- Sensors & Controls

- Smart Sensors Market

Smart Sensors Market Size, Trends, Share, and Growth Forecast 2025 - 2032

Smart Sensors Market Analysis By Sensor Type (Motion Sensors, Temperature Sensors, Pressure Sensors, Image Sensors, Touch Sensors, Position Sensors, Others), Technology (MEMS-based Smart Sensors, CMOS-based Smart Sensors, Others), Component, End-use, and Regional Analysis 2025 - 2032

Smart Sensors Market Share and Trends Analysis

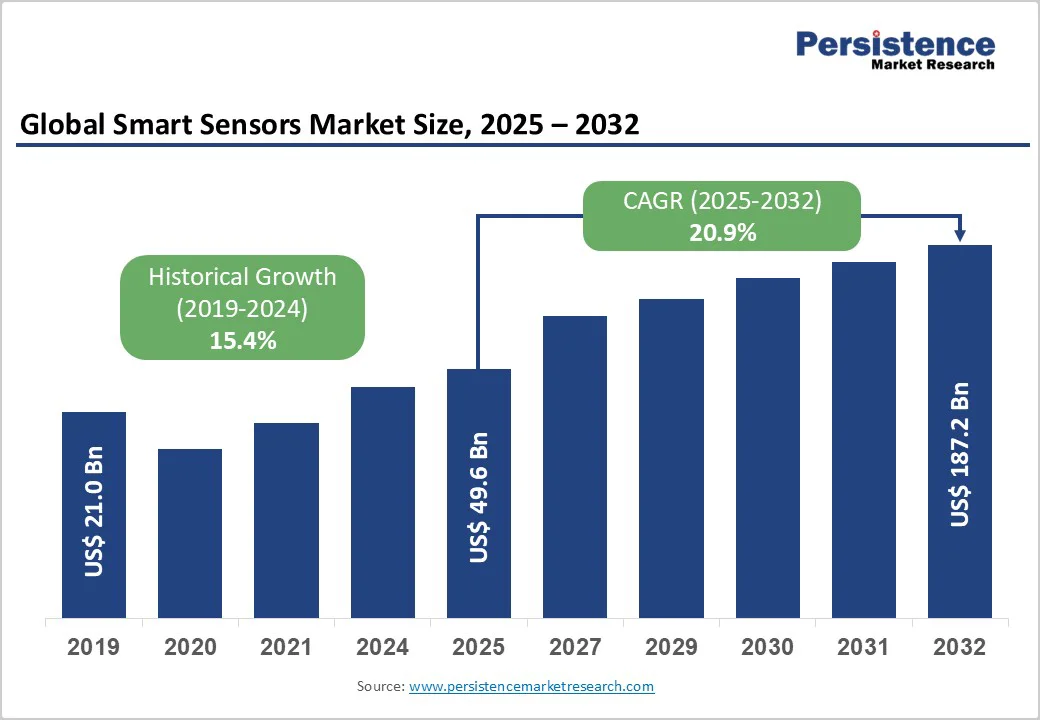

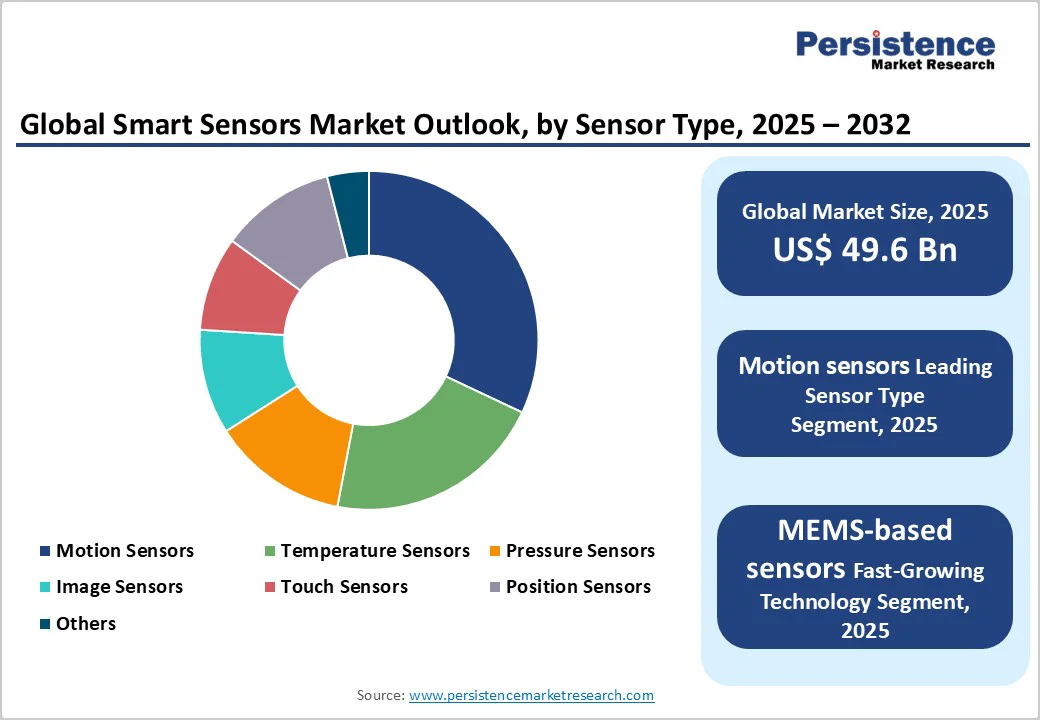

The global smart sensors market size is likely to be valued at US$49.6 billion in 2025 and is projected to reach US$187.2 billion by 2032, growing at a CAGR of 20.9% between 2025 and 2032.

