- Hardware & Software IT Services

- Middleoffice BPO Services Market

Middleoffice BPO Services Market Size, Share, and Growth Forecast 2026 - 2033

Middleoffice BPO Services Market by Service Type (Insurance BPO, Banking BPO, Government, Knowledge Process Outsourcing services, and Others), Deployment Mode (On-Premises and Cloud), Enterprise Size (Small and Medium Enterprises and Large Enterprises), Vertical (BFSI, Manufacturing, Healthcare & Pharmaceuticals, and Retail & Consumer Goods), and Regional Analysis

Middleoffice BPO Services Market Size and Share Analysis

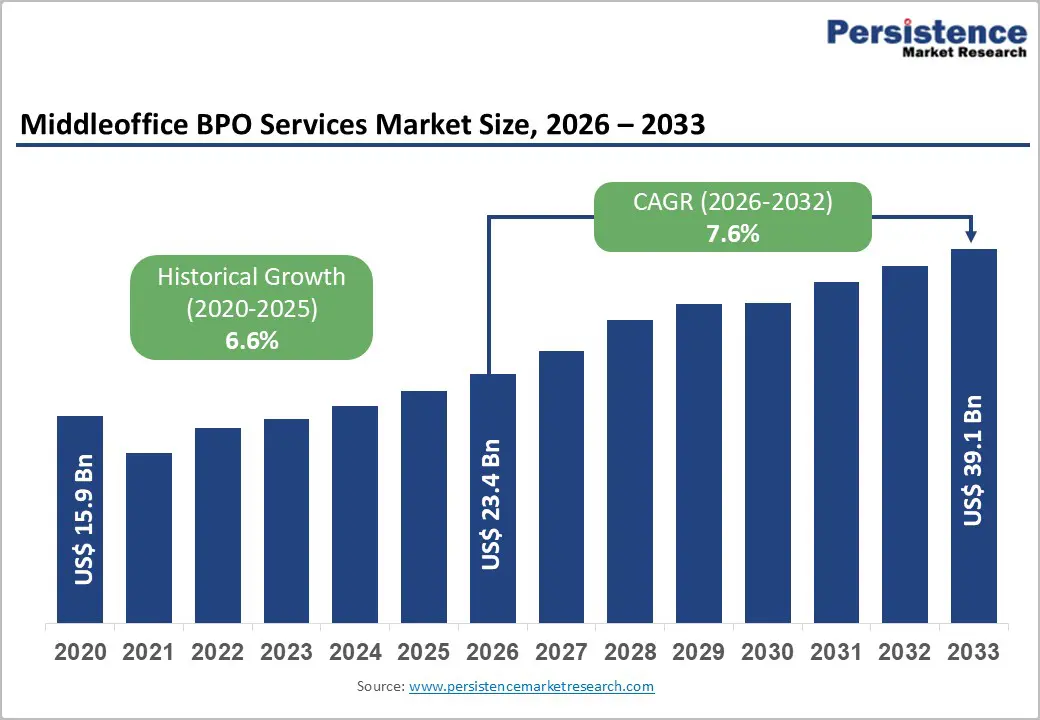

The global Middle Office BPO Services market size was valued at US$ 23.4 billion in 2026 and is projected to reach US$ 39.1 billion by 2033, growing at a CAGR of 7.6% between 2026 and 2033.

The market expansion is fundamentally driven by accelerated digital transformation initiatives across the financial services and insurance sectors, escalating demand for cloud-based middle-office solutions, and organizations' strategic imperative to achieve cost optimization through outsourcing non-core functions. Cloud-based BPO deployment accounted for approximately 52% of the broader BPO market in 2024, reflecting enterprise organizations' preference for scalable, flexible infrastructure that supports rapid business transformation.

