- Executive Summary

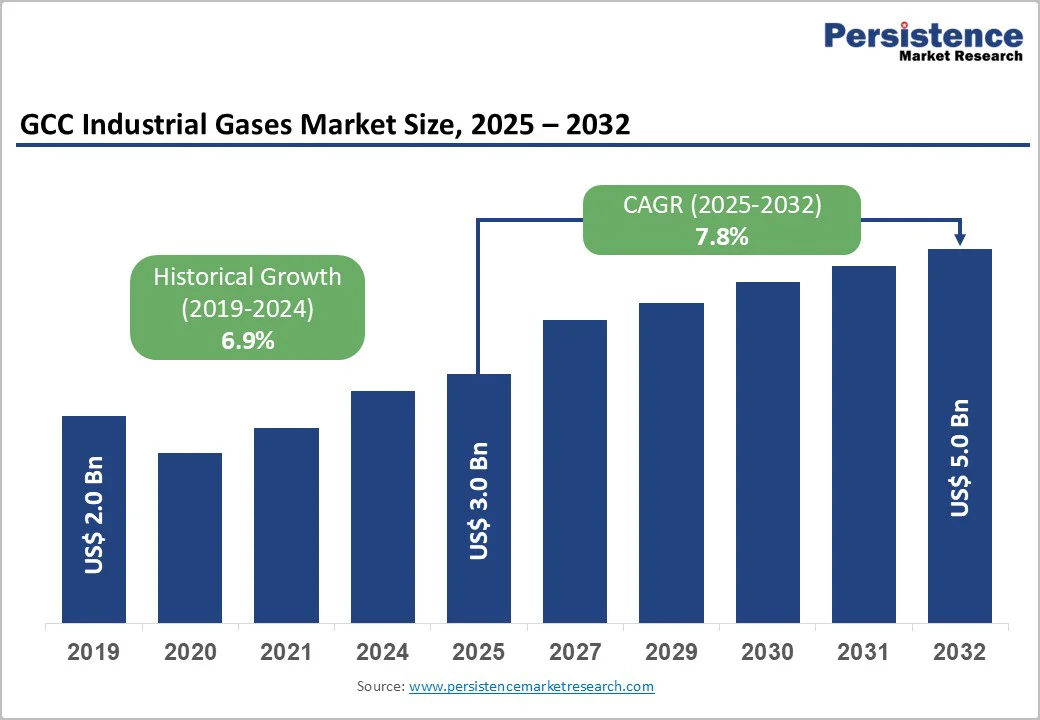

- GCC Industrial Gases Market Snapshot 2024 and 2032

- Market Opportunity Assessment, 2024 -2032, US$ Mn

- Key Market Trends

- Industry Developments and Key Market Events

- Demand Side and Supply Side Analysis

- PMR Analysis and Recommendations

- Market Overview

- Market Scope and Definitions

- Value Chain Analysis

- Macro-Economic Factors

- GCC GDP Outlook

- Industrial Gas Consumption by End-Use Sector

- Energy Transition & Hydrogen Economy

- Industrial Output & Manufacturing Index

- Forecast Factors – Relevance and Impact

- COVID-19 Impact Assessment

- PESTLE Analysis

- Porter's Five Forces Analysis

- Geopolitical Tensions: Market Impact

- Regulatory and Technology Landscape

- Market Dynamics

- Drivers

- Restraints

- Opportunities

- Trends

- Price Trend Analysis, 2019 – 2032

- Country-wise Price Analysis

- Price by Segments

- Price Impact Factors

- GCC Industrial Gases Market Outlook:

- Key Highlights

- GCC Industrial Gases Market Outlook: Gas Type

- Introduction/Key Findings

- Historical Market Size (US$ Mn) and Volume (Tons) Analysis by Gas Type, 2019-2023

- Current Market Size (US$ Mn) and Volume (Tons) Analysis and Forecast, by Gas Type, 2024-2032

