- Food Ingredients & Additives

- Soy Milk Powder Market

Soy Milk Powder Market Size, Share and Growth Forecast, 2026 - 2033

Soy Milk Powder Market by Product Type (Conventional, Organic), Application (Food & beverages, Nutritional supplements, Bakery & Confectionery, Others), and Regional Forecast for 2026 - 2033

Soy Milk Powder Market Share and Trends Analysis

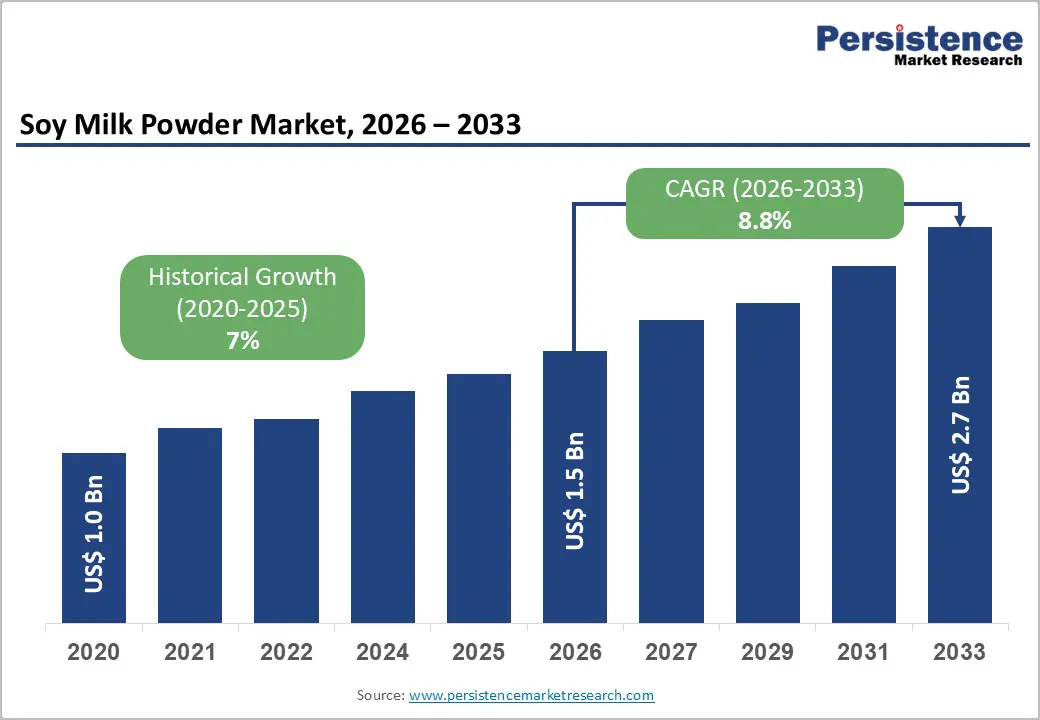

The global soy milk powder market size is likely to be valued at US$ 1.5 billion in 2026, and is projected to reach US$ 2.7 billion by 2033, growing at a CAGR of 8.8% during the forecast period of 2026–2033. This robust trajectory is driven by the accelerating adoption of plant-derived proteins across the food and beverage sectors, where manufacturers have integrated soy milk powder for its functional versatility and clean-label appeal.

Consumers have increasingly prioritized cholesterol-free and lactose-free options, responding to dietary restrictions and wellness trends that favor plant nutrition over traditional dairy. Enhanced processing methods have improved solubility, taste profiles, and nutritional density, addressing previous barriers to mainstream acceptance. Strategic growth opportunities have emerged as formulators embed soy milk powder into functional foods, infant nutrition, sports supplements, and ready-to-drink formats that demand shelf stability and cost efficiency.

Companies can gain a stronger foothold by emphasizing non-genetically modified organism (non-GMO) certification and sustainable sourcing to capture premium segments, particularly in regions where regulatory frameworks favor transparent ingredient declarations. Organizations positioning for long-term success will benefit from investing in flavor innovation and fortification strategies to differentiate their offerings amid intensifying competition from alternative plant proteins, such as oat and almond.

