- Sensors & Controls

- Radiation Detection, Monitoring and Safety Equipment Market

Radiation Detection, Monitoring and Safety Equipment Market Size, Share, and Growth Forecast 2026 - 2033

Radiation Detection, Monitoring and Safety Equipment Market by Product Type (Detection & Monitoring Equipment, Safety Equipment), Technology (Gas-Filled Detectors, Scintillators, Solid-State Detectors, Others), Mode of Operation, End-User, Regional Analysis, 2026 - 2033

Radiation Detection, Monitoring and Safety Equipment Market Size and Trend Analysis

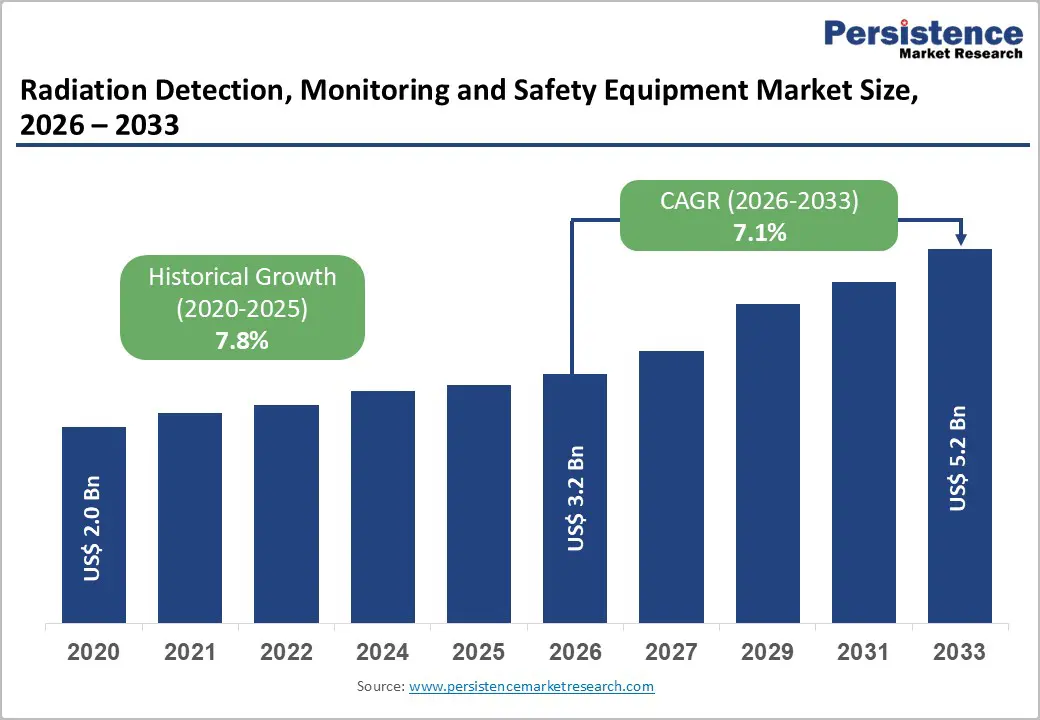

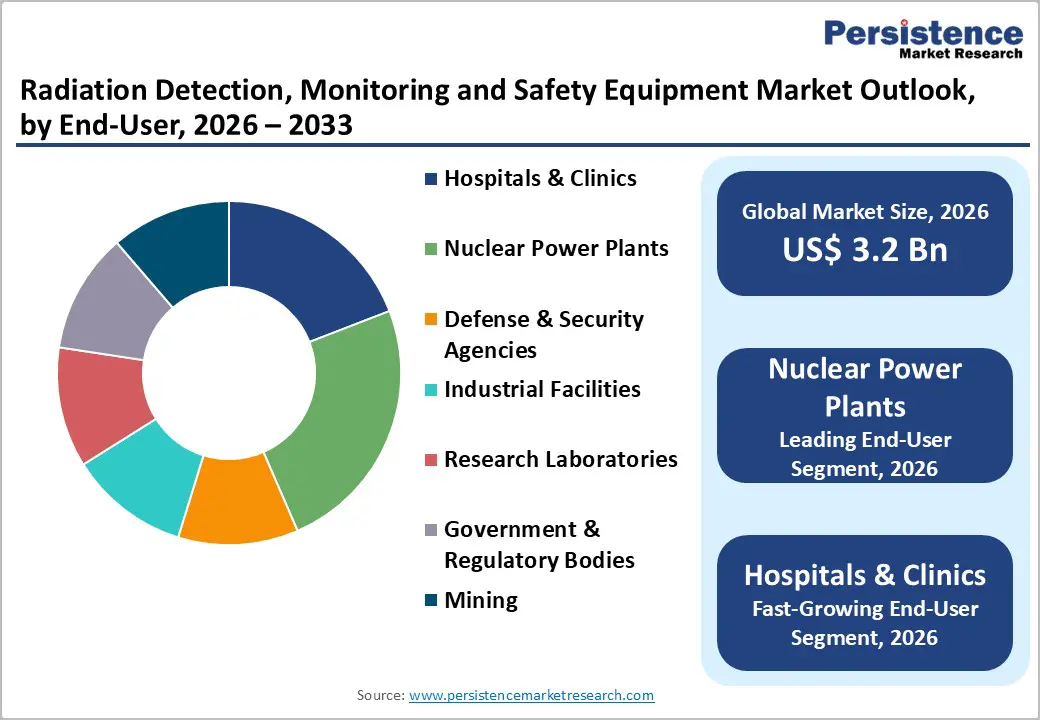

The global radiation detection, monitoring and safety equipment market size is expected to be valued at US$ 3.2 billion in 2026 and projected to reach US$ 5.2 billion by 2033, growing at a CAGR of 7.1% between 2026 and 2033.

The growth is driven by the global expansion of nuclear energy and stringent radiation safety regulations. With over 440 operational nuclear reactors worldwide requiring continuous monitoring, as reported by the International Atomic Energy Agency (IAEA), and more than 3.6 billion X-ray procedures performed annually according to the World Health Organization (WHO), demand for detection and safety equipment is rising. The market benefits from increasing safety compliance across healthcare, nuclear, and industrial sectors, alongside technological advancements in portable, wearable, and IoT-enabled monitoring solutions.

Key Industry Highlights:

