- Telecommunications

- Public Safety LTE and Mobile Broadband Market

Public Safety LTE and Mobile Broadband Market Size, Share, and Growth Forecast 2026 - 2033

Public Safety LTE and Mobile Broadband Market by Solution (Infrastructure, Services), by End Use (Law Enforcement, Emergency Services, Military, Fire Response, Railways, Others), by Regional Analysis, 2026-2033

Public Safety LTE and Mobile Broadband Market Size and Trend Analysis

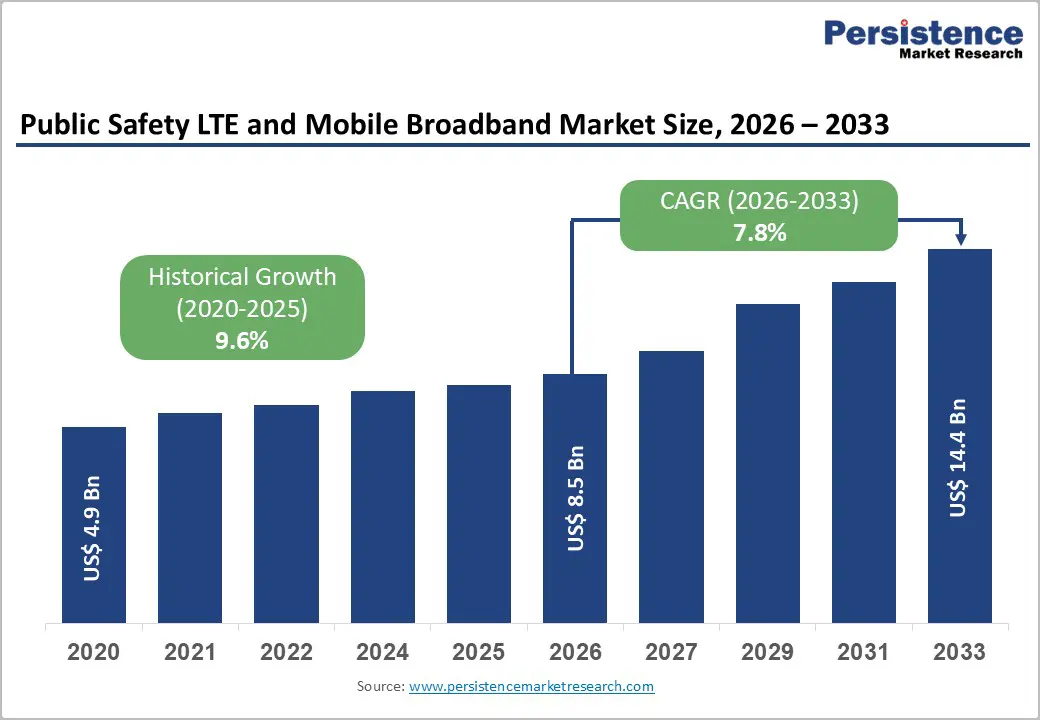

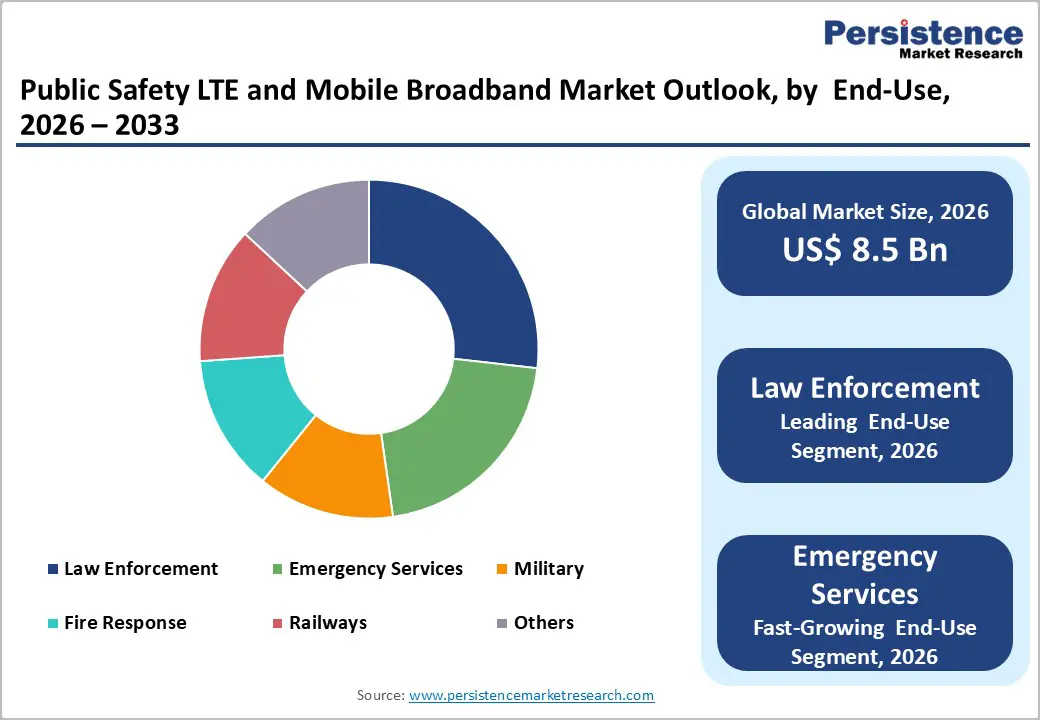

The global Public Safety LTE and Mobile Broadband market size is expected to be valued at US$ 8.5 billion in 2026 and projected to reach US$ 16.7 billion by 2033, growing at a CAGR of 10.1% between 2026 and 2033.

This growth is driven by rising demand for real-time data, video, and mission-critical communications as public safety agencies migrate from legacy LMR systems to broadband-enabled networks. LTE and 5G technologies enhance interoperability, situational awareness, and response efficiency during emergencies. Initiatives such as the U.S. First Responder Network Authority (FirstNet) and government investments in dedicated spectrum, including Band 14, further support adoption by enabling high-speed data, location tracking, and advanced communication capabilities.

