- Sporting Goods & Equipment

- Safety Gloves Market

Safety Gloves Market Size, Trends, Share, and Growth Forecast, 2026 - 2033

Safety Gloves Market by Product Type (Disposable Gloves and Durable Gloves), Material Type Natural Rubber, Nitrile, Neoprene, Vinyl, Leather, and Others), End-user (Medical & Healthcare, Food & Beverages, Chemicals, Manufacturing, Construction, Oil & Gas, Mining and Others), and Regional Analysis for 2026 - 2033

Safety Gloves Market Size and Trends Analysis

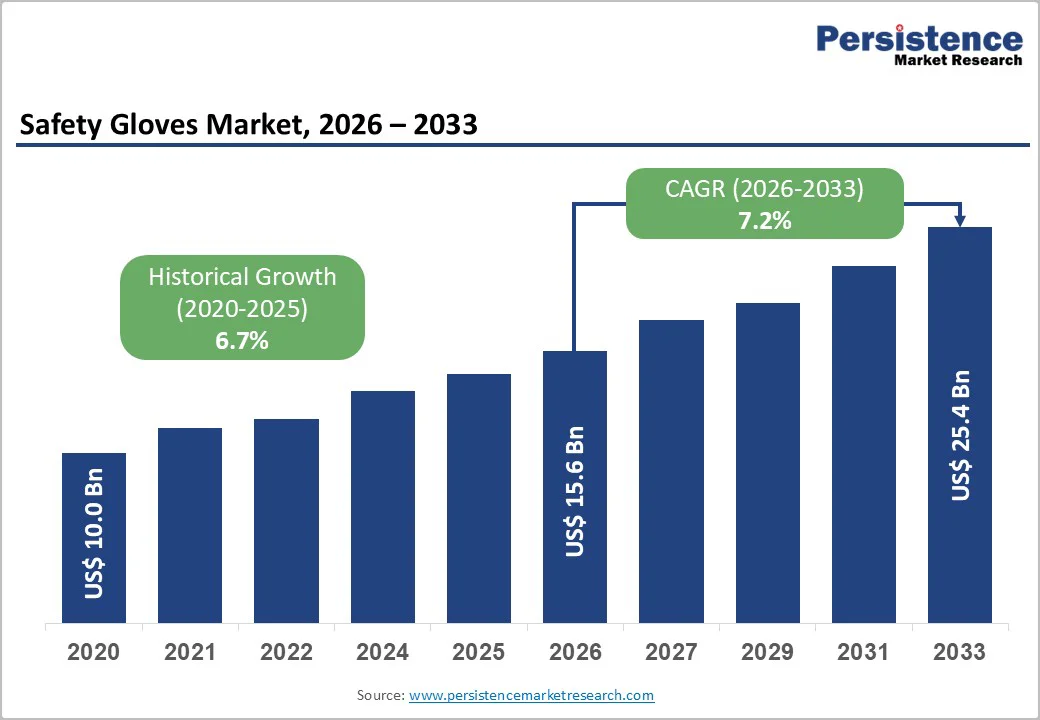

The global safety gloves market size is valued at US$ 15.6 billion in 2026 and is projected to reach US$ 25.4 billion by 2033, growing at a CAGR of 7.2% between 2026 and 2033.

This expansion is driven by a confluence of factors: stringent occupational safety regulations (OSHA, EU standards), heightened hygiene awareness across non-medical sectors, and the rebound of global industrial manufacturing. The market is characterized by a structural shift toward specialized, high-performance hand protection, moving beyond basic compliance to ergonomic and application-specific solutions.

