- Biotechnology

- Biologics Safety Testing Market

Biologics Safety Testing Market Size, Share, and Growth Forecast 2026 - 2033

Biologics Safety Testing Market by Product (Kits & Reagents, Instruments, Services), by Test Type (Endotoxin, Sterility, Cell Line Authentication and Characterization, Adventitious Agent Detection, Bioburden, Other), by Application, by Regional Analysis, 2026-2033

Biologics Safety Testing Market Size and Trend Analysis

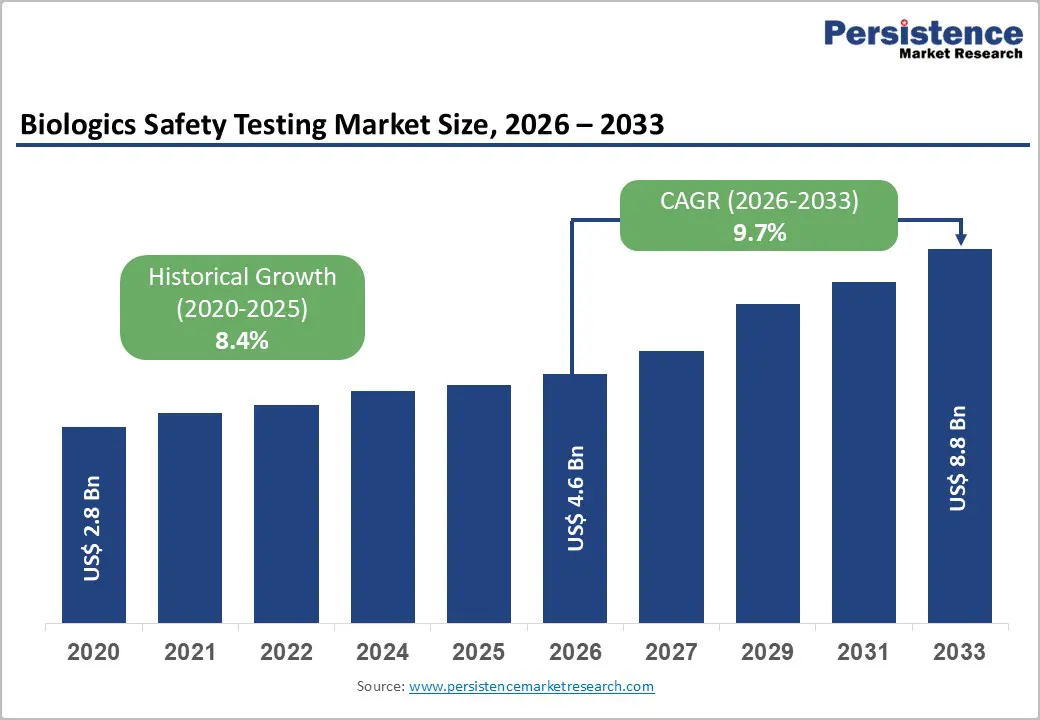

The global biologics safety testing market size is expected to be valued at US$ 4.6 billion in 2026 and projected to reach US$ 8.8 billion by 2033, growing at a CAGR of 9.7% between 2026 and 2033.

The biologics safety testing market plays a critical role in ensuring the quality, purity, and efficacy of complex therapeutics produced using recombinant DNA and other advanced biotechnologies. As biologics are increasingly used for treating cancer, autoimmune disorders, and rare diseases, rigorous safety evaluation has become essential to detect contaminants such as viruses, mycoplasma, endotoxins, and residual DNA. Regulatory agencies worldwide enforce strict guidelines across development, manufacturing, and commercialization stages, driving continuous demand for standardized and high-throughput testing solutions. Market trends indicate growing adoption of rapid molecular methods, automation, and outsourced testing services to improve efficiency and regulatory compliance. Expansion of biosimilar pipelines, rising vaccine production, and increased cell and gene therapy research further support market growth. Together, these factors position biologics safety testing as a foundational component of modern biopharmaceutical manufacturing.

