- Medical Devices

- Examination and Surgical Gloves Market

Examination and Surgical Gloves Market Size, Share, and Growth Forecast 2026 - 2033

Examination and Surgical Gloves Market by Product Type (Examination Gloves, Surgical Gloves), by Material (Latex, Nitrile, Vinyl, Others), by End User (Hospitals, Clinics, Ambulatory Surgical Centers, Diagnostic Laboratories, Others), by Regional Analysis, 2026-2033

Examination and Surgical Gloves Market Size and Trends Analysis

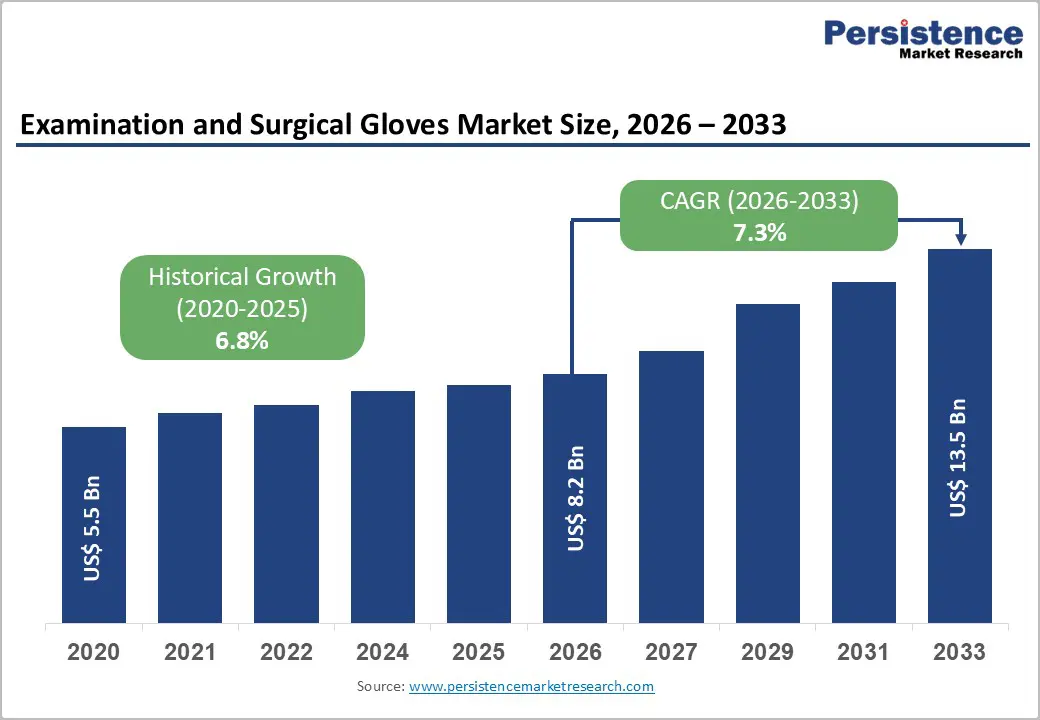

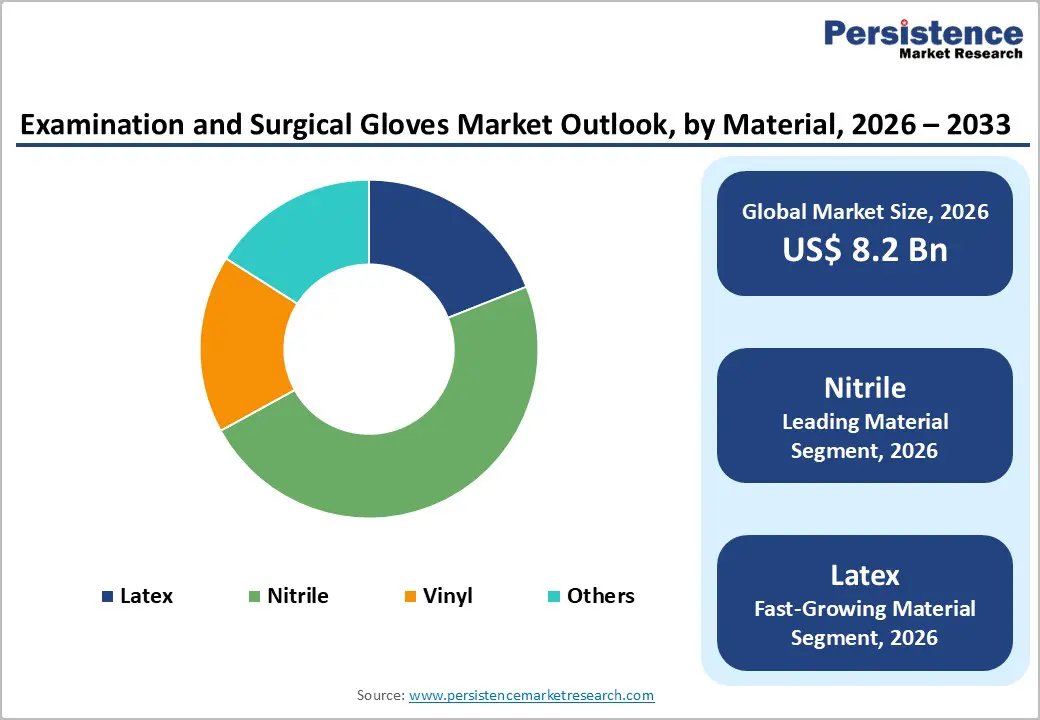

The global Examination and Surgical Gloves market size is expected to be valued at US$ 8.2 billion in 2026 and projected to reach US$ 13.5 billion by 2033, growing at a CAGR of 7.3% between 2026 and 2033.

