- Food Ingredients & Additives

- Food Safety Testing Services Market

Food Safety Testing Services Market Size, Share, Growth, and Regional Forecast, 2026 to 2033

Food Safety Testing Services Market by Test (Allergen Testing, Chemical and Nutritional Testing, Genetically Modified Organism Testing, Microbiological Testing, Residue and Contamination Testing, Others), Application (Meat, Poultry and Seafood Products, Dairy and Dairy Products, Beverages, Processed Food, Cereals & Grains), Technology (Polymerase Chain Reaction (PCR), Immunoassay-based, Chromatography and Spectrometry, Others), and Regional Analysis from 2026 to 2033

Food Safety Testing Services Market Share and Trends Analysis

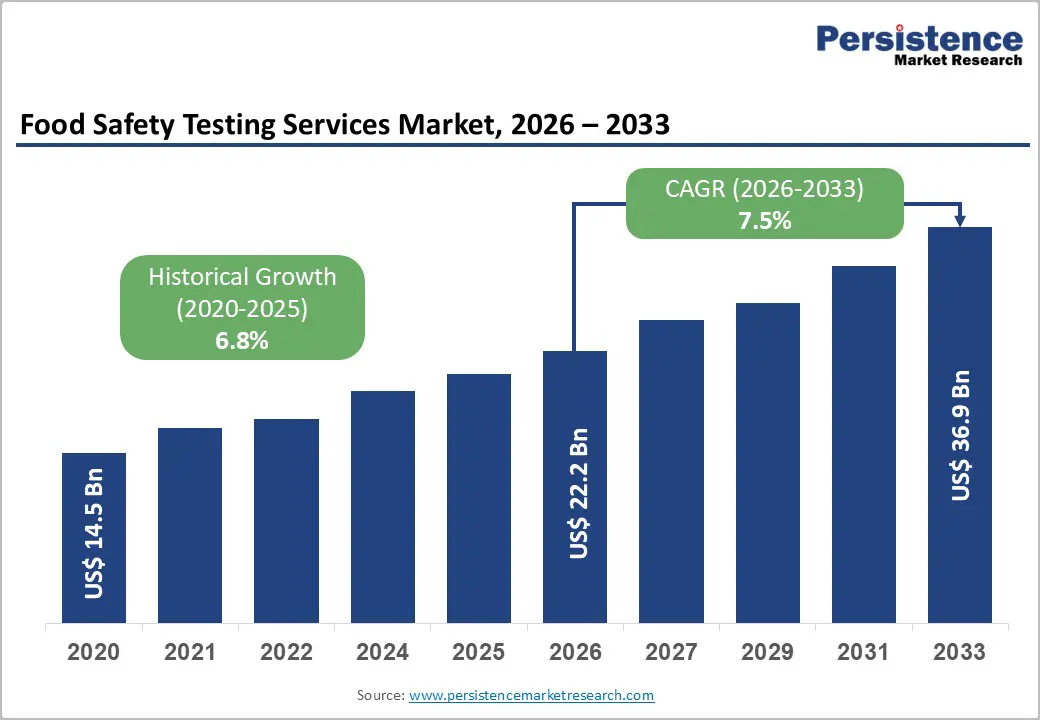

The global food safety testing services market is estimated to grow from US$ 22.2 Bn in 2026 to US$ 36.9 Bn by 2033. The market is projected to record a CAGR of 7.5% during the forecast period from 2026 to 2033.

