- Medical Devices

- Orthopedic Surgical Robots Market

Orthopedic Surgical Robots Market Size, Share, and Growth Forecast, 2026 - 2033

Orthopedic Surgical Robots Market by Application (Spine Surgery, Others), Product Type (Robotic Systems, Others), End-user (Hospitals, Orthopedic Specialty Centers, Ambulatory Surgical Centers (ASCs), Others), and Regional Analysis for 2026 - 2033

Orthopedic Surgical Robots Market Share and Trends Analysis

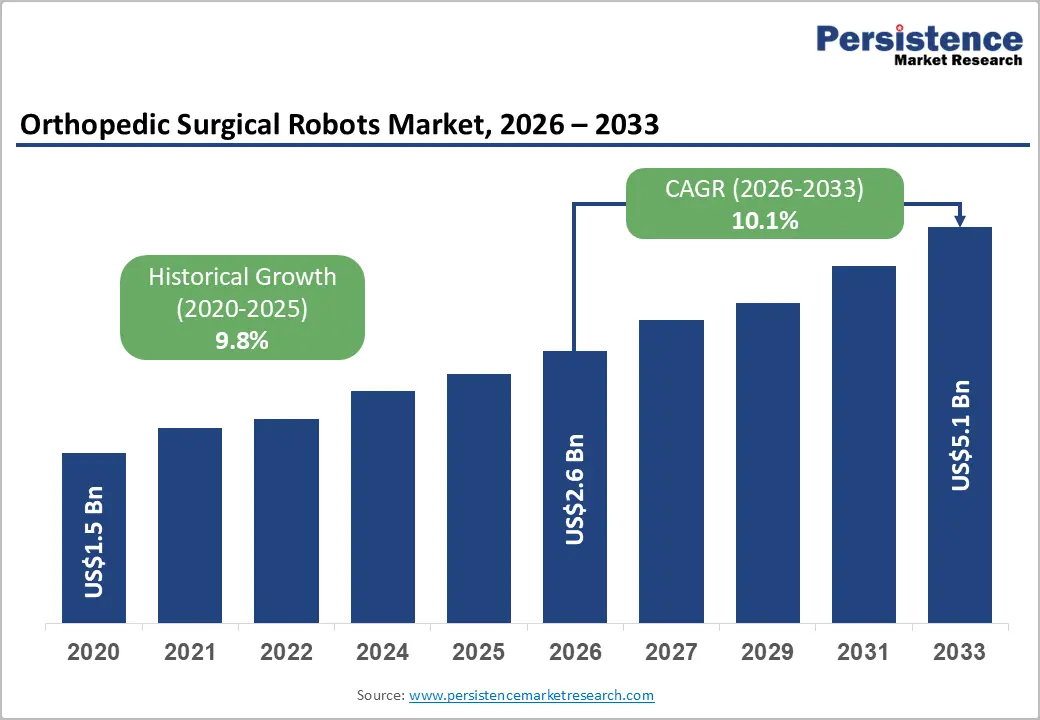

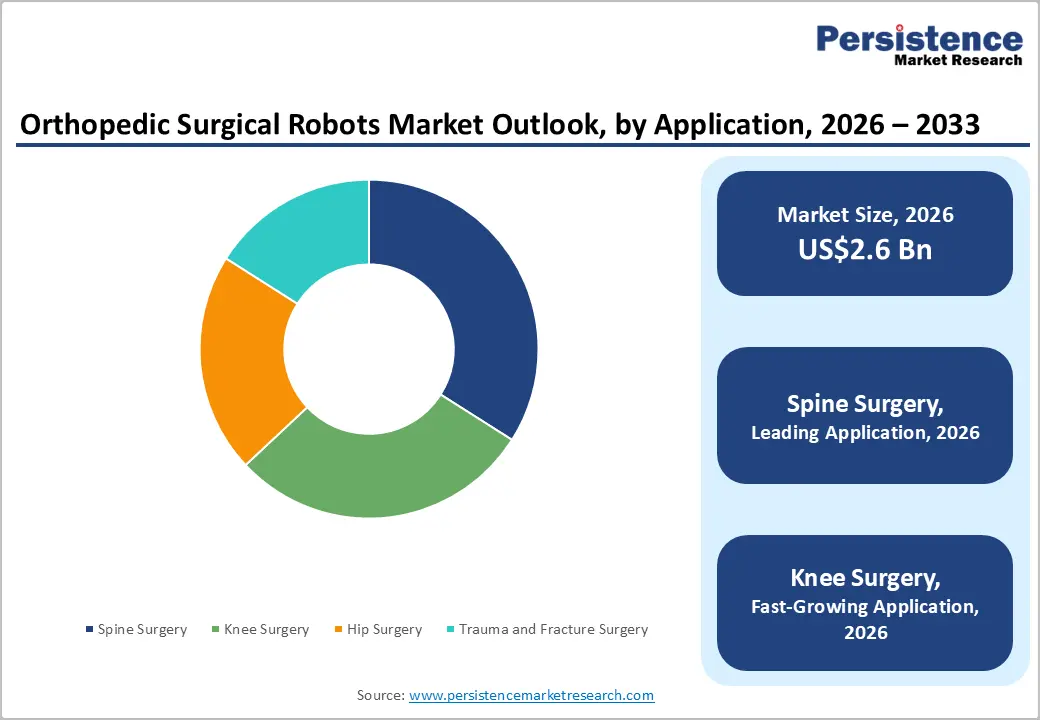

The global orthopedic surgical robots market size is likely to be valued at US$2.6 billion in 2026 and is projected to reach US$5.1 billion by 2033, growing at a CAGR of 10.1% during the forecast period from 2026 to 2033, driven by the rising orthopedic procedure volumes, increasing adoption of robotic orthopedic surgery, and growing demand for precision-driven minimally invasive interventions.

Aging demographics, higher incidence of osteoarthritis and spinal disorders, and continuous advancements in AI-powered orthopedic surgical robots are accelerating hospital investments globally. In addition, healthcare systems are prioritizing surgical efficiency, shorter recovery timelines, and improved implant positioning accuracy, strengthening long-term demand for smart orthopedic surgery platforms and robotic-assisted orthopedic workflows.

Key Industry Highlights:

- Leading Application Segment: Spine surgery is expected to hold around 34% of the market share in 2026, while knee surgery is projected to grow the fastest at a CAGR of 10.4% through 2033, driven by rising robotic-assisted joint replacement procedures.

- Dominant Product Type: Robotic systems are anticipated to account for nearly 41% of revenue share in 2026, whereas surgical planning software is likely to witness the fastest growth at 10.3% CAGR during 2026 - 2033 due to increasing AI-based workflow integration.

- Leading End-user: Hospitals are projected to dominate with an estimated 56% share in 2026, while Ambulatory Surgical Centers (ASCs) are expected to register the fastest growth at 10.7% CAGR through 2033, supported by rising outpatient orthopedic surgeries.

