- Medical Devices

- Surgical Helmet System Market

Surgical Helmet System Market Size, Share, and Growth Forecast 2026 - 2033

Surgical Helmet System Market by Product (Without LED, With LED), by End User (Hospitals, Ambulatory Surgical Centers, Academic & Research Institutes), by Regional Analysis, 2026-2033

Surgical Helmet System Market Size and Trend Analysis

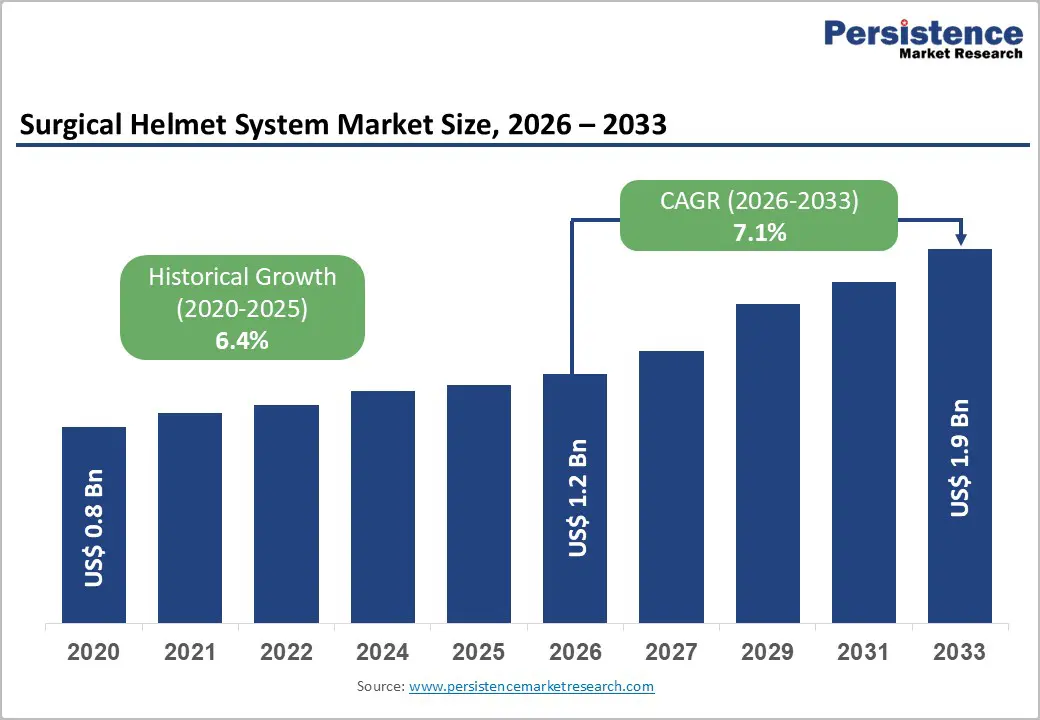

The global surgical helmet system market size is expected to be valued at US$ 1.2 billion in 2026 and projected to reach US$ 1.9 billion by 2033, growing at a CAGR of 7.1% between 2026 and 2033.

Surgical helmet systems are specialized protective devices widely used in orthopedic and trauma surgeries to reduce the risk of surgical site contamination and protect surgeons from blood splashes and airborne pathogens. Their importance increased significantly during the COVID-19 pandemic, as studies highlighted their potential role in minimizing microorganism transmission in operating rooms. With surgeries emerging as a major contributor to global disease burden, healthcare providers are increasingly adopting advanced protective equipment to improve safety standards and working conditions for medical professionals.

Technological advancements have reshaped the surgical helmet system market, transforming basic protective gear into sophisticated systems with cooling fans, battery-powered operation, LED lighting, and integrated cameras. Growing orthopedic procedure volumes, especially hip and knee replacements among aging populations, are further driving adoption. Increasing investments in research and development and a focus on durable, customizable solutions are expected to support continued market growth globally.

Key Market highlights

- The surgical helmet system with LED segment is projected to hold around 71% share in 2026, driven by enhanced illumination, durability, and increased adoption in orthopedic surgeries.

