- Healthcare Services

- Surgical Preoperative Planning Software Market

Surgical Preoperative Planning Software Market Size, Share and Growth Forecast, 2026 - 2033

Surgical Preoperative Planning Software Market by Surgical Specialty (Orthopedic Surgery, Spine Surgery, Others), Deployment Mode (On-Premise, Cloud-Based, Hybrid), Technology (2D Planning, 3D Reconstruction & Modeling, Others), and Regional Analysis for 2026 - 2033

Surgical Preoperative Planning Software Market Size and Trends Analysis

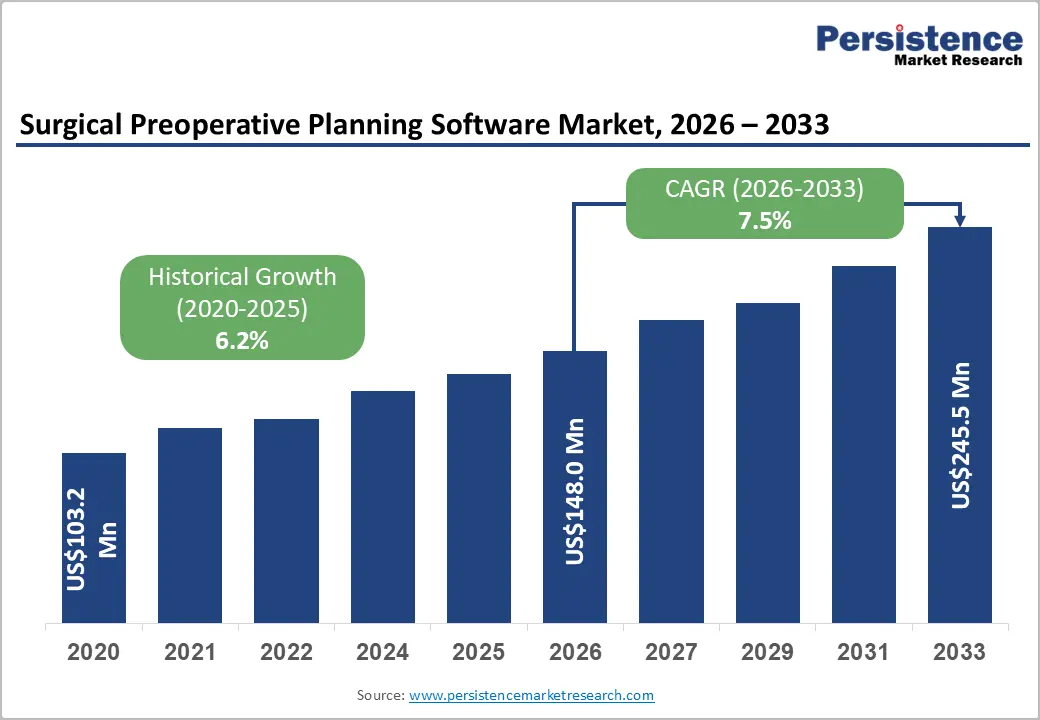

The global surgical preoperative planning software market size is likely to be valued at US$148.0 million in 2026 and is projected to reach US$245.5 million by 2033, growing at a CAGR of 7.5% during the forecast period from 2026 to 2033, driven by the growing adoption of digital surgery, AI-powered surgical planning, and 3D surgical simulation technologies. Increasing volumes of orthopedic, neurosurgical, cardiovascular, and spine procedures are boosting demand for solutions that enhance surgical precision and workflow efficiency.

The integration of surgical planning software, advanced imaging, and predictive analytics, alongside expanding cloud-based healthcare infrastructure, continues to support market growth.

Key Industry Highlights:

- Dominant Surgical Specialty: Orthopedic surgery is expected to lead with an estimated 35% share in 2026, while neurosurgery is projected to be the fastest-growing segment at 8.1% CAGR through 2033, driven by rising adoption of precision-guided and minimally invasive procedures.