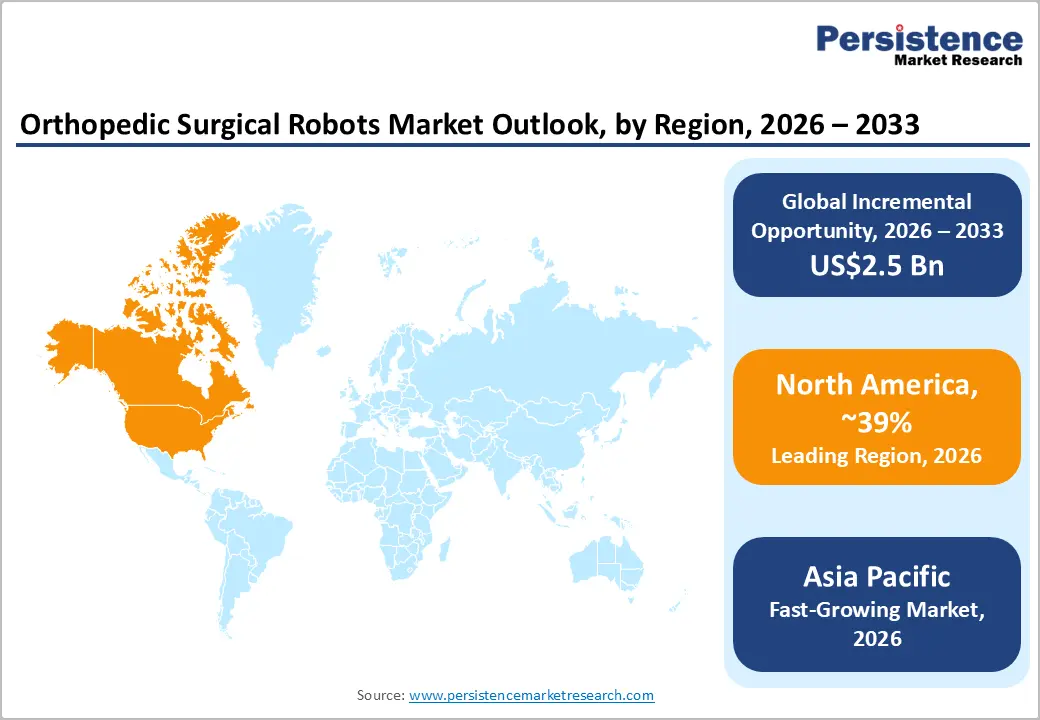

- Regional Leadership: North America is poised to lead with approximately 39% market share in 2026, while Asia Pacific is forecast to expand at the fastest CAGR of 10.5% from 2026 to 2033, driven by healthcare modernization in China and India.

- Competitive Environment: Competitive activity is centered on AI-enabled navigation, robotic platform expansion, surgeon training partnerships, and regional commercialization strategies across Asia Pacific and Europe.

DRO Analysis

Driver - Rising Burden of Degenerative Bone Disorders and Demand for Precision-Based Surgery

The growing prevalence of musculoskeletal disorders is a key factor driving growth in the orthopedic surgical robots market. According to the World Health Organization (WHO), nearly 1.71 billion people globally are affected by musculoskeletal conditions, while the U.S. Centers for Disease Control and Prevention (CDC) estimates that around 53 million adults in the U.S. live with arthritis-related disorders. Rising cases of knee osteoarthritis, spinal degeneration, and hip disorders are significantly increasing orthopedic surgical volumes worldwide.

This expanding patient population is accelerating demand for robotic joint replacement systems and precision-driven orthopedic procedures. Hospitals are increasingly adopting robotic platforms to improve implant alignment accuracy, reduce revision surgeries, and support minimally invasive interventions with faster patient recovery. Growing emphasis on surgical efficiency, standardized outcomes, and advanced imaging integration continues to strengthen the adoption of robotic-assisted orthopedic technologies across healthcare systems.

Restraint - High Costs and Complex System Integration

The market faces significant barriers due to the high cost of robotic-assisted surgical systems. Hospitals must invest heavily in robotic hardware, imaging systems, navigation software, maintenance, and surgeon training programs. According to the American Hospital Association (AHA), the total lifecycle cost of robotic surgical platforms can reach several million dollars, limiting adoption among mid-sized hospitals and ambulatory surgical centers, especially in price-sensitive markets.

The market also faces operational and regulatory challenges during implementation. Integration of robotic systems often requires operating room modifications, software interoperability upgrades, and specialized workforce training, increasing deployment timelines. In addition, regulatory approvals from agencies such as the U.S. Food and Drug Administration (FDA) and the European Medicines Agency (EMA) can delay product commercialization. Limited reimbursement support and uncertain return on investment continue to slow adoption across smaller healthcare facilities.

Opportunity - Expansion of AI-Driven Robotics and Emerging Market Adoption

The market is witnessing strong opportunities through the rapid integration of AI-powered surgical planning, robotic navigation systems, and smart imaging technologies. Hospitals are increasingly adopting data-driven platforms to improve precision in spine and joint surgeries. The shift toward smart orthopedic surgery platforms is enhancing procedural accuracy, reducing revision rates, and improving surgical efficiency. This is significantly strengthening demand for next-generation robotic-assisted orthopedic solutions.

Another major growth opportunity lies in the successful adoption of advanced technologies such as cloud-connected robotics, real-time 3D imaging, and AI-assisted decision support tools across leading healthcare systems in the U.S., Europe, Japan, and South Korea. Asia Pacific, Latin America, and the Middle East are also emerging as high-growth regions due to rapid healthcare infrastructure upgrades and rising surgical volumes. Increasing deployment of robotic systems in China and India, supported by hospital expansion and medical tourism, is expected to drive strong long-term market growth.

