- Transportation & Logistics

- Forklift Truck Safety Solutions Market

Forklift Truck Safety Solutions Market Size, Share, Trends, Growth, Forecasts 2026 - 2033

Forklift Truck Safety Solutions Market by Product (Proximity Sensors, Camera Systems, Safety Lighting, Others), Industry (Manufacturing, Warehousing, Distribution Centers, Logistics, Others), and Regional Analysis 2026 - 2033

Forklift Truck Safety Solutions Market Share and Trends Analysis

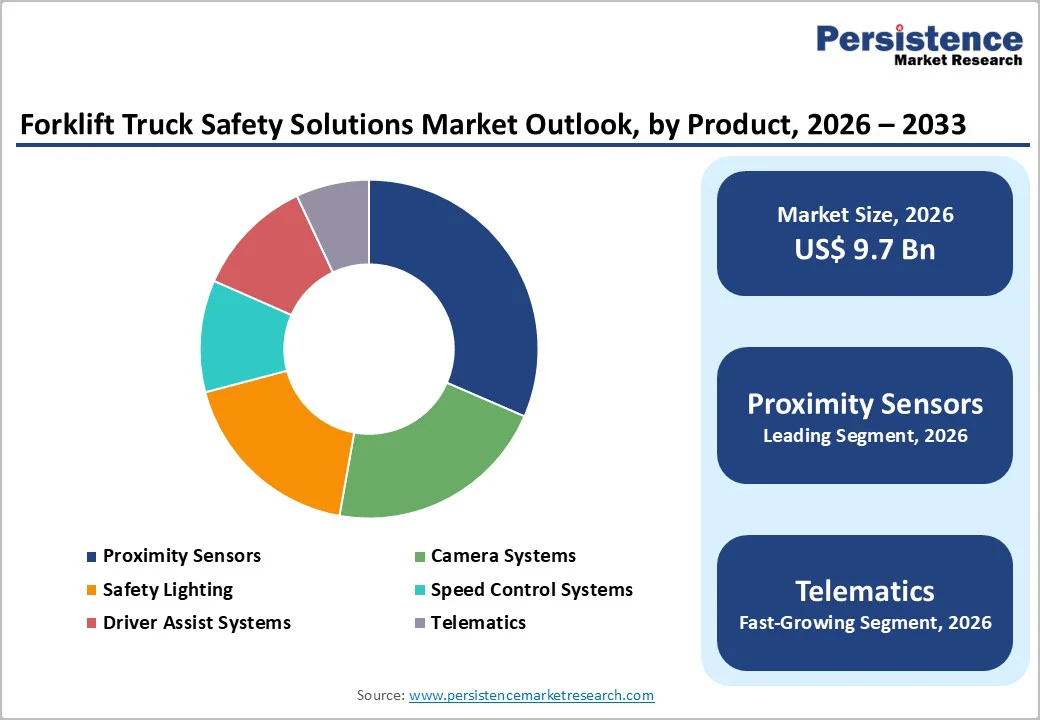

The global forklift truck safety solutions market size is likely to value at US$9.7 billion in 2026 and is projected to reach US$24.6 billion by 2033, growing at a CAGR of 14.2% between 2026 and 2033.

This rapid growth is powered by increasing workplace safety regulations, surging automation in material handling, and the steady expansion of global logistics and e-commerce sectors. Technological convergence, especially integrations of AI, IoT, and telematics, enables more advanced incident prevention and operational efficiency.

The market’s expansion remains strongly linked to end-user industry adoption dynamics, especially within manufacturing, warehousing, and distribution.

Key Industry Highlights:

- Proximity Sensors Leadership: Proximity sensors command 31.5% market share as the primary collision-prevention technology, with documented incident reductions of 50-65% across deploying facilities, demonstrating category dominance driven by regulatory mandates and proven safety effectiveness.