The market demonstrates robust expansion driven by escalating healthcare-associated infection (HAI) incidence, heightened infection prevention compliance protocols mandated by regulatory bodies such as the FDA and OSHA, and surging global demand for disposable medical protective equipment. Hospital-acquired infections affect 7% of patients in high-income countries and up to 15% in low- and middle-income regions according to WHO, compelling healthcare facilities to strengthen infection control measures through consistent glove utilization across all clinical departments and procedures.

Key Market Highlights

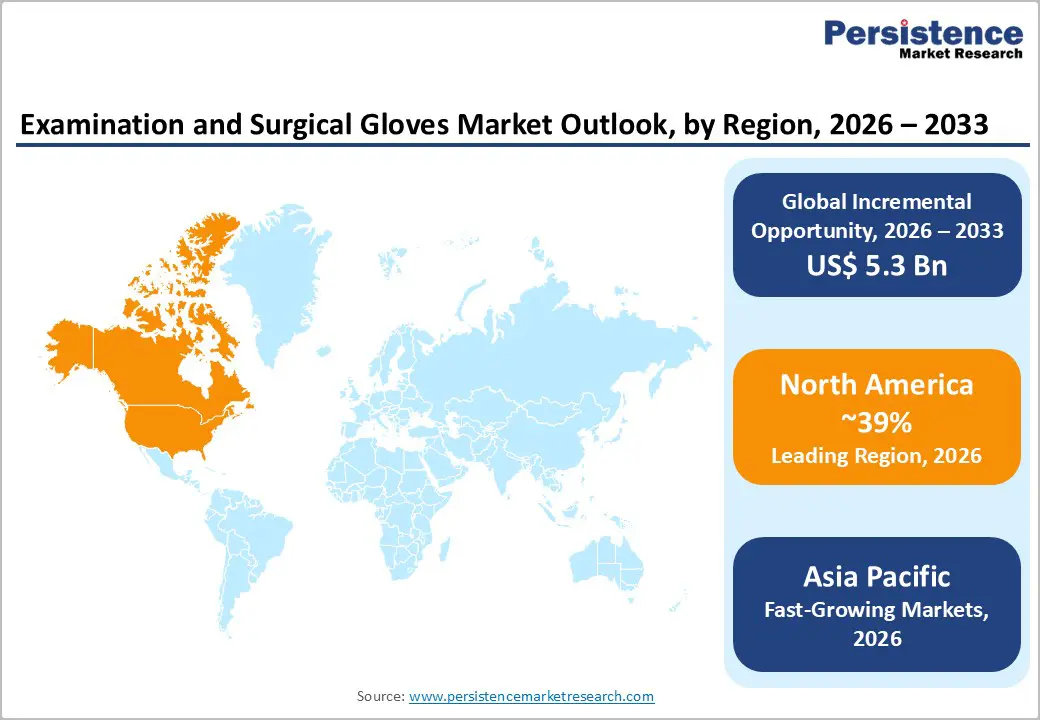

- Leading Region: North America leads the examination and surgical gloves market with 39% share in 2025, driven by advanced healthcare infrastructure, strict regulations, high surgical volumes, and strong local manufacturing.

