- Renewable Energy

- Smart Grid Market

Smart Grid Market Trends, Size, Share, Growth, Forecasts, 2025 - 2032

Smart Grid Market By Component (Software, Hardware, Services), Application (Transmission Grid, Distribution Grid, Generation Grid, Others) Communication Technology (Wired, Wireless), End-user (Residential, Others), and Regional for 2025 - 2032

Smart Grid Market Share and Trends Analysis

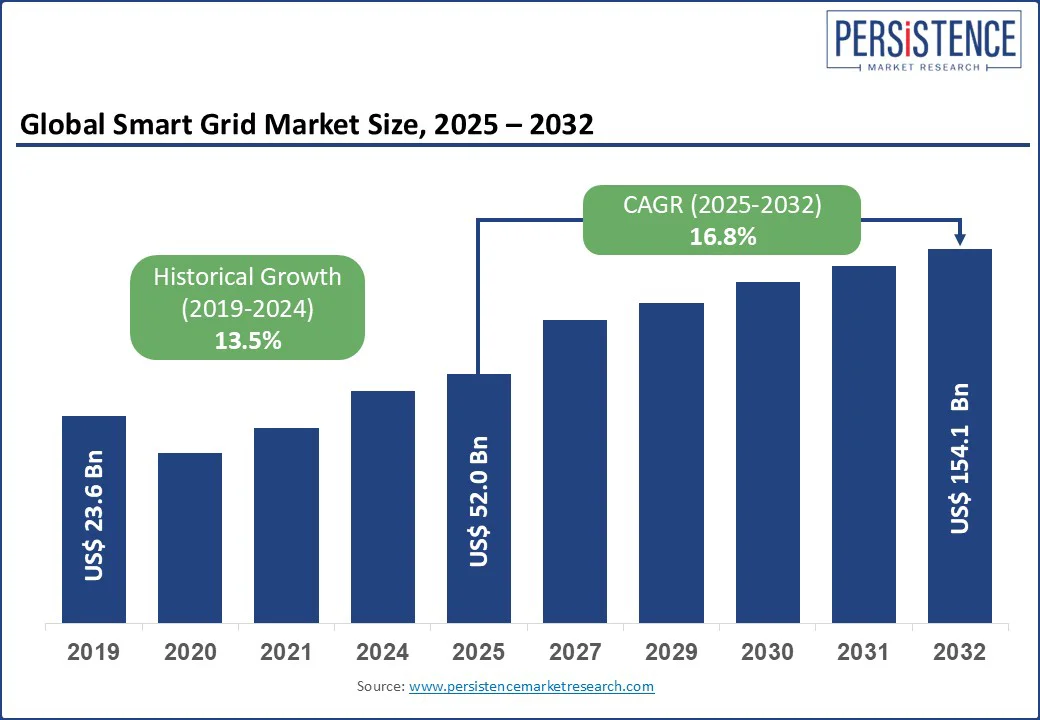

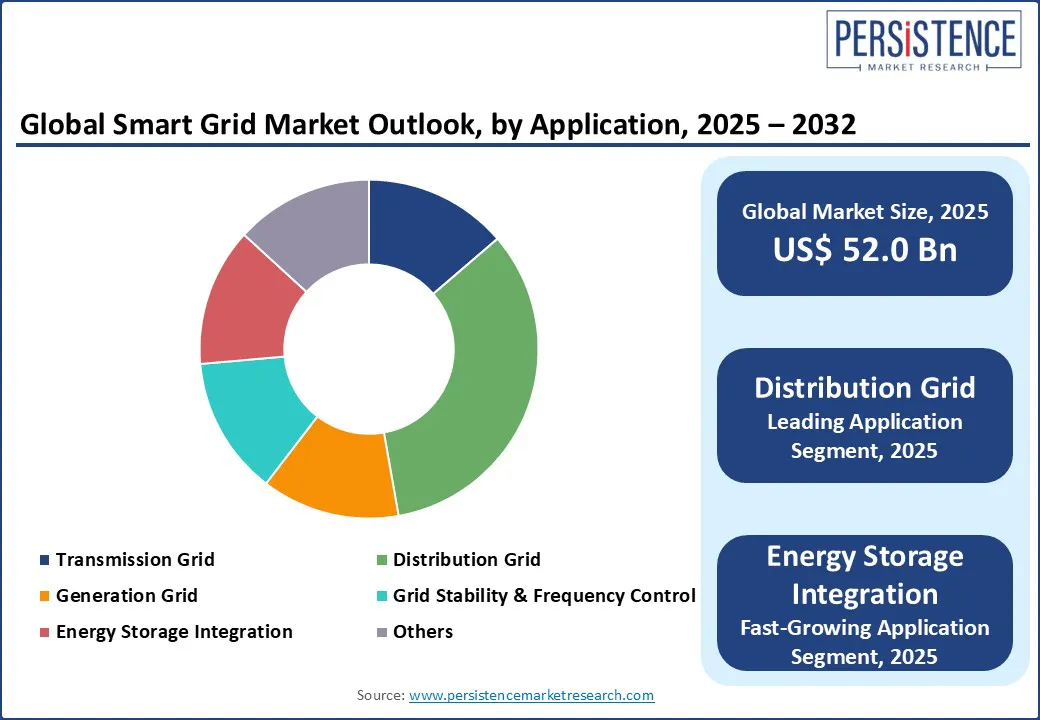

The global smart grid market size is likely to be valued at US$ 52 Bn in 2025 and is estimated to reach US$ 154.1 Bn in 2032, growing at a CAGR of 16.8% during the forecast period 2025 - 2032. The smart grid market growth is driven by the rising demand for efficient power systems, expanding renewable integration, and urgent infrastructure modernization. Rise in electric mobility and industrial electrification is driving the demand for smart grids.

Countries including China and Japan (US$ 597 Bn), the U.S. (US$ 10.5 Bn via Grid Resilience Innovative Partnership), and Europe (US$ 184 Bn) are investing heavily in grid digitalization. India and Bangladesh are scaling smart meter rollouts and digital billing.

Advanced technologies such as real-time analytics, edge computing, and smart sensors are improving grid stability, outage detection, and frequency control. With transmission grids largely digitized, the focus has shifted to distribution networks to effectively manage distributed generation and maintain voltage stability. Key solutions include smart switchgear, grid software, and predictive maintenance, enabling resilient, data-driven power systems.

Key Industry Highlights:

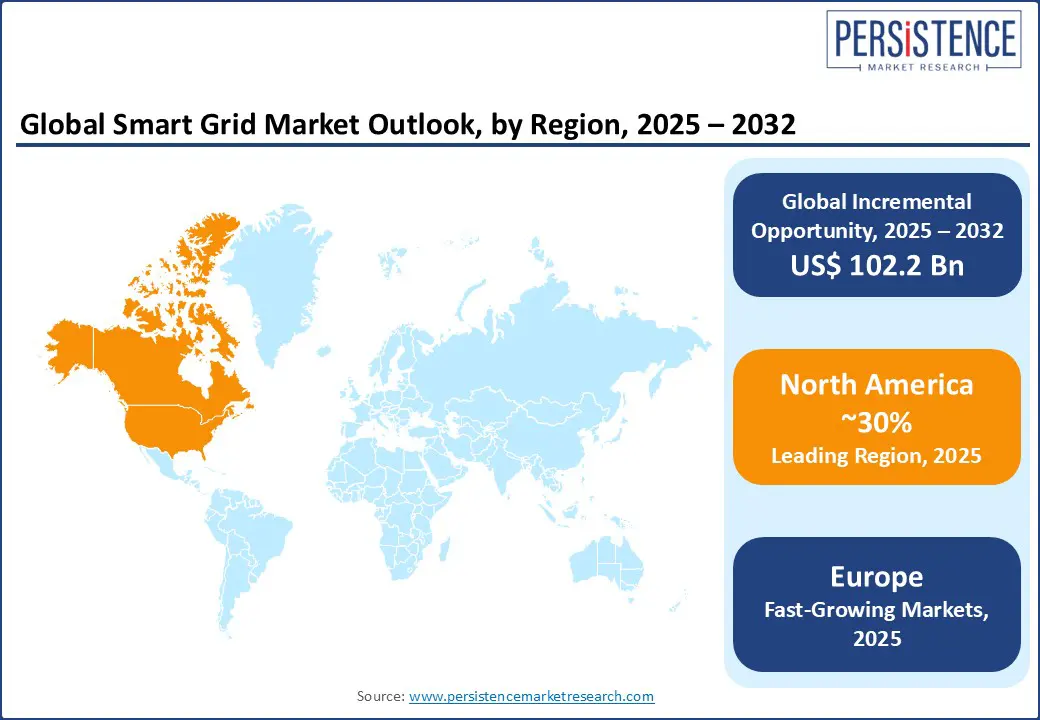

- North America is projected to dominate, accounting for a market share of approximately 30.2% in 2025, with the U.S. investing over US$ 10.5 Bn under the GRIP program to boost grid resilience, digital infrastructure, and distributed energy integration.

- Europe is anticipated to account for a 25.3% market share in 2025, backed by US$ 184 Bn in digital grid investments by 2030, focused on automation, decarbonization, and decentralized power systems under the EU’s clean energy roadmap.

- Software is likely to lead the component category with a 48.2% share in 2025, driven by the surge in real-time analytics, digital twins, and AI-driven energy management tools.

- The distribution grid applications segment is expected to dominate with 33.1% market share, propelled by growing rooftop solar, urban electrification, and real-time infrastructure monitoring.

- Key players in the smart grid market, such as Schneider Electric, GE Vernova, and Siemens, are shaping the innovation curve with modular DERMS, AI-powered platforms, and next-gen cybersecurity tools for smarter grid ecosystems.

- Electricity demand in developing regions is set to grow by over 2,600 TWh by 2030, pushing legacy grids toward smarter, more agile infrastructure that can adapt to load volatility and renewable influx.

|

Global Market Attribute |

Details |

|

Market Size (2024A) |

US$ 44.5 Bn |

|

Estimated Market Size (2025E) |

US$ 52.0 Bn |

|

Projected Market Value (2032F) |

US$ 154.1 Bn |

|

Value CAGR (2025 to 2032) |

16.8% |

|

Historical Market Growth (CAGR 2019 to 2024) |

13.5% |

Market Dynamics

Driver - Surging Electricity Demand and Aging Grids Are Driving the Push for Smarter Power Infrastructure

According to the International Energy Agency, electricity consumption is growing rapidly, especially across emerging markets, where demand is expected to rise by over 2,600 TWh by 2030, equal to five times Germany’s current usage. Much of this surge stems from rising urbanization, increased industrial activity, and growing residential cooling needs.

Electricity demand is rising nearly three times faster in many emerging and developing regions than in advanced economies, consistent with the IEA forecasts through 2027. However, traditional grids are struggling to handle this scale and variability, creating a pressing need for intelligent and efficient grid operations.

The pressure on old infrastructure is intensifying, particularly as more countries integrate intermittent renewables and electrify end-use sectors such as mobility and heating. Companies including Schneider Electric and Siemens are rolling out digital grid platforms that enable better load forecasting, decentralized energy integration, and real-time control. These systems help utilities reduce congestion, stabilize fluctuating supply, and cut carbon emissions, all while accommodating shifting demand patterns.

Restraint - Limited Utility Investment and Operational Losses Slow Progress in Digital Grid Upgrades

Many utilities, especially those in developing countries, face financial distress due to poor cost recovery, outdated billing systems, and high distribution losses. The pandemic aggravated these challenges, and by 2022, a population of 20 million lost access to electricity. Such instability made it difficult to allocate funds for modernizing infrastructure, rolling out digital tools, or deploying smart meters at scale.

The problem runs deeper than just financing; technical grid losses contribute around 1 gigaton of CO2 emissions annually, while non-technical losses generate US$ 80-100 Bn in lost revenue each year. Even though companies such as Oracle and Electrica have introduced digital billing, metering, and monitoring systems, many utilities still lack the institutional capacity and investment confidence to implement them system-wide.

These gaps restrict momentum and delay the transition to intelligent grids, undermining reliability and keeping regions locked in cycles of inefficient power delivery.

Opportunity - Digital Grid Technologies Open New Doors for Resilience, Energy Access, and Decentralization

Digital tools such as demand-side management platforms, AI-powered forecasting, and IoT-based sensors are reshaping how electricity is produced, distributed, and consumed.