Key Market Highlights

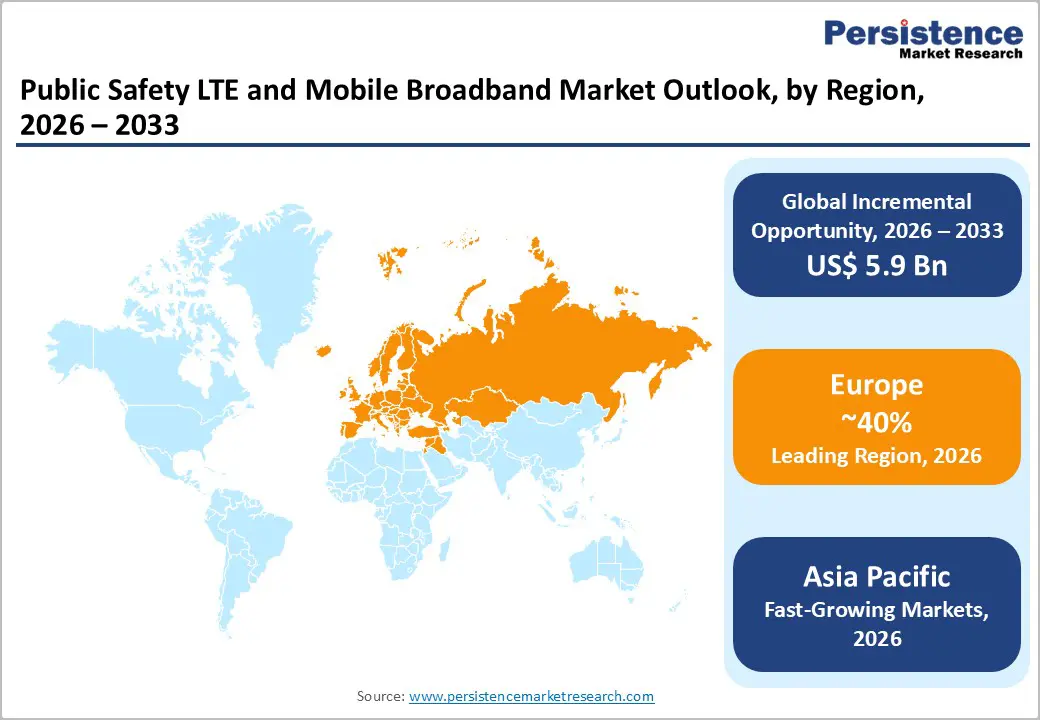

- Leading Region: North America leads the Public Safety LTE and Mobile Broadband market with ~40% share (2025), driven by FirstNet’s nationwide Band 14 deployment and priority broadband access for first responders.

- Fastest-Growing Region: Asia Pacific holds ~32% share in 2025 and is the fastest-growing region, supported by China’s 700 MHz public safety broadband initiatives and Japan’s expanding PS-LTE networks.

- Leading Category: Infrastructure dominates the Solution segment with ~65% share (2025), reflecting heavy investment in RAN, core networks, and resilient broadband infrastructure for mission-critical operations.

- Fastest-Growing Category: Law Enforcement accounts for ~35% share of End Use in 2025, driven by high adoption of real-time surveillance, mobile command systems, and field data applications.

- Key Market Opportunity: 5G Standalone represents a key growth opportunity, enabling ultra-reliable low-latency communication for disaster response, smart city integration, and next-generation public safety services.

| Global Market Attributes | Key Insights |

|---|---|

| Public Safety LTE and Mobile Broadband Size (2026E) | US$ 8.5 billion |

| Market Value Forecast (2033F) | US$ 16.7 billion |

| Projected Growth CAGR(2026-2033) | 10.1% |

| Historical Market Growth (2020-2025) | 9.6% |

Market Dynamics

Market Drivers

Advancements in Mission-Critical LTE and 3GPP Communication Capabilities

The integration of 3GPP mission-critical services, including mission-critical push-to-talk, push-to-video, and group communications, is a major driver for Public Safety LTE adoption. These capabilities enable seamless, real-time multimedia communication among first responders, significantly improving coordination during emergencies. Compared to legacy narrowband systems such as TETRA and Airwave, LTE-based platforms deliver substantially higher data throughput and operational flexibility.

