- Agrochemicals

- MEA Household Insecticides Market

MEA Household Insecticides Market Size, Share, and Growth Forecast, 2025 - 2032

MEA Household Insecticides Market by Product Type (Gel/Cream, Mat, Roll on, Patches, Powdered Granules and Liquid), by Sales Channel (Store-based retailing, Supermarket, Drug Stores & Pharmacy, Departmental Stores and Online Retailers), by Application (Cockroaches, Mosquitoes, Ants, Flies & Moths, and Others, by Nature, and Country Analysis for 2025 - 2032

MEA Household Insecticides Market Size and Share Analysis

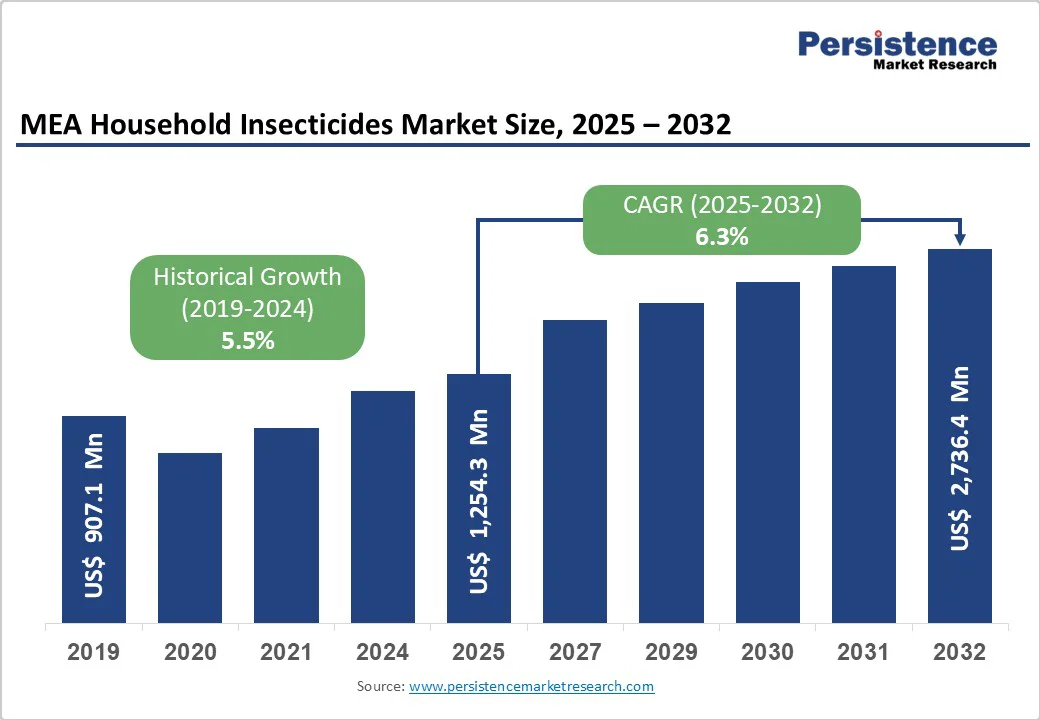

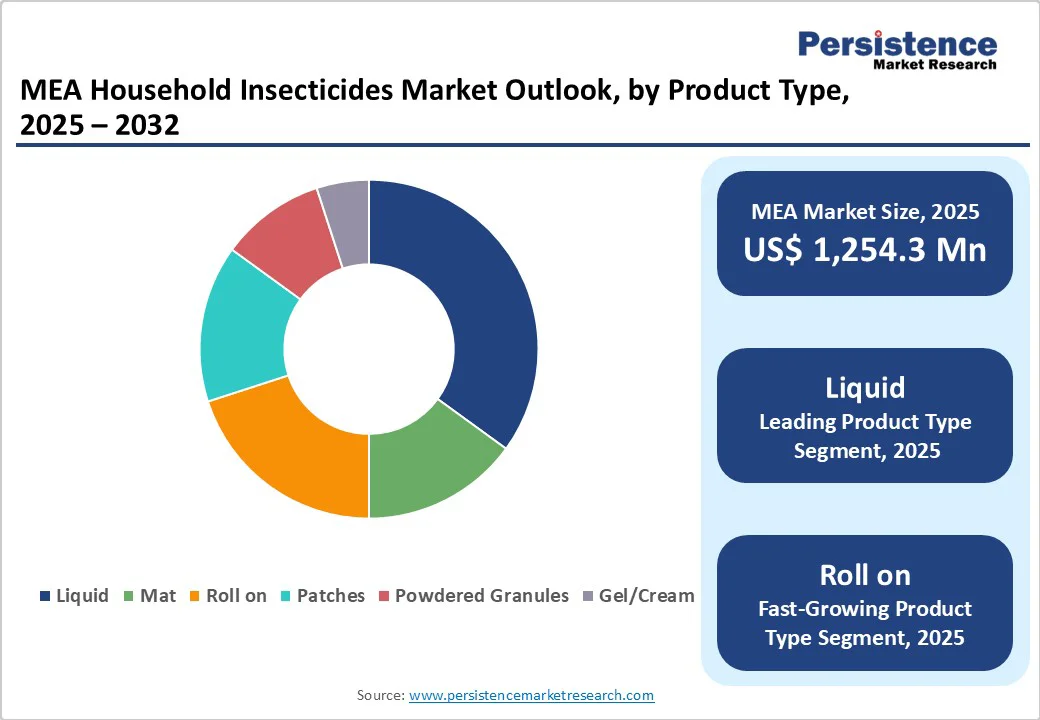

The Middle East & Africa Household Insecticides market size was valued at US$ 1,254.3 million in 2025 and is projected to reach US$ 2,736.4 million by 2032, growing at a CAGR of 6.3% between 2025 and 2032. This robust growth trajectory reflects the region's increasing focus on public health protection, driven by rising vector-borne disease prevalence and accelerating urbanization patterns.

Key Highlights of the Market

- Product Segments: Liquid formulations lead the market with a 37.3% share in 2025, driven by their versatility, ease of application, and proven effectiveness across diverse pest control scenarios. The fastest-growing segment is roll-on applications, fueled by consumer lifestyle shifts toward portability, convenience, and on-the-go protection solutions.

- Application Segments: Mosquito control dominates with a 30.6% market share in 2025, underscoring ongoing public health efforts to mitigate vector-borne diseases. The ant control segment is projected to grow at the fastest rate, supported by increasing urban infestations and rising demand for targeted household pest management products.