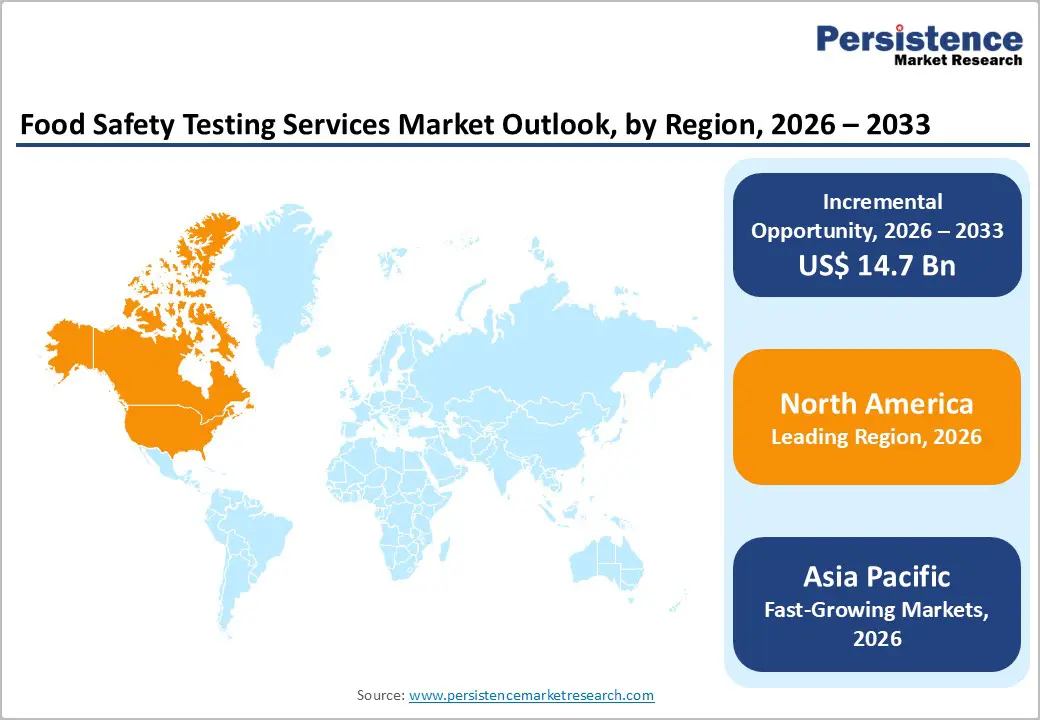

The food safety testing services industry is expanding steadily, driven by rising food safety regulations, increasing consumer awareness, and demand for contaminant-free products. North America leads, supported by stringent regulatory frameworks and advanced testing infrastructure. The Asia-Pacific region is the fastest-growing region, driven by rapid industrialization, rising food exports, and intensified regulatory enforcement across emerging markets.