Key Market Highlights

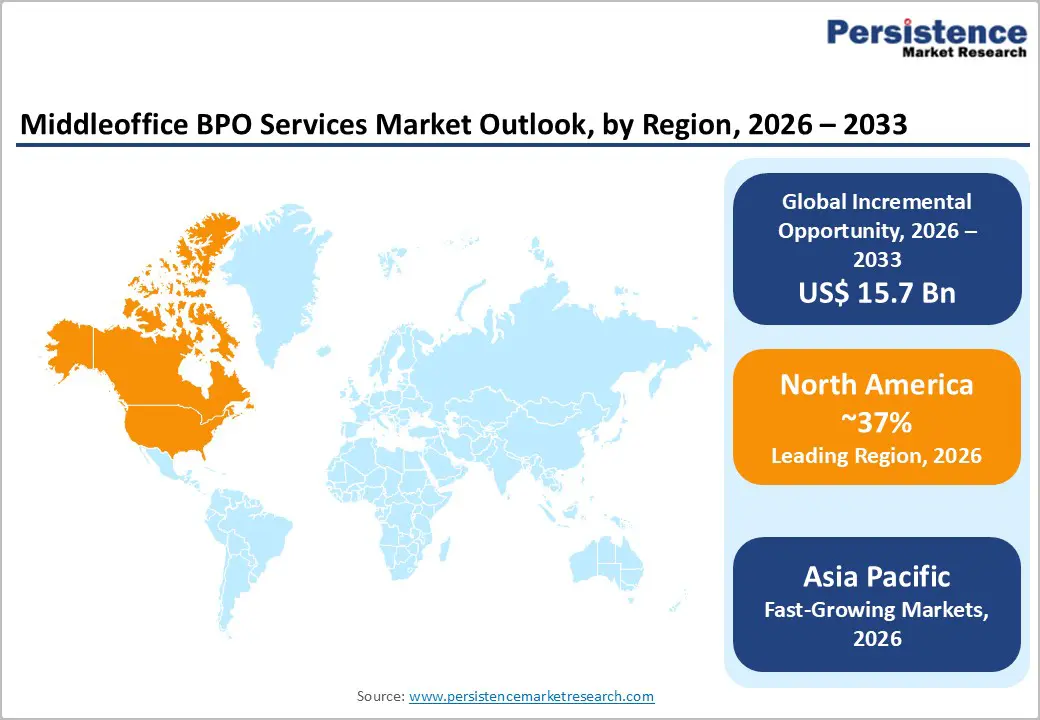

- Leading Region: North America dominates the Middle Office BPO Services market with approximately 37% global market share, driven by concentration of major financial institutions, insurance companies, advanced technology infrastructure, and demand for specialized outsourced services addressing cost optimization and regulatory compliance requirements.

- Fastest Growing Region: Asia Pacific represents the fastest-growing regional market, driven by India's mature talent pools and technology capabilities, China's emerging BPO expansion, government policy support for IT services, and expanding domestic demand from Chinese conglomerates and ASEAN manufacturers pursuing sophisticated analytics.