- Telematics Growth Acceleration: Telematics solutions are the fastest-growing product segment, with a 16.9% CAGR, reflecting market evolution from point-solution safety systems to comprehensive fleet intelligence platforms integrating GPS tracking, predictive analytics, and remote diagnostics.

- Manufacturing and Warehousing Dominance: The manufacturing sector leads with 33.8% market share, while warehousing expands fastest at 15.1% CAGR, reflecting e-commerce fulfillment infrastructure acceleration and corresponding logistics modernization requirements.

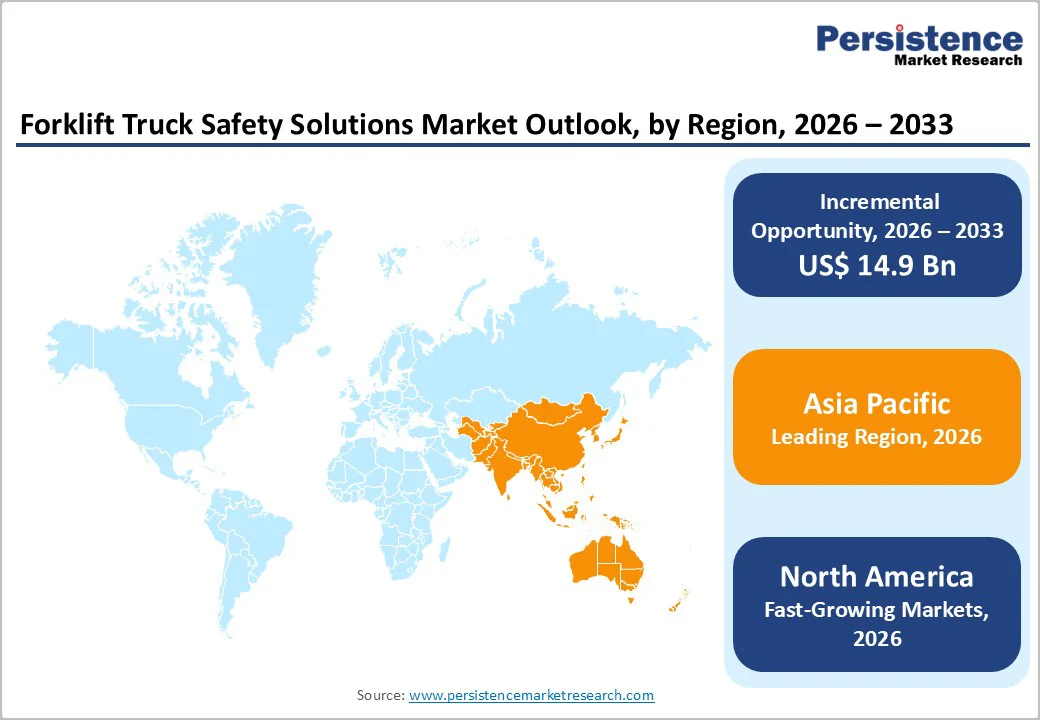

- Asia Pacific Regional Leadership: Asia Pacific dominates with 39% global market share and the highest growth rate at 15.6% CAGR, with China commanding 45% of the regional autonomous forklift market, indicating a structural shift of materials handling innovation and deployment toward the Asia Pacific region.

- Regulatory and Compliance Drivers: Stringent OSHA compliance requirements, EU machinery directives, and workplace safety mandates create non-discretionary technology adoption requirements, establishing regulatory compliance as the primary market growth catalyst independent of economic cyclicality.

| Key Insights | Details |

|---|---|

| Forklift Truck Solutions Market Size (2026E) | US$ 9.7 billion |

| Market Value Forecast (2033F) | US$ 24.6 billion |

| Projected Growth CAGR (2026 - 2033) | 14.2% |

| Historical Market Growth (2020 - 2025) | 11.8% |

Market Dynamics Analysis

Driver - Stringent Regulatory Compliance and Workplace Safety Mandates

Occupational safety regulations are a major catalyst in the market, particularly as the Occupational Safety and Health Administration (OSHA) identifies forklifts as a leading cause of workplace injuries, with over 7,000 incidents annually in North America. OSHA Standard 1910.178 requires operator training, daily inspections, maintenance, and safety guards, driving the adoption of proximity detection systems, camera solutions, and automatic braking.