Category-wise Analysis

Application Insights

Spine surgery is estimated to lead the market with around 34% share in 2026, as it remains highly dependent on precision-based navigation, where robotic systems significantly improve accuracy and consistency. The spine surgery robotics market is gaining traction due to its ability to reduce screw misplacement risk, radiation exposure, and revision surgeries. Hospitals are increasingly standardizing robotic workflows for complex spinal fusion and deformity correction procedures, making spine applications the most established segment.

Knee surgery is projected to be the fastest-growing segment, expected to expand at nearly 10.4% CAGR through 2033, supported by rising osteoarthritis prevalence and growing demand for accurate implant alignment. Adoption of knee replacement surgical robots is increasing as patients and providers prioritize faster recovery and improved post-surgical outcomes. The shift toward same-day discharge knee procedures in markets such as the United States and select Asian economies is further accelerating procedure volumes.

Product Type Insights

Robotic systems are estimated to dominate the market with about 41% share in 2026, as they represent the core infrastructure enabling robotic-assisted orthopedic procedures. Their integrated design combining imaging, navigation, and robotic articulation enhances surgical precision and workflow efficiency. Hospitals are increasingly investing in full-suite robotic platforms rather than fragmented solutions, reinforcing system-level adoption across orthopedic departments.

Surgical planning software is expected to be the fastest-growing segment, projected to grow at nearly 10.3% CAGR through 2033, driven by increasing reliance on AI-based preoperative planning. Its role is expanding as surgeons adopt digital tools for patient-specific implant positioning and procedural optimization. Growing integration with robotic systems is making it a critical layer in improving surgical accuracy and reducing intraoperative variability.

End-user Insights

Hospitals are estimated to hold the largest share at around 56% in 2026, supported by strong infrastructure, high surgical volumes, and better access to capital-intensive robotic systems. They continue to lead adoption due to their ability to integrate robotics into complex orthopedic workflows, particularly for spine and joint procedures. This makes hospitals the primary center for robotic surgical expansion globally.

Ambulatory surgical centers are projected to be the fastest-growing end-user segment, expanding at nearly 11.7% CAGR through 2033, driven by the shift toward outpatient orthopedic procedures. Robotic-assisted minimally invasive surgeries are enabling faster recovery and same-day discharge models, improving operational efficiency. Increasing patient preference for lower-cost, quicker-care settings is accelerating the adoption of robotic systems in ASCs.

Regional Analysis

North America Orthopedic Surgical Robots Market Trends

North America is estimated to lead the orthopedic surgical robots market with around 39% global share in 2026, making it the most mature and high-adoption regional market. The region shows strong integration of robotic-assisted knee and spine procedures, supported by advanced hospital infrastructure and high surgical volumes. The adoption of robotic orthopedic surgery is largely standardized in leading healthcare systems, where robotics is increasingly used for routine joint replacement and complex spinal cases.

U.S. Orthopedic Surgical Robots Market Trends

The U.S. is estimated to account for nearly 75% of the regional share in 2026, driven by the large-scale deployment of robotic knee arthroplasty and spine navigation systems across major hospital networks. Recent expansion is estimated in the increased adoption of robotic-assisted total knee replacement programs across large integrated hospital groups and academic medical centers, where robotics is being embedded into standard orthopedic surgical pathways. This reflects a shift toward routine, protocol-based use of robotic systems in joint reconstruction.

Canada Orthopedic Surgical Robots Market Trends

Canada is estimated to hold about 10% regional share in 2026, with adoption concentrated in major tertiary hospitals in provinces such as Ontario and British Columbia. Recent upgrades are estimated in hospital surgical departments where advanced imaging-integrated navigation systems are being introduced to support robotic-assisted knee and spine procedures. Adoption remains selective and center-driven, indicating gradual but steady market penetration.

Europe Orthopedic Surgical Robots Market Trends

Europe is estimated to account for around 27% of the global market in 2026, reflecting a structured and steadily expanding adoption environment for orthopedic robotic systems. Growth is supported by rising orthopedic procedure volumes, aging populations, and increasing emphasis on surgical precision in knee and spine procedures. The region is gradually integrating robotic systems into orthopedic departments across advanced hospital networks.

