- Biotechnology

- Molecular Diagnostics in Infectious Disease Testing Market

Molecular Diagnostics in Infectious Disease Testing Market Size, Share, Growth, and Regional Forecast, 2026 to 2033

Molecular Diagnostics in Infectious Disease Testing Market by Type of LNP (Instruments and Analyzers, Assays and Reagents, Services and Software), Therapeutic Area (Polymerase Chain Reaction (PCR), Isothermal Nucleic Acid Amplification Technology (INAAT), Microarrays, Next-Generation Sequencing (NGS), Hybridization, Others), Application (Hepatitis B, Hepatitis C, AIDS, Tuberculosis, Methicillin-Resistant Staphylococcus Aureus (MRSA), Hospital-Acquired Infections, Chlamydia Trachomatis and Neisseria Gonorrhoeae (CT/NG), Human Papillomavirus (HPV) Infection, Others), End User (Hospitals, Private Labs, Clinics, Academic Institutes, Laboratories, Others), and Regional Analysis from 2026 to 2033.

Molecular Diagnostics in Infectious Disease Testing Market Size and Trends

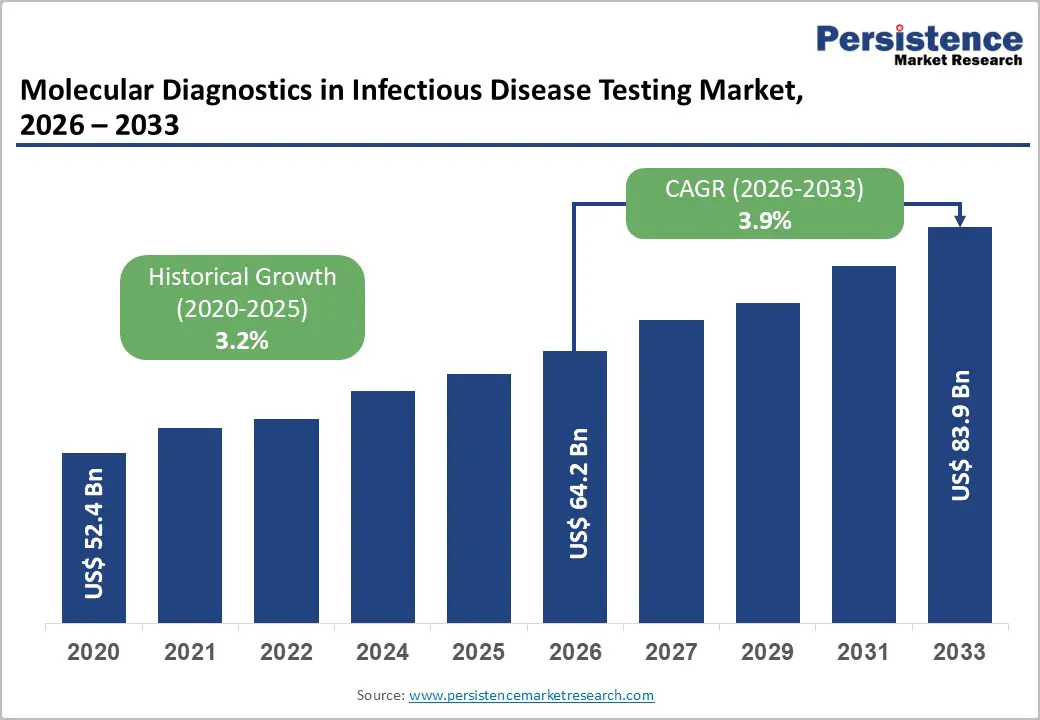

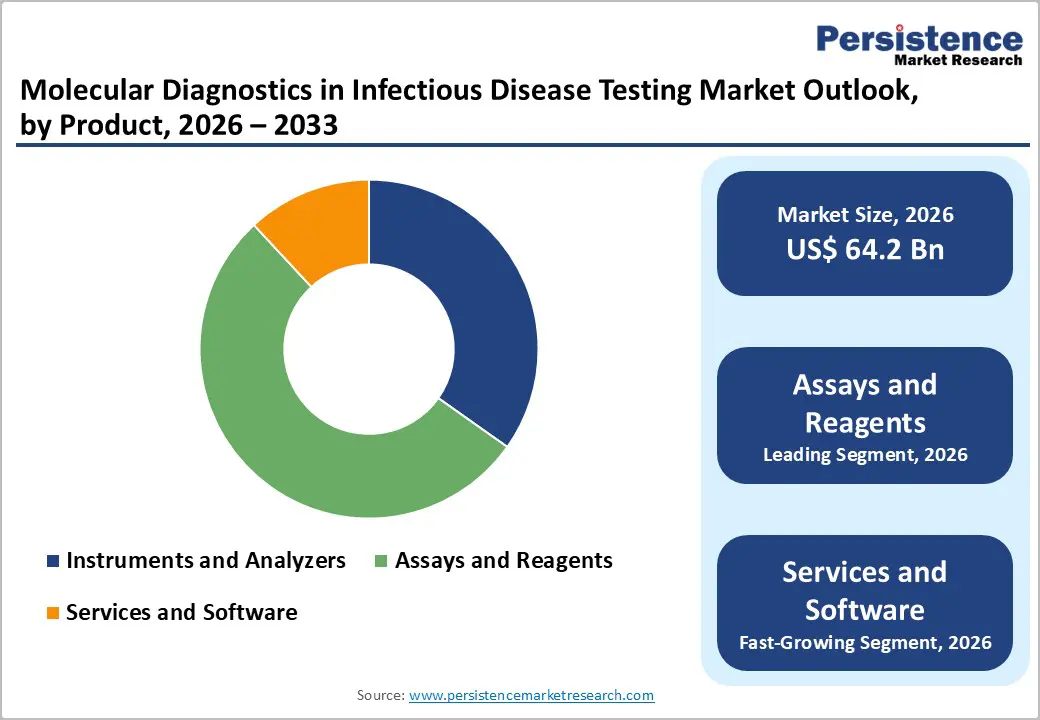

The global molecular diagnostics in infectious disease testing market is estimated to grow from US$ 64.2 Bn in 2026 to US$ 83.9 Bn by 2033. The market is projected to record a CAGR of 3.9% during the forecast period from 2026 to 2033.

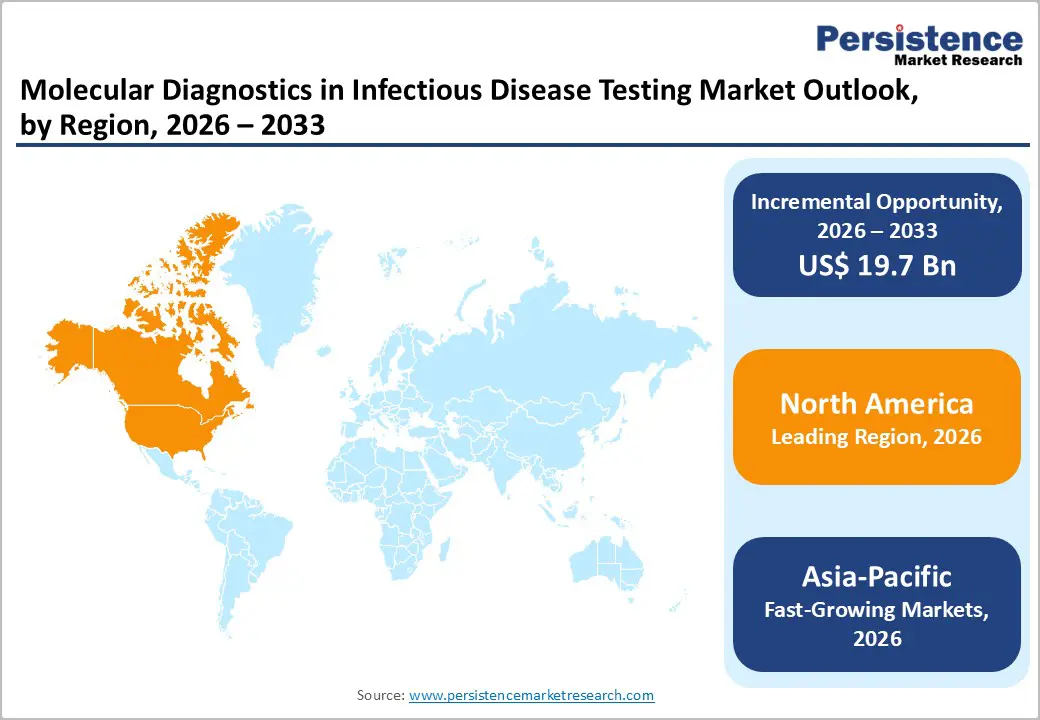

The global infectious disease in-vitro diagnostics market is growing steadily, driven by expanding diagnostic testing, health integration, telehealth adoption, and data analytics. North America leads due to advanced laboratory infrastructure and stringent regulatory standards. Asia-Pacific is the fastest-growing region, supported by healthcare expansion, government initiatives, rising disease awareness, and increased investments in platforms and services.