Nationwide deployments such as FirstNet demonstrate the impact of these advancements, offering priority and preemption across extensive geographic coverage. Public safety agencies report significantly faster multimedia transmission, enabling live video sharing, data analytics, and enhanced situational awareness during dynamic incidents such as wildfires, natural disasters, and large-scale public events, ultimately reducing response times and operational risks.

Government-Led Investments and Dedicated Spectrum Allocation for Public Safety Broadband

Government investments and dedicated spectrum allocation play a critical role in accelerating Public Safety LTE network deployment worldwide. Initiatives led by authorities such as the First Responder Network Authority support large-scale infrastructure upgrades, including deployable assets designed to enhance rural, remote, and indoor coverage. These investments ensure reliable connectivity where commercial networks may fail during emergencies.

Globally, regulatory policies mandating broadband communication for public safety agencies further reinforce adoption. Allocation of low-band spectrum, such as the 700 MHz band, supports wide-area coverage and improved signal penetration. Reduced latency and assured network availability during peak usage strengthen confidence among agencies, driving the transition toward broadband-based mission-critical communication systems.

Market Restraints

High Capital Expenditure and Ongoing Infrastructure Deployment Costs

High infrastructure deployment costs remain a key restraint for the Public Safety LTE and Mobile Broadband market. Establishing LTE or 5G core networks, radio access networks, and secure backhaul systems requires significant capital investment, particularly for dedicated public safety deployments. Nationwide networks often involve multi-billion-dollar expenditure, creating financial barriers for regional and municipal agencies with limited budgets.

Beyond initial rollout, ongoing maintenance and upgrades add further cost pressure. Public safety networks must be resilient to harsh environmental conditions and capable of operating during disasters, increasing operational expenditure. As a result, many smaller agencies delay full adoption or rely on commercial partnerships, slowing the transition from legacy communication systems in underfunded regions.