Key Industry Highlights

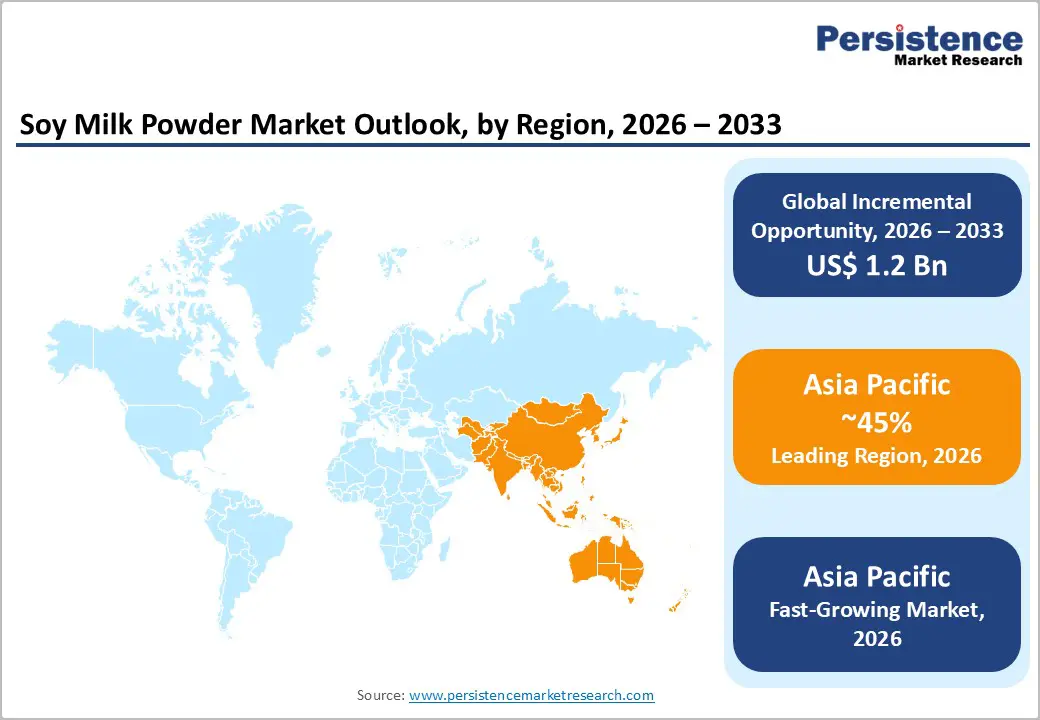

- Regional Leadership: Asia Pacific is projected to dominate with over 45% share in 2026, supported by strong consumption of soy-based nutrition products.