Key Industry Highlights

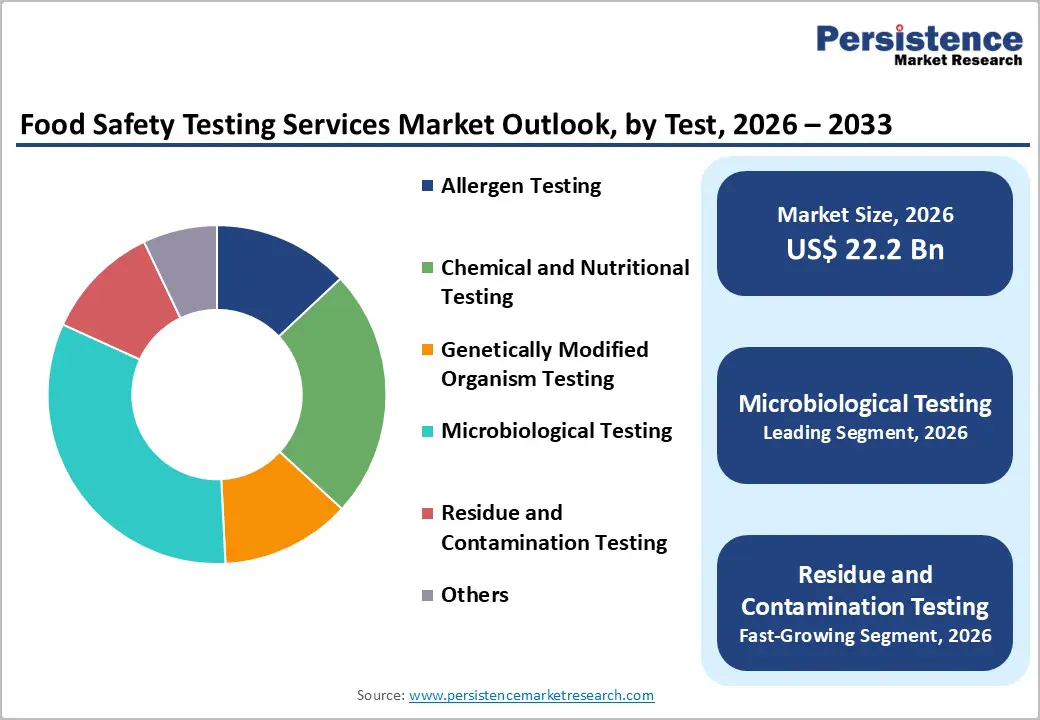

- Dominant Segment: Microbiological testing accounts for 32.6% of the Food Safety Testing Services Market in 2025, driven by high demand for pathogen detection, regulatory compliance, and routine food safety monitoring across meat, dairy, and processed foods.

- Dominant Region: North America leads the market in 2025, with a 39.5% share, owing to stringent regulations, advanced laboratory infrastructure, and high adoption of testing services. Asia-Pacific is the fastest-growing region, supported by increasing food production, rising exports, and strengthening regulatory frameworks.

- Market Drivers: Growth is fueled by rising food safety regulations, increasing consumer awareness of contaminants, globalization of food trade, and demand for safe, high-quality products.

- Market Opportunity: Key opportunities include the development of rapid and automated testing solutions, expansion in emerging markets, integration of digital monitoring tools, advanced pathogen detection technologies, and growth in specialized testing for allergens, residues, and GMOs.

| Global Market Attributes | Key Insights |

|---|---|

| Food Safety Testing Services Market Size (2026E) | US$ 22.2 Bn |

| Market Value Forecast (2033F) | US$ 36.9 Bn |

| Projected Growth (CAGR 2026 to 2033) | 7.5% |

| Historical Market Growth (CAGR 2020 to 2025) | 6.8% |

Market Dynamics

Driver - Increasing Foodborne Illnesses

Foodborne illnesses represent a major and growing public health challenge, directly increasing demand for comprehensive food safety testing services. According to the U.S. Centers for Disease Control and Prevention (CDC), an estimated 48 million Americans fall ill from foodborne disease annually, leading to approximately 128000 hospitalizations and 3000 deaths each year. These illnesses are caused by pathogens such as norovirus, nontyphoidal Salmonella, Campylobacter, and E. coli, highlighting the persistent risk of contamination across the food supply chain. The continued high number of cases signals ongoing vulnerabilities in food production and handling that necessitate rigorous testing for prevention and control.

Globally, the World Health Organization (WHO) estimates that unsafe food results in about 600 million cases of foodborne diseases and 420000 deaths annually, affecting nearly one in ten people worldwide. This global burden, ranging from microbial pathogens to chemical contaminants, underscores the need for comprehensive testing services to safeguard public health and maintain confidence in food systems. Expansion of international trade and more complex supply chains further amplify these risks, as contaminated products can rapidly cross borders. These trends drive growth in food safety testing services to detect hazards earlier and reduce illness incidence.

Restraints - Lack of Skilled Workforce

A critical restraint on the food safety testing services market is the shortage of skilled laboratory personnel capable of performing complex analytical, microbiological, and chemical tests. In the United States, clinical laboratory workforce surveys show that vacancy rates in clinical labs range from 7-11% and can exceed 25% in some areas, indicating significant understaffing among trained lab technologists and technicians. The Bureau of Labor Statistics (BLS) projects demand for laboratory technologists and technicians to grow by 11% through 2030, yet the number of accredited training programs and graduates remains insufficient to meet this increase. This mismatch between workforce supply and testing needs limits food safety laboratories' capacity to expand services.