Regulatory enforcement in a few jurisdictions mandates collision avoidance technology for industrial vehicles, and the EU is enforcing machinery safety directives (Directive 2006/42/EC). India’s Factories Act also mandates operator certification and workplace safety systems.

These regulations create non-discretionary capital expenditures, exposing facilities to significant penalties for non-compliance. Additionally, government insurance incentives promote the adoption of safety technologies, offering a 12-18% reduction in premiums and reinforcing the economic justification for compliance, leading to sustained capital investment cycles regardless of economic conditions.

Explosive Growth in E-Commerce Logistics and Warehouse Automation Demand

E-commerce expansion has fundamentally transformed material handling economics. Global e-commerce revenues reached approximately US$5.8 trillion in 2024 and continue expanding at 8-12% annually, driving proportional growth in warehousing and distribution infrastructure.

Asia Pacific autonomous forklift adoption has accelerated dramatically, with China commanding 45% of the regional autonomous forklift market revenue in 2024, driven by the country's advanced manufacturing capabilities and fast-growing e-commerce market.

Logistics operators responded to accelerating fulfillment demands by increasing warehouse operational hours: forklift utilization rates have increased 37% since 2020 through the adoption of 24/7 warehouse operations and extended shift patterns.

This heightened utilization corresponds directly to elevated collision risk; warehouses operating extended hours experience measurable increases in operator fatigue, attention lapses, and accident frequency.

The market response manifests through technology adoption: sophisticated telematics systems enabling real-time fleet monitoring, fatigue-detection-enabled safety systems, and collision avoidance solutions have become operational necessities rather than optional upgrades.

Restraints - Capital Expenditure Barriers and Implementation Complexity

High implementation costs pose significant adoption constraints, particularly for small-to-medium enterprises (SMEs) and facilities in emerging market. Comprehensive forklift safety solutions spanning proximity sensors, camera systems, speed control mechanisms, and telematics platforms require capital investments ranging from US$8,000-15,000 per forklift unit, creating substantial budgetary commitments for facilities operating diverse equipment fleets.

Integration complexity adds further friction: retrofitting legacy forklift equipment with safety technologies requires technical expertise, operational downtime during installation, and workforce retraining, factors that are particularly burdensome for continuous-operation warehouses, where installation windows are severely constrained.

Regional economic variations heighten cost sensitivity, with developing economies in Southeast Asia, Latin America, and sub-Saharan Africa facing lower purchasing power parity. This makes safety technology investments particularly cost-sensitive. The lack of standardized interfaces between forklift manufacturers and safety solution providers leads to costly, customized implementations and longer deployment times.

Technical Standardization Challenges and Legacy Equipment Incompatibility

Fragmented industry standards and equipment diversity create significant technology integration constraints. Forklift manufacturers employ proprietary control architectures, communication protocols, and electrical systems that limit interoperability with third-party safety solutions.

The absence of unified global standards for sensor integration, data transmission protocols, and safety system architecture creates technical incompatibilities requiring custom engineering solutions on a per-equipment-model basis.

Legacy forklift fleets, particularly in manufacturing facilities with equipment ages exceeding 10-15 years, present fundamental compatibility challenges: retrofitting older equipment with modern wireless sensor networks often proves technically unfeasible or economically unjustifiable.

Wireless communication spectrum constraints in certain industrial environments, particularly facilities with RF-intensive manufacturing processes (welding operations, electromagnetic environments), necessitate alternative communication architectures that limit deployment flexibility. These technical barriers particularly impact small equipment manufacturers and regional safety solution providers, who lack resources to engineer solutions across diverse equipment platforms.