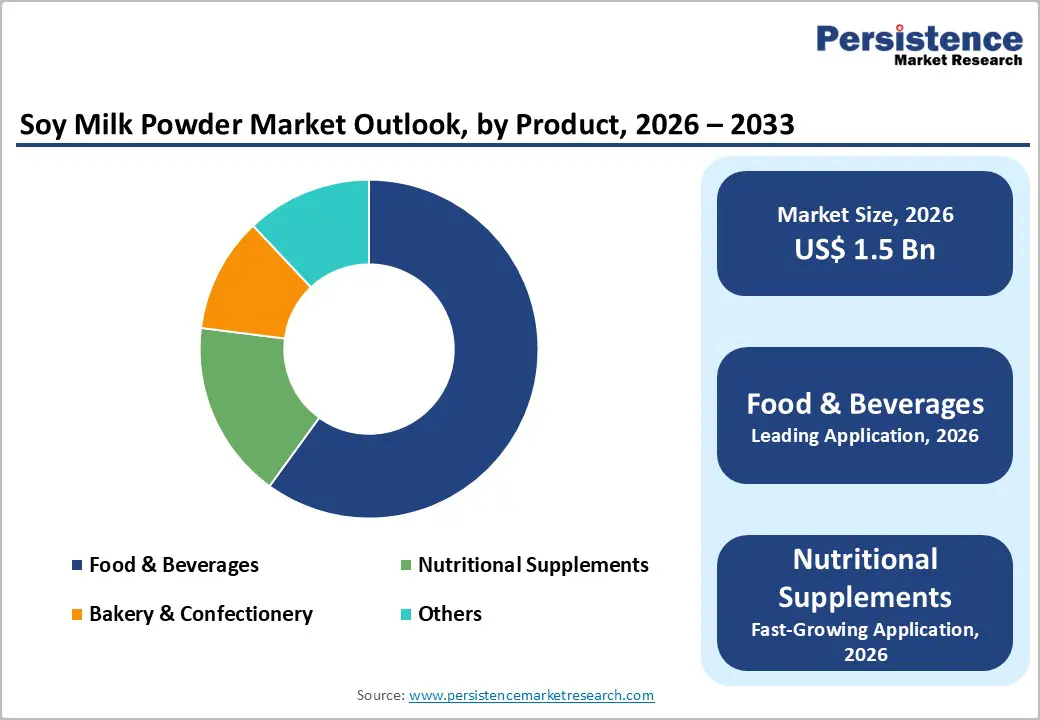

- Leading Application Segment: Food & beverages are expected to account for about 60% of the market in 2026, driven by the extensive use of non-dairy ingredients in reconstituted beverages, bakery formulations, and ready-to-mix products.

- Leading Product Type: The conventional segment is projected to lead with approximately 72% revenue share in 2026, owing to its cost efficiency and scalable production.

- Fastest-Growing Product Type: Organic powder is anticipated to register the fastest growth through 2033, aided by clean-label preference and premium nutrition demand.

- Competitive Environment: Competitive dynamics are shaped by strategic capacity expansions, product innovation, and portfolio diversification, as manufacturers focus on improving processing efficiency, expanding organic offerings, and addressing evolving nutrition-focused applications.

| Key Insights | Details |

|---|---|

|

Soy Milk Powder Market Size (2026E) |

US$ 1.5 Bn |

|

Market Value Forecast (2033F) |

US$ 2.7 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

8.8% |

|

Historical Market Growth (CAGR 2020 to 2025) |

7% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Shift toward Plant-Based, Shelf-Stable, and Nutrition-Focused Food Consumption

The soy milk powder market is growing due to a tangible shift toward plant-based, lactose-free, and nutritionally functional products. Epidemiological data from the National Institutes of Health (NIH) indicate that 70% of the global population exhibits some level of lactose malabsorption, creating sustained demand for dairy substitutes. Soy milk powder addresses this need effectively due to its high protein content, cholesterol-free profile, and nutritional equivalence to dairy milk. Its powdered format also provides extended shelf life, lower transportation costs, and ease of storage, making it suitable for both consumer and institutional applications. The versatility of soy milk powder allows its use in reconstituted beverages, bakery products, and fortified nutritional programs, ensuring broad market relevance. Growing consumer awareness of healthy, functional diets further supports adoption across demographics.

The demand for shelf-stable and long-life food products has accelerated since 2020, driven by urbanization, changing consumption habits, and supply chain resilience strategies. Soy milk powder offers logistical advantages, including reduced dependence on refrigeration, minimized waste, and ease of bulk transport, which are particularly valuable for large-scale food manufacturers and institutional programs. Several major food companies expanded plant-based processing facilities to support government-backed school nutrition and emergency food distribution programs, signaling increased confidence in the segment. This strategic capacity expansion underlines the scalability, reliability, and cost-efficiency of soy milk powder. The fortified and functional formulations further enhance its role in targeted nutrition markets. Such developments underscore soy milk powder as a resilient and sustainable protein source that supports both commercial and social nutrition initiatives. The combination of health-driven demand and operational advantages continues to propel market growth.

Supply Chain Vulnerability and Competitive Pressure from Alternative Plant-Based Milks

The ongoing challenges stem from volatility in soybean raw material prices, driven by climate variability, geopolitical trade tensions, and rising input costs. In 2025, global soybean prices fluctuated sharply as trade disruptions between the U.S. and China forced buyers to shift sourcing to Brazil, highlighting uncertainties in supply and production costs. Such volatility particularly affects smaller processors with limited hedging options, while consumer price sensitivity in emerging markets limits the ability to pass on increased costs. This creates pressure on profitability throughout the value chain and forces manufacturers to adopt more resilient supply chain strategies. Regional initiatives, such as government subsidies and improved storage infrastructure, have aimed to stabilize local soybean production. Despite these efforts, companies must continuously monitor supply risks. Maintaining predictable margins requires strategic planning and operational agility to mitigate disruptions.