- Oxygen

- Nitrogen

- Helium

- Acetylene

- Argon

- Hydrogen

- Carbon Dioxide

- Methane

- Florine Gases

- Others

- Market Attractiveness Analysis: Gas Type

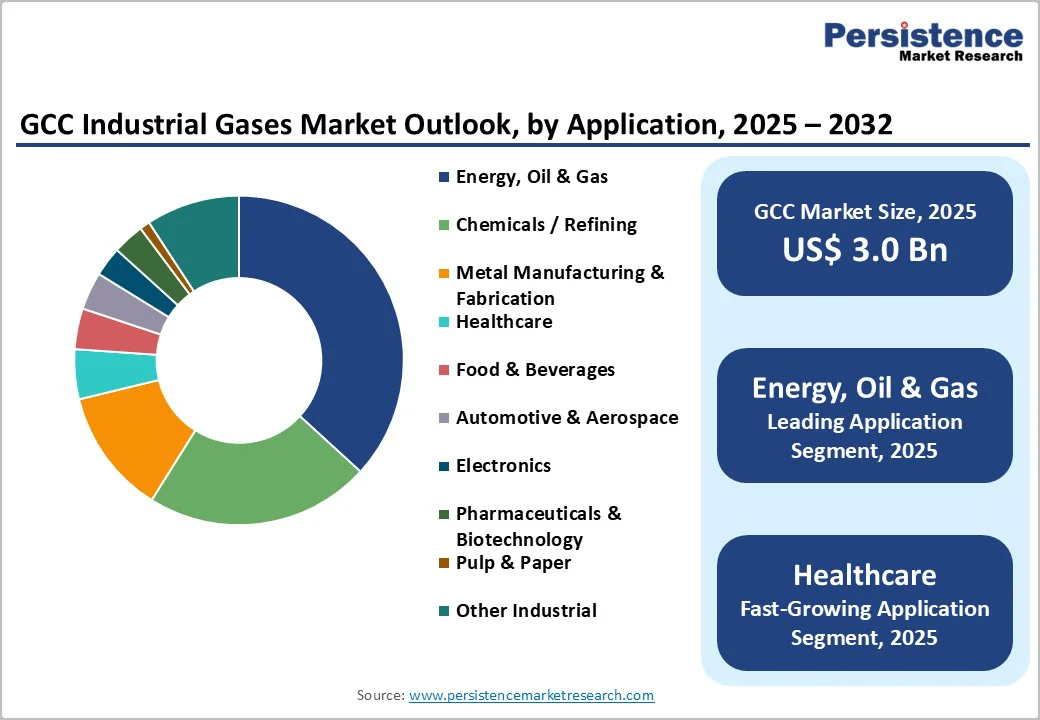

- GCC Industrial Gases Market Outlook: Application

- Introduction/Key Findings

- Historical Market Size (US$ Mn) and Volume (Tons) Analysis by Application, 2019-2023

- Current Market Size (US$ Mn) and Volume (Tons) Analysis and Forecast, by Application, 2024-2032

- Metal Manufacturing and Fabrication

- Healthcare

- Automotive & Aerospace

- Electronics

- Energy, Oil & Gas

- Food & Beverages

- Pulp & Paper

- Chemicals

- Pharmaceuticals & Biotechnology

- Other Industrial Application

- Market Attractiveness Analysis: Application

- GCC Industrial Gases Market Outlook: Supply Mode

- Introduction/Key Findings

- Historical Market Size (US$ Mn) and Volume (Tons) Analysis by Supply Mode, 2019-2023

- Current Market Size (US$ Mn) and Volume (Tons) Analysis and Forecast, by Supply Mode, 2024-2032