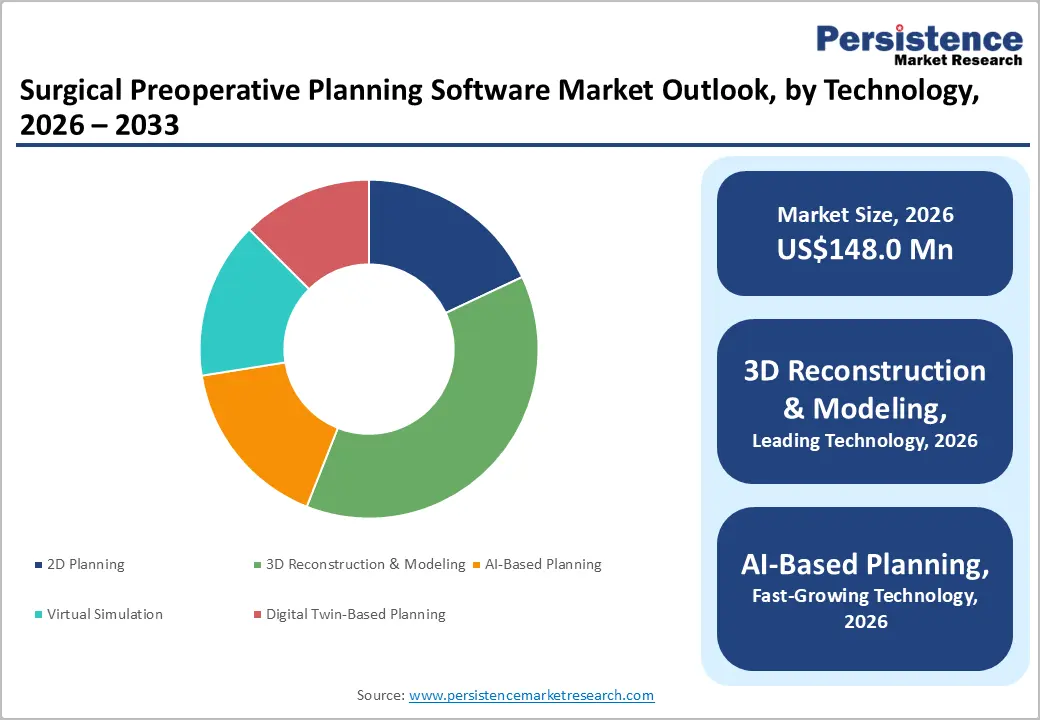

- Leading Technology: The 3D reconstruction & modeling segment is anticipated to account for approximately 38% of market revenue in 2026, while AI-based planning is likely to record the fastest growth at 9.2% CAGR during 2026 - 2033, supported by advancements in automation and predictive analytics.

- Dominant Deployment Mode: On-premise solutions are projected to hold around 52% of the market share in 2026, while cloud-based platforms are expected to be the fastest-growing deployment segment at 9.8% CAGR through 2033, reflecting increasing healthcare digitalization.