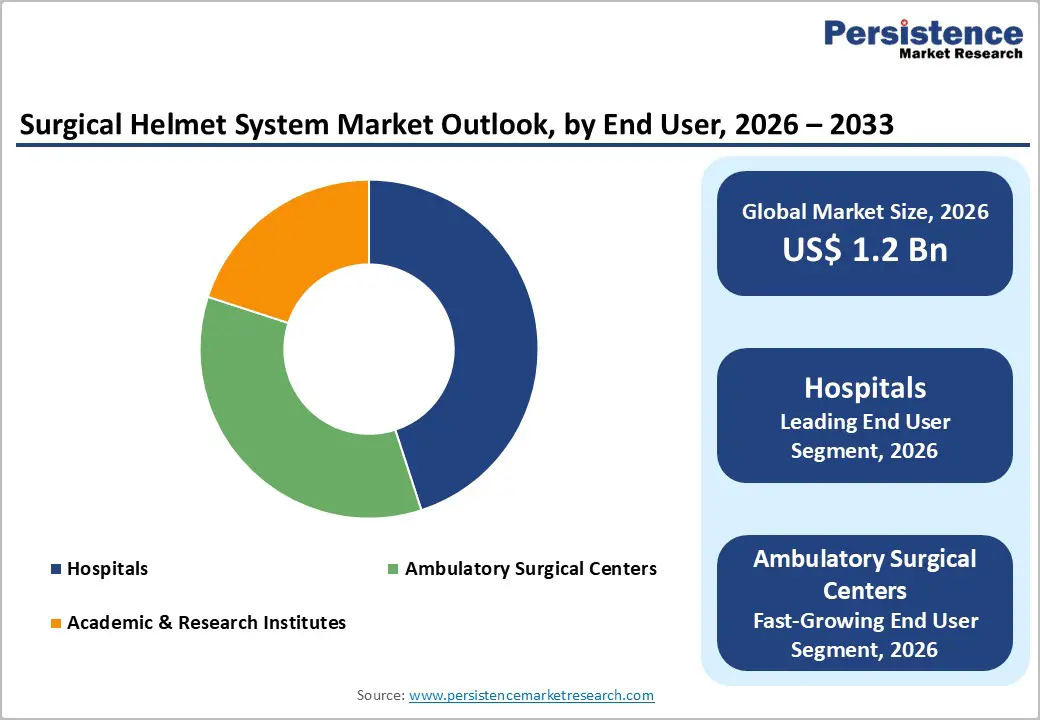

- Hospitals are expected to account for approximately 45% share in 2026, due to high surgical volumes, expanding orthopedic and trauma procedures, and strict infection control protocols.