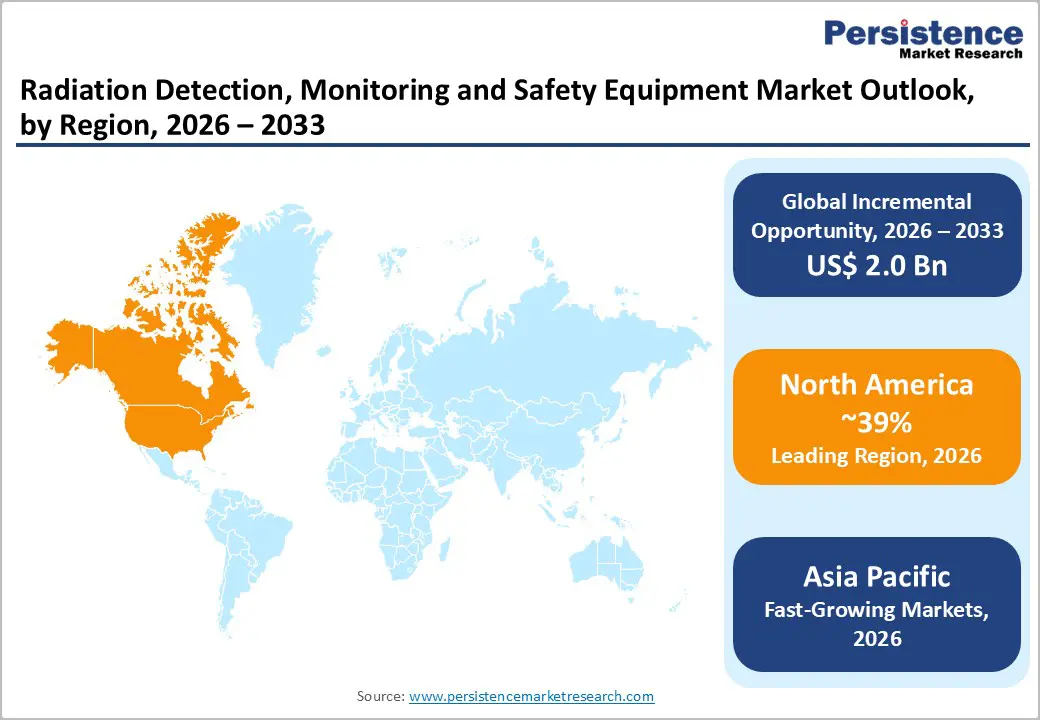

- Leading Region: North America leads the market with a 39% share in 2025, supported by mature U.S. nuclear infrastructure and stringent NRC regulatory compliance.

- Fastest-Growing Region: Asia Pacific is the fastest-growing region at an 8.7% CAGR (2025 - 2032), fueled by China and India nuclear expansion and regional manufacturing scale advantages.

- Leading Product Category: Detection & Monitoring Equipment dominates with 58% share in 2025, driven by mandatory real-time radiation monitoring across hospitals, nuclear, and industrial facilities.

- Fastest-Growing Product Category: Safety Equipment is the fastest-growing product segment, driven by rising adoption of wearable and shielding solutions across healthcare, nuclear, and industrial sectors.

- Key Market Opportunity: Global nuclear decommissioning of 120+ reactors and high-radiation field applications present high-margin growth potential for specialized detection systems.

| Key Insights | Details |

|---|---|

| Radiation Detection, Monitoring and Safety Equipment Size (2026E) | US$ 3.2 billion |

| Market Value Forecast (2033F) | US$ 5.2 billion |

| Projected Growth CAGR (2026 - 2033) | 7.1% |

| Historical Market Growth (2020 - 2025) | 7.8% |

Market Dynamics

Drivers - Global Nuclear Power Capacity Expansion Driving Radiation Equipment Demand

The global push toward nuclear energy as a low-carbon solution is a key driver for the Radiation Detection, Monitoring and Safety Equipment market. According to the International Atomic Energy Agency (IAEA), 54 reactors are currently under construction worldwide, with over 100 more planned through 2033. China alone targets 150 new reactors by 2035, generating substantial demand for detection and monitoring infrastructure across the nuclear fuel cycle.

To meet compliance, nuclear facilities invest heavily in fixed monitoring systems, personal dosimeters, and integrated safety solutions aligned with standards like 10 CFR 20 in the U.S. and equivalent international regulations. This ongoing nuclear expansion ensures sustained market growth, long-term stability, and continuous opportunities for vendors supplying advanced detection, safety, and monitoring technologies.

Stringent Occupational Radiation Safety Regulations Fuel Market Growth

Worldwide regulatory authorities enforce strict limits on occupational radiation exposure, creating a strong market pull for advanced detection and safety equipment. In the U.S., the Nuclear Regulatory Commission mandates real-time monitoring to keep worker doses below 50 mSv annually, while EURATOM sets limits of 20 mSv across Europe. Over 1.2 million U.S. workers exposed to ionizing radiation require compliant protective devices and monitoring systems.

Healthcare and industrial sectors also face stringent regulatory oversight, with the FDA ensuring approved standards for diagnostic imaging and radiation-emitting devices. These enforceable regulations drive consistent replacement cycles, encourage adoption of technological upgrades, and expand demand for portable, wearable, and fixed radiation safety solutions across multiple end-use industries.

Restraints - High Capital Investment and Maintenance Costs Limit Market Growth

Advanced radiation detection and monitoring systems rely on costly scintillation crystals, semiconductor detectors, and precision electronics, driving high acquisition expenses. Fixed area monitoring stations can cost between US$ 25,000-75,000, with annual calibration and maintenance adding 15-20% of the initial investment. IAEA assessments indicate that 65% of industrial facilities in developing countries still operate legacy analog systems due to budget constraints.