Rapid digital transformation initiatives, a surge in Internet of Things (IoT) deployments, and the rise of Industry 4.0 frameworks across major economies are driving unprecedented demand for intelligent sensing solutions.

The expanding automotive sector’s shift towards autonomous and connected vehicles, coupled with growing emphasis on energy efficiency and environmental monitoring, underscores the comprehensive growth trajectory expected in the forecast period.

Key Market Highlights:

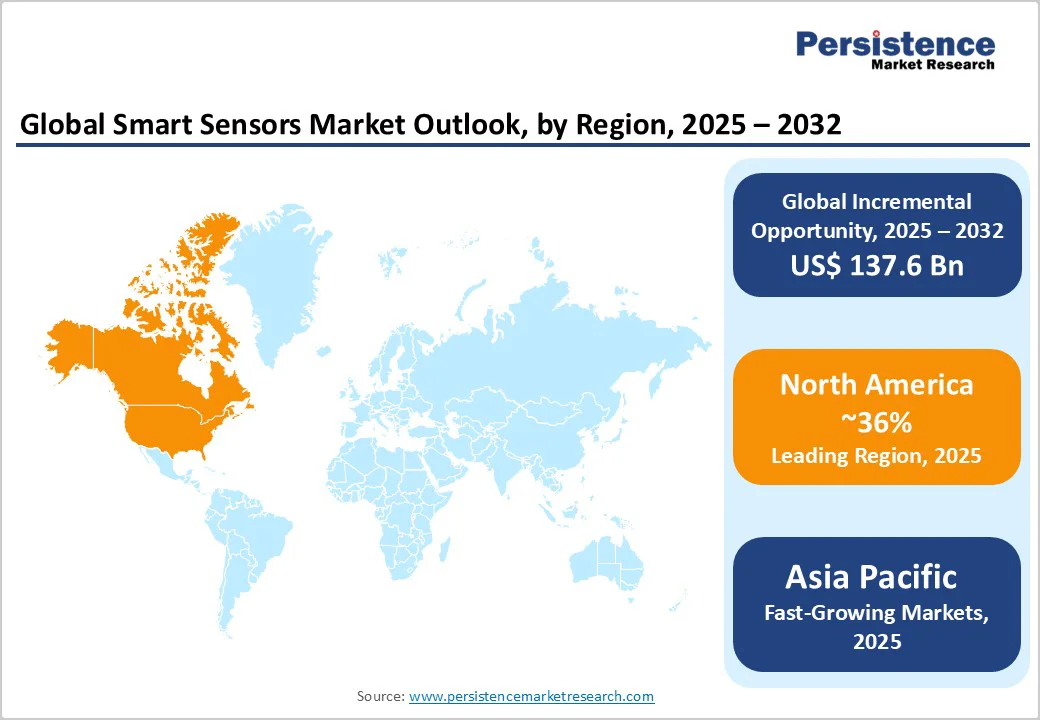

- Leading Region: North America leads the market with 36% revenue share in 2025, driven by early IoT adoption, strong semiconductor manufacturing, and advanced Industry 4.0 initiatives.

