- Food Ingredients & Additives

- Milk Protein Concentrate Market

Milk Protein Concentrate Market Size, Share, and Growth Forecast 2026 - 2033

Milk Protein Concentrate Market by Product Type (MPC 40, MPC 70, MPC 80, MPC 85, Others), by Nature (Organic, Conventional), by End Use (Infant Formula and Baby Foods, Dietary Supplements, Dairy Products, Sports Nutrition, Bakery & Confectionery, Others), and by Regional Analysis, 2026-2033

Milk Protein Concentrate Market Size and Trends Analysis

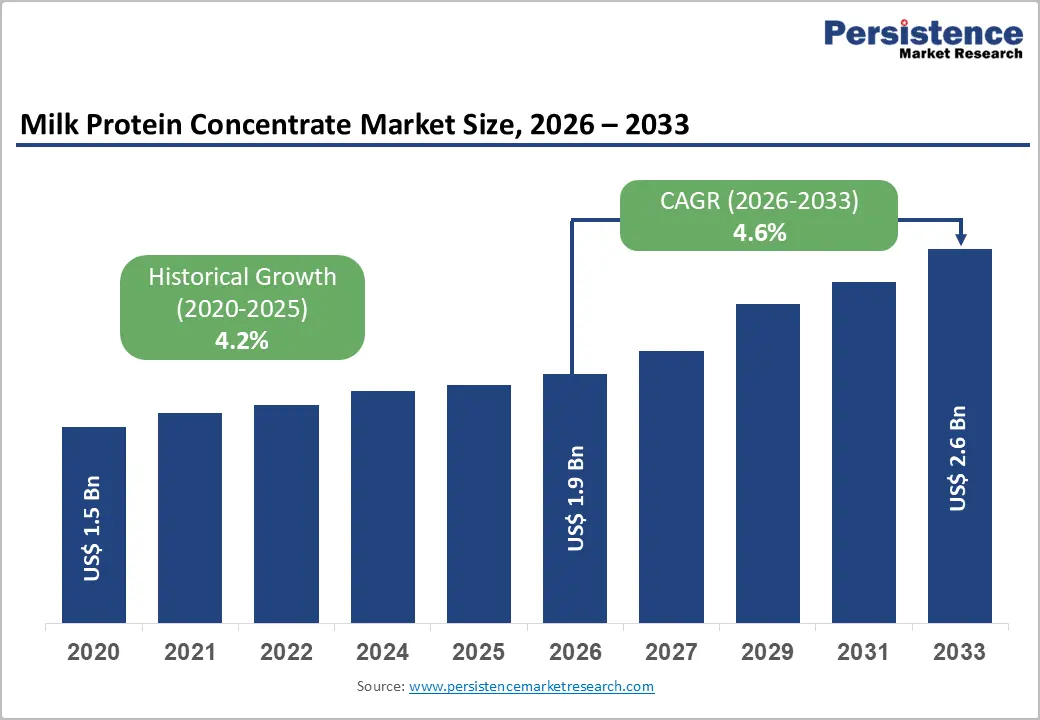

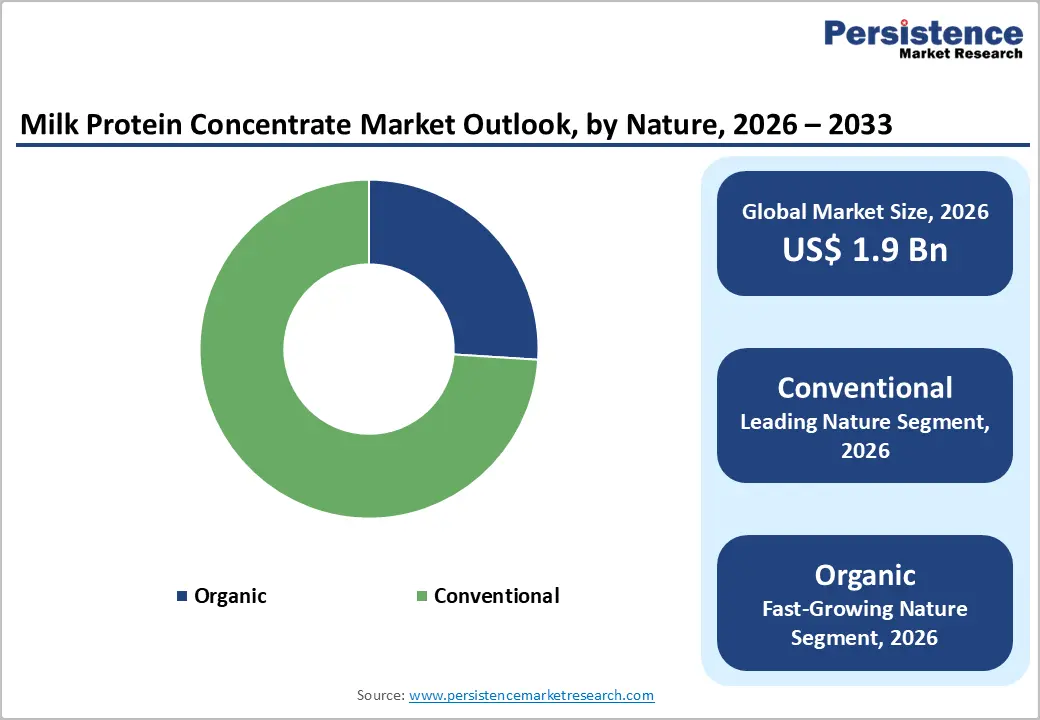

The global Milk Protein Concentrate Market size is expected to be valued at US$ 1.9 billion in 2026 and projected to reach US$ 2.6 billion by 2033, growing at a CAGR of 4.6% between 2026 and 2033