Key Industry Highlights

- Dominant Segment: Reagents and assay kits hold 53.3% share in 2025, driven by high testing volumes, recurring demand, and widespread use across molecular, immunoassay, and rapid diagnostic platforms. Their accuracy, scalability, and compatibility with automated analyzers support efficient workflows and consistent clinical decision-making.

- Dominant Region: North America leads the market in 2025 with 43.9% share, supported by advanced laboratory infrastructure, strong regulatory oversight, and high adoption of molecular and automated diagnostics. Asia-Pacific is the fastest-growing region, driven by expanding healthcare access, government-led screening programs, rising infectious disease burden, and increased investments in diagnostic laboratories and manufacturing.

- Market Drivers: Market growth is driven by the rising prevalence of infectious diseases, increased demand for early and accurate diagnosis, technological advances in molecular and rapid testing, expansion of centralized and decentralized laboratories, and growing integration of diagnostics with digital health systems.

- Market Opportunity: Key opportunities include multiplex and point-of-care testing, expansion of molecular diagnostics in emerging markets, integration of AI and data analytics in diagnostics, development of affordable rapid tests, and increasing adoption of automated and high-throughput platforms.

| Global Market Attributes | Key Insights |

|---|---|

| Global Molecular Diagnostics in Infectious Disease Testing Market Size (2026E) | US$ 64.2 Bn |

| Market Value Forecast (2033F) | US$ 83.9 Bn |

| Projected Growth (CAGR 2026 to 2033) | 3.9% |

| Historical Market Growth (CAGR 2020 to 2025) | 3.2% |

Market Dynamics

Driver: Growing demand for early, accurate, and rapid diagnosis to improve clinical outcomes

The growing demand for early, accurate, and rapid diagnosis is a key driver of the infectious disease in-vitro diagnostics market because timely pathogen identification directly influences clinical decisions and outcomes. According to the World Health Organization (WHO), diagnostic results inform approximately 70% of healthcare decisions, underscoring their central role in effective treatment and disease management. Early detection of infectious agents enables prompt treatment initiation, which can reduce complications, prevent disease progression, and decrease transmission. For example, rapid molecular tests such as the Xpert MTB/RIF assay can detect tuberculosis and drug resistance in under two hours versus several weeks with conventional culture methods, greatly accelerating clinical intervention. This need for faster, more reliable diagnostics has driven widespread adoption of in-vitro diagnostic tools in hospitals, reference laboratories, and point-of-care settings globally, expanding overall market demand.

Government and public health emphasis on rapid diagnostics further justifies this demand. WHO’s integrated diagnostics initiatives highlight that early detection and diagnosis are gateways to effective treatment and improved patient outcomes across HIV, tuberculosis, hepatitis, and other infectious diseases. The prevalence of major infectious diseases also reinforces the need for rapid, accurate tests; WHO estimates hundreds of millions of cases annually for malaria (300–500 million), sexually transmitted infections (~333 million), and HIV (~33 million), each requiring timely diagnosis to guide care and infection control. Additionally, expansions in laboratory infrastructure, such as the establishment of more than 100 Viral Research and Diagnostic Laboratories in India alone, reflect policy responses to the diagnostic demand for rapid identification of emerging and re-emerging pathogens. Together, these data illustrate that the imperative for early, precise detection significantly propels market growth.

Restraints: High cost of advanced molecular diagnostic instruments and reagents

The high cost of advanced molecular diagnostic instruments and reagents represents a significant restraint for the infectious disease in-vitro diagnostics market because it limits adoption by smaller healthcare facilities and low-resource settings. Advanced systems such as real-time PCR instruments typically range from USD 50,000 to USD 150,000, with additional expenses for specialized reagents and maintenance, which together inflate the total cost of ownership for laboratories. Government and laboratory reports show that even concessional pricing for instruments like the GeneXpert system can remain around USD 32,000 for a four-module unit, making initial capital outlay substantial. These high upfront and ongoing costs constrain the capacity of regional and rural healthcare centers to implement cutting-edge molecular diagnostics, which reduces overall market penetration and reinforces disparities in healthcare access.