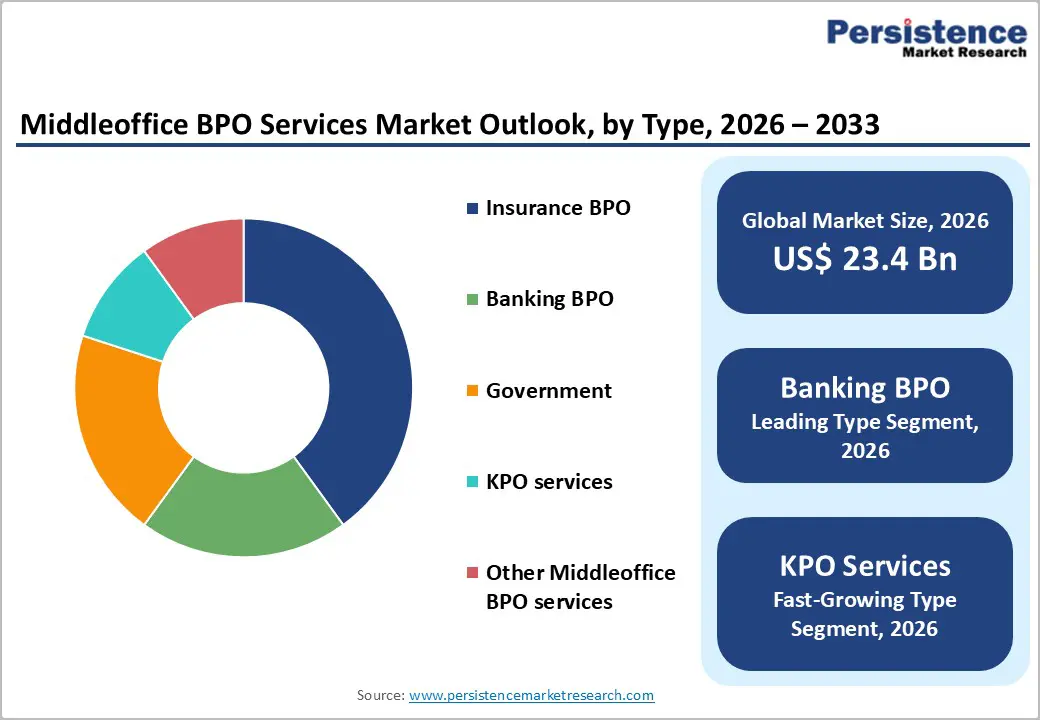

- Dominant Service Type: Banking Business Process Outsourcing represents the dominant service type segment with approximately 42% market share, encompassing mortgage processing, credit card operations, and finance and accounting functions critical to banking operations and cost optimization.

- Growing Service Type: Knowledge Process Outsourcing services expand at approximately 9.1% CAGR through 2033, driven by organizations' demand for specialized analytical expertise, research capabilities, and strategic business intelligence supporting enhanced decision-making and competitive differentiation.

- Key Market Opportunity: Healthcare and Life Sciences BPO services expansion represents the principal market opportunity, growing from US$ 417.7 billion in 2025 to US$ 694.3 billion by 2030, driven by regulatory compliance requirements, medical coding outsourcing, and healthcare organizations' emphasis on patient care over administrative functions.

| Key Insights | Details |

|---|---|

|

Global Middle Office BPO Services Market Size (2026E) |

US$ 23.4 Bn |

|

Market Value Forecast (2033F) |

US$ 39.1 Bn |

|

Projected Growth CAGR (2026-2033) |

7.6% |

|

Historical Market Growth (2020-2025) |

6.6% |

Market Dynamics

Market Growth Drivers

Digital Transformation and Cloud-Based Infrastructure Adoption

The accelerated adoption of cloud computing technologies is a fundamental driver of the middle office BPO services market's expansion, as organizations increasingly transition from legacy on-premises infrastructure to scalable, flexible cloud-based operational models. Cloud-based BPO deployment solutions accounted for 52% of the broader business process outsourcing market in 2024, as organizations recognized substantial advantages in cost efficiency, implementation speed, and operational agility. Industry forecasts indicate that approximately 83% of enterprise workloads will be processed via cloud infrastructure by 2025, reflecting the structural shift toward cloud-native service delivery models.

Cloud-based middle office solutions enable financial services and insurance organizations to streamline operations without requiring substantial capital investments in physical infrastructure, reducing operational expenditure while simultaneously improving scalability to accommodate fluctuating business demands. Middle office outsourcing platforms delivered through cloud infrastructure demonstrate a CAGR of approximately 21.8%, substantially exceeding growth rates of traditional on-premises models. Organizations leverage cloud-based BPO services for critical middle office functions, including trade settlement, performance calculation and attribution, data management, and risk analytics, with providers deploying solutions across Amazon Web Services (AWS), Microsoft Azure, and Google Cloud Platform (GCP).

Cost Optimization Requirements and Talent Shortage Resolution

Organizations across BFSI and other verticals face escalating pressure to optimize operational costs while addressing global talent shortages, making specialized middle-office BPO providers strategically essential to maintain competitiveness and service quality. According to the research, 59% of financial services organizations cite cost savings as the primary motivation for outsourcing middle office functions, reflecting the financial imperative driving outsourcing adoption. Global talent scarcity, particularly for specialized financial services and technical expertise, has incentivized organizations to leverage offshore delivery models, with BPO providers establishing delivery centers in cost-competitive geographies such as India, the Philippines, Mexico, and Eastern Europe.

The acceleration of remote work capabilities post-COVID has fundamentally transformed talent acquisition dynamics, enabling organizations to access specialized professionals globally without geographic constraints, substantially expanding addressable talent pools. Financial institutions outsource billions of dollars in IT and operations annually, with life insurers alone expected to outsource approximately US$ 28 billion in IT and operations by 2026. Cost-conscious procurement teams increasingly demand bundled outsourcing arrangements that combine digital tools, process optimization, and outcome-based performance guarantees, creating a competitive advantage for providers that demonstrate rapid ROI and measurable cost reduction.

