sanitary pads, tampons, and panty liners because of its strong fluid management capability, soft texture, cost efficiency, and compatibility with high-speed automated production lines. According to the Association of the Nonwoven Fabrics Industry (INDA), global nonwoven production exceeded 12 million metric tonnes in 2023, with hygiene applications representing the largest end-use category. Leading companies such as Svenska Cellulosa Aktiebolaget SCA (Essity) and Kimberly-Clark Corporation have vertically integrated nonwoven manufacturing to control costs and improve quality consistency. At the same time, Organic Cotton and Biodegradable Materials are emerging as the fastest-growing sub-segments, supported by rising sustainability awareness and increasing demand for eco-friendly hygiene solutions among premium consumers in North America and Europe.

By Distribution Channel Insights

Supermarkets & hypermarkets lead in terms of distribution channel, contributing approximately 34% of total retail revenue. Their dominance is supported by high consumer foot traffic, wide product assortment, competitive pricing, and strong in-store visibility that encourages habitual and impulse purchases. Organized retail chains such as Walmart, Carrefour, Tesco, and Metro AG offer extensive feminine hygiene sections featuring both private-label and branded products, making them primary purchase destinations in North America, Europe, and urban Asia Pacific market. According to the Consumer Goods Forum, organized grocery retail accounts for over 70% of personal care purchases in developed retail markets globally. However, Online Retail and Direct-to-Consumer (D2C) channels are the fastest-growing segments, driven by digital adoption, subscription convenience, product variety, and enhanced privacy in purchasing. This shift is encouraging brands to adopt omnichannel strategies to maintain market competitiveness.

Regional Insights

North America Women Hygiene Care Product Trends

The United States leads the North American Women Hygiene Care Product market, characterized by a mature and highly penetrated consumer base with strong demand for premium, organic, and sustainable products. The U.S. Food and Drug Administration (FDA) classifies tampons as Class II medical devices and regulates absorbency, labeling, and ingredient disclosure, ensuring strict safety standards. As of 2024, 41 U.S. states have eliminated the “tampon tax,” improving affordability and supporting stable category growth.

Procter & Gamble Co. and Kimberly-Clark Corporation maintain strong positions through their Always, Tampax, and Kotex brands. Sustainability-focused innovation remains a key trend, with D2C brands such as Thinx expanding rapidly in period underwear and subscription-based organic formats. The U.S. Department of Health and Human Services (HHS) has integrated menstrual hygiene into broader women’s health equity initiatives, strengthening institutional demand. Canada reflects similar premiumization trends, with growing adoption of reusable menstrual cups and organic cotton products.

Europe Women Hygiene Care Product Trends

Europe is the fastest growing region and a sustainability-focused market for women's hygiene care products, with a strong presence in Germany, the United Kingdom, France, Spain, and the Nordic countries. The EU Single-Use Plastics Directive, enforced from 2021, has accelerated the transition toward biodegradable and organic product materials, with compliance monitored by the European Environment Agency. In the United Kingdom, the zero-VAT policy on period underwear introduced in January 2023 has supported growth in reusable formats.

Essity AB, headquartered in Sweden, leads the European market through its Libresse and Bodyform brands. Consumers in Germany and France show high sensitivity toward ingredient transparency and chemical-free formulations, driving growth in certified organic ranges. Meanwhile, Spain and Italy are witnessing rising demand for panty liners and feminine wash products, supported by retail modernization and increasing health awareness. Harmonized EU regulations continue to enhance product standards and streamline cross-border trade.

Asia Pacific Women Hygiene Care Product Trends

Asia Pacific is the largest and fastest-growing regional market for women hygiene care products, supported by large population size, rising female workforce participation, government hygiene programs, and expanding retail and e-commerce infrastructure. China, the world’s largest feminine hygiene manufacturing hub, is experiencing rapid premiumization, with increasing adoption of organic cotton and ultra-thin premium pads. Japan remains a global innovation leader, with Unicharm Corporation advancing SAP formulations and ergonomic designs that influence global markets.