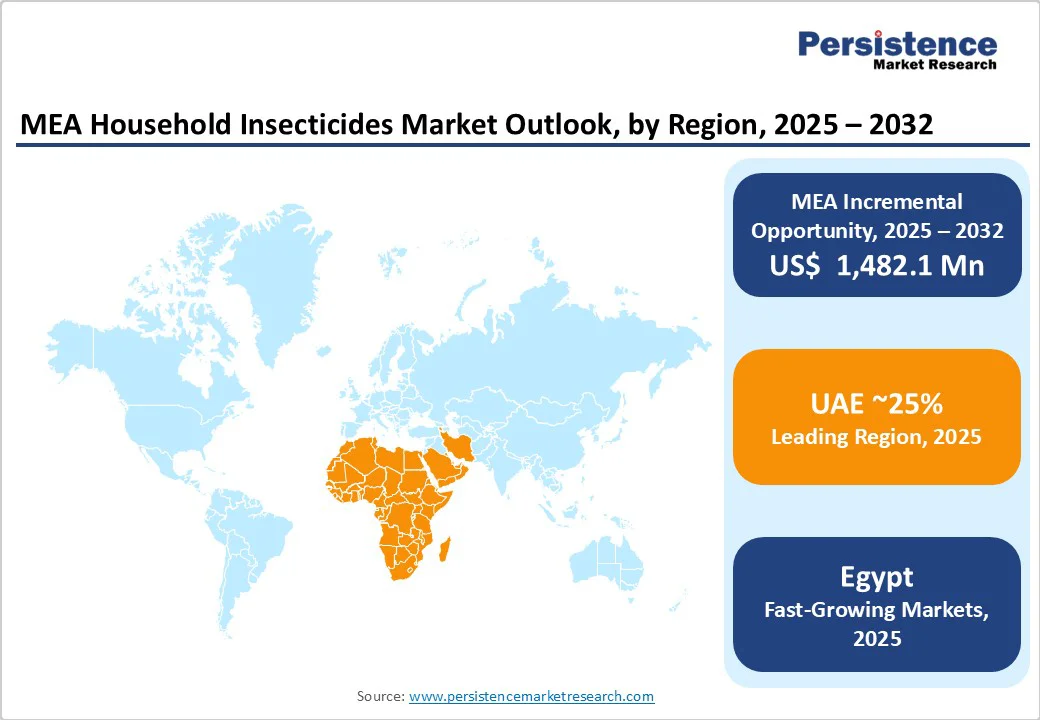

- Regional Leaders: UAE leads the MEA household insecticides market with a 23.3% share, driven by tourism growth, high urban density, and climatic conditions that favor pest proliferation. Strong retail infrastructure and premium product availability further reinforce its market leadership.

- Distribution Channels: Store-based retailing accounts for 30.5% of total sales in 2025, reflecting sustained consumer trust in traditional outlets. Supermarkets and hypermarkets represent the fastest-growing channel, benefiting from product accessibility, bulk purchasing options, and integrated shopping convenience.

- Formulation Innovation: Synthetic products maintain a dominant 73.8% share in 2025 due to consistent efficacy and cost-effectiveness. However, natural and bio-based alternatives are expanding rapidly, driven by consumer awareness of eco-friendly formulations and regulatory emphasis on sustainable pest control solutions.

- Strategic Developments: The market is witnessing consolidation through mergers and acquisitions aimed at portfolio diversification and regional penetration. Notable moves include UPL’s collaboration with Corteva and Sumitomo Chemical’s expansion initiatives, emphasizing innovation-led growth and global competitiveness.

| Key Insights | Details |

|---|---|

| MEA Household Insecticides Market Size (2025E) | US$ 1,254.3 Mn |

| Projected Market Value (2032F) | US$ 2,736.4 Mn |

| Forecast Growth Rate (CAGR 2025 to 2032) | 6.3% |

| Historical Growth Rate (CAGR 2019 to 2024) | 5.5% |

Market Dynamics Analysis

Driver - Rising Vector-Borne Disease Prevalence

The MEA region faces substantial public health challenges from mosquito-transmitted diseases, with malaria, dengue, and chikungunya cases reaching epidemic proportions in several countries. According to WHO data, vector-borne diseases affect over 80% of the global population at risk, with the MEA region experiencing disproportionately high mortality rates.

The region's warm and humid climate conditions create ideal breeding environments for disease vectors, necessitating continuous household protection measures. Government health authorities actively promote mosquito control initiatives through national awareness campaigns, directly driving consumer adoption of household insecticides.

This health imperative generates consistent year-round demand, particularly during monsoon seasons when vector populations peak.

Accelerating Urbanization and Infrastructure Development

Rapid urban expansion across MEA countries has intensified pest management challenges, with population density increases creating favorable conditions for insect proliferation. Urban centers in the UAE, Egypt, and Saudi Arabia are experiencing unprecedented growth rates, leading to sanitation pressures and increased human-vector contact opportunities.

The construction boom has inadvertently created numerous breeding sites for mosquitoes and other pests, while improved living standards have elevated consumer expectations for pest-free environments. Modern residential complexes and commercial establishments mandate effective pest control solutions, creating sustained market demand.

Additionally, the hospitality sector's expansion, particularly in tourism-dependent economies like the UAE, requires comprehensive pest management to maintain international service standards.

Restraint - Health and Environmental Safety Concerns

Growing awareness of potential health risks associated with synthetic insecticides has created consumer hesitancy, particularly regarding products containing DEET and other neurotoxic compounds. Prolonged exposure concerns related to respiratory and dermatological effects are constraining market penetration among health-conscious households.

Regulatory scrutiny has intensified, with authorities implementing stricter guidelines on chemical concentrations and labeling requirements, increasing compliance costs for manufacturers. The contradiction between effectiveness demands and safety requirements creates formulation challenges that limit product optimization opportunities.

Limited Rural Market Penetration

Despite representing significant population segments, rural areas across MEA countries exhibit limited awareness and accessibility to modern household insecticides. Infrastructure deficiencies, including inadequate retail distribution networks and limited internet connectivity, restrict market reach.

Economic constraints and traditional pest control practices maintain preference for conventional methods over commercial products. The digital divide hampers educational initiatives and product awareness campaigns, perpetuating underutilization of effective pest control solutions in areas with high vector-borne disease prevalence.