Key Market Highlights

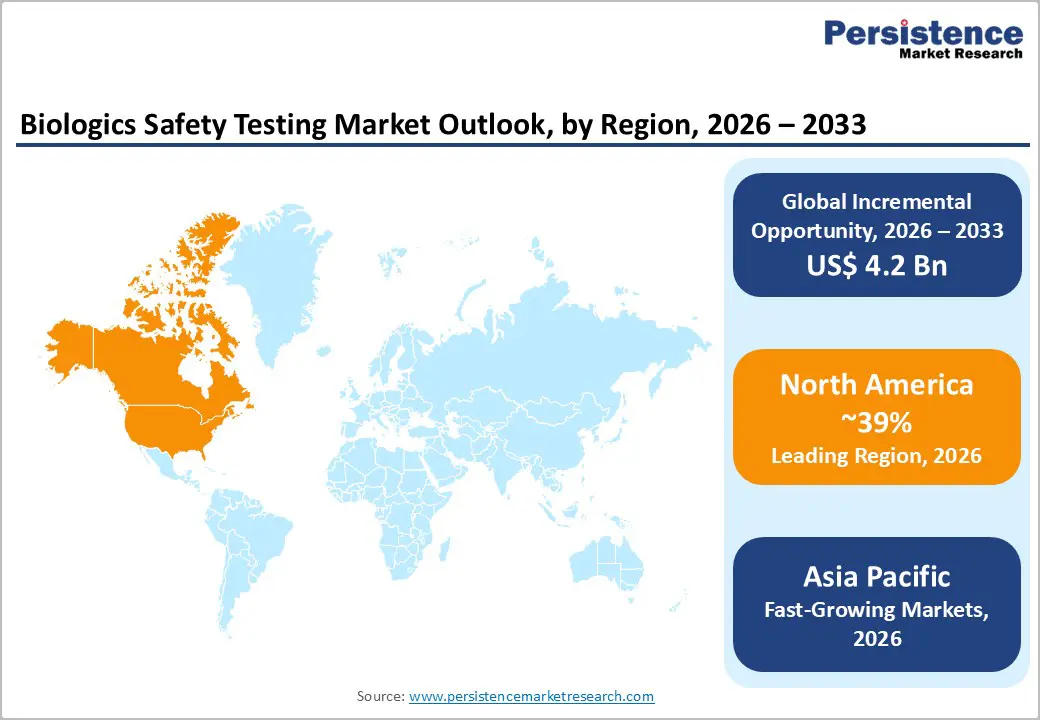

- North America dominates the biologics safety testing market, driven by strong regulatory frameworks, advanced pharmaceutical manufacturing infrastructure, high biologics R&D investments, and early adoption of cutting-edge testing technologies.

- Asia Pacific is the fastest-growing region, fuelled by increasing biologics manufacturing, supportive government initiatives, rising prevalence of chronic diseases, and expanding contract research organizations (CROs).