Market Restraints

Data Security, Cybersecurity, and Regulatory Compliance Complexities

The middle-office BPO services market faces substantial challenges from escalating data security requirements, evolving cybersecurity threats, and increasingly complex regulatory frameworks, which elevate operational costs and complexity for service providers and their clients. Middle office functions involve processing sensitive financial and customer information, which requires robust security infrastructure, encryption protocols, and cybersecurity defenses to protect against sophisticated threat actors. Organizations must comply with stringent regulatory frameworks, including GDPR, CCPA, Basel IV, and sector-specific regulations governing data handling, privacy protection, and financial reporting, imposing substantial compliance costs on BPO providers and their customers.

European Central Bank cyber-resilience stress tests and regulatory emphasis on liquidity risk management and internal governance have substantially increased compliance obligations for financial institutions that outsource middle-office functions. The complexity and cost of maintaining compliance across multiple regulatory jurisdictions create barriers, particularly for smaller organizations lacking specialized compliance expertise or capital resources. Security breaches involving outsourced service providers can impose devastating reputational and financial consequences for client organizations, creating reluctance to outsource highly sensitive functions despite cost reduction incentives.

Legacy System Integration Challenges and Operating Model Complexity

Organizations maintaining heterogeneous technology landscapes characterized by disparate legacy systems, proprietary databases, and fragmented data architectures encounter substantial complications in integrating modern middle office BPO solutions, limiting market adoption, particularly among mature enterprises. Middle office outsourcing service providers report that operating model customization and technology system integration represent persistent challenges as client requirements increasingly exceed service provider standardization capabilities.

Approximately 44% of small firms and 61% of large firms have outsourced middle-office functions, with the remaining organizations delaying adoption due to integration complexity and concerns about operational continuity during transition periods. Legacy system constraints, including data format incompatibility, restricted API availability, and limited interoperability, create substantial change management costs and extended implementation timelines. The tension between client demand for customization and providers' preference for standardization creates operational friction, with BPO providers facing margin compression as change costs and technology investments escalate.

Market Opportunities

Knowledge Process Outsourcing and High-Value Analytics Services Expansion

Knowledge Process Outsourcing services represent the fastest-growing segment within the broader middle office BPO market, driven by organizations' strategic imperative to access specialized analytical and research expertise supporting enhanced business decision-making and competitive differentiation. The Knowledge Process Outsourcing market is expected to reach US$ 297.5 billion by 2034 from US$ 124.29 billion in 2024, expanding at a CAGR of approximately 9.1%, substantially exceeding growth rates of traditional transaction-based BPO services. North America contributed over 36% of global KPO revenues in 2024, with enterprises outsourcing complex analytical tasks requiring advanced skills and domain-specific knowledge to specialized providers.

Organizations increasingly outsource research and development, engineering design, financial analysis, legal process outsourcing, and regulatory compliance functions to providers maintaining specialized expertise and offshore delivery capabilities. Large enterprises contributed 61.3% of the KPO market revenue in 2024, but emerging AI-driven self-service platforms are democratizing access, enabling small and medium enterprises to engage in modular analytics and specialized services at 20.4% CAGR. Providers differentiating through deepening domain specialization, seamless human-AI collaboration, and modular team structures aligned with client needs are capturing premium market positioning.

Healthcare and Life Sciences BPO Services Acceleration

The healthcare and life sciences vertical represents an exceptionally compelling market opportunity for middle office BPO providers, driven by regulatory compliance requirements, escalating operational complexity, and organizations' strategic focus on patient care delivery over administrative functions. The global healthcare BPO market is valued at US$ 417.7 billion in 2025 and is projected to grow to US$ 694.3 billion by 2030, representing extraordinary market expansion opportunities for experienced healthcare BPO specialists. Healthcare organizations increasingly outsource medical coding, claims processing, revenue cycle management, data analytics, and compliance-related functions to specialized providers with healthcare domain expertise and an understanding of complex reimbursement regulations.

Insurance BPO services grew at approximately 5.4% CAGR, with life insurers outsourcing policy administration, claims management, and annuity block administration to specialized providers, achieving operational excellence. Pension risk transfer administration represents a US$ 45 billion market in 2024, with complex regulatory requirements and specialized underwriting expertise creating substantial outsourcing opportunities. Regulatory mandates, including the HIPAA Emergency Preparedness Rule and accreditation standards, drive healthcare organizations to establish comprehensive business continuity and disaster recovery capabilities, creating demand for managed services providers that offer integrated solutions to support healthcare operations.