- Fastest-Growing Region: Asia-Pacific is the fastest-growing region, supported by rapid healthcare expansion, rising diagnostic testing volumes (over 50 million tests per month in India), infection control initiatives, and manufacturing cost advantages.

- Dominant Segment: Nitrile gloves hold the largest share (48% in 2025) due to superior durability, allergy-free properties, cost efficiency, and widespread use across healthcare and laboratory settings.

- Fastest-Growing Segment: Latex gloves are the fastest-growing, driven by demand in precision and microsurgical procedures requiring high tactile sensitivity and premium applications.

- Key Opportunity: Expanding healthcare infrastructure and increasing diagnostic testing in Asia-Pacific, particularly in India, are creating strong, sustained demand for gloves across institutional and emerging consumer segments.

| Global Market Attributes | Key Insights |

|---|---|

| Market Size (2026E) | US$ 8.2 billion |

| Market Value Forecast (2033F) | US$ 13.5 billion |

| Projected Growth CAGR (2026-2033) | 7.3% |

| Historical Market Growth (2020-2025) | 6.8% |

Market Dynamics

Market Growth Drivers

Rising Prevalence of Hospital-Acquired Infections and Infection Prevention Mandates

Healthcare-associated infections represent a critical patient safety challenge, with estimates indicating 135,000 deaths annually in Europe attributed to HAI complications. Regulatory agencies including the Centers for Disease Control and Prevention (CDC), OSHA, and FDA have established stringent guidelines mandating glove usage across all clinical touchpoints involving potential pathogen exposure, bodily fluid contact, or contaminated surface handling. These regulatory frameworks create a non-negotiable baseline demand for medical gloves in hospital settings, clinics, ambulatory surgical centers, and diagnostic laboratories. Healthcare facilities face mandatory compliance requirements for glove use during examinations, surgical procedures, specimen collection, and patient care activities. Hospitals conducting high-volume procedural operations require substantial daily glove consumption, with staff performing dozens of examinations per shift, each necessitating fresh glove changes to prevent cross-contamination.

Expanding Healthcare Infrastructure and Increasing Surgical Procedure Volumes

Global healthcare capacity expansion, particularly in emerging markets, drives unprecedented demand for medical gloves across hospital networks, outpatient facilities, and diagnostic centers. India alone performs over 50 million diagnostic tests monthly in urban and rural laboratories combined, each requiring multiple glove changes throughout the testing process. Growth in elective surgeries, chronic disease management, and preventive care screenings creates sustained consumption across all end-user segments. The proliferation of ambulatory surgical centers offering same-day procedures contributes to decentralized glove demand patterns, with facilities maintaining independent procurement cycles and inventory management systems. Rising prevalence of chronic conditions including diabetes, cardiovascular disease, respiratory infections, and oncological disorders necessitates increased medical examinations, diagnostic procedures, and surgical interventions, collectively amplifying glove utilization across healthcare systems globally.

Market Restraints

Cost Pressures and Supply Chain Volatility Affecting Profit Margins

Glove manufacturing remains sensitive to fluctuating raw material costs, particularly nitrile butadiene rubber (NBR) feedstock prices, acrylonitrile, and butadiene commodity pricing, which have remained elevated since late 2023. Manufacturing cost increases directly compress profit margins for market participants, compelling competitive pricing strategies that intensify competition among established and emerging glove producers. Supply chain disruptions, including logistics delays and shipping cost escalation, amplify production expenses and inventory carrying costs. Price-sensitive healthcare procurement teams, particularly in public healthcare systems and developing nations, increasingly employ group purchasing organizations (GPOs) and centralized procurement mechanisms to negotiate lower unit costs, reducing pricing power for glove manufacturers and constraining overall market value growth despite volume expansion.