As the demand for decentralization rises, regions such as Brazil saw distributed solar PV grow by over 7 GW in 2022, marking a 50% jump in one year. This rapid growth shows how much untapped energy potential exists beyond traditional grid setups. Companies including GE Vernova and Eaton are enabling factories and homes to become energy producers, reducing the load on central networks and promoting resilience.

These developments are particularly transformative in underserved or remote areas, where traditional grid expansion is costly or slow. Mini-grids, smart inverters, and modular systems offer clean, stable electricity to off-grid communities.

Technologies launched by firms such as LUMA and Mitsubishi in Puerto Rico and Taiwan show how targeted digital interventions can bring fast, flexible, and scalable solutions. These shifts improve energy equity and create open space for new investment models. By leveraging smarter digital layers, the smart grid helps meet energy needs while unlocking localized energy generation and greater system flexibility.

Trend - AI, Edge Computing, and Real-Time Data Are Reshaping Grid Innovation Worldwide

Grid innovation has entered a new phase driven by AI, real-time data platforms, and edge-level decision-making. Siemens’ Enhanced Grid Sensor and Schneider Electric’s ADMS technologies are helping utilities predict faults, manage distributed energy resources, and improve outage response. These capabilities are no longer just operational upgrades; they have become strategic necessities for maintaining stability in increasingly complex power systems.

Cybersecurity is also becoming a front-line concern as grids become more digital. GE Vernova’s recent focus on AI- and ML-driven grid protection, along with Cisco’s work on secure network infrastructure, highlights the growing intersection of tech and resilience.

At the same time, the demand from sectors such as EVs and cooling is surging. Air conditioners alone could double to 4 billion units by 2030, with 590 million added in emerging markets. As grids grow smarter and more connected, the ability to manage peak loads, optimize decentralized generation, and maintain reliability depends on agile, predictive platforms.

Category-wise Analysis

Component Insights

Based on component, the software segment is expected to hold a market share of around 48.2% in 2025, driven by the rising demand for real-time data management, advanced analytics, and decentralized grid control.

Platforms such as Siemens' Gridscale X and IBM’s Storage Assurance are playing a central role in helping utilities optimize grid operations by improving visibility, stability, and flexibility across energy networks. As grid complexity increases with the rise in distributed energy resources, utilities are adopting intelligent software to enhance decision-making and ensure seamless integration of renewable sources.

New-as-a-service business models are also driving momentum in this segment. ABB’s BESS-as-a-Service, launched in 2025, bundles software, hardware, and system optimization into a single flexible package that strengthens power stability and helps enterprises scale up without upfront capital costs.

These innovations are essential for modernizing infrastructure and making the smart grid more adaptable, with software becoming the brain behind efficient grid transmission, storage integration, and frequency control in global energy systems.

Application Insights

By application, the distribution grid segment is projected to hold a market share of around 33.1% in 2025, driven by rapid urban electrification, the surge in rooftop solar, and rising grid modernization efforts.

Real-time distribution monitoring solutions, such as Siemens’ SICAM Enhanced Grid Sensor launched in August 2024, are helping utilities prevent overloads, optimize infrastructure, and seamlessly integrate renewables. ABB's innovation rollout in China further supports distribution-level upgrades with modular switchgear and cloud-based platforms that improve flexibility and reduce downtime across local networks.

New growth opportunities are emerging with the adoption of AI, IoT, and machine learning, which will transform conventional distribution networks into intelligent, adaptive systems. These technologies enable predictive maintenance, precise demand-supply balancing, and improved outage management, which are key for addressing the complexity introduced by decentralized energy sources.

As countries including the U.S., China, and India accelerate digital infrastructure deployment, distribution networks are becoming the central nerve of the smart grid, enabling real-time responsiveness and enhanced energy resilience across the system.

Regional Insights

North America Smart Grid Market Trends

North America is expected to hold a market share of around 30.2% in 2025, driven by large-scale funding programs, rapid technology adoption, and the growing demand for resilient and decentralized power systems.

The U.S. Department of Energy allocated US$ 10.5 Bn through the GRIP program to modernize the electricity grid, with US$ 3 Bn supporting the expansion of digital infrastructure. Advanced solutions such as GE Vernova’s GridOS® and Itron’s Grid Edge Essentials are transforming data orchestration across distribution and transmission grids, enabling real-time visibility, improved frequency control, and seamless integration of distributed energy resources (DERs).