Category-wise Insights

Service Type Analysis

The banking business process outsourcing segment represents the dominant service type within the middle office BPO market, commanding approximately 42% of total market share, encompassing mortgage processing, credit card processing, finance and accounting, and transaction processing functions critical to banking operations. Banking BPO services include policy issuance, premium collection, and policy maintenance for insurance subsidiaries, with specialized providers leveraging advanced technology for accuracy, compliance, and efficiency. The BFSI BPO services market is expected to grow from US$ 130.26 billion in 2025 to reach US$ 269.63 billion by 2033, reflecting sustained demand for specialized outsourced services addressing cost pressures and regulatory complexity.

Insurance BPO services account for approximately 38% of market share, with providers specializing in policy administration, claims processing, underwriting, and compliance management that employ advanced AI and machine learning technologies. Knowledge Process Outsourcing services are experiencing the fastest growth, with a CAGR of approximately 19.1% through 2034, encompassing research, analytics, legal process outsourcing, and specialized knowledge work requiring advanced professional expertise. Government BPO services and Other Middle Office BPO Services collectively account for the remaining market share, supporting public-sector organizations and specialized verticals.

Deployment Mode Analysis

The Cloud-based deployment mode represents the fastest-growing segment, capturing approximately 52% of the broader BPO market and expanding at exceptional rates as organizations prioritize digital transformation and operational agility. Cloud-based middle office solutions delivered through Amazon Web Services, Microsoft Azure, and Google Cloud Platform provide superior scalability, accessibility, and cost efficiency compared to traditional on-premises models. Cloud deployment enables BPO providers to implement faster, reduce capital expenditure requirements, and offer flexible consumption-based pricing models, aligning with client cost management objectives.

In 2025, approximately 83% of enterprise workloads will utilize cloud infrastructure, establishing cloud as the dominant deployment paradigm for enterprise applications, including middle office BPO services. The On-Premises deployment mode maintains approximately 48% market share, particularly prevalent among regulatory-constrained organizations including financial institutions and government agencies requiring stringent data residency controls and offline operational continuity. However, growth rates for on-premises deployments are declining as organizations recognize the advantages of cloud deployment. Hybrid deployment approaches combining on-premises core systems with cloud-based analytics and reporting are gaining organizational adoption as enterprises seek balanced optimization of control, compliance, and scalability.

Enterprise Size Analysis

The Large Enterprise segment commands the dominant market position, accounting for approximately 63% of the middle office BPO services market, reflecting the complex organizational structures, geographic distribution, and substantial operational scale requiring specialized outsourced services. Large enterprises command 61-63% of Business Process Outsourcing market revenues, with organizations possessing sophisticated procurement processes, substantial service budgets, and demand for integrated solutions spanning multiple service categories. Large enterprises maintain established relationships with tier-one BPO providers including Accenture, IBM, Capgemini, and Cognizant, leveraging consolidated partnerships enabling economies of scale and enhanced service alignment with strategic objectives.

The Small and Medium Enterprises (SMEs) segment accounts for approximately 37% of market share and is experiencing faster growth as emerging automation technologies and modular service models democratize access to sophisticated BPO services that were previously accessible primarily to large organizations. AI-driven self-service platforms and emerging no/low-code automation technologies enable SMEs to engage specialized services at 20.4% CAGR, reducing technology barriers and enabling organizations with limited internal IT expertise to leverage advanced analytics and operational optimization services. Providers increasingly emphasize flexible engagement models with outcome-based pricing structures supporting SME cost management objectives.

Vertical Analysis

The Banking, Financial Services, and Insurance (BFSI) vertical dominates the middle office BPO services market, commanding approximately 58% of total market share, driven by the sector's complex regulatory requirements, cost pressures, and operational complexity, which necessitate specialized outsourced services. THE BFSI BPO services market is expected to grow from US$ 130.26 billion in 2025 to reach US$ 269.63 billion by 2033, representing extraordinary market expansion opportunities. Insurance organizations are particularly active in outsourcing policy administration, claims processing, and actuarial support functions, with specialized providers commanding premium positioning through domain expertise and regulatory fluency.