Key Industry-Highlights:

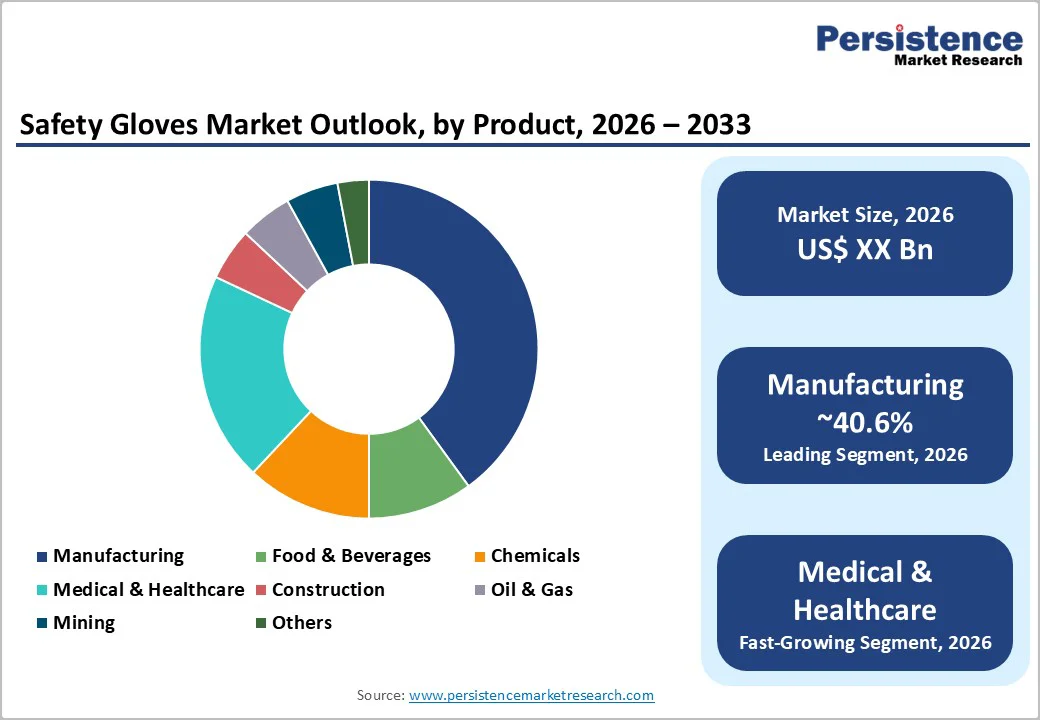

- Leading End-user: Manufacturing holds the largest share at 40.6%, driven by continuous exposure to mechanical, thermal, and chemical risks, making durable gloves essential for worker protection. Healthcare and food processing follow, supported by sterility and hygiene compliance requirements.

- Material Dynamics: Nitrile dominates with 32.1% share, recognized for its chemical resistance, durability, and latex-free properties. Natural rubber is emerging as the fastest-growing material, particularly in cost-sensitive markets and surgical environments that require high tactile sensitivity.

- Product Segment: Disposable gloves represent the fastest-growing product type, supported by rising hygiene awareness and strict sanitization protocols across food handling, retail, hospitality, and pharmaceuticals.

- Sustainability Transition: Biodegradable nitrile gloves are gaining traction as a strategic innovation focus, addressing environmental concerns related to single-use waste and supporting ESG-compliant procurement.