Opportunity - Integration of Advanced Driver Assistance Systems (ADAS) and Autonomous Vehicle Readiness

The autonomous vehicle ecosystem, ranging from fully autonomous forklifts to semi-autonomous collaborative robots operating in mixed human-robot environments, presents substantial opportunities for technological convergence. Current autonomous forklift market valuations indicate US$4.8 billion in 2025, expanding to US$11.1 billion by 2033 (11% CAGR), demonstrating rapid adoption momentum.

Safety solutions enabling mixed-mode warehouse operations, in which human operators and autonomous vehicles operate in shared facility spaces, require advanced perception systems, real-time threat detection, and predictive path-planning algorithms.

This convergence creates high-value solution opportunities: companies integrating collision avoidance systems with autonomous navigation architectures command estimated technology premiums of 35-50% compared to standalone safety solutions.

Complementary technologies, such as automatic braking systems, lane departure warning mechanisms, and adaptive cruise control, proven in automotive industry implementations, present transfer opportunities to material handling applications.

Sustainability Alignment and Fleet Electrification Economics

Fleet electrification trends create integrated optimization opportunities combining safety and environmental performance objectives. Electric forklift adoption is expanding significantly, with the Asia-Pacific market demonstrating particularly strong growth as logistics operators transition from combustion-engine equipment to battery-electric platforms.

Modern electric forklifts inherently integrate advanced telematics through battery management systems, creating a cost-effective foundation for comprehensive safety solution deployment.

Electrification enables new safety capabilities: real-time energy management data correlates with operator fatigue patterns and driving behavior modifications, supporting predictive collision risk assessment.

Sustainability-focused warehouse operators, particularly major retailers and third-party logistics (3PL) providers, prioritize electric fleet deployment aligned with corporate carbon neutrality commitments, creating procurement preferences for safety solutions seamlessly integrated with electrified equipment.

This sustainability-safety convergence opportunity, estimated at US$1.8-2.4 billion through 2033, enables solution providers to address multiple customer priorities, safety, environmental performance, and operational cost reduction, within a unified technological architecture.

Category-wise Analysis

Product Type Insights

Proximity sensors hold a 31.5% market share, maintaining clear leadership in the forklift truck safety solutions market. Their dominance stems from serving as the core collision-prevention technology, enabling real-time detection of obstacles, equipment, and personnel without operator input.

The segment includes ultrasonic sensors for cluttered environments, laser sensors for millimeter-level outdoor precision, and infrared sensors effective under variable lighting. Adoption is strongly reinforced by OSHA safety directives, which emphasize the use of collision-detection systems.

Their lower cost per unit enables rapid fleet deployment, with industrial facilities reporting 50-65% reductions in collision incidents, lowering downtime, insurance exposure, and worker compensation expenses.

Telematics is the fastest-growing product category, with a 16.9% CAGR, reflecting a shift toward integrated intelligence platforms over basic collision alerts. These systems unify GPS tracking, fleet management software, remote diagnostics, and real-time analytics to optimize fleet efficiency, cut travel, and reduce downtime. Advanced analytics detect fatigue and risky behavior while predicting failures.

Industry Insights

Manufacturing holds a dominant 33.8% share of the forklift truck safety solutions market, driven by intensive material-handling activity and stringent regulatory oversight. Manufacturing environments feature dense traffic zones, frequent human-equipment interactions, and continuous forklift use, elevating collision exposure and accelerating the adoption of safety technology.

Proximity sensors and collision avoidance systems show the strongest penetration due to their cost-effectiveness and alignment with factory risk profiles. Facilities implementing structured safety programs report 40-55% reductions in worker compensation claims and 30-45% improvements in audit compliance. Industry 4.0-enabled plants are seeing increased adoption as operational monitoring and real-time safety analytics converge.

Warehousing is the fastest-growing end-use segment, advancing at 15.1 percent CAGR as e-commerce fulfillment accelerates modernization cycles and elevates safety technology adoption. Rising 24/7 operational intensity and higher forklift utilization heighten collision risks, driving strong demand for telematics and fleet management solutions.