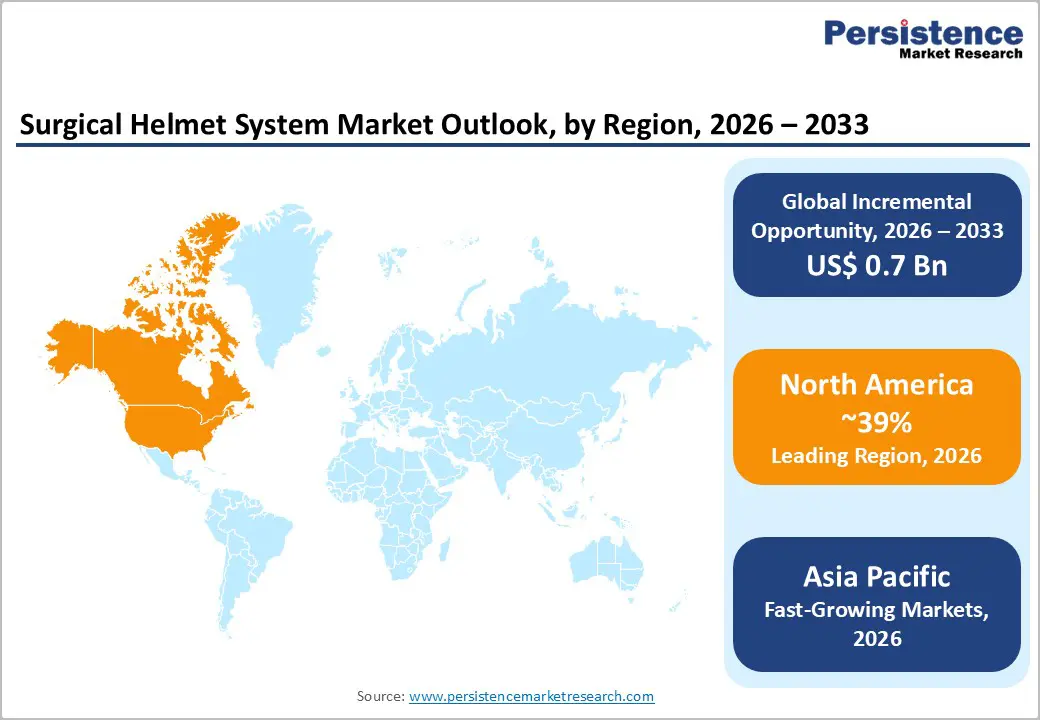

- North America is anticipated to dominate with an estimated 42% market share in 2026, supported by advanced healthcare infrastructure, high surgical volumes, and ongoing research and development in protective equipment.

- Modern surgical helmet systems are increasingly equipped with LED lights, cooling fans, battery operation, and integrated cameras, improving surgeon comfort, visibility, and operational efficiency.

- Surgical helmet systems are essential in orthopedic and trauma surgeries to protect surgeons from blood splashes, reduce surgical site contamination, and enhance overall patient and staff safety.

| Report Attribute | Details |

|---|---|

|

Surgical Helmet System Market Size (2026E) |

US$ 1.2 billion |

|

Market Value Forecast (2033F) |

US$ 1.9 billion |

|

Projected Growth CAGR (2026-2033) |

7.1% |

|

Historical Market Growth (2020-2025) |

6.4% |

Market Dynamics

Driver- Rising Orthopedic and Trauma Procedures

The global surgical helmet system market is primarily driven by the growing volume of orthopedic and trauma procedures worldwide. The increasing prevalence of musculoskeletal disorders, coupled with aging populations, has significantly accelerated demand for joint replacement surgeries such as hip and knee arthroplasties. Globally, an estimated 278 million people are affected by musculoskeletal conditions, creating sustained procedural demand. Elective orthopedic surgeries continue to rise as life expectancy improves and patients seek enhanced mobility and quality of life. Surgical helmet systems play a critical role in these procedures by providing protection against bone cement aerosols and surgical contaminants, particularly in high-risk orthopedic and trauma operating environments.

In addition to infection control, ergonomic advantages are contributing to market growth. Advanced helmet systems are designed to improve surgeon comfort, reduce fatigue, and enhance visibility during prolonged surgical procedures. Studies indicate that improved ergonomics can extend surgeon endurance by approximately 20% in lengthy operations, directly supporting procedural efficiency and patient outcomes. In the U.S. alone, nearly one million arthroplasty procedures are performed annually, as reported by the American Academy of Orthopaedic Surgeons (AAOS). The increasing emphasis on operating room safety standards and surgeon well-being continues to reinforce demand for ventilated surgical helmet systems across hospitals and trauma centers.

Restraint- High cost of surgical helmets to limit market growth

The high cost of surgical helmet systems remains a significant restraint, particularly in low- and middle-income countries. Limited healthcare budgets, inadequate hospital infrastructure, and shortages of trained orthopedic specialists restrict the adoption of advanced protective equipment. Many healthcare systems struggle to provide even basic orthopedic care, making investments in high-cost personal protective equipment challenging. In underdeveloped regions, the lack of awareness and training regarding surgical helmet systems further reduces adoption, despite rising surgical site infection risks.