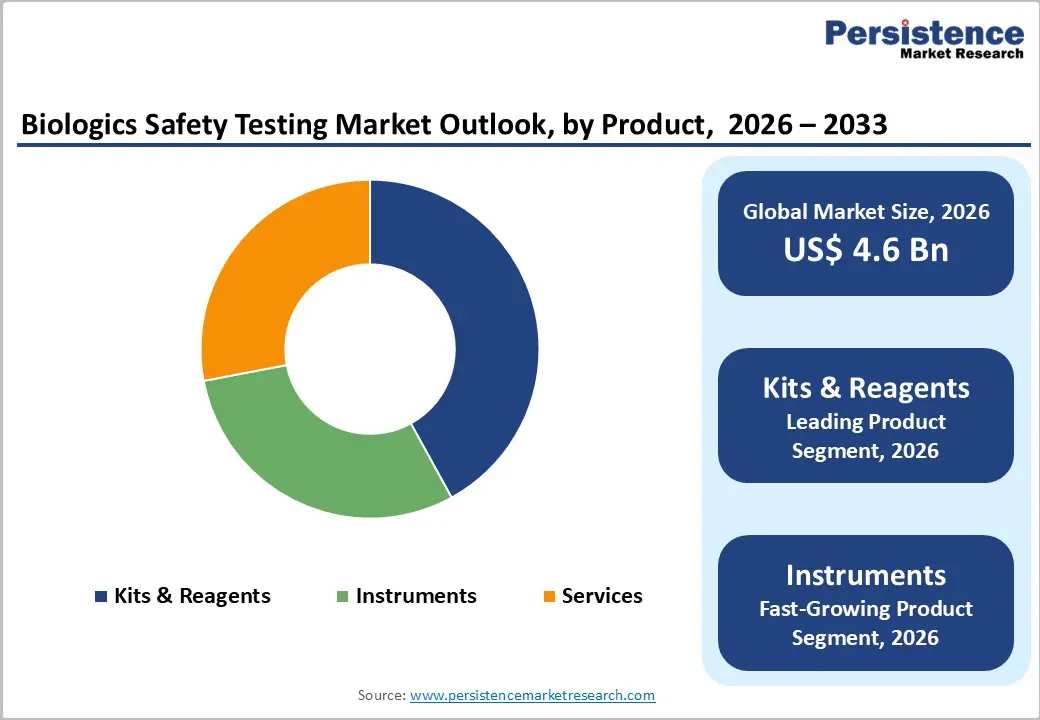

- In vitro testing kits hold the largest product share, owing to their cost-effectiveness, reproducibility, and growing preference over animal-based testing for safety and compliance.

- Contract research organizations (CROs) and biopharmaceutical companies are the fastest-growing end users, supported by outsourcing trends, increasing biologics pipeline, and demand for specialized safety testing services.

| Global Market Attributes | Key Insights |

|---|---|

| Biologics Safety Testing Market Size (2026E) | US$ 4.6 billion |

| Market Value Forecast (2033F) | US$ 8.8 billion |

| Projected Growth CAGR (2026-2033) | 9.7% |

| Historical Market Growth (2020-2025) | 8.4% |

Market Dynamics

Driver: Surge in Biologics Approvals

Rapid growth in biologics pipelines particularly vaccines, monoclonal antibodies, and cell and gene therapies has intensified the need for comprehensive safety testing across development and manufacturing stages. Regulatory agencies require extensive viral clearance, endotoxin, and sterility assessments before clinical use or commercial release, significantly expanding laboratory workloads. Each production batch must comply with strict pharmacopeial standards, increasing routine consumption of reagents and validated assays. A substantial share of overall testing activity now focuses on sterility and pyrogen detection to prevent contamination and protect patient safety. As accelerated approval pathways bring more advanced therapies to market, manufacturers face pressure to shorten development timelines without compromising quality. This has elevated demand for sensitive, reproducible testing platforms capable of supporting high-throughput screening while meeting regulatory expectations. Together, expanding biologics approvals and regulatory scrutiny continue to anchor long-term growth in the biologics safety testing sector.

Stringent Regulatory Mandates

Global regulatory frameworks remain one of the strongest forces shaping the biologics safety testing market. Authorities such as the FDA and EMA enforce detailed requirements for identity, potency, purity, and contamination control before granting lot release or marketing authorization. Compliance with international standards, including ICH guidelines and pharmacopeial monographs, is mandatory throughout clinical development and commercialization. Sterility testing is essential for injectable biologics, while viral safety and residual DNA analyses are critical for recombinant and cell-based products. Newer analytical approaches, such as recombinant Factor C assays for endotoxin detection, are gaining traction because they improve sensitivity and reduce dependence on animal-derived reagents. Ethical considerations and sustainability objectives further encourage adoption of alternative testing methods. These evolving regulatory expectations reinforce continuous investment in advanced assays, validation services, and documentation systems, sustaining steady demand across monoclonal antibodies, vaccines, and emerging advanced therapies.