The rise of alternative plant-based milk powders, including almond, oat, and pea formulations, is intensifying competition for soy milk powder producers. By April 2025, oat milk had overtaken other plant-based options in consumer preference in key markets such as the U.K., reflecting shifting tastes and allergen-driven choices. These alternatives appeal to consumers seeking lactose-free, taste-preferred, or allergen-friendly options, compelling soy milk powder companies to innovate. To maintain market share, producers are investing in R&D, product differentiation, and marketing campaigns. The growing popularity of plant-based options underscores the importance of aligning product portfolios with emerging consumer trends. Strategic innovation and branding efforts are increasingly critical. Without them, soy milk powder manufacturers risk losing relevance in a rapidly evolving market landscape.

Strategic Growth through Institutional Nutrition and Premium Product Innovation

Emerging economies offer significant potential to expand soy milk powder consumption through integration into large-scale nutrition programs and public health initiatives. In India, for instance, the government has increasingly promoted soy-based foods in school feeding schemes and maternal nutrition programs to improve protein intake and address malnutrition. Such initiatives offer manufacturers a clear avenue to partner with public institutions and develop localized production capabilities, strengthening both market presence and social impact. The focus on plant-based nutrition in institutional programs highlights growing governmental support and the opportunity for companies to align products with public health priorities.

The premium and organic soy milk powders are gaining traction among health-conscious consumers and specialized nutrition segments. Danone’s acquisition of Kate Farms, a U.S.-based plant-based organic nutrition company, demonstrates major corporate investment in high-value, clean-label offerings. Likewise, Califia Farms launched a new line of organic plant-based milk powders, reflecting the shift toward premium formulations that appeal to lifestyle, sports, and medical nutrition markets. These developments indicate that innovation in premium and organic soy milk products can create differentiated growth opportunities that complement institutional and public sector demand.

Category-wise Analysis

Product Type Insights

Conventional soy milk powder is expected to remain the dominant product type, capturing an estimated 72% revenue share in 2026, driven by its strong cost advantage, broad availability, and extensive use by mass-market food producers. This variant is especially favored in price-sensitive markets such as Asia Pacific, where it supports high consumption in beverages, bakery goods, and ready-to-mix foods. Manufacturers rely on conventional soy milk powder for its dependable supply chain and formulation versatility. Bunge announced a major soy protein concentrate launch tied to its upcoming US$550 million facility in Morristown, Indiana, demonstrating industry-wide commitment to scaling conventional soy-based proteins for broad food applications and reinforcing confidence in this core segment’s continued leadership.

Organic soy milk powder is projected to be the fastest-growing product type, expanding rapidly at a CAGR of nearly 10% through 2033, as consumers increasingly prefer clean-label, sustainably sourced products with added health benefits. Growth is particularly strong in Europe and North America, where stringent organic certification standards, regulatory support, and high consumer trust drive demand for premium offerings. This segment is gaining traction across infant nutrition, sports nutrition, and functional food categories, reflecting its versatility and higher-margin potential. In 2025, Silk (a Danone brand) expanded its U.S. plant-based portfolio with enhanced organic soy formulations, demonstrating strategic brand investment in high-value, health-oriented products. Leading companies are increasingly focusing on innovation, quality assurance, and marketing to capture this segment. The trend underscores significant opportunities for product differentiation, brand positioning, and profitability expansion beyond conventional soy milk powders. As consumer awareness of sustainability and nutrition rises, organic soy milk powder is set to remain a key driver of market growth.

