- Medical Devices

- Surgical Dressing Market

Surgical Dressing Market Size, Share, Trends, Growth, and Regional Forecast, 2026 - 2033

Surgical Dressing Market by Product (Silver Dressings, Povidone-Iodine Dressings, PHMB Dressings, and Others), Application (Chronic Wounds, and Acute Wounds) End-user (Hospitals, Specialty Clinics, Ambulatory Surgery Centers, and Home Care Settings), and Regional Analysis from 2026 - 2033

Surgical Dressing Market Share and Trends Analysis

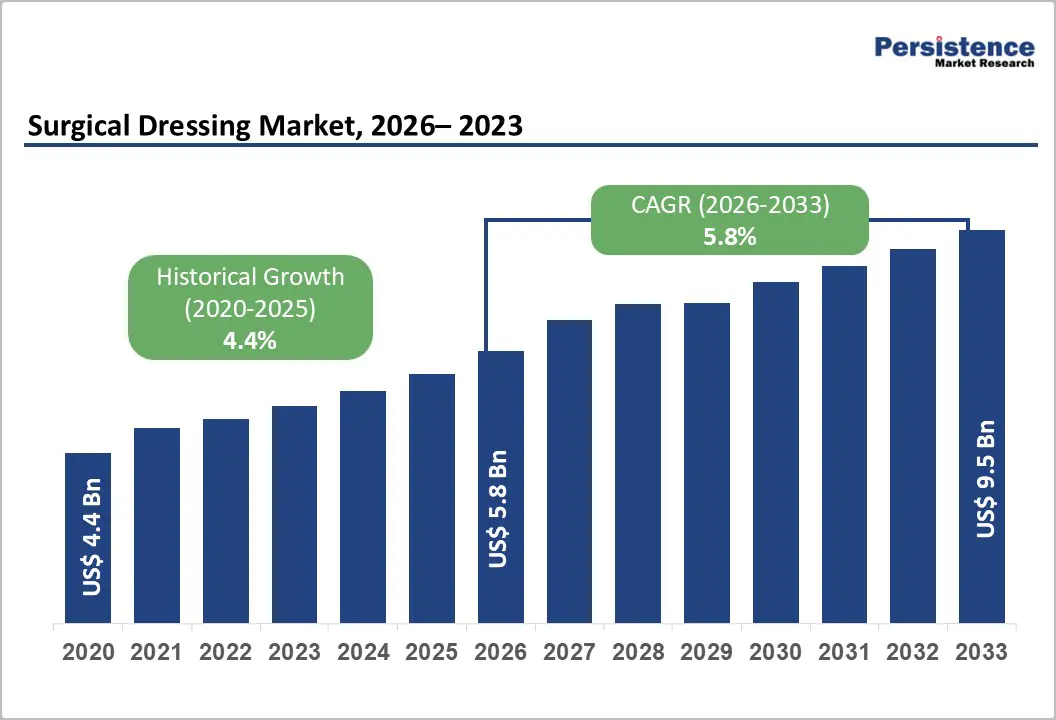

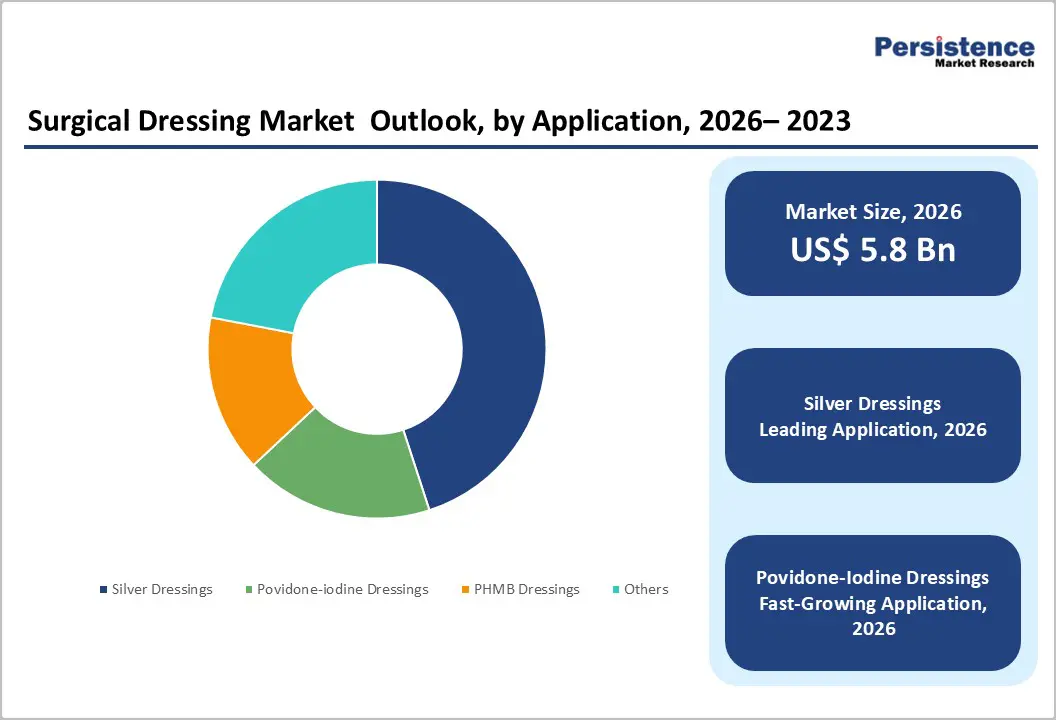

The global surgical dressing market size is estimated to grow from US$ 5.8 Bn in 2026 to US$ 9.5 Bn by 2033 growing at a CAGR of 5.3% during the forecast period from 2026 to 2033.

Global demand for surgical dressings is rising steadily, driven by the growing burden of chronic and acute wounds, increasing awareness of advanced wound management solutions, and a strong shift toward minimally invasive and patient-centric care models. The rising incidence of diabetes, vascular disorders, pressure ulcers, and post-surgical wounds has significantly increased the need for moisture-balancing, infection-preventive, and healing-accelerating dressings.

Expansion of hospitals, specialty wound care clinics, ambulatory surgery centers, and home healthcare services supported by higher healthcare expenditure and improved access to advanced wound therapies is accelerating overall market growth. Ongoing innovation in semi-permeable foams, films, and hydrogel-based dressings is improving exudate management, minimizing infection risk, and enhancing clinical outcomes. In parallel, the growing adoption of home-based wound care, increasing clinical focus on reducing hospital length of stay, and rising acceptance of advanced dressings in long-term care environments are further propelling market expansion.