Germany Orthopedic Surgical Robots Market Trends

Germany is estimated to lead with around 28% regional market share in 2026, supported by strong adoption of robotic-assisted orthopedic systems in university hospitals and specialized orthopedic centers. Recent expansion is estimated in the increased utilization of navigation-guided robotic spine surgery systems in tertiary care hospitals for complex spinal reconstruction procedures. This reflects deeper integration of robotic precision tools into high-acuity orthopedic workflows.

U.K. Orthopedic Surgical Robots Market Trends

The U.K. is estimated to hold about 18% regional market share in 2026, driven by efficiency-focused adoption under public healthcare systems. Recent expansion is estimated in robotic-assisted knee replacement programs across selected high-volume NHS orthopedic centers aimed at reducing surgical backlogs and improving procedural consistency. Adoption remains targeted, with emphasis on throughput optimization and outcome improvement.

Asia Pacific Orthopedic Surgical Robots Market Trends

Asia Pacific is estimated to be the fastest-growing region, contributing around 22% global share in 2026, and is currently in a strong expansion phase of orthopedic robotics adoption. Growth is driven by rising orthopedic disease burden, rapid healthcare infrastructure development, and increasing demand for smart orthopedic surgery platforms. The region is transitioning from early adoption to broader deployment across major hospital networks.

China Orthopedic Surgical Robots Market Trends

China is estimated to hold around 40% of the regional market in 2026, driven by the rapid installation of robotic-assisted spine and knee surgery systems across large tertiary hospitals. Recent expansion is estimated in the wider deployment of robotic surgical units in tier-1 and tier-2 city hospitals, where orthopedic departments are increasingly integrating robotics into routine surgical workflows. This indicates strong system-level scaling of robotic adoption.

India Orthopedic Surgical Robots Market Trends

India is estimated to account for around 15% of the regional market in 2026, with adoption concentrated in leading private hospital chains across major metropolitan cities. Recent expansion is estimated in the introduction of robotic-assisted joint replacement programs in premium orthopedic centers, driven by rising demand for minimally invasive procedures and medical tourism inflows. This reflects an early but rapidly accelerating adoption curve.

Competitive Landscape

The orthopedic surgical robots market is moderately consolidated, led by Stryker, Zimmer Biomet, Medtronic, and Smith+Nephew, which dominate through established robotic platforms and strong hospital networks. Their advantage lies in integrated ecosystems combining robotics, imaging, and AI-powered orthopedic surgical robots with long-term service contracts. Continuous upgrades and installed base expansion further strengthen their market position. Competition is largely driven by platform integration rather than standalone devices.

Specialized players such as Globus Medical, Brainlab, and THINK Surgical focus on spine robotics, navigation, and surgical planning innovation. High entry barriers persist due to regulatory approvals, capital costs, and training requirements. However, demand for minimally invasive orthopedic robotics market solutions is attracting niche innovation and new entrants. Growing hospital partnerships and technology integration are expected to gradually intensify competition and drive consolidation.

Key Industry Developments:

- In September 2025, Globus Medical expanded robotic spine surgery capabilities through advanced imaging integration and intraoperative navigation enhancements. The company focused on strengthening its footprint in the spine surgery robotics market.

- In January 2025, Stryker expanded its Mako robotic platform capabilities through enhanced AI-assisted surgical planning features designed for complex knee and hip replacement procedures. The development strengthened the company’s position within the robotic joint replacement systems segment.

Companies Covered in Orthopedic Surgical Robots Market

- Stryker Corporation

- Zimmer Biomet Holdings

- Smith+Nephew

- Medtronic plc

- Globus Medical

- Johnson & Johnson MedTech

- NuVasive

- Brainlab AG

- Corin Group

- THINK Surgical

- OMNIlife Science

- Asensus Surgical

- Renishaw plc

- Curexo Inc.

Frequently Asked Questions

The global orthopedic surgical robots market is estimated to reach US$2.6 billion in 2026.

Rising orthopedic procedure volumes and demand for precision-based minimally invasive surgeries drive the market.

The market is projected to grow at a CAGR of 10.1% from 2026 to 2033.

Growth is driven by AI-enabled surgical planning, outpatient orthopedic expansion, and adoption in emerging healthcare systems.

Key players include Stryker, Zimmer Biomet, Medtronic, Smith+Nephew, Globus Medical, Brainlab, and THINK Surgical.