Application Insights

The food & beverages segment is likely to account for approximately 60% of the soy milk powder market revenue share in 2026, driven by its extensive use in reconstituted beverages, bakery items, plant-based dairy alternatives, and ready-to-mix formulations. Large-scale food processors prefer soy milk powder for its extended shelf life, neutral taste, and formulation flexibility, making it a reliable staple for mainstream products. The ingredient’s consistency and functional properties allow manufacturers to maintain quality while meeting high-volume demand. Vitasoy International expanded its soy-based beverage and ingredient distribution across key Asia Pacific markets, reinforcing soy milk powder’s central role in everyday food applications. This move demonstrates strong industry confidence and ongoing investment to meet growing consumer demand for plant-based products. The segment’s stability and scale continue to make it a cornerstone of the global soy milk powder market.

The nutritional supplements segment is anticipated to be the fastest-growing application, with a 2026-2033 CAGR of around 9.5%, fueled by rising consumer interest in plant-based proteins, functional nutrition, and wellness-oriented products tailored to active lifestyles. Soy milk powder’s high protein content, versatility, and functional benefits make it ideal for protein blends, sports nutrition, meal replacements, and performance supplements. This segment also benefits from consumer demand for clean-label, allergen-friendly, and non-GMO products, which enhances its premium appeal. Sunwave Foods launched a new non-GMO soy protein powder specifically targeting the sports nutrition market, exemplifying innovation to meet specialized demand. Manufacturers are increasingly focusing on product development, branding, and distribution to capture growth in high-value nutrition segments. The rapid expansion of this application highlights its potential to complement mainstream food & beverage uses while driving premium market growth.

Regional Insights

North America Soy Milk Powder Market Trends

North America is slated to capture a sizeable portion of the soy milk powder market share in 2026, led by the United States, where the strong demand for organic and clean-label products is supported by a favorable regulatory environment governed by the U.S. Food and Drug Administration (FDA). The regional market benefits from advanced food processing infrastructure and widespread retail and foodservice distribution, which support innovation-driven launches and private-label expansion. Consumer interest in plant-based nutrition continues to attract companies showcasing new dairy-free and protein-fortified products. The Plant Based World Expo 2025 in New York City brought together more than 3,000 industry stakeholders, highlighting emerging plant-based innovations and reinforcing North America’s position as a hub for product development and commercial collaboration.

North America also demonstrates robust growth potential as consumers shift toward sustainable and health-oriented diets. Organic soy milk powder and fortified soy-based proteins are increasingly featured in mainstream retail and specialty channels, driven by clean-label trends and demand for functional nutrition. The region’s strong ecosystem for food innovation, including trade shows, conferences, and cross-sector partnerships, fuels ongoing interest in plant-based categories. Continued industry engagement and collaborative platforms are expected to sustain momentum, making North America both a leading market and an area of dynamic growth within the global soy milk powder landscape.

Europe Soy Milk Powder Market Trends

Europe represents a substantial share of the soy milk powder demand worldwide, with Germany, the U.K., France, and Spain leading consumption through well-established retail networks and strong adoption of plant-based products. The region’s harmonized regulatory framework, aligned with European Food Safety Authority (EFSA) standards, enhances quality assurance and supports organic certification, which resonates with sustainability-minded consumers. European food companies are increasingly focusing on plant proteins and clean-label formulations, reflecting a broader industry shift toward health and environmental goals. Fi Europe 2025 in Paris spotlighted advanced plant-based and alternative protein ingredients, showcasing how European suppliers are pushing innovations in nutrition, texture, and clean-label performance, illustrating growing investment and interest in plant-based categories.

Europe shows a decent market growth for soy milk powder applications, driven by strong institutional and consumer support for sustainable diets and diversified protein sources. Premium and organic variants are gaining traction in foodservice and retail, supported by policy goals around nutrition and environmental impact reduction. The region’s sophisticated consumer base and retail infrastructure make it fertile ground for innovative soy products, helping Europe maintain both leadership in quality and rapid growth as sustainability and functional nutrition continue to shape purchasing habits.

Asia Pacific Soy Milk Powder Market Trends

Asia Pacific is projected to continue its dominance in the soy milk powder market, with a share of approximately 45%, led by China, India, Japan, and the ASEAN countries. The region’s dominance stems from deep cultural familiarity with soy foods, high prevalence of lactose intolerance, and cost-effective manufacturing advantages that support broad consumption. Government nutrition initiatives in several markets encourage plant-based protein intake and food diversification, strengthening long-term fundamentals. The 2025 Asia Soy Foods Report, released by the U.S. Soybean Export Council, highlighted rising demand across Asian markets and the importance of soy foods in dietary patterns, emphasizing sustained growth and the need for producer engagement.