Cost-related challenges extend beyond initial purchase expenses. Reusable surgical helmets require regular cleaning, sterilization, and maintenance, increasing operational costs, while disposable helmets add recurring expenditure. Small hospitals and ambulatory surgical centers often find these costs prohibitive. Additionally, limited access to validated clinical data linking helmet use to reduced infection rates has slowed widespread acceptance. Existing studies are often based on small patient populations and focus on specific infection types, limiting their general applicability. The availability of alternative infection control methods, such as enhanced operating room ventilation and standard PPE, further discourages adoption. Collectively, affordability constraints, insufficient infrastructure, and limited clinical evidence continue to restrict market growth in resource-constrained healthcare settings.

Opportunity- Expansion in Emerging Healthcare Markets

Emerging healthcare markets present a strong growth opportunity for the surgical helmet system market. Rapid expansion of hospital infrastructure, increasing surgical volumes, and improving access to orthopedic care in developing economies are creating favorable conditions for market entry. Governments and private healthcare providers in Asia-Pacific, Latin America, and parts of the Middle East are investing in modern operating room facilities and infection control standards. These initiatives are gradually increasing awareness of advanced protective systems among surgeons and hospital administrators.

Additionally, the development of cost-effective and lightweight surgical helmet systems tailored for resource-limited settings can significantly expand adoption. Manufacturers focusing on modular designs, affordable materials, and simplified maintenance requirements can address key barriers in emerging markets. Rising medical tourism, particularly for orthopedic and trauma procedures, further strengthens demand for internationally accepted safety standards. As infection prevention gains priority and surgical volumes continue to rise, especially in tertiary and specialty hospitals, surgical helmet systems have strong potential to transition from optional equipment to standard operating room protection in developing regions.

Category-wise Insights

Product Type Analysis

The surgical helmet system with LED accounted for approximately 71% of the global market share in 2025, reflecting strong demand for enhanced visibility and safety in operating rooms. These helmets are equipped with built-in LED lights positioned at the front, enabling surgeons to achieve focused and consistent illumination during complex surgical procedures. Improved lighting reduces dependency on overhead operating room lights and helps surgeons maintain clear visibility in deep or confined surgical fields. This is particularly important in orthopedic and trauma surgeries, where precision and accuracy are critical.

The dominance of this segment is further supported by continuous product innovation and strategic focus by key manufacturers. Modern LED-equipped helmets are designed for durability, long operational life, and reliability during emergency procedures. Their robust construction ensures uninterrupted performance in high-pressure surgical environments. Additionally, LEDs contribute to energy efficiency and reduced heat generation, enhancing user comfort during lengthy procedures. As hospitals increasingly prioritize advanced surgical tools that improve efficiency and safety, LED-based surgical helmet systems continue to drive growth and maintain leadership in the global market.

End User Analysis

Hospitals are expected to account for approximately 45% of the global surgical helmet system market share in 2026, making them the leading end-user segment. The growing number of hospitals and specialized healthcare facilities dedicated to orthopedic and trauma care has significantly increased access to surgical procedures worldwide. Rising incidence of road accidents, sports injuries, and age-related musculoskeletal disorders has led to a higher demand for orthopedic surgeries, most of which are performed in hospital settings.

Hospitals handle a large volume of complex surgical procedures that require strict infection control measures and advanced protective equipment for surgical teams. The need for different types of surgical helmet systems across various departments further supports market growth. Additionally, hospitals are more likely to invest in technologically advanced and durable surgical helmets due to higher patient throughput and regulatory compliance requirements. Continuous expansion of hospital infrastructure and increasing surgical volumes are expected to sustain strong demand from this end-user segment globally.

Regional Insights

North America Surgical Helmet System Market Trends and Insights

North America represents a mature and technology-driven market for surgical helmet systems, with the U.S. accounting for approximately 32.0% of the global market share in 2025. The region benefits from a well-established healthcare infrastructure, high surgical volumes, and strict operating room safety standards. Continuous investments in healthcare facilities and the availability of trained medical professionals support the adoption of advanced protective equipment during complex procedures, particularly in orthopedic and trauma surgeries.