Key Industry Highlights

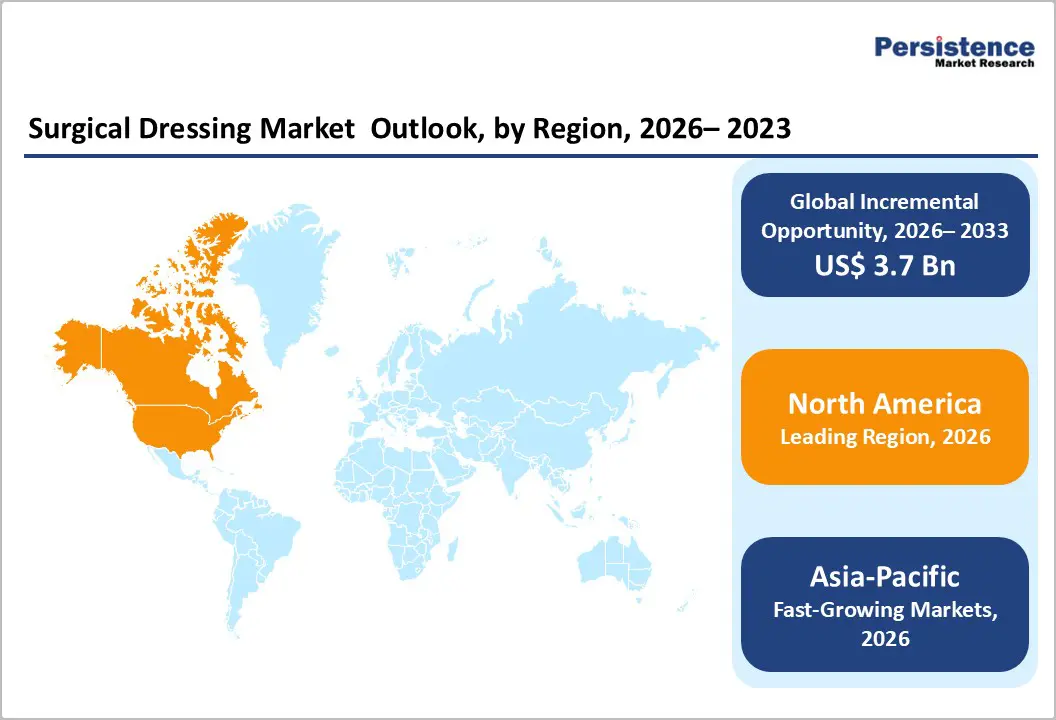

- Leading Region: North America holds the largest market share at 47.4%, supported by advanced healthcare infrastructure, high adoption of advanced wound care products, strong reimbursement systems, and early uptake of innovative interactive dressings.

- Fastest-Growing Region: Asia Pacific is expanding at the fastest pace due to a large and aging population, rising prevalence of chronic diseases, rapid expansion of hospital and outpatient infrastructure, and increasing investment in advanced wound management solutions.

- Leading Product Segment: Silver dressings dominate the market due to their broad applicability across chronic and acute wounds, superior antimicrobial efficacy, moisture control, and suitability for both inpatient and home care settings.

- Fastest-Growing Product Segment: Povidone-iodine dressings are witnessing rapid growth as healthcare providers increasingly adopt moisture-retentive solutions for burns, surgical wounds, and chronic ulcers requiring gentle healing environments.

- Leading Application Segment: Chronic wounds remain the largest application area, driven by high treatment volumes associated with diabetic foot ulcers, pressure ulcers, and venous leg ulcers that require prolonged and consistent use of interactive dressings.

- Fastest-Growing Application Segment: Acute wounds are expanding rapidly as rising surgical procedures, trauma cases, and post-operative care needs increase demand for advanced dressings that support faster healing and infection prevention.

| Key Insights | Details |

|---|---|

|

Surgical Dressing Market Size (2026E) |

US$ 5.8 Bn |

|

Market Value Forecast (2033F) |

US$ 9.5 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

5.8% |

|

Historical Market Growth (CAGR 2020 to 2025) |

4.4% |

Market Dynamics

Driver - Rising Surgical Volumes and Shift Toward Advanced Antimicrobial Dressings

The global increase in elective surgical procedures, emergency trauma interventions, and complex post-operative wound management is a major driver of demand for surgical dressings across hospitals and ambulatory care settings. Factors such as an aging population, higher prevalence of chronic diseases requiring surgical intervention, expanding access to healthcare services, and rising incidence of road accidents and sports injuries are contributing to higher surgical case volumes worldwide. As surgical throughput increases, so does the need for reliable wound protection solutions that support faster healing, minimize complications, and reduce length of hospital stay. Ambulatory surgery centers, in particular, are witnessing growing demand for surgical dressings that enable efficient post-operative care and early patient discharge.

There is a pronounced shift toward advanced and antimicrobial surgical dressings as healthcare providers prioritize infection prevention, optimal moisture balance, and improved clinical outcomes. Concerns around surgical site infections and hospital-acquired infections are accelerating adoption of silver-based, iodine-based, foam, and hydrogel dressings that provide antimicrobial protection while maintaining ideal wound environments. These advanced dressings help reduce dressing change frequency, enhance patient comfort, and support faster tissue regeneration. Increasing clinical evidence supporting their efficacy, along with growing emphasis on value-based care and cost reduction through complication prevention, continues to reinforce their adoption across inpatient, outpatient, and home care settings.