Interoperability Challenges with Legacy LMR and Communication Systems

Interoperability with legacy land mobile radio systems continues to hinder seamless adoption of Public Safety LTE solutions. Many public safety agencies operate long-established LMR networks that lack native broadband compatibility, requiring complex and costly hybrid integration approaches. These transitional solutions increase system complexity and prolong migration timelines.

High-profile implementation delays highlight these challenges, particularly when vendor changes or technology shifts disrupt continuity. Fragmented communication environments can create reliability concerns during multi-agency operations, where seamless handover between voice and data systems is critical. Until interoperability frameworks mature and migration paths stabilize, agencies may remain cautious in fully replacing trusted legacy communication platforms.

Market Opportunities

Expansion into 5G Standalone Networks for Ultra-Reliable Public Safety Communications

The transition toward 5G Standalone (SA) networks presents a significant growth opportunity for the Public Safety LTE and Mobile Broadband market. 5G SA enables ultra-reliable low-latency communication, supporting mission-critical applications such as real-time video analytics, remote incident monitoring, and autonomous response systems in fire services, railways, and critical infrastructure protection. These capabilities substantially enhance operational precision during time-sensitive emergencies.

Ongoing 5G deployments within public safety ecosystems highlight this opportunity. Upgrades to deployable network assets and in-building coverage solutions strengthen resilience during disasters and large public events. As agencies prioritize future-proof communication platforms with higher throughput and reliability, demand for integrated 4G/5G public safety networks continues to expand globally.

Growth in Smart City and Intelligent Public Safety Integrations

The expansion of smart city initiatives creates strong opportunities for Public Safety LTE adoption, particularly in rapidly urbanizing regions. Integration of IoT sensors, AI-driven analytics, and connected surveillance systems relies heavily on secure, high-capacity broadband networks. Public safety LTE supports real-time data exchange for applications such as traffic monitoring, crowd management, and predictive incident response.

Emerging economies across Asia are increasingly deploying private and shared broadband networks for public safety use cases. Falling 5G infrastructure costs and supportive digitalization policies further accelerate adoption. As urban authorities seek intelligent, data-driven safety solutions, vendors offering scalable and secure public safety broadband platforms are well-positioned to capture growing demand.

Category-wise Insights

Solution Analysis

Infrastructure dominates the Solution category, accounting for around 65% market share in 2025, driven by large-scale investments in radio access networks, core networks, and supporting backhaul for public safety broadband. Agencies prioritize robust macro and small cell deployments to ensure wide-area, in-building, and disaster-resilient coverage. Expansion of dedicated and prioritized LTE infrastructure under national programs highlights the critical role of network reliability in supporting mission-critical voice, data, and video communications.

Looking ahead, the services segment is expected to emerge as the fastest-growing category as public safety agencies seek managed services, network optimization, and lifecycle support. Increasing complexity of hybrid LTE–5G environments and integration with legacy systems is driving demand for system integration, maintenance, and analytics-driven network management, supporting long-term operational efficiency.

End Use Analysis

Law enforcement leads the End Use category with approximately 35% market share in 2025, supported by strong demand for real-time data access, situational awareness tools, and secure broadband connectivity. Police agencies increasingly rely on LTE networks for surveillance, mobile command operations, and field data applications. Adoption of commercial LTE overlays and dedicated public safety networks has accelerated deployments, reinforcing law enforcement as the largest user group.

Emergency medical services and disaster response agencies are expected to witness the fastest growth over the forecast period. Rising focus on rapid response, remote diagnostics, and live data sharing from incident scenes is increasing reliance on broadband connectivity. As public safety operations become more data-intensive, these segments are adopting advanced communication platforms to improve response coordination and outcomes.

Regional Insights

North America Public Safety LTE and Mobile Broadband Market Trends and Insights

North America leads the global Public Safety LTE and Mobile Broadband market with approximately 40% market share in 2025, driven by early adoption of nationwide broadband infrastructure for first responders. Strong federal backing, mature telecom ecosystems, and large-scale public safety modernization programs underpin this leadership. Law enforcement, fire, and emergency medical agencies increasingly rely on broadband connectivity for mission-critical voice, video, and data services.