Third-party logistics providers adopt standardized safety frameworks, while the Asia Pacific leads global warehousing growth due to dominant e-commerce volumes and expanding regional logistics infrastructure.

Regional Market Insights

North America Forklift Truck Safety Solutions Market Trends

North America maintains a significant market presence with a prominent growth trajectory at 13.9% CAGR. The United States market leads regional performance, driven by OSHA's stringent regulatory framework, high labor costs that create an economic justification for automation, and a mature industrial infrastructure that enables rapid technology adoption.

North America’s market size reflects strong purchasing power and stringent regulatory enforcement, with OSHA Standard 1910.178 driving mandatory operator training, inspections, and integrated safety systems.

Regional facilities exhibit the world’s highest penetration of safety technology: proximity sensors exceed 85% adoption, collision avoidance systems reach 70%, and telematics platforms support fleet optimization in roughly 65% of major logistics operations. This advanced adoption reflects mature industrial infrastructure and continuous safety.

The Canadian market contributes incremental growth, maintaining technology adoption rates comparable to the United States.

Regional competitive dynamics center on North American leaders, including Toyota Material Handling, Crown Equipment Corporation, and emerging safety-focused providers. Investment activity remains strong, with venture capital and private equity directing significant funding toward innovations in collision avoidance and telematics.

Annual technology development investment is estimated at around US$150-200 million across North American safety solution providers, reinforcing sustained market advancement.

Europe Forklift Truck Safety Solutions Market Analysis

Europe represents a considerable market force, with a 24% global market share and a 13.2% CAGR, indicating a mature market with sustained expansion. European regulatory harmonization through CE marking requirements (Machinery Directive 2006/42/EC) and functional safety standards (ISO 13849-1) creates a unified compliance framework facilitating pan-European technology deployment.

Germany, the United Kingdom, France, and Spain account for approximately 75% of European market revenue, with Germany dominating through a strong manufacturing sector and a stringent occupational safety culture prioritizing workplace accident prevention. Germany's dependence on manufacturing exports drives comprehensive facility modernization cycles that incorporate advanced safety technologies.

The European market exhibits a strong worker-protection orientation, driven by stringent regulatory frameworks and a preference for proven, compliance-certified technologies. The region’s logistics hubs, especially in the United Kingdom and Benelux, demonstrate advanced adoption of telematics aligned with data-driven fleet optimization.

The competitive landscape includes major manufacturers such as Jungheinrich and KION Group, as well as specialized safety providers. Strategic moves, including Jungheinrich’s acquisition of ELOKON and Trio Mobil’s cloud-based platform launch, reflect consolidation toward integrated safety analytics ecosystems.

Asia Pacific Forklift Truck Safety Solutions Market Analysis

Asia Pacific dominates with a 39% market share and represents the strongest growth with a 15.6% CAGR in the forecast period. China commands approximately 45% of the Asia Pacific autonomous forklift market revenue, driven by the country's advanced manufacturing capabilities, massive e-commerce infrastructure, and government initiatives promoting logistics automation and smart manufacturing.

China's rapid deployment of warehouse automation, in response to accelerated e-commerce growth and labor cost pressures, creates substantial opportunities for forklift safety solution adoption.

Japan demonstrates the Asia-Pacific region's highest projected growth rate, reflecting labor shortages and a cultural emphasis on precision automation and robotics technology adoption. Japanese manufacturers (Toyota Industries, Mitsubishi Heavy Industries, Isuzu) maintain a strong regional presence, with Toyota particularly dominant through its comprehensive integration of safety solutions in modern forklift platforms.

Indian manufacturing expansion, driven by "Make in India" initiatives and efforts to attract foreign direct investment, creates greenfield opportunities for the deployment of safety technology in newly constructed facilities. ASEAN nations (Vietnam, Thailand, Indonesia) are experiencing accelerating manufacturing sector growth, with an estimated 25-30% expansion in warehouse capacity through 2033.