Restraints - Cost Sensitivity and Continued Reliance on Traditional Surgical Dressings

The widespread availability and continued use of low-cost traditional dressings, such as conventional gauze and basic wound coverings, remain a significant restraint on the adoption of advanced surgical dressings. In resource-limited healthcare settings, particularly in low- and middle-income regions, cost considerations often outweigh clinical benefits when selecting wound care products. Public hospitals, smaller clinics, and rural healthcare facilities frequently rely on basic dressings due to budget constraints, limited procurement flexibility, and established clinical practices. This sustained dependence on conventional solutions slows the transition toward advanced surgical dressings, even in cases where improved healing outcomes and reduced complication rates could justify higher upfront costs.

Moreover, the high cost of advanced surgical dressings—including antimicrobial, bioactive, and specialty foam or hydrogel products—poses a major barrier to broader market penetration. Premium pricing is driven by complex manufacturing processes, incorporation of antimicrobial agents, and regulatory compliance requirements. These higher costs can limit reimbursement coverage and restrict adoption in cost-sensitive healthcare systems, particularly for outpatient and home care use where reimbursement policies may be less comprehensive. As a result, healthcare providers often reserve advanced dressings for severe or high-risk wounds, limiting volume growth despite rising clinical awareness of their benefits.

Opportunity - Expanding Opportunities through Emerging Markets and Advanced Dressing Innovation

Rapid expansion of healthcare infrastructure in emerging markets, particularly across Asia Pacific, Latin America, and the Middle East, is creating significant growth opportunities for the surgical dressing market. Increasing access to hospitals, ambulatory surgery centers, and specialty wound care clinics, combined with rising surgical procedure volumes and a growing burden of chronic diseases such as diabetes and vascular disorders, is driving sustained demand for advanced wound care solutions. As healthcare spending increases and awareness of modern wound management improves, providers in these regions are gradually transitioning from conventional dressings toward advanced surgical dressings that offer better healing outcomes and reduced complication rates.

Furthermore, innovation in smart and bioactive surgical dressings is opening new avenues for product differentiation and value-based pricing. Development of antimicrobial, sensor-enabled, and healing-accelerating dressings that monitor wound conditions, manage exudate, and reduce infection risk is aligning well with the global focus on infection prevention and cost containment. Healthcare systems are increasingly prioritizing solutions that lower surgical site infection rates, reduce hospital readmissions, and shorten treatment duration. Advanced dressings that demonstrate clinical and economic benefits are therefore gaining traction, supporting wider adoption across inpatient, outpatient, and home care settings while enabling manufacturers to command premium pricing.

Category-wise Analysis

By Product, Silver Dressings Dominate Globally Due to Broad Use Across Chronic and Acute Wound Management

The silver dressings segment is projected to dominate the global surgical dressing market in 2026, accounting for a revenue share of 45.0%. Segment leadership is driven by widespread use in managing moderate-to-high exudating wounds, including pressure ulcers, diabetic foot ulcers, venous leg ulcers, surgical wounds, and traumatic injuries. Silver-based dressings provide effective antimicrobial protection while maintaining optimal moisture balance, helping reduce infection risk and support faster healing. Their suitability across inpatient, outpatient, and home care settings, combined with reduced dressing change frequency and improved patient comfort, continues to strengthen adoption.

Growing use of advanced antimicrobial and silicone-border variants, along with increasing penetration in home care and long-term care facilities, is further supporting segment growth. Continuous innovation focused on improved conformability, extended wear time, and enhanced infection control reinforces the global dominance of silver dressings.