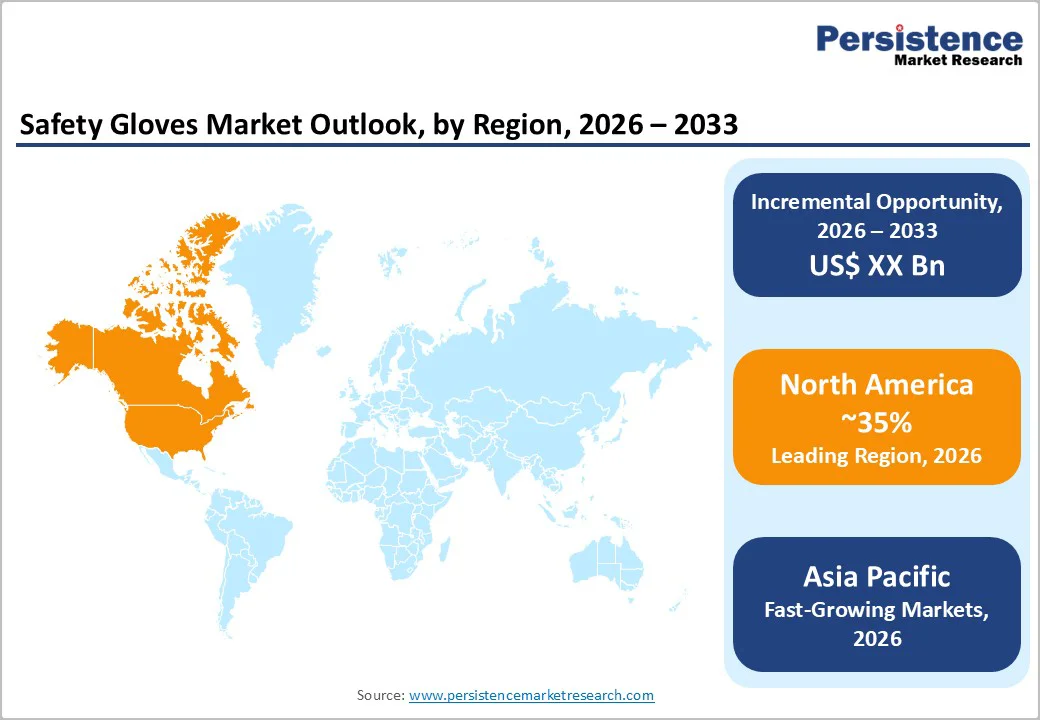

- Regional Market Dynamics: North America leads in regulatory-driven value adoption with 35%, while Asia-Pacific records the highest volume growth, supported by rapid industrialization, low-cost manufacturing, and expanding PPE production capacity.

| Key Insights | Details |

|---|---|

| Safety Gloves Market Size (2026E) | US$ 15.6 Bn |

| Market Value Forecast (2033F) | US$ 25.4 Bn |

| Projected Growth (CAGR 2026 to 2033) | 7.2% |

| Historical Market Growth (CAGR 2020 to 2025) | 6.7% |

Market Dynamics

Drivers - Stringent Occupational Safety Regulations and Compliance Enforcement

Regulatory mandates remain the primary catalyst for market adoption. Agencies such as the Occupational Safety and Health Administration (OSHA) in the U.S. and the European Agency for Safety and Health at Work (EU-OSHA) enforce strict PPE standards, making hand protection non-negotiable in high-risk sectors.

In 2024, regulatory bodies intensified scrutiny on workplace injuries, where hand injuries account for over 20% of disabling workplace accidents globally. The enforcement of standards such as EN 388 (mechanical risks) and EN 374 (chemical risks) compels industries to upgrade from general-purpose gloves to specialized, higher-value cut-resistant and chemical-resistant alternatives, directly boosting market revenue.

Industrial Resurgence and Expansion of High-Risk Sectors

The global recovery of the manufacturing, construction, and oil & gas sectors post-pandemic is fueling sustained demand. The manufacturing sector alone commands a 40.6% share, with vast volumes of abrasion-, impact-, and thermal-protection gloves.

As automation increases, the demand shifts toward gloves that offer high dexterity for precision alongside protection. Furthermore, the expanding chemical and pharmaceutical processing industries require advanced nitrile and neoprene solutions to handle hazardous substances. With global industrial output projected to grow by approximately 3-4% annually, the baseline demand for durable safety gloves remains robust and non-cyclical.

Restraints - Raw Material Price Volatility and Supply Chain Instability

The market faces structural challenges from fluctuating costs of key inputs such as Nitrile Butadiene Rubber (NBR) and Natural Rubber Latex. In Q2 2025, NBR prices in the U.S. surged to approximately US$ 3,070 per metric ton due to feedstock shortages (butadiene) and maintenance shutdowns at major petrochemical plants.

Such volatility squeezes manufacturers' profit margins, who struggle to pass on full cost increases to price-sensitive end-users. Additionally, reliance on Southeast Asia (Malaysia, Thailand, Vietnam) for over 65% of the global rubber glove supply exposes the market to geopolitical risks, shipping delays, and tariff uncertainties, creating periodic supply shocks.