Both hardware and software segments are gaining momentum as utilities focus on expanding their digital capabilities across grid applications. The U.S. is witnessing robust developments in energy storage integration and decentralized grid operations, while Canada is emerging as a testbed for innovative models such as DC microgrids in commercial spaces. Collaborations, such as Itron’s partnership with Schneider Electric and Eaton’s partnership with Siemens Energy, are accelerating the deployment of flexible, modular power systems that enhance service reliability and grid performance, opening up fresh opportunities in service-based models across North America’s evolving energy landscape.

Europe Smart Grid Market Trends

Europe is projected to hold a market share of around 25.3% in 2025, driven by robust investment momentum and strong policy support for grid modernization and decarbonization goals.

The European Union’s ambitious action plan sets aside US$ 633 Bn in electricity grid investments by 2030, with US$ 184 Bn dedicated specifically to digitalization. Countries including Germany, France, Italy, and the Nordics are prioritizing distribution grid upgrades, improved asset monitoring, and accelerated deployment of intelligent systems to support fluctuating renewable generation and electrification of transport and industries.

The region is witnessing growing adoption of advanced grid control software, fault detection systems, and decentralized energy solutions, opening new growth avenues in smart metering, predictive maintenance, and real-time load management.

The REPowerEU plan injects an additional US$ 31.5 Bn into enhancing grid interconnectors and reinforcing transmission infrastructure. Digital platforms across Europe now enable utilities to optimize operations, reduce downtime, and defer future capital costs, which are essential for managing the energy transition. As more EU nations align with net-zero targets, digital grid solutions, smart energy services, and resilient infrastructure are becoming the cornerstones of the region’s evolving energy landscape.

Competitive Landscape

The global smart grid market remains consolidated, with leading players such as General Electric, Schneider Electric, Siemens, ABB, Mitsubishi Electric, and Cisco Systems, Inc. a significant share through sustained innovation and strategic collaborations.

These companies are investing heavily in grid digitalization, edge intelligence, and integrated software platforms to boost grid reliability, efficiency, and sustainability. Many are also aligning their offerings with national clean energy goals and electrification programs to expand their footprint.

Governments across regions are actively supporting public-private partnerships and funding initiatives to accelerate smart infrastructure deployment.

Companies such as Itron, Eaton, SAP, and EsyaSoft Technologies are capitalizing on this momentum by offering advanced analytics, grid automation tools, and demand-side management platforms. As the market scales, players are expected to focus on modular, service-based business models and data-driven energy optimization to unlock new growth avenues in transmission.

Key Industry Developments

- In June 2025, Eaton and Siemens Energy launched a strategic initiative to deliver modular, grid-independent power systems for data centers in North America. The joint solution integrates on-site generation and smart infrastructure to improve grid resilience and accelerate renewable integration.

- In February 2024, Itron and Schneider Electric partnered to integrate EcoStruxure ADMS and Grid Edge Intelligence, enabling real-time visibility from smart meters and DERs. This collaboration supported decentralized energy adoption and strengthened grid flexibility across North America.

Companies Covered in Smart Grid Market

- General Electric Company

- Schneider Electric SE

- Wipro Limited

- EsyaSoft Technologies Private Limited

- Cisco Systems, Inc.

- SAP SE

- ABB Ltd.

- Itron, Inc.

- Globema Sp. z o.o.

- Xylem Inc.

- Eaton Corporation plc

- Grid4C Inc.

- Mitsubishi Electric Corporation

- Siemens AG

- International Business Machines Corporation (IBM)

Frequently Asked Questions

The Smart Grid Market is projected to be valued at US$ 52.0 Bn in 2025.

Based on application, the distribution grid is expected to hold approximately 33.1% market share in 2025, driven by rapid urban electrification, rooftop solar adoption, and increased grid modernization efforts.

The smart grid market is poised to witness a CAGR of 16.8% from 2025 to 2032.

Escalating power demand and aging grids accelerate the shift to intelligent energy infrastructure.

Digital technologies enabling decentralized energy, improved resilience, and expanded access present key opportunities for smart grid adoption.

Prominent players in the smart grid market include GE Electric, Schneider Electric, Siemens, ABB, Mitsubishi Electric, and Cisco Systems, Inc.