Globally, shortages of qualified laboratory personnel extend beyond clinical settings to food safety and public health laboratories. Estimates indicate that only about 4,900 students graduate annually from medical laboratory science and technician programs in the U.S., yet there are more than 9,000 job openings, suggesting a vacancy rate of roughly 46%for these roles. Moreover, surveys report that 80% of laboratories have open positions for medical laboratory scientists, underscoring widespread staffing gaps. These workforce shortfalls lead to delays in testing, increased workloads for existing staff, and impede food safety testing services' ability to respond promptly to contamination risks and regulatory demands.

Opportunity - Rapid & Automated Testing Solutions

Rapid and automated food safety testing technologies significantly enhance the speed and efficiency of hazard detection compared with traditional culture-Based methods that can take 2-7 days to yield results. Modern rapid pathogen detection methods, including PCR and other molecular techniques, can deliver actionable results in minutes or hours, enabling food producers and regulators to make immediate decisions on product safety and prevent contaminated batches from entering the supply chain. This reduction in turnaround time is critical for minimizing public health risk and reducing costly recalls. Rapid indicator tests integrated into routine monitoring provide results on the same day, enabling real-time safety management at critical control points, such as processing lines or before distribution.

Government and public health agencies increasingly recognize the value of rapid methods for surveillance and outbreak response. For example, culture-independent diagnostic tests (CIDTs) used in foodborne disease surveillance have been adopted to accelerate pathogen detection, demonstrating that diagnostic innovation enables earlier intervention during contamination events. Although traditional culture techniques remain foundational for confirmatory testing and detailed strain characterization, rapid methods bolster overall system responsiveness. The ability of rapid tests to deliver screening results quickly helps food businesses comply with regulatory standards and support consumer safety and confidence in the food supply.

Category-wise Analysis

By Test, Microbiological Testing Dominates the Food Safety Testing Services Market

Microbiological testing accounts for 32.6% of the global market in 2025, as it directly addresses the primary cause of foodborne illnesses by detecting harmful bacteria, viruses, yeasts, and parasites that contaminate food. The World Health Organization estimates that unsafe food contaminated with microbial pathogens causes over 200 diseases and results in approximately 600 million illnesses and 420 000 deaths worldwide annually, underscoring the critical need for pathogen detection across the supply chain. Government food safety authorities such as the U.S. FDA emphasize microbiological safety as central to preventing foodborne outbreaks and protecting public health through targeted hazard control and surveillance. Because microbes can proliferate at low doses and spread rapidly through distribution networks, routine microbiological analysis remains essential for regulatory compliance and consumer protection, giving this test type the largest share of global food safety testing activities.

By Application, Meat, Poultry and Seafood Products dominates due to high pathogen risk, frequent contamination, and strict safety regulations

Meat, poultry, and seafood dominate the food safety testing services market because these products are consistently associated with a high burden of serious foodborne illnesses, thereby driving extensive testing demand. According to the U.S. CDC Interagency Food Safety Analytics Collaboration, animal-origin foods such as chicken, pork, turkey, and beef are major contributors to Salmonella illnesses, with chicken alone accounting for nearly one-fifth of cases in outbreak data. Meat and poultry are also the most common sources of fatal infections, largely due to pathogens such as Salmonella and Listeria that thrive in these products. This link to severe illness necessitates rigorous microbiological and residue testing throughout processing and distribution to protect public health and comply with safety regulations.

Regional Insights

North America Food Safety Testing Services Market Trends

North America dominates the food safety testing services market, with a 39.5% share in 2025, owing to rigorous regulatory enforcement, high testing volumes, and established laboratory infrastructure. In the United States alone, public health surveillance systems such as PulseNet link DNA fingerprints of foodborne pathogens from over 80 public health laboratories, enabling rapid identification and investigation of outbreaks. The U.S. FDA reports conducting millions of analytical tests annually for pathogens, toxins, and contaminants in imported and domestic foods to enforce standards under laws such as the Food Safety Modernization Act (FSMA). The USDA’s Food Safety and Inspection Service (FSIS) tests meat and poultry for pathogens such as Salmonella and E. coli in hundreds of thousands of samples each year to protect consumers. These extensive, government-mandated testing programs drive high demand for food safety testing services across North America.