- Fastest Growing Region: Asia Pacific is the fastest-growing region at a 22% CAGR, fueled by China’s sensor production, Japan’s automotive innovations, and India’s digital infrastructure expansion.

- Dominant Segment: Motion sensors dominate globally with over 32% share, supported by automotive ADAS, robotics, and consumer electronics applications.

- Fastest Growing Segment: MEMS-based sensors are the fastest-growing technology segment, capitalizing on miniaturization, cost efficiency, and multi-sensor fusion.

- Key Market Opportunity: Healthcare and wearables offer the most promising growth opportunity, as smart biosensors and telehealth solutions transform patient care and chronic disease management.

| Key Insights | Details |

|---|---|

| Smart Sensors Market Size (2025E) | US$49.6 billion |

| Market Value Forecast (2032F) | US$187.2 billion |

| Projected Growth CAGR (2025 - 2032) | 20.9% |

| Historical Market Growth (2019-2024) | 15.4% |

Market Dynamics

Driver - Proliferation of IoT and Connected Devices

The global surge in IoT device deployment, projected to exceed 30 billion connected devices by 2025, is a primary driver for smart sensor demand. Such devices rely on precise data capture to enable automation, asset tracking, and environmental monitoring in manufacturing, logistics, agriculture, and smart building applications.

Real-time condition monitoring minimizes downtime, optimizes resource utilization, and reduces operational costs. Enterprises are leveraging sensor networks for granular visibility into processes, driving investments in scalable, interoperable sensor platforms. The rise of 5G networks further amplifies demand by supporting higher data throughput and ultra-low latency communication, enabling sensors to deliver actionable insights instantaneously.

Advances in MEMS-Based Sensor Technologies

Micro-Electro-Mechanical Systems (MEMS) technologies have revolutionized sensor miniaturization and integration. MEMS accelerometers, gyroscopes, and pressure sensors are integral to Advanced Driver Assistance Systems (ADAS) and autonomous vehicle platforms, supporting functions such as collision avoidance, lane departure warning, and adaptive cruise control. The automotive sector’s stringent safety standards have accelerated R&D in high-precision MEMS devices.

The growing wearable electronics market relies on ultra-compact MEMS sensors for fitness trackers, smartwatches, and medical wearables. MEMS innovations have also enabled multi-sensor fusion on a single chip, reducing BOM and power consumption while enhancing performance.

Restraint - Complex Integration and High Deployment Costs

Deploying smart sensors across legacy systems entails substantial upfront investments in hardware, software, and skilled personnel. Complex protocols and interoperability challenges between heterogeneous devices can slow rollout.

Industries such as oil & gas, chemicals, and utilities must adhere to stringent safety and compliance standards, which extend project timelines and increase costs. Small and medium-sized enterprises often face budget constraints, limiting large-scale sensor network adoption despite evident efficiency gains.

Cybersecurity and Data Privacy Concerns

As sensors become ubiquitous in critical infrastructure, from smart grids and traffic management to healthcare monitoring, the risk of cyberattacks on sensor networks rises significantly. Regulatory frameworks such as the European Union’s GDPR and the U.S.’s HIPAA impose strict data privacy and security requirements.

Companies must implement end-to-end encryption, secure firmware updates, and identity management protocols, which increases overall total cost of ownership (TCO). Any breach can have severe operational and reputational impacts, prompting cautious adoption among risk-averse industries.