Regulatory Compliance Complexity and Quality Assurance Burdens

Medical glove manufacturers must navigate increasingly complex regulatory requirements including FDA 510(k) clearance processes, ISO 13485 quality management certification, ASTM performance testing protocols, and stringent biocompatibility validation procedures. Compliance costs associated with sterility validation, tensile strength testing, puncture resistance verification, and barrier performance documentation represent substantial ongoing operational expenses. FDA Import Alerts and product detention mechanisms create supply chain disruptions and revenue losses, requiring manufacturers to invest in regulatory consulting and compliance management infrastructure. The introduction of advanced regulatory requirements such as Unique Device Identifiers (UDI) and enhanced post-market surveillance obligations increases operational complexity for global manufacturers distributing across multiple jurisdictions with divergent regulatory frameworks.

Market Opportunities

Emerging Demand from Asia-Pacific Healthcare Expansion and Diagnostic Test Growth

Asia-Pacific represents the fastest-expanding regional market, driven by rapid hospital network expansion, rising medical tourism volumes, and substantially elevated diagnostic testing frequencies. China, India, Indonesia, and Vietnam continue scaling healthcare infrastructure investments, with India performing over 50 million monthly diagnostic tests across laboratory networks. Government initiatives promoting hygiene standards, infection prevention protocols, and public health infrastructure modernization accelerate glove adoption across public and private healthcare facilities. Local glove manufacturing capacity has expanded significantly in synthetic materials, improving product affordability and supply stability within the region. Rising medical tourism in Thailand, India, and Malaysia generates incremental glove demand from international patient volumes, while telemedicine expansion introduces consumer-direct glove distribution channels through home-health kits accompanying virtual care consultations. The region's manufacturing cost advantages and emerging production capabilities create opportunities for market participants to establish regional production hubs capturing supply chain efficiencies and reducing distribution costs.

Category-wise Insights

Product Type Analysis

Examination gloves represent the dominant product category, commanding approximately 63% market share in 2024, reflecting consistent utilization across daily patient care, routine health assessments, preventive examinations, and diagnostic activities. Examination gloves provide cost-effective barrier protection with economies of scale supporting continuous manufacturing processes and stable pricing despite feedstock volatility. The segment benefits from high-volume demand across outpatient clinics, primary care facilities, diagnostic laboratories, and emergency departments where examination gloves represent essential consumables for every patient interaction. Hospitals and clinics collectively conduct hundreds of millions of examinations annually, with staff performing dozens of glove changes per shift during triage assessments, blood draws, physical examinations, respiratory evaluations, and laboratory procedures. Expanding home-health services incorporating telemedicine support additionally introduce consumer-direct distribution channels for examination glove kits, creating emerging consumer segments beyond traditional institutional healthcare procurement. Surgical gloves, though representing a smaller market segment, demonstrate specialized application requirements necessitating sterility validation, enhanced barrier properties, and premium material specifications, supporting higher-margin positioning for market participants.

Material Analysis

Nitrile gloves maintain dominant market positioning with 48% market share in 2025, driven by superior durability, exceptional chemical and puncture resistance, broad-spectrum allergen-free formulation, and cost-effectiveness compared to natural latex alternatives. Nitrile's superior barrier properties against petroleum-based chemicals, biological fluids, and hazardous substances establish it as the preferred choice across medical, laboratory, and food-handling environments. Healthcare professionals increasingly adopt nitrile formulations due to widespread latex sensitivities affecting healthcare worker populations, with natural rubber latex allergens triggering Type I allergic reactions in sensitized individuals. Manufacturers are co-locating nitrile production facilities with glove factories to optimize supply chain efficiencies and insulate margins against volatile feedstock pricing. FDA Quality Management System Regulation updates catalyze broader adoption of materials with stable supply profiles and documented safety performance. Latex gloves retain niche positioning in microsurgical and specialized procedures requiring exceptional tactile fidelity and unmatched sensitivity, with latex commanding premium pricing in precision-intensive applications. Vinyl gloves represent the lowest-cost alternative for non-critical tasks, though weak barrier properties and limited chemical resistance restrict usage to quick-turn, lower-risk applications.