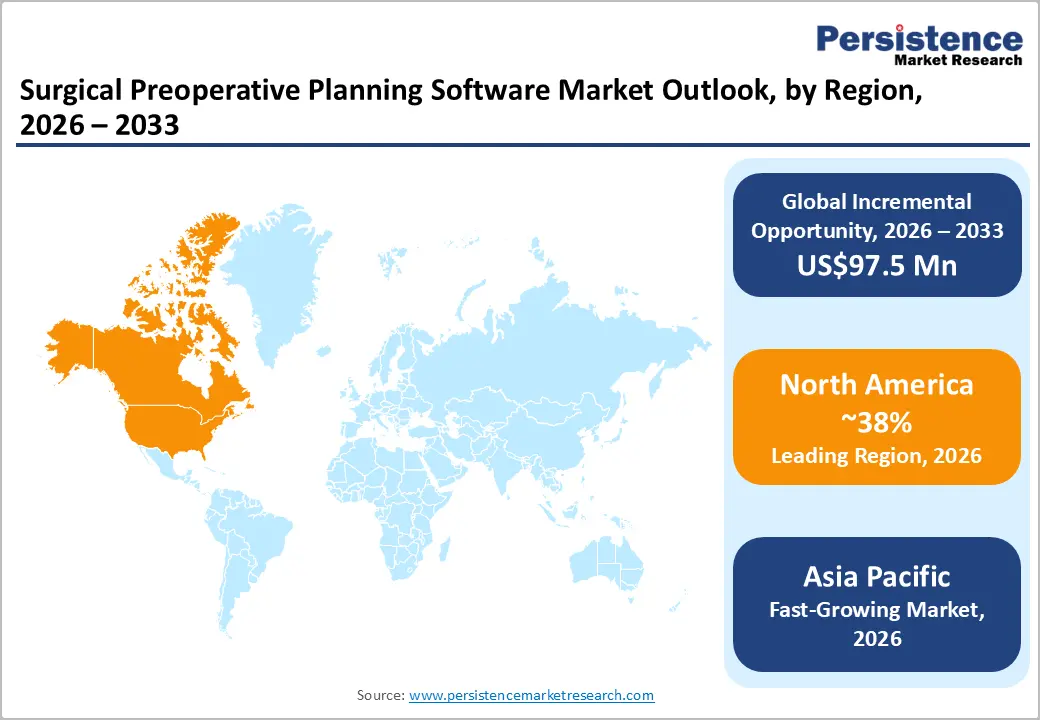

- Regional Leadership: North America is poised to dominate with an estimated 38% share in 2026, while Asia Pacific is forecast to register the fastest growth at 9.4% CAGR through 2033, supported by expanding healthcare infrastructure and surgical volumes.

- Competitive Environment: Competitive activity is centered on AI-enabled product innovation, cloud-based platform development, strategic partnerships, and personalized surgical planning solutions, with notable advancements announced by Olympus, Corin, and Johnson & Johnson in 2025.

DRO Analysis

Driver - Growing Adoption of AI-Enabled and Image-Guided Surgical Planning

The increasing use of artificial intelligence and advanced medical imaging is accelerating demand for surgical preoperative planning software. According to the World Health Organization (WHO), more than 300 million surgical procedures are performed each year globally, while the OECD reports continued growth in orthopedic, cardiovascular, and neurosurgical interventions across developed healthcare systems. The widespread use of CT, MRI, and 3D imaging technologies allows surgeons to visualize patient-specific anatomy before surgery, improving procedural planning and accuracy.

AI-powered planning platforms automate anatomical segmentation, implant positioning, and risk assessment, helping reduce planning time and intraoperative variability. Growing adoption of robot-assisted surgery, which surpassed 2.6 million procedures globally in 2024 according to Intuitive Surgical, further increases the need for precise preoperative planning. As hospitals invest in digital surgery, image-guided interventions, and workflow optimization technologies, demand for advanced planning software is expected to rise steadily throughout the forecast period.

Restraint - High Implementation Costs and Integration Complexity

High implementation costs and integration challenges remain significant barriers to broader adoption of surgical preoperative planning software. Advanced platforms require integration with imaging systems, PACS, electronic health records (EHRs), and surgical navigation technologies, often requiring substantial capital investment and specialized IT expertise. According to the Healthcare Information and Management Systems Society (HIMSS), interoperability and system integration continue to rank among the leading challenges in healthcare digital transformation projects.

Beyond software acquisition costs, healthcare providers must invest in cybersecurity, clinician training, software validation, and workflow redesign. Data from the American Hospital Association (AHA) indicate that many community and rural hospitals continue to face financial pressures that limit investments in advanced digital infrastructure. These challenges are particularly pronounced in developing markets where healthcare IT spending remains comparatively low, slowing adoption rates despite the clinical benefits offered by advanced planning solutions.

Opportunity - Expansion of Cloud-Based Surgical Planning in Emerging Healthcare Markets

Emerging healthcare markets present substantial opportunities for vendors offering cloud-based surgical planning software solutions. According to the World Bank, healthcare expenditure across many Asia-Pacific and Middle Eastern economies has increased steadily over the past decade, supporting investments in hospital modernization and digital health technologies. Countries such as China, India, Indonesia, and Saudi Arabia are expanding healthcare infrastructure while accelerating adoption of cloud-enabled clinical platforms.

Cloud deployment significantly reduces upfront infrastructure costs compared with traditional on-premise systems and enables remote collaboration among surgeons, radiologists, and multidisciplinary teams. According to the International Telecommunication Union (ITU), internet penetration exceeded 68% globally in 2024, improving access to cloud-based healthcare applications. The growing adoption of subscription-based software models further lowers entry barriers for mid-sized hospitals and specialty clinics. As AI, cloud computing, and virtual surgical simulation technologies continue to converge, vendors are well positioned to capitalize on the expanding digital healthcare ecosystem across emerging markets.

Category-wise Analysis

Surgical Specialty Insights

Orthopedic surgery is expected to lead the market with an estimated 35% share in 2026, supported by its high surgical volume globally. According to the World Health Organization (WHO), musculoskeletal conditions affect more than 1.7 billion people worldwide, creating substantial demand for joint replacement, fracture fixation, and trauma procedures. The increasing use of 3D implant templating, patient-specific instrumentation, and digital surgical planning tools is helping surgeons improve procedural accuracy and postoperative outcomes.