Pricing Pressures and Intense Market Competition

The safety gloves market is highly fragmented and price-sensitive, particularly in the disposable segment. Major manufacturers such as Hartalega and Top Glove have had to decommission older, less efficient production lines to manage costs.

The presence of low-cost manufacturers in China, leveraging lower energy costs, exerts constant downward pressure on global pricing, forcing established players to compete on thin margins or pivot to premium, differentiated products to survive.

Opportunity - Sustainable and Biodegradable Glove Technologies

With billions of disposable gloves ending up in landfills annually, sustainability has transitioned from a niche preference to a critical procurement requirement. Innovations such as biodegradable nitrile gloves (e.g., utilizing Eco Best Technology or organic additives) that decompose in 1-5 years versus centuries offer massive actionable potential.

Healthcare systems and corporate ESG mandates are driving demand for these green alternatives. The "Green PPE" market segment is estimated to present a US$ 1.5 billion opportunity by 2030, as premium buyers in Europe and North America show willingness to pay a marginal premium for reduced environmental impact.

Diversification into Specialized "Smart" and Ergonomic Gloves

There is a significant unmet need for gloves that prevent musculoskeletal disorders (MSDs) and hand fatigue while integrating technology. Opportunities exist in developing ultra-thin, high-dexterity gloves with ANSI Cut Level A7-A9 protection using advanced engineered yarns (e.g., Dyneema, Kevlar).

Furthermore, the convergence of PPE with IoT, such as gloves with embedded RFID tags for compliance tracking or Near Field Communication (NFC) for access control, represents a high-value frontier in the Oil & Gas and high-security manufacturing sectors.

Category-wise Analysis

Product Type Insights

Durable gloves dominate the market value, driven by their high unit price and critical role in heavy industry. This segment encompasses mechanical protection (cut, impact, abrasion), chemical protection, and thermal gloves.

The dominance is sustained by the rigorous safety requirements of the manufacturing, construction, and oil & gas sectors, where a single pair of specialized impact gloves can cost 20x-50x more than disposable alternatives. Innovations in "second-skin" knitting technologies have reinforced this lead by improving user compliance.

Disposable gloves are the fastest-growing category, fueled by the rapid expansion of the healthcare, pharmaceutical, and food service sectors. The shift from vinyl to thinner, stronger, and allergy-free nitrile disposables is a key sub-trend. The recurring nature of consumption where a single worker may use 10-20 pairs daily ensures continuous volume growth, outbound by strict hygiene protocols in both developed and emerging markets.

Material Type Insights

Nitrile holds the largest share due to its superior balance of chemical resistance, puncture resistance, and hypoallergenic properties compared to latex. It has become the industry standard in healthcare ("medical grade") and food handling, effectively displacing natural rubber in many regions due to latex allergy concerns. Its dominance is reinforced by its versatility; nitrile can be formulated for both ultra-thin disposable exams and heavy-duty chemical industrial gloves.

Despite allergy concerns, Natural Rubber is the fastest-growing segment, driven by its unmatched elasticity, tactile sensitivity, and cost-effectiveness in specific applications. It remains highly preferred in surgical settings for precision tasks and in developing markets where cost is a primary determinant. Furthermore, improvements in protein-reduction manufacturing technologies are mitigating some allergy risks, sustaining its relevance.

End-user Insights

Manufacturing is the behemoth of the market, encompassing automotive, aerospace, electronics, and heavy machinery. The diversity of hazards in this sector, from sharp metal edges in automotive assembly to corrosive solvents in electronics, creates a massive variety of glove types. The push towards "Industry 4.0" and automated assembly lines hasn't reduced glove usage; rather, it has shifted demand toward higher-dexterity, precision-protection gloves.

The Medical & Healthcare segment is expanding most rapidly, projected to outpace industrial growth. This is driven by aging global populations increasing healthcare utilization, the expansion of healthcare infrastructure in the Asia Pacific, and stricter infection control protocols. The segment is also seeing a value shift, with higher adoption of specialized surgical gloves and chemotherapy-tested nitrile gloves.