Small hospitals, clinics, and research laboratories often face chronic financial limitations, delaying upgrades to modern detection and safety equipment. These high capital and ongoing operational costs restrict market penetration in emerging regions, slowing adoption of advanced, technologically sophisticated radiation monitoring and safety solutions despite rising regulatory and operational demand.

Shortage of Trained Radiation Safety Professionals Hinders Adoption

Modern radiation detection systems require specialized personnel for accurate operation, calibration, and data analysis, creating a workforce dependency that limits market growth. The International Labour Organization (ILO) estimates a global shortage of 75,000 qualified radiation safety officers, while the World Health Organization (WHO) reports only 25% of healthcare facilities maintain adequate staffing for radiation safety compliance.

Integration with SCADA, building management, and monitoring networks further complicates deployment, particularly for small and medium-sized enterprises lacking technical expertise. This skills gap slows adoption of advanced detection technologies, reduces operational efficiency, and presents a significant barrier for vendors aiming to expand in emerging and resource-constrained markets.

Opportunities - Medical Radiation Safety System Modernization Presents Significant Opportunities

Rising cancer incidence is driving rapid expansion of diagnostic imaging and radiotherapy, creating urgent demand for radiation safety equipment. The World Health Organization (WHO) projects a 60% increase in cancer cases by 2040, accelerating deployment of CT scanners, PET systems, and radiotherapy units that require comprehensive staff protection. In 2025, the U.S. FDA approved 28 new dosimetry devices, reflecting innovation and adoption potential.

Hospitals in Asia Pacific expanding radiotherapy capacity by 35% represent prime growth markets for advanced detection solutions. AI-enabled real-time exposure tracking systems offer premium pricing potential while ensuring compliance with the ALARA (As Low As Reasonably Achievable) principle across healthcare networks, enhancing operational safety and driving sustained market expansion.

Nuclear Decommissioning and Radioactive Waste Management Drive Market Expansion

Aging nuclear reactors scheduled for retirement are creating substantial opportunities for specialized radiation detection equipment. The International Atomic Energy Agency (IAEA) identifies over 120 commercial reactors set for decommissioning through 2033, each requiring robust monitoring systems to ensure safe dismantling and handling of radioactive materials. Fukushima cleanup operations, for example, deploy thousands of ruggedized detectors capable of measuring extreme radiation fields exceeding 100 mSv/h.

Europe faces 25 GW of nuclear capacity retirement by 2035, according to the World Nuclear Association, highlighting the growing need for modular, intrinsically safe detection systems. These solutions, designed for contaminated zone characterization, represent high-margin growth segments for manufacturers targeting decommissioning, waste management, and environmental monitoring applications.

Category-wise Analysis

Product Type Insights

Detection & monitoring equipment leads with a 58% share in 2025, driven by mandatory real-time radiation hazard identification across heavily regulated sectors. In the U.S., NRC regulations require continuous area monitoring in 95% of nuclear facilities, emphasizing detection systems over personal protective equipment. Hospitals rely on Geiger-Müller counters and ion chambers for daily radiopharmaceutical scans, while DOE records indicate annual deployment of over 750,000 units. Advanced features such as automated alarming, data logging, and regulatory reporting reinforce this segment’s dominance.

Safety Equipment is the fastest-growing product segment, driven by rising awareness of personnel protection and shielding requirements across healthcare, nuclear, and industrial applications. Modern protective gear, barriers, and interlock systems are increasingly integrated with digital monitoring technologies. Hospitals, research labs, and industrial facilities are upgrading to ergonomic and wearable protection solutions, meeting both compliance mandates and evolving workforce safety expectations.