Opportunities - Sustainable Product Development Focus

The global shift toward environmental sustainability presents significant opportunities for bio-based and eco-friendly insecticide formulations. Consumer preference evolution toward natural ingredients creates market space for plant-derived active compounds and biodegradable packaging solutions.

Regulatory support for environmentally responsible products, combined with corporate sustainability commitments, incentivizes research and development investments in green chemistry. This trend alignment offers manufacturers differentiation opportunities and premium pricing potential while addressing environmental concerns.

Digital Commerce Expansion and Direct-to-Consumer Channels

E-commerce platform proliferation across MEA markets has democratized product access, enabling direct consumer engagement and personalized marketing approaches. Mobile commerce growth and improved logistics networks facilitate market penetration in previously underserved regions.

Digital platforms provide cost-effective channels for consumer education and brand building, particularly important for new product launches and category expansion. The direct-to-consumer model enables better margin control and customer relationship management while reducing dependency on traditional retail channels.

Category-wise Insights

Product Type Analysis

Liquid insecticides dominate with a 37.3% share in 2025, driven by superior versatility and immediate action capabilities. These formulations offer precise application control and rapid pest knockdown effects, making them preferred for targeted treatments.

The spray delivery mechanism provides user convenience and effective coverage across diverse household environments. Liquid products demonstrate extended shelf life and formulation stability, supporting distribution efficiency across the region's challenging climate conditions.

Roll-on applications represent the fastest-growing segment, benefiting from increased outdoor activities and personal protection awareness. This format provides controlled, mess-free application suitable for skin contact applications and targeted surface treatments.

The convenience factor appeals to urban consumers seeking portable and discreet pest protection solutions. Innovation in roll-on formulations includes extended-release technologies and fragrance integration, expanding application scenarios beyond traditional pest control.

Sales Channel Analysis

Store-based retailing commands a 30.5% share in 2025, reflecting consumer preference for physical product inspection and immediate availability. Traditional retail outlets provide trusted purchasing environments where consumers can seek product advice and compare options.

Inventory accessibility and established consumer shopping patterns support consistent sales volumes through conventional channels. Promotional campaigns and seasonal merchandising opportunities enhance product visibility and impulse purchasing behavior.

Supermarkets represent the fastest-growing sales channel, benefiting from one-stop shopping convenience and integrated promotional strategies. These venues offer extensive product assortments and competitive pricing through bulk procurement advantages.

Strategic shelf placement and cross-merchandising with related household products enhance product exposure and purchase consideration. Supermarket expansion across MEA urban centers provides broader market access and consumer touch points.

Application Analysis

Mosquito-targeted applications account for a 30.6% share, driven by vector-borne disease prevention imperatives and seasonal usage patterns. The segment benefits from continuous health authority recommendations and public awareness campaigns highlighting disease transmission risks.

Product innovation focuses on long-lasting protection and pleasant user experiences to encourage consistent application. Government procurement for public health initiatives provides stable demand foundations beyond consumer purchases.

Ant control applications demonstrate the fastest growth rate, reflecting urbanization-related infestations and improved product availability. Modern urban environments create favorable conditions for ant colonies, necessitating effective control solutions.

Innovative gel baits and targeted formulations offer superior efficacy compared to traditional methods, driving category adoption. Consumer education regarding ant behavior and control strategies enhances product utilization and repeat purchases.

Nature Analysis

Synthetic formulations maintain 73.8% share through proven effectiveness and cost-competitive positioning. These products offer broad-spectrum pest control and extended residual activity, meeting diverse household protection needs. Manufacturing scale economies enable affordable pricing that supports mass market accessibility. Established regulatory approvals and market familiarity facilitate consumer adoption and repeat purchases.

Natural formulations represent the fastest-growing segment, driven by environmental consciousness and health safety preferences. Plant-based active ingredients and essential oil formulations appeal to families with children and pets.

Premium positioning opportunities exist for natural products, supporting margin improvement while addressing sustainability concerns. Innovation in natural formulation effectiveness addresses historical performance gaps compared to synthetic alternatives.