Restraint: High Capital and Operational Costs

Significant capital requirements present a major barrier for smaller biopharmaceutical manufacturers and independent testing laboratories. Establishing compliant biosafety facilities, including BSL-2 or BSL-3 laboratories, requires heavy investment in containment systems, air-handling infrastructure, and validated analytical equipment. Specialized instrumentation for molecular assays, viral detection, and sterility testing adds further financial burden, while recruiting and retaining skilled personnel increases operating expenses. These infrastructure demands can raise total testing costs substantially and extend setting up timelines for new facilities. In addition, compliance with evolving regulatory expectations requires continuous method validation, audits, and documentation upgrades. Ethical scrutiny around animal-based assays also adds complexity and cost through additional oversight and alternative-method development. For organizations operating in cost-sensitive or resource-limited markets, these financial pressures can slow adoption of advanced testing platforms and restrict in-house capability expansion.

Opportunity: Growth in Cell and Gene Therapies

The rapid expansion of cell and gene therapy pipelines presents a major growth opportunity for biologics safety testing providers. Increasing regulatory approvals for these advanced modalities are driving demand for specialized assays targeting replication-competent viruses, vector copy number, residual host DNA, and adventitious agents. Because many cellular therapies have short shelf lives, manufacturers require fast, reliable testing solutions that support rapid product release without compromising compliance. Platform-based methods that can be adapted across multiple products are gaining attention for their ability to streamline validation and reduce development timelines. Growing investment in automation and high-throughput systems further enhances laboratory efficiency, particularly as production volumes scale in Asia-Pacific manufacturing hubs. As governments promote domestic biomanufacturing and clinical research infrastructure, testing service providers and reagent suppliers are well positioned to benefit from expanding CGT pipelines and long-term industry investment.

Adoption of Rapid Microbiological Methods

Shifting from conventional culture-based techniques to rapid microbiological methods is creating fresh opportunities across the biologics safety testing landscape. Technologies such as PCR-based detection, automated imaging systems, and recombinant Factor C endotoxin assays significantly shorten testing cycles while maintaining regulatory compliance. These approaches can cut time-to-result by days compared with traditional sterility or LAL methods, enabling faster batch release and improved supply-chain responsiveness. Ethical initiatives aimed at reducing animal-derived reagents further support the transition toward alternative assays, particularly in European markets. High-throughput platforms and robotics are increasingly deployed in large testing laboratories to minimize human error and manage rising sample volumes from biologics and cell-therapy production lines. Adoption is accelerating in countries such as China and India as facilities modernize and scale operations. This movement toward rapid, automated testing is reshaping competitive dynamics and driving investment across the sector.

Category-wise Insights

Product Analysis

Kits and reagents are expected to dominate the biologics safety testing market in 2025, supported by their recurring use, scalability, and suitability for high-throughput laboratory environments. These consumables form the backbone of routine sterility, endotoxin, mycoplasma, and viral detection assays used across vaccine manufacturing, monoclonal antibody production, and recombinant therapeutics. Their compatibility with automated platforms and standardized workflows aligned with pharmacopeial requirements strengthens adoption in both in-house and outsourced testing facilities. Contract research and testing organizations rely heavily on validated reagent kits to maintain consistency across multiple client programs, reinforcing steady purchasing volumes. Growing cell and gene therapy pipelines further expand usage, as each batch requires repeated safety verification before release. Continuous product upgrades, including animal-free endotoxin assays and rapid molecular kits, enhance performance while meeting evolving regulatory and ethical expectations, allowing this category to retain the largest share.

Application Analysis

Vaccine and therapeutic development represent the largest application area for biologics safety testing, driven by stringent regulatory oversight throughout discovery, clinical trials, and commercial manufacturing. Monoclonal antibodies, recombinant proteins, and viral-vector-based products require extensive viral clearance studies, sterility validation, and residual impurity testing at multiple production stages. Global immunization programs and expansion of biosimilar pipelines have further elevated testing volumes, particularly for large-scale vaccine batches that demand rapid yet compliant release. Regulatory authorities mandate comprehensive safety datasets for lot approval, sustaining long-term demand for analytical services and consumables in this segment. Growth is also supported by increased investment in biologics manufacturing capacity across North America, Europe, and Asia-Pacific. As pharmaceutical companies accelerate development timelines while maintaining strict quality controls, vaccine and therapeutic programs continue to account for the highest proportion of biologics safety testing activity worldwide.