Moreover, the cost per test using molecular diagnostics remains markedly higher than many conventional methods, further discouraging widespread use. Data from WHO’s ACT-Accelerator initiative indicates that at the start of the COVID-19 pandemic, molecular tests were priced between USD 20–30 in low- and middle-income countries, compared with much lower costs for rapid antigen tests, highlighting persistent affordability challenges despite negotiated price reductions. These higher consumable costs, combined with expenditures for skilled personnel and laboratory infrastructure, make molecular in-vitro diagnostics less feasible for routine infectious disease screening in budget-constrained health systems. Consequently, many facilities defer investment in advanced diagnostics or rely on external reference laboratories, which can delay diagnosis and reduce the frequency of testing, impeding broader market expansion.

Opportunity: Expansion of multiplex assays enabling simultaneous detection of multiple pathogen

The expansion of multiplex assays enabling simultaneous detection of multiple pathogens presents a significant opportunity for the infectious disease in-vitro diagnostics market by improving diagnostic efficiency, throughput, and clinical decision support. Multiplex molecular panels such as those authorized by the U.S. Centers for Disease Control and Prevention (CDC) can detect influenza A/B and SARS-CoV-2 simultaneously within a single reaction, increasing testing throughput three-fold compared with separate assays. This approach reduces reagent use, labor, and time to result while maintaining high specificity and sensitivity, broadening testing capacity during peak respiratory seasons when co-circulation of pathogens is common. Multiplex platforms have also been shown to identify multiple enteric pathogens in stool samples with positivity rates of nearly 40% versus approximately 15% with conventional methods, demonstrating enhanced detection performance and diagnostic yield.

Multiplex assays further enable high-throughput surveillance and epidemiological insights by detecting co-infections and simultaneously screening for a broad array of infectious agents, important for public health monitoring and response. For example, advanced 10-plex immunoassays demonstrated overall agreement rates exceeding 96% with reference tests for pathogens including HIV, hepatitis B and C, syphilis, and herpes, validating their utility across multiple diseases in a single run. In respiratory diagnostics, multiplex PCR panels detect a wide spectrum of bacterial and viral agents in under two hours and have increased pathogen yield substantially compared with traditional methods, improving time-to-diagnosis and enabling targeted antimicrobial therapy decisions. These capabilities not only streamline laboratory workflows but also help laboratories and health systems respond more effectively to complex infectious disease burdens.

Category-wise Analysis

By Product, Assays and Reagents Dominates the Molecular Diagnostics in Infectious Disease Testing Market

Assays and Reagents occupies 53.3% share of the global market in 2025, because they are indispensable consumables required for every test, unlike instruments which are one-time investments. Reagents and kits, including primers, probes, enzymes, and buffers, accounted for the largest share of testing products, around 42–47 % of the infectious disease diagnostics market reflecting their essential role in enabling PCR, immunoassay, and nucleic acid amplification workflows. Governments and laboratories increasingly rely on standardized reagents to ensure test accuracy and reproducibility across high volumes of screening and outbreak response. The recurring nature of reagent purchases, tied directly to testing frequency and expanding disease surveillance programs, ensures a sustained revenue stream and reinforces their market dominance versus instruments and software.

By Technique, PCR dominates due to unmatched sensitivity, rapid turnaround, broad pathogen detection, and widespread government adoption for infectious disease testing.

PCR (polymerase chain reaction) dominates the Molecular Diagnostics in Infectious Disease Testing Market because it delivers rapid, highly sensitive, and specific detection of pathogen genetic material, making it indispensable for clinical and public health diagnostics. PCR’s ability to amplify even tiny amounts of DNA or RNA enables identification of viruses, bacteria, fungi, and parasites directly from clinical samples, often within hours rather than days required for culture-based methods. During the COVID-19 pandemic, real-time reverse transcription PCR (RT-PCR) became the global standard for SARS-CoV-2 detection due to its reliability and speed, illustrating its central role in outbreak response. This broad applicability across diverse pathogens and clinical contexts underpins PCR’s market dominance in molecular infectious disease testing.