Neurosurgery is projected to be the fastest-growing segment, expanding at an 8.1% CAGR during 2026 - 2033. Rising incidences of brain tumors, epilepsy, and other neurological disorders are increasing demand for highly precise surgical interventions. The adoption of AI-powered brain mapping, advanced neuronavigation systems, and minimally invasive neurosurgical techniques continues to strengthen the need for sophisticated preoperative planning software. Growing investments in neurotechnology and precision medicine further support segment growth.

Deployment Mode Insights

On-premise deployment is anticipated to account for approximately 52% of market revenue in 2026, driven by strong adoption among large hospitals and academic medical centers. According to the American Hospital Association (AHA), healthcare organizations continue to prioritize cybersecurity, regulatory compliance, and direct control over patient data, supporting demand for on-premise solutions. These systems also offer deeper integration with imaging platforms, EHRs, and surgical navigation technologies used in complex surgical environments.

Cloud-based deployment is forecast to register the fastest growth at a 9.8% CAGR through 2033. The International Telecommunication Union (ITU) estimates global internet penetration exceeded 68% in 2024, improving access to cloud-enabled healthcare applications across developed and emerging markets. Lower infrastructure requirements, automatic software updates, and enhanced remote collaboration capabilities are encouraging healthcare providers to adopt cloud-based surgical planning platforms. The expansion of digital health initiatives worldwide is expected to further accelerate adoption.

Technology Insights

3D reconstruction & modeling is expected to remain the leading technology segment, capturing an estimated 38% share in 2026. The technology converts CT and MRI scans into highly detailed patient-specific anatomical models, enabling improved surgical visualization and procedural planning. Its widespread adoption across orthopedic, spine, cardiovascular, and cranio-maxillofacial surgeries has made it a critical component of modern digital surgery workflows. The growing preference for personalized treatment planning continues to support segment dominance.

AI-based planning is projected to be the fastest-growing technology segment, advancing at a 9.2% CAGR during 2026 - 2033. Increasing investment in healthcare AI is accelerating the adoption of automated segmentation, predictive analytics, and virtual surgical simulation tools. In 2025, Olympus and Johnson & Johnson introduced new AI-enabled surgical planning solutions, reflecting the industry's growing focus on intelligent clinical decision support. Continuous advancements in machine learning and medical image analysis are expected to further drive technology adoption.

Regional Insights

North America Surgical Preoperative Planning Software Market Trends

North America is expected to account for approximately 38% of the global surgical preoperative planning software market in 2026. The region performs some of the world's highest volumes of complex orthopedic, cardiovascular, and neurological procedures, creating strong demand for surgical planning software. According to the American Joint Replacement Registry (AJRR), hip and knee arthroplasty procedures continue to rise annually, while robotic-assisted surgery adoption has expanded rapidly across major health systems, supporting the use of AI-enabled preoperative planning platforms.

U.S. Surgical Preoperative Planning Software Market Trends

The U.S. is projected to contribute nearly 82% of the North America market in 2026. The country performs over 1 million joint replacement procedures annually, according to the AJRR, making orthopedic planning a major growth area. In addition, the FDA has accelerated clearances for AI-enabled medical imaging and surgical software solutions, while leading hospital systems continue investing in digital operating rooms and personalized surgery technologies.

Canada Surgical Preoperative Planning Software Market Trends

Canada is estimated to account for approximately 12% of the regional market in 2026. According to the Canadian Institute for Health Information (CIHI), joint replacement procedures have shown sustained growth over the past decade, increasing demand for surgical workflow optimization. Investments through Canada's digital health initiatives and growing adoption of image-guided surgery platforms are supporting the integration of advanced planning software across major healthcare facilities.

Europe Surgical Preoperative Planning Software Market Trends

Europe is expected to represent approximately 29% of global market revenue in 2026, supported by strong adoption of minimally invasive and image-guided surgical procedures. The region benefits from advanced healthcare infrastructure and growing use of AI in clinical workflows. The implementation of the European Union Medical Device Regulation (EU MDR) has also increased focus on validated software-based surgical technologies, encouraging adoption across healthcare systems.

Germany Surgical Preoperative Planning Software Market Trends

Germany is anticipated to hold nearly 29% of the European market in 2026. According to the OECD, Germany maintains one of the highest hospital bed capacities and surgical procedure volumes in Europe, creating favorable conditions for digital surgery adoption. The country's strong medical technology industry and investments in AI-driven healthcare solutions continue to strengthen demand for advanced preoperative planning platforms.