Opportunity - Rise of Edge AI and On-Sensor Processing

Edge AI is transforming smart sensor capabilities by enabling on-device data processing and machine-learning inference. Sensors integrated with microcontrollers and dedicated AI accelerators can execute anomaly detection, image classification, and predictive analytics locally, reducing dependency on cloud infrastructure and data transmission costs.

This paradigm is critical for applications requiring ultra-low latency, such as industrial robotics, autonomous vehicles, and critical healthcare monitoring. The integration of neuromorphic computing architectures in sensor nodes is gaining traction, offering energy-efficient, real-time analytics at the edge.

Healthcare and Wearables Expansion

Smart sensors are pivotal in advancing telehealth, remote patient monitoring, and personalized medicine. The wearable medical devices market is projected to grow at a positive CAGR by 2032. It relies heavily on high-accuracy biosensors for measuring vital signs, glucose, and other health metrics.

Governments and healthcare providers are incentivizing digital health initiatives, particularly in light of an aging population and the need for chronic disease management. Innovations in biocompatible, flexible sensors and minimally invasive implantable devices present significant market opportunities, enabling continuous monitoring without compromising patient comfort.

Category-wise Analysis

By Sensor Type Insights

Motion sensors, including accelerometers and gyroscopes, command approximately 32% of the sensor-type market. Their widespread use in automotive safety systems, industrial robotics, and wearable electronics underscores their leadership. In ADAS, high-precision MEMS motion sensors enable features such as electronic stability control and rollover detection.

In consumer electronics, they facilitate gesture control, screen orientation, and fitness tracking. The industrial segment utilizes motion sensors for vibration analysis and predictive maintenance, reducing unplanned downtime by up to 30%. Strong growth in e-mobility and smart robotics continues to bolster demand for advanced motion sensing.

By Technology Insights

MEMS-based smart sensors held the largest share at around 58% in 2025. Their compact form factor, low power consumption, and cost efficiency make them ideal for embedded applications. Automotive OEMs have standardized on MEMS for airbag deployment sensors, tire pressure monitoring, and inertial measurement units.

Consumer electronics drivers include compact wearable devices and smartphones, which integrate multiple MEMS sensors on a single die. In industrial automation, MEMS sensors enable precise measurements of flow, tilt, and acoustics. Continued R&D in materials and packaging is expected to improve MEMS reliability and performance further.

By Component Insights

Microcontrollers account for over 35% of component revenues, serving as the brains of smart sensors. Integrated MCUs facilitate local data aggregation, signal conditioning, and communication protocols (e.g., BLE, Zigbee, LoRaWAN). The rise of efficient 32-bit ARM Cortex-M architectures tailored for IoT applications has enhanced processing capabilities while minimizing energy footprints.

Key trends include the integration of AI accelerators and secure enclaves within MCUs, enabling encrypted on-chip analytics and protecting sensitive data. The ability to run machine-learning models directly on sensor nodes enhances real-time decision-making and reduces cloud dependency.

By Industry Insights

The healthcare sector leads demand for smart sensors, capturing nearly 24% of the market. Biosensors, electrochemical sensors, and inertial sensors are central to patient monitoring devices, smart inhalers, and rehabilitation trackers. Telehealth platforms integrate multiple sensors to remotely monitor vital signs, reducing hospital readmissions by 15-20%.

Regulatory approvals for wearable medical devices have accelerated product launches. Growth drivers include government reimbursement policies for remote patient monitoring, the rising prevalence of chronic diseases, and consumer adoption of health-focused wearables.

Regional Insights

North America Smart Sensors Market Trends

North America, led by the U.S., remains at the forefront of sensor technology and adoption. The region’s emphasis on R&D and home to major sensor manufacturers-such as Honeywell, Texas Instruments, and Microchip-propels innovation. In manufacturing, smart factories implement sensor networks for end-to-end visibility, predictive maintenance, and quality control, yielding productivity gains up to 25%.

Automotive OEMs headquartered in Michigan and California are integrating sophisticated sensor suites for ADAS, connected car services, and hydrogen-fuel-cell vehicles. Healthcare institutions across the U.S. are deploying wireless biosensors for ICU monitoring and chronic care management, driven by reimbursement incentives and pandemic-accelerated digital health programs.