Europe Food Safety Testing Services Market Trends

Europe is a key region in the food safety testing services market owing to stringent regulatory standards, widespread foodborne illness surveillance, and strong consumer awareness of food safety. The WHO reports that over 23-million Europeans suffer from foodborne illnesses annually, resulting in approximately 4,700 deaths, with pathogens like Salmonella, Campylobacter, STEC, and Listeria driving most outbreaks. The European Food Safety Authority (EFSA) and the European Centre for Disease Prevention and Control (ECDC) implement rigorous monitoring programs that require routine microbiological, chemical, and residue testing of meat, dairy, seafood, and processed foods. A strong public health emphasis, combined with harmonized EU regulations and advanced laboratory infrastructure, ensures consistent demand for comprehensive food safety testing services, positioning Europe as a critical and influential market for global food safety initiatives.

Asia-Pacific Food Safety Testing Services Market Trends

The Asia-Pacific region is the fastest-growing in the food safety testing services market because foodborne illnesses impose an exceptionally high public health burden and drive demand for enhanced testing and controls. In the WHO South-East Asia Region alone, more than 150 million people fall ill and about 175000 die from foodborne diseases annually, with children under five especially affected, reflecting widespread contamination and hygiene challenges. Similarly, in the broader Asia-Pacific region, unsafe food causes over 275 million illnesses and 225000 deaths each year, highlighting both the scale of risk and the need for expanded safety monitoring and testing. Government recognition of these health impacts and efforts to strengthen food safety systems accelerate the adoption of testing services across rapidly developing economies.

Market Competitive Landscape

Leading food safety testing services focus on microbiological, chemical, and allergen testing across meat, dairy, and processed foods. By ensuring regulatory compliance, preventing contamination, and supporting public health, they enhance food safety, enable rapid outbreak response, and build consumer confidence, driving demand and fueling growth in the global Food Safety Testing Services Market.

Key Industry Developments:

- In August 2025, Bio-Rad Laboratories announced that it had launched the EZ-Check Salmonella spp. Kit, a rapid qualitative test for detecting Salmonella species in a wide range of food and environmental samples. The kit, which used real-time PCR technology with read-to-use reagents, was validated by AOAC International under the Performance Tested Methods program and received NF VALIDATION certification from AFNOR Certification, confirming its robustness and accuracy..

- In March 2025, Bio-Rad Laboratories announced it had launched the XP-Design Assay Salmonella Serotyping Solution, a new tool designed for rapid and accurate detection and characterization of Salmonella species in food and environmental samples.

Companies Covered in Food Safety Testing Services Market

- Adpen Laboratories

- Aegis Food Testing Laboratories (Vanguard Sciences)

- ALS Limited

- Asureuality Limited

- Avomeen Analytical Services

- Bio-Rad Laboratories

- Bureau Veritas SA

- Campden BRI

- Det Norske Vertias AS (DNV)

- EMSL Analytical Inc.

- Others

Frequently Asked Questions

The global food safety testing services market is projected to be valued at US$ 22.2 Bn in 2026.

Rising foodborne illnesses, strict regulations, consumer awareness, global trade, and demand for safe, quality foods.

The global food safety testing services market is poised to witness a CAGR of 7.5% between 2026 and 2033.

Rapid testing solutions, automation, emerging markets, allergen detection, digital traceability, and specialized contaminant testing expansion.

Adpen Laboratories, Aegis Food Testing Laboratories (Vanguard Sciences), ALS Limited, Asureuality Limited, Avomeen Analytical Services, Bio-Rad Laboratories.