Key Industry Highlights

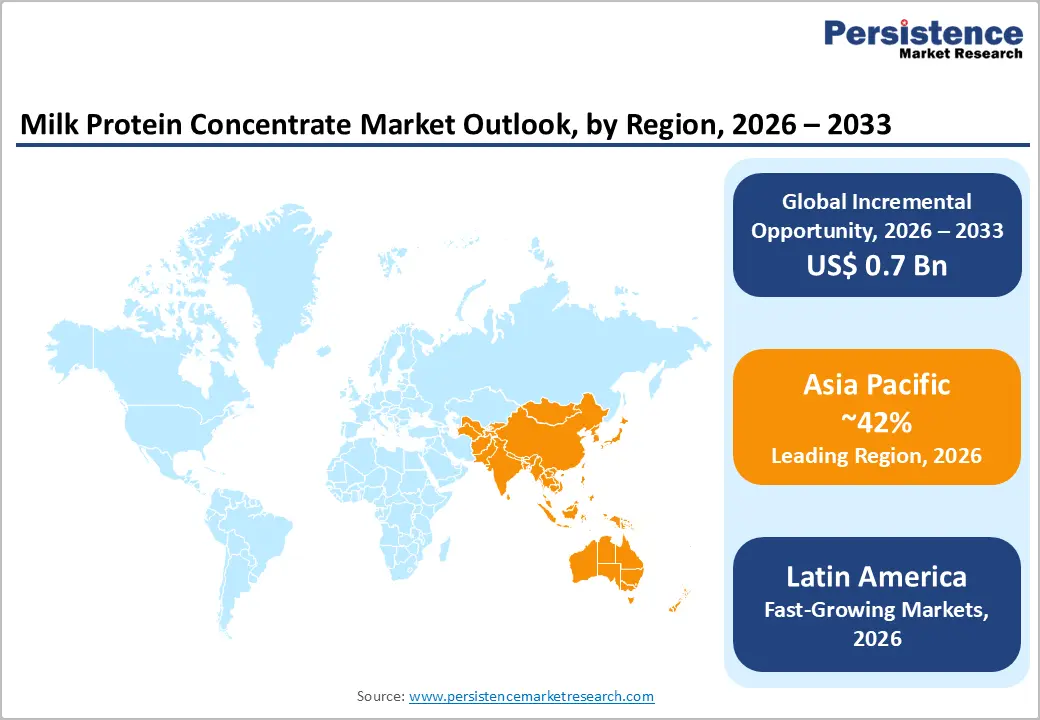

- Leading Region: Asia Pacific dominated the global market in 2025 with a 42% share, driven by rapid urbanization and the massive demand for infant formula in China and India.

- Dominant Segment: Conventional MPC remains the dominant nature segment with a 74% share, supported by large-scale production efficiencies and global industrial demand.

- Fastest Growing Segment: Organic MPC is the quickest-expanding category, fueled by the global "Clean-Label" movement and consumer preference for natural, hormone-free ingredients.

- Key Market Opportunity: Technological Innovation in precision fermentation and membrane filtration offers a path to higher yields and sustainable, animal-free protein alternatives.