Regional dynamics show a strong preference for cost-effective solutions among smaller operations, while multinational logistics operators implement comprehensive telematics and collision avoidance architectures. Technology transfer from developed markets to the Asia Pacific accelerates the adoption of proven safety methodologies, though regional requirements often necessitate modifications.

Competitive Landscape

The global forklift truck safety solutions market shows moderate consolidation, with the leading key players holding around 35-40% share, while the remaining 60-65% is distributed among 200+ regional and specialized providers.

Competition reflects dual dynamics: major forklift manufacturers integrating embedded safety systems and specialized firms delivering retrofit and analytics-driven solutions. Consolidation is accelerating through acquisitions and strategic partnerships, while innovation-focused entrants intensify competition through advanced detection accuracy and software-driven differentiation.

Strategic Developments

- In May 2025, Mitsubishi Heavy Industries launched an automated safety lighting and AI driver-assist suite, targeting fast-growing Asia Pacific warehousing operations and aiming to expand its APAC safety technology market share by 8% by the end of 2027.

- In August 2024, Toyota Industries Corporation expanded its strategic alliance with Microsoft to deliver a cloud-based global telematics and fleet safety reporting platform, aiming for a 20% reduction in client incident rates within 12 months of implementation.

- In September 2022, Mitsubishi Logisnext Asia Pacific (MLAP) formed a strategic partnership with xSQUARE to jointly develop an AGV fleet based on Logisnext forklifts and roll out xSQUARE’s intelligent warehousing solutions via MLAP’s Asia-Oceania and South African distribution network.

Business Strategies

Market leaders advance their competitive position through three converging strategic pathways.

Major global forklift manufacturers strengthen control across the full equipment lifecycle by integrating safety technologies into unified product ecosystems, reinforcing customer dependence and enhancing platform value. Innovative safety-focused providers elevate differentiation by developing proprietary sensing capabilities, AI-driven analytics, and sector-specific safety architectures tailored to industries such as automotive, pharmaceuticals, and food processing.

Regional and mid-tier players accelerate growth by targeting underserved geographies with cost-optimized, locally adaptable safety solutions supported through strategic partnerships with domestic forklift distributors.

Companies Covered in Forklift Truck Safety Solutions Market

- Toyota Material Handling

- Kion Group AG

- Jungheinrich AG

- Hyster-Yale Materials Handling, Inc.

- Mitsubishi Heavy Industries

- Crown Equipment Corporation

- Anhui Heli Co., Ltd.

- Elokon

- Linde Material Handling

- Komatsu Ltd.

- AME- Advance microwave Engineering Srl

- Ubiquicom

- Seen Safety ltd.

- Siera AI

- Rombit

Frequently Asked Questions

The global forklift truck safety solutions market is likely to be valued US$9.7 billion in 2026, with projections to expand to US$24.6 billion by 2033.

The Forklift Truck Safety Solutions Market is driven by stringent global regulatory compliance requirements, surging e-commerce-led logistics activity, and the convergence of advanced technologies including AI-based predictive analytics, IoT-enabled telematics platforms, and next-generation sensor networks enabling real-time hazard detection and fleet optimization.

The forklift truck safety solutions market is projected to grow at 14.21% CAGR from 2026 to 2033.

Key market opportunities in the Forklift Truck Safety Solutions Market include accelerating infrastructure development across emerging economies, integration of autonomous navigation technologies within material-handling ecosystems, and growing alignment of safety solutions with global fleet electrification trends driven by rising electric forklift adoption.

Key players in the Global Forklift Truck Safety Solutions Market include major multinational equipment manufacturers such as Toyota Material Handling Industries, KION Group, Jungheinrich AG, Crown Equipment Corporation, and Mitsubishi Heavy Industries, alongside specialized collision-avoidance providers like TORSA, Safe Drive Systems, and Claitec, as well as emerging AI-driven analytics companies including Litum Technologies and CombiQ.