Regional Insights

North America Molecular Diagnostics in Infectious Disease Testing Market Trends

North America dominates the molecular diagnostics in infectious disease testing market with 45.1% share in 2025, because of its highly developed healthcare infrastructure, extensive laboratory networks, and strong public health systems that facilitate widespread adoption of advanced diagnostic technologies. In 2024, North America accounted for roughly 38–40 % of the global infectious disease molecular diagnostics market, reflecting its capacity for large-scale testing and technology deployment. The United States, in particular, has supported robust molecular testing capacity in response to disease surveillance needs, with millions of PCR tests conducted nationwide during major outbreaks such as COVID-19, underscoring its expansive diagnostic ecosystem. Furthermore, substantial government funding for laboratory modernization, strong regulatory frameworks, and high healthcare expenditure levels ensure rapid integration of innovative diagnostic solutions across clinical and point-of-care settings.

Europe Molecular Diagnostics in Infectious Disease Testing Market Trends

Europe is an important region in the molecular diagnostics in infectious disease testing Market due to its robust public health infrastructure, coordinated laboratory networks, and proactive disease surveillance systems. The European Centre for Disease Prevention and Control (ECDC) supports integrated microbiology laboratory networks across EU member states, enhancing capacity for epidemiological surveillance, outbreak response, and cross?border infectious disease control. These networks provide standardized testing and quality assurance, reinforcing rapid detection and reporting of communicable diseases. Additionally, Europe maintains high testing volumes for major pathogens, with over 120?million HIV tests annually and millions of tuberculosis tests conducted across EU/EEA countries, illustrating persistent demand for accurate diagnostics. Strong government investment, universal healthcare systems, and regulatory frameworks further drive adoption of advanced molecular techniques for infectious disease management and public health readiness.

Asia-Pacific Molecular Diagnostics in Infectious Disease Testing Market Trends

Asia Pacific is the fastest?growing region in the molecular diagnostics in infectious disease testing market due to its large population, expanding healthcare infrastructure, and increasing focus on diagnostic capacity building. The region’s infectious disease molecular diagnostics segment is growing rapidly, supported by rising laboratory investments and broader access to PCR and related technologies. China, India, and other countries are significantly scaling up testing capabilities to meet public health needs, with widespread PCR use for multiple pathogens driving higher diagnostic volumes. Governments are also prioritizing infectious disease surveillance and screening programs, reflecting rising disease burdens and the need for accurate, early detection. These trends collectively underpin strong regional growth momentum in molecular infectious disease diagnostics relative to other markets.

Market Competitive Landscape

Leading companies in the molecular diagnostics in infectious disease testing market focus on advanced assay development, automation, and regulatory compliance. Investments in high-throughput platforms, AI-assisted interpretation, and process standardization enhance accuracy and reproducibility. Collaborations with hospitals, public health agencies, and academia accelerate molecular, multiplex, and point-of-care diagnostics, supporting early detection, outbreak response, and precision public health worldwide.

Key Industry Developments:

- In December 2025, BD expanded its BD MAX™ System menu by introducing new IVDR?certified VIASURE assays in partnership with Certest Biotec. The launch enhanced the system’s molecular diagnostic capabilities, enabling more comprehensive detection of infectious diseases. The collaboration aimed to provide laboratories with reliable, regulatory-compliant assays, improving workflow efficiency and diagnostic accuracy across clinical settings.

- In June 2025, bioMérieux strengthened its next-generation sequencing (NGS) capabilities by acquiring Day Zero Diagnostics’ solutions and technologies. The acquisition expanded bioMérieux’s molecular diagnostics portfolio, enhancing its ability to deliver advanced genomic testing and pathogen detection.

Companies Covered in Molecular Diagnostics in Infectious Disease Testing Market

- Abbott Laboratories

- Becton Dickinson and Company

- bioMérieux

- Thermo Fisher Scientific Inc.

- F. Hoffmann-La Roche Ltd

- Siemens AG

- Veridex, LLC

- Luminex Corp.

- GenMark Diagnostics, Inc.

- Qiagen N.V.

- Genomix Biotech

- bioTheranostics

Frequently Asked Questions

The global molecular diagnostics in infectious disease testing market is projected to be valued at US$ 64.2 Bn in 2026.

Rising infectious diseases, demand for rapid, accurate testing, technological advances, and expanded laboratory infrastructure drive growth.

The global molecular diagnostics in infectious disease testing market is poised to witness a CAGR of 3.9% between 2026 and 2033.

Opportunities include multiplex testing, point-of-care diagnostics, AI integration, emerging markets expansion, and high-throughput molecular platforms.

Abbott Laboratories, Becton, Dickinson and Company, bioMérieux, Thermo Fisher Scientific Inc., F. Hoffmann-La Roche Ltd.