Europe Smart Sensors Market Trends

Strong industrial roots and collaborative R&D ecosystems characterize Europe’s smart sensors market. Germany leads with comprehensive adoption in automotive and manufacturing sectors, driven by Industry 4.0 roadmaps and government incentives for digitalization. Major automotive OEMs in Germany, France, and the U.K. invest heavily in LiDAR, radar, and ultrasonic sensor integration for next-gen mobility solutions.

The European Union’s regulatory harmonization, including GDPR and the Cybersecurity Act, ensures secure data handling and fosters trust in IoT deployments. Smart building initiatives in the Nordics emphasize energy management and occupancy sensing, reducing energy consumption by 15-20% in pilot buildings.

Asia Pacific Smart Sensors Market Trends

Asia Pacific, led by China, Japan, and India, is the fastest-growing region with a CAGR exceeding 22%. China’s vast consumer electronics manufacturing base and government support for semiconductor self-sufficiency have accelerated sensor production and innovation. Japanese automakers are integrating advanced MEMS and radar sensors into electric vehicles, while India’s burgeoning electronics ecosystem and Make in India initiatives are fostering local sensor startups.

Southeast Asia’s smart agriculture and infrastructure projects utilize environmental and soil sensors to enhance crop yields and optimize water usage. Collaborative efforts between industry and academia in the Asia Pacific are driving next-generation sensor research in nanomaterials and flexible electronics.

Competitive Landscape

The global smart sensors market exhibits a moderately consolidated structure, with top players capturing over 45% of total revenues. STMicroelectronics, Infineon Technologies, Honeywell, Texas Instruments, and Analog Devices lead through extensive product portfolios, global reach, and strategic alliances.

These companies emphasize continuous R&D investments, as reflected in double-digit R&D spend-averaging 8-10% of revenue-to develop AI-enabled, low-power sensors.

Recent consolidation moves include STMicroelectronics’ acquisition of NXP’s MEMS sensors business for US$ 950 million, aimed at bolstering automotive and industrial sensing capabilities. Smaller specialized vendors focus on niche applications such as medical wearables and environmental monitoring, driving innovation in biocompatible materials and ultra-low-power designs.

Key Market Developments:

- July 2025: STMicroelectronics finalizes acquisition of NXP’s MEMS sensor business (US$950 million), enhancing its portfolio in automotive and industrial sensors with advanced MEMS accelerometers and gyroscopes.

- March 2025: Honeywell launches Versatilis™ IoT Sensor Solutions, offering battery-powered wireless sensors with integrated analytics for predictive maintenance and environmental monitoring.

- May 2025: Infineon Technologies introduces new 77 GHz Radar System on Chip (SoC) for enhanced ADAS performance, enabling extended detection range and multi-object tracking capabilities.

Companies Covered in Smart Sensors Market

- Microsemi

- STMicroelectronics

- Infineon

- ABB

- Omron

- Rockwell

- SICK,

- Eaton

- Honeywell

- Texas Instruments

- Renesas

- Yokogawa

- NXP

- Analog Devices

- Siemens, Bosch

- Sensirion

- GE

- Cannon

- Sony

- Ams

- TDK

Frequently Asked Questions

The global smart sensors market is valued at US$ 49.6 billion in 2025 and projected to reach US$ 187.2 billion by 2032, reflecting a robust CAGR of 20.9%.

Key drivers include the proliferation of IoT devices, advancements in MEMS technology, Industry 4.0 adoption, and increased emphasis on real-time monitoring for predictive maintenance.

Motion sensors command the largest share at approximately 32%, owing to their critical role in automotive ADAS, industrial robotics, and consumer electronics.

North America leads with 36% revenue share, while Asia Pacific is the fastest-growing region at a CAGR of 22%, driven by China’s manufacturing prowess and government digitization initiatives.

Healthcare and wearables represent the most promising opportunity, as smart biosensors and remote monitoring solutions transform chronic disease management and personalized care.

Major players include STMicroelectronics, Honeywell International, Infineon Technologies, Texas Instruments, Analog Devices, ABB, Omron, NXP Semiconductors, and others, leading in R&D and strategic collaborations.