- Key Developments: In February 2025,Agropur announced the Grand Champions of its Club of Excellence competition, awarding Ferme Gagnonval (Sainte-Hénédine) for outstanding milk quality and Ferme Roland Caron (Laurierville) for excellence in animal welfare.

| Key Insights | Details |

|---|---|

| Global Milk Protein Concentrate Market Size (2026E) | US$ 1.9 Bn |

| Market Value Forecast (2033F) | US$ 2.6 Bn |

| Projected Growth (CAGR 2026 to 2033) | 4.6% |

| Historical Market Growth (CAGR 2020 to 2025) | 4.2% |

Market Dynamics

Driver – Growing Global Emphasis on High-Protein Diets and Sports Nutrition

The primary driver for the Milk Protein Concentrate Market is the accelerating shift toward protein-dense diets among health-conscious consumers and fitness enthusiasts. MPCs, particularly high-concentration variants like MPC 80 and MPC 85, offer a complete protein source containing both Casein and Whey in their native state. According to the World Health Organization (WHO), the global geriatric population is projected to reach 2 billion by 2050, creating a massive demand for protein-enriched products to combat age-related muscle loss. In the sports sector, the trend has moved beyond professional athletes to "lifestyle" users who consume Ready-to-Drink (RTD) protein shakes and nutritional bars. Organizations like the International Society of Sports Nutrition (ISSN) have highlighted the efficacy of milk-derived proteins in muscle protein synthesis, leading manufacturers to favor MPC for its excellent heat stability and neutral flavor profile in diverse formulations.

Restraints – Volatility in Raw Milk Prices and Supply Chain Fluctuations

A significant barrier to the steady growth of the Milk Protein Concentrate Market is the inherent instability of raw milk costs, which are influenced by climatic conditions, geopolitical trade tensions, and fluctuating feed prices. For instance, the implementation of U.S. Tariffs in early 2025 has impacted the pricing of imported dairy ingredients from Europe, creating cost pressures for North American manufacturers. Droughts in major dairy-producing regions like Oceania can lead to sudden supply shortages, forcing processors to navigate a volatile cost environment. Because MPC production is a capital-intensive process involving advanced membrane filtration, any increase in raw material or energy costs can significantly compress profit margins. This volatility often leads to price hikes for end-products, potentially deterring price-sensitive consumers in developing economies from adopting premium protein-enriched foods.

Opportunity – Integration into Personalized Nutrition and Clinical Medical Foods

The burgeoning field of Personalized Nutrition offers a massive untapped growth pocket for the Milk Protein Concentrate Market. Consumers are increasingly seeking tailored nutritional solutions based on their DNA, lifestyle, and specific health goals. MPCs are ideal for clinical nutrition applications, such as enteral feeding formulas for hospital patients and specialized shakes for diabetics. The high calcium and bioactive peptide content in concentrates like MPC 85 supports bone health and blood pressure regulation. As digital health platforms become more prevalent, the demand for customized protein blends that address specific deficiencies is expected to rise. Manufacturers that can provide traceable, high-quality proteins for these niche medical segments will be able to command premium pricing. Furthermore, the development of "Clean-Label" and minimally processed MPCs aligns with the growing consumer preference for transparency and naturality in their health supplements.

Category-wise Analysis

Nature Analysis

The Conventional segment held the leading position in the Milk Protein Concentrate Market in 2025, accounting for a dominant 74% market share. This leadership is attributed to the well-established global dairy supply chain and the lower cost of conventional farming compared to organic practices. Conventional MPC is the standard choice for large-scale industrial food processing, where consistency and volume are paramount. However, the Organic segment is recognized as the fastest-growing category, projected to witness a robust CAGR through 2032. This growth is fueled by an escalating consumer preference for "Clean-Label" products that are free from synthetic hormones, pesticides, and antibiotics. In regions like Europe and North America, health-conscious parents are increasingly willing to pay a premium for organic infant formula, encouraging major players like Arla Foods and Danone to expand their organic ingredient portfolios.

End Use Analysis

The Dairy Products and Sports Nutrition segments represent the largest revenue streams for Milk Protein Concentrates. In the dairy sector, MPCs are indispensable for standardized cheese production and enhancing the protein content of yogurts and puddings. In March 2025, Mother Dairy launched its "Pro" range in India, featuring milk with 30% more protein, illustrating the trend of protein fortification in everyday dairy staples. Conversely, the Dietary Supplements and Infant Formula segments are the fastest-growing application areas. The increasing global focus on "Healthy Aging" has led to a surge in protein powders and meal replacements for the elderly. Similarly, the pediatric nutrition market continues to expand in developing nations, where MPC is valued for its ability to deliver essential minerals and proteins in a form that is easy for infants to digest, driving significant volume growth in these high-value categories.

Region-wise Insights

Asia Pacific Milk Protein Concentrate Market Trends and Insights

The Asia Pacific region is the leading regional segment, holding a 42% market share in 2025, and is also the fastest-growing market globally. This dominance is propelled by rapid urbanization, increasing disposable incomes, and changing dietary patterns in emerging economies like China and India. In China, the government’s focus on domestic infant formula self-sufficiency has significantly increased the demand for high-grade MPC from local producers.