Technology Analysis

Scintillators maintain market leadership with a 42% share in 2025 due to exceptional gamma spectroscopy performance and high energy resolution. NIST benchmarks confirm 97% energy resolution versus 75% for gas-filled technologies. EURATOM mandates scintillator-based monitoring for nuclear fuel cycle compliance across EU member states. NaI(Tl) and CsI(Tl) crystals dominate SPECT medical imaging, while over 400 operational reactors globally deploy scintillator arrays, demonstrating durability in harsh radiation environments.

Solid-State Detectors are the fastest-growing technology, favored for compact design, higher sensitivity, and low-power operation. Semiconductor detectors, including CZT and Si-based systems, are increasingly adopted in portable, wearable, and field-deployable monitoring equipment. Applications in medical diagnostics, nuclear inspection, and industrial safety benefit from rapid response times and compatibility with IoT-enabled real-time monitoring networks, driving adoption across multiple end-use sectors.

Mode of Operation Insights

Fixed/stationary systems hold a 52% market share in 2025, providing continuous monitoring for critical infrastructure. IAEA safety standards require perimeter coverage for 85% of nuclear facility controlled areas. Integration with PLC and SCADA systems enables automated alarming, trend analysis, and regulatory reporting. Oil & gas and uranium mining operations deploy fixed NORM monitors across 10,000+ sites globally, ensuring uninterrupted worker safety and environmental compliance.

Portable/Handheld systems are the fastest-growing mode, gaining traction due to flexibility and rapid deployment in field operations. Handheld survey meters, portable dosimeters, and mobile gamma spectrometers enable on-the-spot monitoring for nuclear, defense, and industrial facilities. These devices support emergency response, temporary site monitoring, and mobile inspection needs, driving demand for lightweight, rugged, and user-friendly solutions.

End-user Insights

Nuclear power plants dominate with a 37% share in 2025, fueled by stringent safety requirements throughout the fuel cycle. The World Nuclear Association reports 443 operable commercial reactors globally, each requiring continuous radiation surveillance under G-21/GM-10 guidelines. Post-Fukushima investments exceed US$ 15 million per site annually for comprehensive system upgrades. 10 CFR 50 licensing and General Design Criteria 64 mandate redundant detection systems, ensuring sustained demand from construction through decommissioning phases.

Healthcare facilities and research laboratories represent the fastest-growing end-users, driven by expanding diagnostic imaging, radiotherapy, and radiopharmaceutical applications. Hospitals increasingly deploy modern detection and monitoring solutions, including wearable dosimeters and AI-enabled exposure tracking systems. Academic and industrial research labs adopt compact, high-precision detectors for radiological experiments, safety compliance, and regulatory reporting, creating a strong growth trajectory in these sectors.

Regional Insights

North America Radiation Detection, Monitoring and Safety Equipment Market Trends

North America holds a 39% share in 2025, maintaining global leadership through a mature commercial nuclear power infrastructure and strict NRC regulatory oversight. U.S. Department of Energy (DOE) national laboratories advance next-generation HPGe detectors and fiber optic sensing technologies across 14 R&D facilities. Annual defense budgets of US$ 850 billion support deployment of radiation portal monitors at 350+ land border crossings and major seaports.

The region’s healthcare sector drives further demand, with the FDA approving 32 innovative dosimetry devices in 2025. Hospitals and clinics implement state-of-the-art monitoring solutions to ensure staff safety and regulatory compliance. Strong investments in nuclear, defense, and medical applications reinforce North America’s dominant market position and provide long-term stability for radiation detection and safety equipment manufacturers.

Europe Radiation Detection, Monitoring and Safety Equipment Market Trends

Europe exhibits steady growth, with a projected CAGR of 6.2% from 2025 to 2032, supported by harmonized EURATOM safety standards. France’s 56 operating reactors, supplying 70% of national electricity, drive continuous investment in monitoring infrastructure under ASN mandates. Germany’s nuclear phase-out accelerates decommissioning radiation monitoring demand across six reactor sites, while the U.K.’s Hinkley Point C EPR deployment incorporates 200+ fixed detection stations. Spain expands Trillo NPP safety instrumentation per CSN directives, ensuring compliance with stringent regional safety standards.