Asia Pacific is also poised to be the fastest-growing regional market for soy milk powder, with a CAGR of about 10.2% between 2026 and 2033. The market here is undergoing unprecedented expansion driven by an increase in discretionary spending, rapid urbanization, and the proliferation of e-commerce, which has broadened the consumer base for soy milk products. Premium and fortified formats are gaining acceptance among younger, health-conscious populations in urban centers. Strong regional import demand for soy ingredients, such as U.S. soy beans dominating Southeast Asian food processing illustrates the import-driven growth dynamic that supports future expansion across food, beverage, and nutrition applications.

Competitive Landscape

The global soy milk powder market structure is moderately fragmented, comprising multinational food and beverage companies, specialized soy ingredient manufacturers, and strong regional players. Leading companies leverage large-scale processing capabilities, established soybean sourcing networks, and diversified product portfolios to serve food & beverage, institutional, and nutrition segments. Cost efficiency, consistent quality, and supply reliability remain key competitive factors. Major players continue to invest in processing technology, fortification, and quality assurance to strengthen market positioning. Long-term contracts with food manufacturers and nutrition programs further reinforce their competitive advantage.

Regional and niche manufacturers compete by focusing on specific geographies, organic and non-GMO products, or specialized applications such as infant and sports nutrition. Entry barriers include food safety compliance, organic certification requirements, and capital-intensive processing infrastructure. However, clean-label demand and localized sourcing strategies enable smaller players to differentiate. Strategic partnerships and co-manufacturing agreements are becoming more common. Gradual market consolidation is expected as leading companies expand capacity and enhance premium product portfolios.

Key Industry Developments

- In December 2025, Alinova Canada Inc. invested nearly US$ 24 million to build Canada's first non-GMO soymilk powder processing plant in Ontario, using local soybeans to produce over 1,200 metric tonnes annually. The Ontario government supports the project with US$ 1.5 million through the Eastern Ontario Development Fund, creating 15 jobs and enhancing agri-food processing capacity amid global protein demand.

- In November 2025, Dutch Mill Thailand introduced DNA Soy Milk High-Protein in Black Soybean and Golden Pea flavors, each providing 15g of quality protein per carton for health-focused consumers. The no-added-sugar, zero-cholesterol formula offers natural sweetness to energize active lifestyles conveniently.

- In April 2025, Nestlé launched Bear Brand Milk N’Soy, a powdered hybrid drink blending dairy and soy proteins with proprietary enzymes for optimal texture and flavor, targeting nutritional gaps in Philippine schoolchildren over age 3. The product delivers protein, calcium, magnesium, vitamin D, and fiber to combat stunting and undernutrition amid rising obesity.

Companies Covered in Soy Milk Powder Market

- Archer Daniels Midland

- Cargill Inc.

- Danone S.A.

- Nestlé S.A.

- Kerry Group plc

- CHS Inc.

- SunOpta Inc.

- Fuji Oil Holdings Inc.

- Vitasoy International Holdings Ltd.

- Yili Group

- China Mengniu Dairy Company Ltd.

- Kikkoman Corporation

- NOW Health Group

- Blue Diamond Growers

- Organic Valley

- Devansoy Inc.

Frequently Asked Questions

The global soy milk powder market is projected to reach US$ 1.5 billion in 2026.

Key growth drivers include increasing lactose intolerance awareness, expanding demand for plant-based dairy alternatives, longer shelf-life advantages, and growing use of soy milk powder in packaged foods, beverages, and nutritional products.

The market is poised to witness a CAGR of 8.8% between 2026 and 2033.

Major opportunities include premiumization through organic and clean-label products, expansion of soy-based nutritional supplements, increased penetration in emerging markets, and innovation in fortified and functional soy formulations.

Some of the leading companies in the market include Archer Daniels Midland, Cargill Inc., Danone S.A., Fuji Oil Holdings, Kerry Group, and Nestlé S.A.