Regional market Insights

North America Safety Gloves Market Trends

North America remains a dominant force, characterized by a mature industrial base and the world's most stringent safety enforcement environment. The U.S. market is heavily influenced by OSHA mandates and ANSI/ISEA 105 standards, which drive the adoption of high-performance cut and impact-resistant gloves.

The region is an innovation hub, with major players like Protective Industrial Products (PIP) and Ansell introducing advanced engineered yarns and smart PPE. Recent US tariffs on Chinese medical imports are reshaping the supply chain, favoring domestic production and imports from allies like Malaysia, creating a distinct sourcing dynamic compared to other regions.

Europe Safety Gloves Market Trends

Europe accounts for a significant share, driven by the strong industrial bases of Germany (automotive/machinery) and France. The region is defined by strict adherence to EN standards (e.g., EN 420, EN 388), ensuring high-quality product penetration.

A key differentiator is the region's aggressive stance on sustainability; the EU Green Deal and corporate ESG goals are forcing manufacturers to adopt eco-friendly packaging and biodegradable glove materials faster than in any other region. The market here is highly consolidated around quality-focused players adhering to REACH regulations regarding chemical safety in glove manufacturing.

Asia Pacific Safety Gloves Market Trends

Asia Pacific is the fastest-growing market, fueled by rapid industrialization in China, India, and ASEAN nations. It serves a dual role: the world's primary production hub for gloves (especially rubber and nitrile in Malaysia/Thailand) and a burgeoning consumer market.

Rising safety awareness in China's massive manufacturing sector and India's construction boom is transitioning workers from bare-hand labor to using basic PPE. The region benefits from proximity to raw material sources (natural rubber plantations), offering a structural cost advantage that supports mass-market volume growth.

Competitive Landscape

The market is moderately fragmented, with the top 10 players controlling roughly 35% of the global share. It features a tiered structure: Tier 1 consists of diversified global giants (Ansell, Honeywell, 3M) providing high-tech, durable solutions.

Tier 2 comprises massive volume producers of disposables (Top Glove, Hartalega) based in Southeast Asia. The market is currently consolidating as established players seek scale to combat pricing pressures and acquire niche technologies.

Key Industry Developments:

- In November 2024, Dipped Products PLC completed the acquisition of a Thailand-based rubber glove manufacturing facility. Such an acquisition helps the company to expand its global footprint in the rubber glove manufacturing industry and strengthen its presence in international markets.

- In June 2024, Uvex revealed its newest product: the uvex Profi pure HG safety glove. This glove is designed to provide excellent grip in wet working conditions. The key to the Profi pure HG’s impressive performance is its Hydro Grip technology, which gives a waterproof grip without losing traction.

- In April 2024, Ansell Ltd. acquired Kimberly-Clark’s Personal Protective Equipment business (KCPPE) from Kimberly-Clark Corporation for USD 640 million in cash. Such an acquisition helps the company to enhance its market presence in the personal protective equipment market.

Companies Covered in Safety Gloves Market

- 3M

- Carolina Glove Co.

- Amada Miyachi America

- Mallcom

- Lakeland Industries

- Delta Plus

- Superior Glove Works Limited

- Globus Group

- Midas Safety

- Alpha Packaging, Inc.

- The Lincoln Electric Company

- DuPont de Nemours, Inc.

- Others Key Players

Frequently Asked Questions

The Safety Gloves market is estimated to be valued at US$ 15.6 Bn in 2026.

The key demand driver for the Safety Gloves market is increasing workplace safety enforcement across industrial environments. Rising global regulations on worker protection, especially in manufacturing, construction, oil & gas, mining, and healthcare, are compelling organizations to adopt certified hand protection equipment to reduce injury risks and ensure compliance.

In 2026, North America is expected to dominate with an exceeding 35% revenue share in the global Safety Gloves market.

Among the End- use, Manufacturing holds the highest preference, capturing beyond 40.3% of the market revenue share in 2026, surpassing other End- use type.

The key players in Safety Gloves are 3M, Carolina Glove Co., Amada Miyachi America, Mallcom, and Lakeland Industries.