Regional Market Insights

UAE Household Insecticides Market Analysis

The UAE household insecticides market represents 22.3% of regional share, establishing itself as the second-largest market with revenues exceeding US$ 200 million in 2022. The country's strategic position as a global tourism destination creates heightened pest control requirements across hospitality establishments, directly driving market demand.

Rapid urbanization and modern infrastructure development have elevated living standards, resulting in increased consumer expectations for pest-free environments. The UAE's desert climate, characterized by extreme heat and seasonal humidity, provides ideal conditions for mosquitoes, flies, and cockroaches, necessitating continuous protection measures.

The regulatory framework emphasizes public health protection through stringent import standards and safety requirements, ensuring only registered products from original manufacturers enter the market. This regulatory approach maintains product quality standards while protecting consumer safety.

The country's affluent population demonstrates willingness to invest in premium and technologically advanced pest control solutions, supporting market premiumization trends. International events such as Expo 2020 Dubai have amplified pest management requirements, creating sustained demand for professional-grade household insecticides across residential and commercial applications.

Egypt Market Analysis

Egypt emerges as the fastest-growing market within the MEA region, driven by unique climatic conditions and demographic factors. The country's proximity to the Nile River creates extensive breeding grounds for mosquitoes and other vectors, generating consistent demand for household protection solutions.

Hot summers and high humidity levels during specific seasons intensify pest activity, requiring year-round vigilance from households and businesses. Dense urban centers including Cairo and Alexandria experience elevated pest pressure due to population concentration and sanitation challenges.

The Egyptian government's focus on public health improvement through vector control initiatives provides regulatory support for household insecticide adoption. National awareness campaigns highlighting dengue and malaria prevention encourage consumer education and product utilization.

Economic development and rising middle-class purchasing power enable increased spending on household health and hygiene products. The country's large population base and improving retail infrastructure create substantial market opportunity for both domestic and international manufacturers seeking regional expansion.

Competitive Landscape

The MEA household insecticides market exhibits moderate consolidation with leading players holding significant market shares through established distribution networks and brand recognition. Global manufacturers including FMC Corporation, SC Johnson & Son, BASF SE, and Bayer AG maintain strong positions through comprehensive product portfolios and regional manufacturing capabilities.

Local and regional players compete effectively in specific market segments through cost advantages and cultural market understanding. Market concentration analysis reveals opportunities for strategic acquisitions and partnerships to enhance geographic coverage and product diversification.

Recent Industry Developments:

- In August 2024, Flora-scent Organics introduced innovative mosquito-repellent incense sticks that are citronella-free and claimed to be five times more effective than traditional options. A special combination of plant oils, such as peppermint, rosemary, cedarwood, and geraniol from geranium oil, are used to make these environmentally friendly sticks.

- In April 2023, SC Johnson has partnered with the Tanzanian government to eradicate malaria with a US$ 1.5 million investments in malaria diagnosis, treatment, and prevention in Tanzania's highest malaria transmission areas. The multinational company based in the United States expressed its official commitment, together with new Public Private Partnerships, to combat malaria.

Companies Covered in MEA Household Insecticides Market

- AVIMA

- ASTRACHEM

- Reckitt Benckiser Group plc

- Godrej Consumer Products Limited

- Spectrum Brands Holdings, Inc

- Kombat

- BASF SE

- Henkel AG & Co. KGaA,

- FMC Corporation

- Bayer AG

- Pelgar International Limited

- Neogen Corporation

- S. C. Johnson & Son Inc,

- Sumitomo Chemical Co., Ltd

- Corteva, Inc,

- Nufarm Limited

- Other Market Players

Frequently Asked Questions

The MEA Household Insecticides market is estimated to be valued at US$ 1.2 Bn in 2025.

The key demand driver for the Middle East and Africa (MEA) Household Insecticides Market is the rising prevalence of vector-borne diseases, such as malaria, dengue, and chikungunya, coupled with increasing awareness of household hygiene and pest prevention.

In 2025, the UAE region will dominate the market with an exceeding 25% revenue share in the global MEA Household Insecticides market.

Among the Product Type, Liquid Equipment holds the highest preference, capturing beyond 37.3% of the market revenue share in 2025, surpassing other parts.

The key players in the MEA Household Insecticides market are AVIMA, ASTRACHEM, Reckitt Benckiser Group plc, Godrej Consumer Products Limited and Spectrum Brands Holdings, Inc.