India is emerging as a massive market due to its vast vegetarian population, which relies heavily on dairy as a primary protein source. According to the USDA Foreign Agricultural Service, India's fluid milk production is projected to reach over 212 million metric tons by the end of 2024, providing a robust foundation for the domestic MPC industry. The region also benefits from a growing number of working women, which has spurred the consumption of baby feeding products and convenient RTD protein beverages. Major international players are forming joint ventures with local dairy giants to tap into this high-growth potential, focusing on affordable yet nutritious protein solutions for the mass market.

North America Milk Protein Concentrate Market Trends and Insights

North America remains a global leader in scale and product innovation within the Milk Protein Concentrate Market. The United States serves as the regional engine, driven by a mature fitness culture and a highly sophisticated food processing industry. According to the U.S. Dairy Export Council (USDEC), the region has been at the forefront of establishing GRAS (Generally Recognized as Safe) notifications for MPC usage in various food applications.

The innovation ecosystem in the U.S. and Canada is characterized by a strong emphasis on "Clean-Label" and high-functionality ingredients. American consumers are increasingly seeking transparent sourcing and non-GMO certifications. The region is also home to major players like Idaho Milk Products and Glanbia Plc, who are investing heavily in R&D for personalized nutrition. In October 2023, Glanbia Nutritionals introduced a new clear whey protein isolate to meet the demand for functional sports drinks, a trend that is rapidly crossing over into the MPC space for better-tasting, clear protein waters and shakes.

Latin America Milk Protein Concentrate Market Trends and Insights

Latin America Milk Protein Concentrate Market is expected to grow at a CAGR of 8.3% as regional manufacturers prioritize high-purity fractionation for functional food systems. In Brazil, a surging fitness culture and a 60% lactose intolerance rate have catalyzed the demand for ultra-filtered, low-lactose protein isolates and heat-stable dairy concentrates. Manufacturers are now debuting ready-to-drink beverages that maintain smooth textures during high-temperature sterilization processes.

Mexico is transforming its industrial landscape by integrating specialized dairy proteins into government-backed school nutrition programs and private-sector high-protein snacks. Meanwhile, Colombia emphasizes affordable fortified liquid milks to address micronutrient deficiencies among pediatric beneficiaries. These nations are pivoting toward clean-label dairy solutions that eliminate artificial additives while boosting calcium and essential amino acids. This evolution reflects a broader regional commitment to proactive health management and innovative beverage formulation across the active Latin American food technology and dairy processing sector.

Market Competitive Landscape

The Milk Protein Concentrate Market is highly consolidated, with the top ten global players, including Fonterra, Glanbia, and Lactalis, accounting for approximately 70% of the total market share. These industry leaders maintain their dominance through vertical integration, significant R&D budgets, and strategic divestments of non-core businesses to focus on high-margin dairy ingredients. For example, Fonterra has recently realigned its resources toward nutrition solutions and sustainability to stay competitive in the "Performance Nutrition" space. The market is also seeing a rise in "Niche" players and regional dairy cooperatives that differentiate themselves through localized sourcing and specialty organic certifications. Emerging business model trends include a shift toward digital-first sports nutrition brands and the adoption of blockchain technology for "Sea-to-Shelf" traceability to enhance consumer confidence.

Key Developments:

- In February 2025,Agropur announced the Grand Champions of its Club of Excellence competition, awarding Ferme Gagnonval (Sainte-Hénédine) for outstanding milk quality and Ferme Roland Caron (Laurierville) for excellence in animal welfare, reinforcing Agropur’s commitment to quality and responsible dairy farming.

- In August 2024, Idaho Milk Products announced a major expansion with plans to build a US$200 million dual ice cream and powder blending facility at its Jerome, Idaho campus.

Companies Covered in Milk Protein Concentrate Market

- Fonterra Co-Operative Group Limited

- Arla Food Ingredients Group

- Glanbia Plc

- Lactalis Group

- FrieslandCampina

- Saputo Inc.

- Idaho Milk Products

- Molvest

- Erie Foods International

- Grassland Dairy products

- Nutrinnovate Australia

- Others

Frequently Asked Questions

The global market size is expected to reach a value of US$ 1.9 billion in 2026, growing from its base of US$ 1.5 billion in 2020.

The primary drivers include the rising global focus on high-protein diets for fitness and Sarcopenia prevention, alongside the rapid expansion of the Infant Formula market in Asia.

Asia Pacific is the leading regional segment, holding a 42% market share in 2025, largely due to the high consumption of dairy proteins in China and India.

Major opportunities lie in Technological Advancements like precision fermentation and the development of Organic and customized protein solutions for Personalized Nutrition.

Key players include Fonterra Co-Operative Group Limited, Arla Food Ingredients Group, Glanbia Plc, Lactalis Group, FrieslandCampina, Saputo Inc., Idaho Milk Products, and others