Banking institutions outsource mortgage processing, credit card operations, finance and accounting, and transaction processing to achieve cost efficiencies and access specialized expertise. The Healthcare and Pharmaceuticals vertical represents approximately 18% of market share, with rapid expansion driven by regulatory compliance requirements and organizations' emphasis on patient care over administrative functions. Medical billing, claims processing, revenue cycle management, and data analytics outsourcing are growing rapidly, with the healthcare BPO market projected to grow from US$ 417.7 billion in 2025 to US$ 694.3 billion by 2030. Manufacturing and Retail & Consumer Goods verticals collectively account for the remaining 24% market share, with increasing outsourcing of non-core financial and operational functions.

Regional Insights

North America Middleoffice BPO Services Trends

North America maintains regional dominance with approximately 37-40% of the global middle office BPO services market share, supported by the concentration of major financial services institutions, insurance companies, and sophisticated enterprise organizations demanding specialized outsourced services. The United States hosts the headquarters of leading BPO providers, including Accenture, IBM, and Cognizant, establishing the region as a center of service innovation and technology advancement. North American financial institutions and insurance companies extensively outsource mortgage processing, claims administration, and finance and accounting functions to access cost efficiencies and specialized expertise. Organizations in the region emphasize regulatory compliance and data security, driving demand for BPO providers maintaining robust security infrastructure, comprehensive compliance expertise, and advanced threat detection capabilities.

The region benefits from mature BPO market infrastructure, established vendor relationships, and sophisticated purchasing processes enabling large enterprises to consolidate relationships with tier-one providers achieving operational synergies. Cost optimization pressures and intense competitive dynamics are compelling North American organizations to expand outsourcing to include increasingly complex middle office functions, from traditional transaction processing toward analytics and specialized knowledge work. Cloud adoption in North America exceeds 85% among large enterprises, driving a rapid migration of middle-office services to cloud-based delivery models. Digital transformation initiatives, including AI and machine learning integration into middle-office processes, are advancing more rapidly in North America than in other regions, creating first-mover advantages for organizations implementing sophisticated automation capabilities.

Europe Middleoffice BPO Services Trends

Europe represents a significant regional market characterized by stringent regulatory frameworks, data privacy requirements, and emphasis on sustainable business practices influencing middle office BPO delivery models. European Union General Data Protection Regulation (GDPR) and regulatory harmonization initiatives have substantially elevated compliance and data residency requirements affecting BPO service providers and their client organizations. Financial institutions and insurance companies in Germany, the United Kingdom, France, and Spain extensively outsource middle office functions to specialized providers possessing deep regulatory expertise and compliance capabilities. European organizations emphasize long-term strategic partnerships with BPO providers over transactional vendor relationships, valuing providers capable of supporting digital transformation initiatives while maintaining stringent compliance and data protection standards.

The region demonstrates cautious adoption of emerging technologies compared to North America, with European organizations prioritizing proven reliability and operational stability over cutting-edge technological implementations. Regulatory emphasis on financial stability, anti-money laundering compliance, and cybersecurity risk management have created sustained demand for specialized BPO services addressing compliance obligations. European BPO providers maintain substantial competitive positioning through deep regulatory expertise, established customer relationships within European financial institutions, and specialized knowledge of regional business practices. Cloud adoption is advancing more gradually than in North America, with organizations maintaining preferences for hybrid deployment models balancing compliance requirements with modernization objectives.

Asia Pacific Middleoffice BPO Services Trends

Asia Pacific is emerging as the fastest-growing regional market for middle office BPO services, with Knowledge Process Outsourcing services demonstrating 20.1% CAGR, substantially exceeding growth rates in mature western markets. India has established itself as the region's dominant BPO delivery hub, leveraging mature talent pools, government policy support for IT services, and cost-competitive labor enabling organizations to achieve extraordinary cost reductions through offshore outsourcing. Asia Pacific countries including Vietnam, Philippines, Malaysia, and Thailand are rapidly expanding BPO capabilities, attracting substantial investments from global BPO providers and creating delivery center competition. Governments across Southeast Asia are investing in STEM education, digital infrastructure, and 5G networking, positioning the region for sustained talent development and service delivery capacity expansion.

Domestic demand for BPO services is accelerating across Asia Pacific as Chinese conglomerates, Indian enterprises, and ASEAN manufacturers pursue sophisticated analytics and specialized knowledge work, creating growth opportunities beyond traditional offshore delivery models. China is rapidly expanding middle office BPO capabilities with government support, particularly in technology-enabled process automation and artificial intelligence applications. Organizations across Asia Pacific are transitioning from cost-focused outsourcing toward strategic partnerships delivering innovation, specialized expertise, and transformational capability. The region's manufacturing advantages and rapidly maturing technological capabilities position Asia Pacific as an increasingly important source of innovative BPO solutions addressing global market demands.