Industrial, research, and healthcare applications further contribute to market growth, with adoption of advanced scintillator and solid-state detection technologies. The region benefits from consistent regulatory enforcement, standardized operational procedures, and long-term modernization projects across nuclear, medical, and industrial sectors.

Asia Pacific Radiation Detection, Monitoring and Safety Equipment Market Trends

Asia Pacific is the fastest-growing region with an 8.7% CAGR from 2025 to 2032, driven by rapid nuclear expansion and industrial modernization. China has 27 reactors under construction, while India pursues a 22 GW nuclear capacity expansion per Department of Atomic Energy targets. Japan has restarted 12 reactors post-Fukushima with enhanced monitoring systems, reflecting strengthened regulatory focus.

The region’s industrial and manufacturing sectors leverage China’s production scale to reduce system costs by 25% compared to Western suppliers. Korea Hydro & Nuclear Power exports incorporate domestic scintillator array technologies compliant with IAEA safeguards. Rising adoption across healthcare, nuclear, and industrial applications, coupled with cost advantages and technology upgrades, positions Asia Pacific as a high-potential growth market for radiation detection and safety solutions.

Competitive Landscape

The global radiation detection, monitoring and safety equipment market is moderately consolidated, with leading players leveraging sustained R&D investment and strategic acquisitions of complementary technologies. Vendors differentiate through IoT-enabled predictive maintenance, digital twin analytics, and advanced detection capabilities, establishing strong competitive advantages and premium positioning over standard equipment. Market participants focus on customizing solutions to meet strict regulatory requirements such as NRC and EURATOM standards. Emerging subscription-based SaaS monitoring platforms offer cost-effective alternatives, reducing capital expenditure for smaller end-users. Innovation, regulatory compliance, and tailored service offerings remain key factors shaping competition and driving long-term market leadership.

Key Developments:

- In February 2025, Mirion Technologies launched IC3™ Portable Ion Chamber specifically designed for nuclear power plants and radiopharmaceutical production facilities, featuring simultaneous gamma/beta/X-ray measurement capability with full IAEA safeguards compliance.

- In June 2025, Smith’s Detection introduced AI-powered handheld radiation detectors improving border security threat identification 45% faster through machine learning pattern recognition algorithms.

- In March 2024, FLIR Systems deployed next-generation scintillator detector modules meeting enhanced EURATOM 2013/59 basic safety standards across European Union nuclear facilities and research centers.

Companies Covered in Radiation Detection, Monitoring and Safety Equipment Market

- Thermo Fisher Scientific Inc.

- Electronic & Engineering Company (I) P. Ltd.

- LND, INC

- Burlington Medical.

- RadComm Systems

- Scionix Holland B.V.

- Centronic

- Trivitron Healthcare

- ATOMTEX

- Landauer

- Nucleonix Systems

- Teledyne FLIR LLC

- Mirion Technologies, Inc.

- Arrow-Tech, Inc.

- Ludlum Measurements, Inc.

Frequently Asked Questions

The market is projected to reach US$ 3.2 billion in 2026, expanding to US$ 5.2 billion by 2033 exhibiting 7.1% CAGR driven by global nuclear safety investments.

Global nuclear expansion with 54 reactors under construction, combined with IAEA and NRC occupational safety mandates, drives detection and monitoring equipment demand.

Scintillators lead with 42% market share in 2025, offering 97% gamma spectroscopy accuracy required by EURATOM and NRC safety standards.

North America dominates with 39% share in 2025, supported by established nuclear infrastructure, DOE R&D initiatives, and strict NRC regulatory oversight.

Decommissioning 120+ commercial reactors worldwide create high-margin demand for specialized high-radiation field detection and monitoring systems.

The radiation, detection, monitoring and safety equipment market is led by companies including Thermo Fisher Scientific Inc., Electronic & Engineering Company (I) P. Ltd., LND, INC, Burlington Medical, and RadComm Systems.