The United States anchors regional dominance through FirstNet, the only nationwide broadband network dedicated to public safety. Extensive Band 14 spectrum coverage, priority and preemption features, and expanding 5G-enabled deployable assets strengthen reliability during disasters. Regulatory support from the FCC further encourages innovation, enabling advanced applications such as real-time network monitoring and enhanced situational awareness tools.

Europe Public Safety LTE and Mobile Broadband Market Trends and Insights

Europe represents a mature yet steadily expanding market, supported by coordinated efforts to migrate from legacy TETRA systems to LTE-based broadband platforms. Regional adoption is reinforced by harmonized mission-critical service standards and cross-border interoperability initiatives. Public safety agencies across major economies are investing in broadband networks to improve data capacity, coverage, and multi-agency coordination.

The European Public Safety LTE and Mobile Broadband market is expected to grow at a CAGR of around 9% over the forecast period. National programs such as Finland’s VIRVE 2.0 and ongoing Emergency Services Network deployments drive modernization despite implementation challenges. EU-level mandates promoting broadband communications for public protection and disaster relief continue to support long-term adoption and technology upgrades.

Asia Pacific Public Safety LTE and Mobile Broadband Market Trends and Insights

Asia Pacific accounts for an estimated 32% market share in 2025, reflecting rapid infrastructure development and expanding public safety digitization initiatives. Governments across the region are investing in broadband communication systems to support urban security, disaster management, and large-scale public events. Rising smartphone penetration and improving telecom infrastructure further accelerate adoption.

The region is also the fastest-growing globally, supported by strong policy backing and cost-effective deployments. China’s private LTE networks for police, Japan’s public safety LTE frameworks, and India’s scalable rollouts highlight diverse implementation models. Integration of 5G, IoT, and smart city platforms positions Asia Pacific as a key growth engine for next-generation public safety broadband solutions.

Competitive Landscape

The Public Safety LTE market exhibits a highly consolidated competitive structure, with a small group of large-scale vendors accounting for over half of total market participation through long-term, nationwide contracts. Market leadership is reinforced by strong portfolios in network infrastructure, mission-critical communications, and end-to-end solution delivery. High entry barriers, regulatory requirements, and the need for proven reliability limit the number of capable competitors.

Competition increasingly centers on technological differentiation rather than pricing. Vendors focus on advancing 5G mission-critical services, resilient radio access networks, and AI-driven analytics to enhance situational awareness. Strategic partnerships, spectrum-sharing models, and integrated device ecosystems are gaining traction, alongside emerging subscription-based and hybrid LMR–LTE deployment approaches.

Key Market Developments

- In March 2025, AT&T and the FirstNet Authority expanded the FirstNet network to support over 7 million connections, introducing enhanced 5G capabilities for first responders, improving deployable assets, network resilience, and real-time data, video, and mission-critical communication performance during large-scale emergencies.

- In 2024, Erillisverkot deployed the VIRVE 2.0 core network by integrating Elisa’s 4G and 5G radio access infrastructure, enabling secure, high-capacity broadband connectivity for Finnish public safety agencies and supporting advanced mission-critical services, interoperability, and future-ready public protection and disaster relief operations.

- In 2025, the FirstNet Authority updated its strategic roadmap to prioritize investments in rural and in-building coverage, deployable network solutions, and capacity upgrades, strengthening nationwide public safety broadband reliability and ensuring consistent priority connectivity during disasters and high-demand emergency response scenarios.

Frequently Asked Questions

The Public Safety LTE and Mobile Broadband market is projected to reach US$ 8.5 billion in 2026, driven by accelerated broadband upgrades and nationwide public safety network deployments.

A key demand driver is the shift toward LTE and 5G mission-critical services, enabling real-time voice, video, and data sharing for first responders across resilient broadband infrastructure.

North America leads the market with ~40% share in 2025, supported by the FirstNet nationwide Band 14 network and strong federal backing for public safety communications.

A major opportunity lies in 5G Standalone adoption, enabling URLLC, IoT integration, and smart city-driven disaster response capabilities for next-generation public safety operations.