Competitive Landscape for the Middleoffice BPO Services Market

The Middle Office BPO Services market exhibits substantial consolidation among established tier-one providers, with Accenture, IBM, Capgemini, Cognizant, and HCL Technologies dominating market competition through superior technology capabilities, extensive client relationships, and global delivery infrastructure. Market leaders employ differentiated strategies emphasizing cloud-native service delivery, AI-powered process automation, and specialized vertical expertise addressing BFSI, healthcare, and manufacturing client requirements. Tier-one vendors invest aggressively in research and development, acquiring emerging technologies and specialized service capabilities to maintain competitive positioning. Competitive strategies emphasize building comprehensive service portfolios spanning transaction processing, analytics, and knowledge work, enabling clients to consolidate relationships and achieve operational synergies. Emerging providers from India, Philippines, and Eastern Europe are leveraging cost advantages and technological capabilities to capture market share from established vendors through specialized service offerings and niche vertical focus. Market consolidation through mergers and acquisitions continues as vendors seek to expand service portfolios, enter new vertical markets, and build technological capabilities supporting digital transformation client requirements.

Key Market Developments

- In December 2024, Accenture PLC announced comprehensive expansion of cloud-based middle office BPO capabilities, integrating generative AI and advanced analytics to support client digital transformation initiatives across BFSI and healthcare verticals, enhancing competitive positioning in rapidly growing cloud-based service markets.

- In October 2024, International Business Machines Corporation repositioned its BPO service offerings toward outcome-based pricing and AI-enabled automation, emphasizing measurable client value delivery and rapid return-on-investment achievement as differentiating competitive factors.

- In August 2024, Cognizant Technology Solutions Corp completed acquisition of specialized middle office automation technology company, expanding capabilities in trade settlement automation, performance calculation, and real-time data management supporting financial services clients.

Companies Covered in Middleoffice BPO Services Market

- Accenture PLC

- International Business Machines Corporation

- Capgemini

- Cognizant Technology Solutions Corp

- Mphasis Ltd

- Capita PLC

- Hewlett Packard Enterprise Company

- HCL Technologies

- State Street Corporation

- ADP LLC

Frequently Asked Questions

The global Middle Office BPO Services market is projected to reach US$ 39.1 billion by 2033, growing from US$ 23.4 billion in 2026 at a CAGR of 7.6%, driven by digital transformation initiatives, cloud adoption, cost optimization requirements, and regulatory compliance pressures across BFSI and healthcare verticals.

Primary demand drivers include accelerated cloud-based infrastructure adoption with 52% of BPO market through cloud deployment, cost optimization requirements with 59% of financial services citing cost savings motivation, global talent shortages driving offshore delivery models, regulatory compliance complexity including GDPR, CCPA, and Basel IV requirements, and artificial intelligence and machine learning integration enhancing operational efficiency across policy administration, claims processing, and financial functions.

Banking Business Process Outsourcing represents the dominant service type with approximately 42% market share, encompassing mortgage processing, credit card operations, and finance and accounting functions, with BFSI BPO services market expected to grow from US$ 130.26 billion in 2025 to US$ 269.63 billion by 2033.

North America leads the global Middle Office BPO Services market with approximately 37% market share, supported by concentration of major financial institutions and insurance companies, sophisticated enterprise organizations, established BPO provider headquarters, and demand for specialized outsourced services addressing cost optimization and regulatory compliance.

Healthcare and Life Sciences BPO services expansion represents the principal market opportunity, projected to grow from US$ 417.7 billion in 2025 to US$ 694.3 billion by 2030, driven by regulatory compliance requirements, medical coding and claims processing outsourcing, healthcare organizations' emphasis on patient care, and specialized expertise demand in healthcare operations management.

Leading market players include Accenture PLC leveraging cloud-native delivery and AI integration; International Business Machines Corporation emphasizing outcome-based service models; Capgemini providing digital transformation services; Cognizant Technology Solutions Corp specializing in BFSI and healthcare; HCL Technologies expanding middle office automation; and Mphasis Ltd, Genpact Limited, and Infosys Limited maintaining strong competitive positioning through specialized service offerings and global delivery capabilities.