End-User Analysis

Hospitals emerge as the leading end-user segment, capturing approximately 47-48% market share in 2024, reflecting comprehensive procedural breadth, intensive daily glove consumption across emergency departments, surgical suites, intensive care units, and general medicine wards. Hospital integration with enterprise resource-planning systems enables real-time inventory monitoring and predictive analytics on glove consumption patterns, linking supply management to labor efficiency and staffing optimization. Hospital staff conduct extensive daily procedures including suturing assistance, IV line preparation, physical examinations, respiratory assessments, medication administration, and surgical interventions, each requiring consistent fresh glove changes to prevent cross-contamination.

Regional Insights

North America Examination and Surgical Gloves Market Trends and Insights

North America maintains dominant market positioning with 39% market share in 2025, driven by advanced healthcare infrastructure, rigorous regulatory oversight, and extensive surgical and diagnostic procedure volumes. The United States market represents the largest and most mature segment globally, supported by robust FDA regulatory frameworks emphasizing infection control, competitive marketplace dynamics encouraging product innovation, and widespread adoption of advanced surgical techniques. Healthcare facilities maintain substantial glove inventory levels reflecting 24/7 operational requirements across emergency departments, surgical centers, intensive care units, and diagnostic laboratories. Stringent OSHA guidelines and CDC infection prevention standards establish non-negotiable compliance baselines mandating glove usage across all patient-contact activities and contaminated surface handling.

Asia Pacific Examination and Surgical Gloves Market Trends and Insights

Asia-Pacific emerges as the fastest-growing regional market at the highest CAGR during 2025-2032, driven by rapid healthcare infrastructure expansion, rising infectious disease prevalence, and substantially elevated diagnostic testing volumes. China, Japan, India, Indonesia, and Vietnam continue implementing aggressive healthcare system modernization initiatives, scaling hospital networks, diagnostic laboratory capacity, and clinical service infrastructure. India performs over 50 million diagnostic tests monthly across urban and rural laboratory networks combined, each generating consistent multi-pair glove consumption throughout specimen collection, processing, and analysis workflows. Government-led public health initiatives promoting hygiene standards, infection prevention protocols, vaccination programs, and maternal-child healthcare services accelerate glove adoption across institutional and community-level healthcare delivery.

Competitive Landscape

Market Structure Analysis

The examination and surgical gloves market is highly competitive and characterized by a mix of large-scale manufacturers and regional suppliers. Competition is primarily driven by pricing, product quality, material innovation, and production capacity. Manufacturers focus on expanding nitrile and powder-free glove portfolios to meet rising infection-control standards and reduce allergy risks. Continuous investments in automation, capacity expansion, and sustainable manufacturing practices are strengthening cost efficiency and supply reliability. Regulatory compliance, certifications, and long-term supply contracts with healthcare providers play a crucial role in maintaining market position.

Key Market Developments

- In May 2025, Hyderabad-based Wadi Surgicals launched the accelerator-free nitrile gloves under its flagship brand, Enliva. Developed through extensive research and development efforts and global collaborations, these gloves became India’s first accelerator-free nitrile gloves, marking a significant advancement in skin-safe and allergy-free hand protection.

Companies Covered in Examination and Surgical Gloves Market

- Top Glove Corporation Bhd

- Ansell Limited

- Hartalega Holdings Berhad

- Kossan Rubber Industries Bhd

- Supermax Corporation Berhad

- Medline Industries, Inc.

- Cardinal Health, Inc.

- Semperit AG Holding

- Kimberly-Clark Corporation

- INTCO Medical

- Dynarex Corporation

- B. Braun Melsungen AG

Frequently Asked Questions

The global market is currently valued at around US$ 7.3 Bn in 2022.

Sales of the market are set to witness a high growth at a CAGR of 7.3% and be valued at around US$ 15.9 Bn by 2033.

Demand for the market increased at a 6.5% CAGR from 2015 to 2022.

The U.S., Germany, Canada, U.K., and France account for most demand for examination and surgical gloves, currently holding around 59.1% market share.

The U.S. accounts for around 86.5% share of the North American market in 2022.

Latin America accounts for around 5.8% share of the global market in 2022.

The China market held a share of about 39.8% in the East Asia examination and surgical gloves market in 2022.

The Germany market is set to expand at a 7.8% CAGR over the forecast period.

The Brazil market is expected to grow at a 9.3% CAGR during the forecast period.

The market in India is set to expand at an 8.9% CAGR over the forecast period.