In India, sanitary napkin penetration in rural areas remains below 40%, representing significant untapped growth potential. Government initiatives such as the National Menstrual Hygiene Scheme (NMHS) and subsidized distribution through Jan Aushadhi centers are gradually improving access. Southeast Asian countries including Indonesia, Vietnam, Thailand, and the Philippines are also witnessing strong demand growth, driven by urbanization, retail expansion, and manufacturing investments by major players.

Competitive Landscape

The global Women Hygiene Care Product market demonstrates a moderately consolidated structure, with multinational leaders such as Procter & Gamble Co., Kimberly-Clark Corporation, Unicharm Corporation, Essity AB, and Kao Corporation collectively accounting for approximately 55–60% of global revenue. Key competitive advantages include strong brand equity, global distribution reach, material innovation capabilities, and sustainability initiatives. Leading companies are actively investing in organic product lines, biodegradable packaging, and D2C subscription models to strengthen consumer engagement and long-term loyalty.

At the same time, emerging challengers such as Thinx, Bodywise (UK) Limited, and Maxim Hygiene are reshaping the market through transparency-driven marketing, sustainable positioning, and community engagement strategies. The industry is also experiencing increased merger and acquisition activity, as established FMCG players acquire sustainability-focused start-ups to accelerate portfolio diversification and maintain competitive advantage in a rapidly evolving market landscape.

Key Developments:

- In January 2024: Unicharm Corporation introduced a new biodegradable range under its Sofy brand for India and Southeast Asian markets, using plant-based topsheet materials to attract eco-conscious consumers and meet rising demand for sustainable menstrual care options in high-growth regions.

- In September 2024: Procter & Gamble expanded its Always Organic Cotton product line into 12 additional European countries, backing the rollout with a focused digital campaign highlighting ingredient clarity and dermatological certification to appeal to consumers seeking chemical-free and eco-friendly menstrual care products.

- In March 2025: Kimberly-Clark Corporation announced a strategic upgrade to its Kotex Direct-to-Consumer subscription service in North America, incorporating AI-driven personalized product recommendations aimed at boosting customer loyalty and encouraging trial among younger, digitally savvy consumers.

Companies Covered in Women Hygiene Care Product Market

- Ontex Group

- Unicharm Corporation

- Svenska Cellulosa Aktiebolaget SCA

- Kimberly-Clark Corporation

- Kao Corporation

- Henkel AG & Co. KGaA

- Edgewell Personal Care Co.

- Glenmark Pharmaceuticals Ltd.

- Procter & Gamble Co.

- Unilever PLC

- Johnson & Johnson Services, Inc.

- Zeta Farmaceutici S.p.A.

- Maxim Hygiene

- Bodywise Limited

- Essity AB

- Energizer Holdings

- Thinx Inc.

- Natracare

- Rael Inc.

- Saathi

Frequently Asked Questions

The global Women Hygiene Care Product Market is projected to reach US$ 94.8 billion by 2033, growing at a CAGR of 7.4% from its 2026 valuation of US$ 57.5 billion.

Key demand drivers include government menstrual hygiene programs, rising female workforce participation, increasing urbanization, and growing consumer preference for premium and sustainable hygiene products across emerging and developed markets.

Sanitary Napkins/Pads dominate the market with about 43% revenue share, supported by strong consumer familiarity, wide price accessibility, government procurement programs, and leading global brands like Always, Kotex, and Sofy.

Asia Pacific leads the global market due to large population scale, rising premium adoption in China, government hygiene initiatives in India, Japanese innovation leadership, and strong demand growth across Southeast Asia.

The strongest growth opportunity lies in D2C e-commerce combined with sustainable product innovation, enabling brands to attract digitally active millennials and Gen Z consumers through subscription models and eco-friendly offerings.