The U.S. market growth is strongly supported by ongoing innovation and research and development activities in surgical helmet technologies. The presence of local manufacturers, increasing funding for product development, and frequent introduction of advanced features such as improved ventilation and enhanced visibility contribute to market expansion. In addition, the growing focus on surgeon safety, infection prevention, and ergonomic comfort during lengthy procedures continues to drive demand. These factors collectively position North America as a key revenue-generating region for the surgical helmet system market.

Europe Surgical Helmet System Market Trends and Insights

Europe remains an important regional market for surgical helmet systems, supported by rising orthopedic procedure volumes and growing emphasis on healthcare worker safety. The UK held approximately 9.9% of the global market share in 2025, reflecting steady adoption across hospitals and surgical centers. Increasing demand for elective procedures, including total hip and knee replacements, is a key contributor to market growth across the region.

Healthcare systems in Europe place strong emphasis on patient safety and surgeon comfort, encouraging the use of protective equipment during complex surgical procedures. Awareness regarding occupational hazards faced by surgeons, including exposure to blood splashes and airborne contaminants, has further strengthened adoption. Additionally, supportive regulatory frameworks and public healthcare funding enable hospitals to invest in advanced surgical equipment. As aging populations drive orthopedic surgery demand and hospitals continue to modernize operating rooms, Europe is expected to maintain consistent growth in the surgical helmet system market.

Asia Pacific Surgical Helmet System Market Trends and Insights

Asia Pacific is emerging as a high-potential market for surgical helmet systems, with China accounting for around 12.4% of the global market share in 2025. Rapid expansion of healthcare infrastructure, rising awareness of surgical safety, and increasing volumes of orthopedic procedures are key factors driving regional growth. Countries such as China are experiencing higher demand for joint replacement and trauma surgeries due to aging populations, urbanization, and increased accident rates.

Hospitals represent the most lucrative end-user segment in the region, as large public and private healthcare facilities perform the majority of complex surgical procedures. Growing investments in hospital modernization and infection control practices are supporting adoption of advanced protective systems. China’s strong focus on technological development and manufacturing capabilities also positions the country as a source of innovative and cost-effective surgical helmet solutions. Overall, improving access to healthcare services and rising safety standards are expected to sustain market growth across Asia Pacific.

Competitive Landscape

Market Structure Analysis

The fact that there are numerous active businesses demonstrates how fiercely competitive the market for surgical helmet systems is. The major industry players are employing various techniques to acquire a competitive edge in this situation. The primary goal of this strategy is to raise the standard of the products they provide. The desire among many businesses in supplying durable, personalized items as well as innovative products is growing.?

Key Market Developments

- In March 2025, Stryker, a global medical technology leader, announced the launch of its latest personal protective equipment, the Steri-Shield 8 Personal Protection System. The system was developed over several years through extensive research, testing, and collaboration with frontline users.

- In May 2024, MAXAIR Systems unveiled the CAPR SHS Advanced Surgical Helmet System at AORN 2024, showcasing improved filtration technology.

Companies Covered in Surgical Helmet System Market

- Zimmer Biomet

- Stryker

- Beijing ZKSK Technology Co., Ltd.

- Kaiser Technology Co., Ltd.

- THI Total Healthcare Innovation GmbH

- MAXAIR Systems

- AresAir

- Regal Healthcare

- Vizbl brand products (Prodancy Pvt. Ltd.)

- Apex Hygiene Products

- Cardinal Health

- Integra LifeSciences Corporation

- Others

Frequently Asked Questions

The global surgical helmet system market is valued at US$ 1.2 billion in 2026.

Rising orthopedic surgeries, infection control needs, surgeon safety requirements, and growing adoption of advanced operating room protection systems.

North America leads with 39% share in 2025.

Expansion in emerging healthcare markets through affordable, technologically advanced surgical helmet systems supporting rising surgical volumes.

Zimmer Biomet, Stryker, Beijing ZKSK Technology Co., Ltd., Kaiser Technology Co., Ltd., THI Total Healthcare Innovation GmbH, and MAXAIR Systems.