By Application, Chronic Wounds Lead Due to Rising Disease Burden and Long-Term Care Needs

The chronic wounds segment is projected to dominate the global surgical dressing market in 2026, accounting for a revenue share of 60.0%. This dominance is primarily attributed to the increasing global prevalence of diabetes, obesity, cardiovascular diseases, and an aging population, all of which contribute significantly to chronic wound incidence. Conditions such as diabetic foot ulcers, pressure ulcers, and venous leg ulcers require prolonged treatment and consistent use of interactive dressings to maintain optimal healing environments.

Advanced surgical dressings help regulate moisture levels, minimize infection risk, and promote granulation tissue formation, making them a preferred choice for chronic wound management. Growing emphasis on early intervention, complication prevention, and reduction of hospital readmissions is further driving demand. In addition, expansion of home healthcare services and structured chronic wound management programs is accelerating adoption across healthcare systems.

By End User, Hospitals Dominate Due to High Patient Volume and Advanced Wound Care Capabilities

The hospitals segment is projected to dominate the global surgical dressing market in 2026, accounting for a revenue share of 48.0%. Hospitals manage a high volume of complex and severe wounds, including post-surgical wounds, trauma injuries, burns, and advanced chronic ulcers, which require specialized wound care products and multidisciplinary clinical oversight. Strong access to trained wound care specialists, standardized protocols, and infection control infrastructure supports higher utilization of advanced surgical dressings in hospital settings.

Hospitals are also early adopters of antimicrobial and bioactive dressings aimed at reducing healing time and preventing complications. Rising surgical procedures, increasing trauma cases, and growing emphasis on shortening hospital stays through effective wound management continue to reinforce segment dominance. Integration of standardized wound care pathways and ongoing clinician training further contributes to sustained leadership.

Region-wise Insights

North America Surgical Dressing Market Trends

The North America surgical dressing market is expected to dominate globally with a value share of 47.4% in 2026, led by the U.S. due to advanced healthcare infrastructure, high wound care expenditure, and early adoption of technologically advanced wound management solutions. The region benefits from a strong presence of leading manufacturers, established distribution and reimbursement frameworks, and wide availability of trained healthcare professionals across hospitals, outpatient facilities, and home care settings.

High prevalence of chronic wounds, including diabetic foot ulcers, pressure ulcers, and venous leg ulcers, continues to drive sustained demand for interactive dressings such as semi-permeable films, foams, and hydrogel-based products. Growing focus on reducing hospital stays and preventing wound infections is accelerating adoption of moisture-balancing and antimicrobial dressings. Favorable reimbursement policies, frequent product launches, and a clear regulatory pathway through FDA approvals further support innovation and rapid clinical uptake. Increasing home healthcare adoption and integration of digital wound monitoring technologies are strengthening market penetration.

Europe Surgical Dressing Market Trends

The Europe surgical dressing market is expected to grow steadily, supported by rising adoption of advanced wound care technologies, an aging population with a high burden of chronic wounds, and strong emphasis on evidence-based and minimally invasive treatment approaches. Countries including Germany, the U.K., France, Italy, and the Nordic region are leading adopters due to well-developed healthcare systems, high clinical awareness, and robust hospital and outpatient infrastructure.

Increasing incidence of diabetes, vascular disorders, and post-surgical wounds is driving demand for moisture-retentive and infection-preventive dressings. European healthcare systems emphasize cost-effective wound management, encouraging adoption of interactive dressings that support faster healing and reduced complication rates. Regulatory harmonization, broader reimbursement coverage for advanced wound therapies, and integration of wound care protocols into community and home care settings are further supporting market growth.

Asia Pacific Surgical Dressing Market Trends

The Asia Pacific surgical dressing market is expected to register a relatively higher CAGR of around 7.2% between 2026 and 2033, driven by expanding healthcare access, rising prevalence of chronic diseases, and increasing awareness of advanced wound management solutions. Countries such as China, India, Japan, South Korea, and Southeast Asian nations are experiencing growing demand for interactive wound dressings due to rising diabetes incidence, increasing surgical volumes, and rapid expansion of hospital and outpatient infrastructure.