Regional Insights

North America Biologics Safety Testing Market Trends and Insights

North America holds the largest share of the biologics safety testing market, driven by a mature biopharmaceutical sector, high R&D investments, and stringent regulatory oversight from agencies such as the FDA. The region benefits from a well-established infrastructure for vaccine production, monoclonal antibodies, and cell and gene therapies, requiring extensive sterility, viral, and endotoxin testing at multiple production stages. Outsourced testing services are widely adopted due to the complexity and volume of biologics pipelines, further fueling market growth. Adoption of rapid microbiological methods, automation, and animal-free assays is increasing, improving throughput and regulatory compliance. The presence of key market players with advanced laboratories and platform technologies enables North America to maintain leadership in both innovation and testing capacity.

Additionally, government funding, expanding clinical trials, and robust intellectual property protections encourage development of next-generation biologics, sustaining strong demand for reliable safety testing across vaccines, therapeutics, and advanced therapies.

Asia Pacific Biologics Safety Testing Market Trends and Insights

The Asia Pacific biologics safety testing market is the fastest-growing region globally, propelled by expanding biopharmaceutical manufacturing, rising healthcare investments, and increasing adoption of advanced biologics such as monoclonal antibodies, vaccines, and cell and gene therapies. Countries like China, India, and Japan are leading growth, supported by government initiatives to improve local vaccine production and regulatory compliance. The region has witnessed rapid establishment of high-throughput laboratories equipped with automated and robotics-based testing platforms, enabling faster, accurate evaluation of sterility, endotoxin levels, and viral contaminants. Increasing outsourcing of biologics safety testing by global pharmaceutical companies to Asia-Pacific labs is also driving growth.

Furthermore, rising awareness of biosimilar development, clinical trial expansion, and infrastructure upgrades in emerging economies are supporting long-term adoption. Ethical initiatives encouraging animal-free assays, along with high demand for vaccines and advanced therapies, make the region a promising market for both consumables and testing services, with strong CAGR projected through 2032.

Competitive Landscape

Market Structure Analysis

Companies developing solutions on assessing the safety of biologics are anticipated to combine industry-leading expertise and operational excellence, which will ensure that critical drug development programs and manufacturing processes become successful. Companies such as Wuxi Apptec, Toxikon Corporation, Lonza Group Ltd., Pace Analytical Services Inc., BioMerieux SA, Genscript Biotech Corp., Thermo Fisher Scientific Inc., SGS S.A., Eurofins Scientific Se, Sigma-Aldrich Corporation (part of Merck KGaA), and Charles River Laboratories International, Inc.are observed to remain active in the global biologics safety testing market throughout the forecast period.

Key Market Developments

- In January 2024, Charles River Laboratories introduced the Endosafe Trillium rCR cartridge, an innovative animal-free solution designed for precise bacterial endotoxin testing.

- in November 2023, Merck KGaA established biosafety testing laboratories in Shanghai, China, providing clients with local access to comprehensive services for cell line characterization and lot release, supporting processes from pre-clinical development through to commercialization.

Companies Covered in Biologics Safety Testing Market

- Charles River Laboratories International, Inc.

- Eurofins Scientific Se

- SGS S.A.

- Thermo Fisher Scientific Inc.

- Genscript

- Biomérieux Sa

- Pace Analytical Services Inc.

- Lonza Group Ltd.

- Toxikon Corporation

- Wuxi Apptec

- Others

Frequently Asked Questions

The global biologics safety testing market is valued at US$ 4.6 billion in 2026.

Rising biologics approvals, increasing vaccines and monoclonal antibody production, regulatory mandates, and growth of cell and gene therapy pipelines.

North America leads with 39% share in 2025.

Expanding cell and gene therapy applications and rapid microbiological methods adoption offer growth potential in emerging markets and automated testing platforms.

Leaders include Charles River Laboratories International, Inc., Eurofins Scientific Se, SGS S.A., Thermo Fisher Scientific Inc., and Genscript.