U.K. Surgical Preoperative Planning Software Market Trends

The U.K. is expected to account for approximately 18% of the regional market in 2026. NHS digital transformation initiatives and increasing deployment of robotic-assisted surgery systems are supporting market growth. The NHS has continued expanding its network of robotic surgery centers, while investments in healthcare AI and imaging analytics are increasing the use of virtual surgical planning solutions to improve procedural efficiency and patient outcomes.

Asia Pacific Surgical Preoperative Planning Software Market Trends

Asia Pacific is projected to account for approximately 24% of the global market in 2026 and is expected to record the fastest growth through 2033. The region benefits from rapidly increasing healthcare expenditure, expanding surgical capacity, and government-led digital health initiatives. According to the World Bank, healthcare spending across major Asia-Pacific economies has grown steadily over the past decade, supporting investments in advanced imaging, AI, and surgical technologies.

China Surgical Preoperative Planning Software Market Trends

China is estimated to contribute nearly 38% of the Asia Pacific market in 2026. The country continues to expand healthcare infrastructure through its national healthcare modernization programs while increasing adoption of AI in medical imaging. Government support for smart hospitals and digital healthcare ecosystems has accelerated the deployment of advanced surgical planning and image-guided surgery solutions across leading healthcare institutions.

Japan Surgical Preoperative Planning Software Market Trends

Japan is projected to account for approximately 22% of the regional market in 2026. According to government statistics, more than 29% of Japan's population is aged 65 years or older, creating significant demand for orthopedic, cardiovascular, and neurological procedures. The country's leadership in robotic surgery adoption and advanced imaging technologies has encouraged healthcare providers to integrate sophisticated preoperative planning platforms to improve surgical precision and clinical outcomes.

Competitive Landscape

The global surgical preoperative planning software market is moderately consolidated, with leading companies including Materialise NV, Brainlab AG, Stryker Corporation, Siemens Healthineers AG, and GE HealthCare accounting for a substantial share of market revenue. These companies leverage strong hospital networks, imaging expertise, and integrated digital surgery portfolios while investing heavily in AI-driven planning, 3D visualization, and surgical workflow automation to strengthen their market positions.

Meanwhile, specialized players such as PeekMed, EchoPixel, and ImmersiveTouch are focusing on niche applications and specialty surgical segments. Barriers such as regulatory approvals, clinical validation requirements, and hospital system integration limit new entrants, although advances in cloud computing and AI are creating opportunities for software-focused innovators. Market consolidation is expected to increase gradually as larger healthcare technology companies pursue acquisitions, partnerships, and platform expansions to enhance their digital surgery and preoperative planning capabilities.

Key Industry Developments:

- In June 2025, HealthpointCapital acquired a majority stake in ImmersiveTouch to strengthen its presence in virtual and augmented reality-enabled surgical planning technologies. The acquisition expanded capabilities in immersive visualization and patient-specific preoperative planning across multiple surgical specialties.

- In March 2025, Olympus Corporation and Ziosoft launched Olympus’ first AI-powered surgical planning platform for liver, lung, and kidney procedures. The solution enhanced 3D anatomical visualization and AI-driven preoperative planning, improving precision in complex surgical interventions.

Companies Covered in Surgical Preoperative Planning Software Market

- Materialise NV

- Brainlab AG

- Stryker Corporation

- Siemens Healthineers AG

- GE HealthCare Technologies Inc.

- Philips Healthcare

- Canon Medical Systems Corporation

- PeekMed

- EchoPixel Inc.

- ImmersiveTouch Inc.

- Ziosoft Inc.

- Medtronic plc

- Zimmer Biomet Holdings Inc.

- Johnson & Johnson MedTech

- Surgical Theater LLC

Frequently Asked Questions

The global surgical preoperative planning software market is projected to reach US$148.0 million in 2026.

Growing adoption of AI-enabled planning, advanced medical imaging, and precision surgery technologies drives market growth.

The surgical preoperative planning software market is expected to grow at a CAGR of 7.5% from 2026 to 2033.

Cloud-based deployment, healthcare digitalization, and expanding adoption across emerging healthcare markets create significant growth opportunities.

Materialise NV, Brainlab AG, Stryker Corporation, Siemens Healthineers AG, and GE HealthCare are among the leading market participants.