Improving affordability and wider availability of advanced wound care products are accelerating adoption across urban and semi-urban settings. The shift toward home-based care and community wound management is further supporting demand for easy-to-use, long-wear dressings such as foams and hydrogels. Government initiatives to strengthen healthcare systems, rising investments in medical education, and expanding presence of global manufacturers through partnerships and local production are contributing to sustained regional growth.

Market Competitive Landscape

The global surgical dressing market is highly competitive, with strong participation from companies such as B. Braun SE, 3M, Cardinal Health, Smith+Nephew, Coloplast, and McKesson Medical-Surgical Inc. These players benefit from well-established distribution networks, diversified surgical and advanced wound care portfolios, and ongoing innovation across products such as gauze and non-woven dressings, semi-permeable films, foam dressings, hydrocolloids, hydrogels, and antimicrobial surgical dressings. Rising surgical volumes, increasing prevalence of chronic and post-operative wounds, and heightened focus on infection prevention and optimal moisture management are driving widespread adoption across hospitals, specialty clinics, ambulatory surgery centers, and home care settings.

Manufacturers are increasingly emphasizing advanced antimicrobial and bioactive dressing technologies, enhanced absorbency and breathability, and user-friendly designs that support faster healing, reduced dressing change frequency, and improved patient comfort. Key strategic priorities include expanding surgical dressing product portfolios, strengthening clinical evidence and outcomes, enhancing clinician training and awareness, improving reimbursement coverage, and accelerating penetration in outpatient and home-based surgical wound care environments.

Key Industry Developments:

- In December 2025, MPM Medical announced a major expansion of its U.S. manufacturing capabilities through the acquisition of a full collagen manufacturing platform along with associated FDA 510(k) clearance for surgical collagen devices. This expansion strengthens the company’s capacity to supply high-quality, U.S.-manufactured collagen products to advanced wound care, surgical, and private-label partners, supporting growing demand for collagen-based surgical dressings.

- In July 2025, scientists at Birla Institute of Technology and Science (BITS) Pilani, Hyderabad campus, developed a smart wound dressing designed to actively eliminate infection-causing bacteria. The researchers noted that early detection of infections is often difficult, particularly in chronic and deep wounds, highlighting the importance of responsive and intelligent wound care technologies.

- In July 2024, Mölnlycke Health Care, a global MedTech leader specializing in wound care and surgical solutions, announced a US$15 million investment in MediWound Ltd. (Nasdaq: MDWD) through a definitive share purchase agreement under a private investment in public equity (PIPE). MediWound is a global leader in next-generation enzymatic therapies for non-surgical wound debridement, with a focus on improving clinical outcomes, enhancing patient experience, and reducing treatment costs and unnecessary surgical interventions.

Companies Covered in Surgical Dressing Market

- B. Braun SE

- 3M

- Cardinal Health

- Smith+Nephew

- Coloplast

- Mölnlycke AB

- Convatec Group PLC

- Lotus

- AVERY DENNISON CORPORATION

- Advanced Medical Solutions Limited

- McKesson Medical-Surgical Inc.

- Medline

- PAUL HARTMANN AG

- MediWound

- Others

Frequently Asked Questions

The global surgical dressing market is projected to be valued at US$ 5.8 Bn in 2026.

Rising surgical volumes, increasing incidence of chronic wounds and trauma cases, growing geriatric and diabetic populations, and accelerating adoption of advanced and antimicrobial dressings to reduce surgical site infections drive sustained market growth.

The global surgical dressing market is poised to witness a CAGR of 5.8% between 2026 and 2033.

Expansion of outpatient and home-based wound care, rising demand for advanced antimicrobial and moisture-retentive dressings, and increasing surgical procedures in emerging markets present high-growth opportunities.

B. Braun SE, 3M, Cardinal Health, Smith+Nephew, Coloplast McKesson Medical-Surgical Inc., are some of the key players in the surgical dressing market market.