- Pipeline

- Bulk Gas Delivery

- Cryogenic Tanks & Liquid Dewars

- Market Attractiveness Analysis: Supply Mode

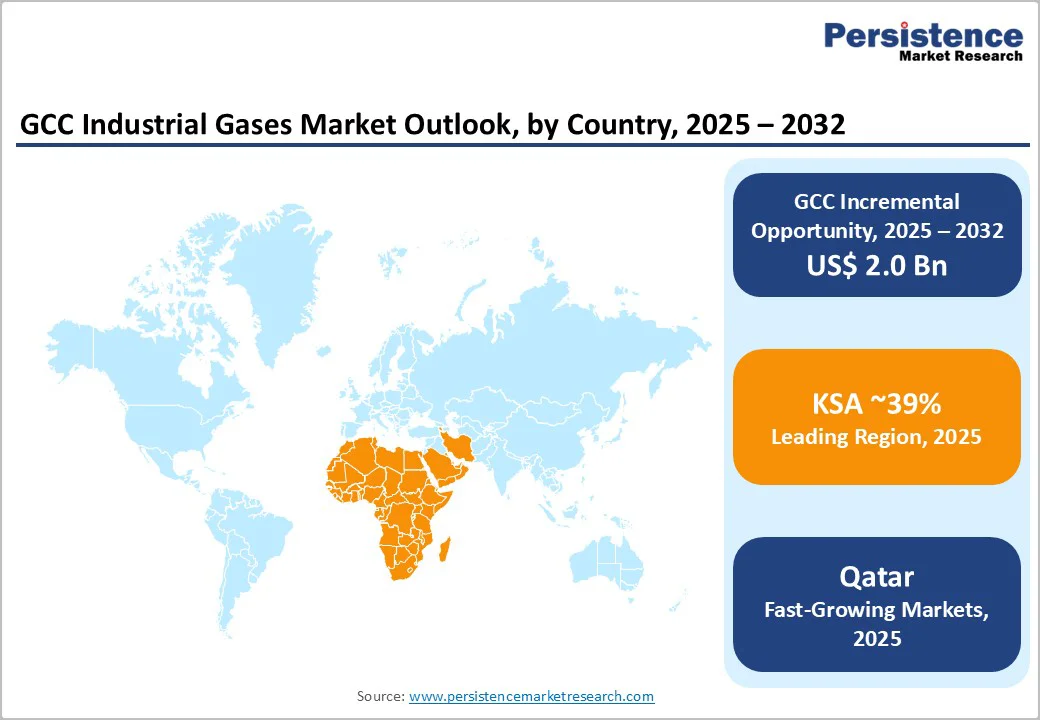

- GCC Industrial Gases Market Outlook: Country

- Key Highlights

- Historical Market Size (US$ Mn) and Volume (Tons) Analysis by Country, 2019-2023

- Current Market Size (US$ Mn) and Volume (Tons) Analysis and Forecast, by Country, 2024-2032

- Kingdom of Saudi Arabia (KSA)

- United Arab Emirates (UAE)

- Qatar

- Kuwait

- Oman

- Bahrain

- Market Attractiveness Analysis: Country

- Kingdom of Saudi Arabia (KSA) Industrial Gases Market Outlook:

- Key Highlights

- Pricing Analysis

- Kingdom of Saudi Arabia (KSA) Market Size (US$ Mn) and Volume (Tons) Analysis and Forecast, by Gas Type, 2024-2032

- Oxygen

- Nitrogen

- Helium

- Acetylene

- Argon

- Hydrogen

- Carbon Dioxide

- Methane

- Florine Gases

- Others

- Kingdom of Saudi Arabia (KSA) Market Size (US$ Mn) and Volume (Tons) Analysis and Forecast, by Application, 2024-2032

- Metal Manufacturing and Fabrication

- Healthcare

- Automotive & Aerospace

- Electronics

- Energy, Oil & Gas

- Food & Beverages

- Pulp & Paper

- Chemicals

- Pharmaceuticals & Biotechnology

- Other Industrial Application

- Kingdom of Saudi Arabia (KSA) Market Size (US$ Mn) and Volume (Tons) Analysis and Forecast, by Supply Mode, 2024-2032

- Pipeline

- Bulk Gas Delivery

- Cryogenic Tanks & Liquid Dewars

- United Arab Emirates (UAE) Industrial Gases Market Outlook:

- Key Highlights

- Pricing Analysis

- United Arab Emirates (UAE) Market Size (US$ Mn) and Volume (Tons) Analysis and Forecast, by Gas Type, 2024-2032

- Oxygen

- Nitrogen

- Helium

- Acetylene

- Argon

- Hydrogen

- Carbon Dioxide

- Methane

- Florine Gases

- Others

- United Arab Emirates (UAE) Market Size (US$ Mn) and Volume (Tons) Analysis and Forecast, by Application, 2024-2032

- Metal Manufacturing and Fabrication

- Healthcare

- Automotive & Aerospace

- Electronics

- Energy, Oil & Gas

- Food & Beverages

- Pulp & Paper

- Chemicals

- Pharmaceuticals & Biotechnology

- Other Industrial Application

- United Arab Emirates (UAE) Market Size (US$ Mn) and Volume (Tons) Analysis and Forecast, by Supply Mode, 2024-2032

- Pipeline

- Bulk Gas Delivery

- Cryogenic Tanks & Liquid Dewars

- Qatar Industrial Gases Market Outlook:

- Key Highlights

- Pricing Analysis

- Qatar Market Size (US$ Mn) and Volume (Tons) Analysis and Forecast, by Gas Type, 2024-2032

- Oxygen

- Nitrogen

- Helium

- Acetylene

- Argon

- Hydrogen

- Carbon Dioxide

- Methane

- Florine Gases

- Others

- Qatar Market Size (US$ Mn) and Volume (Tons) Analysis and Forecast, by Application, 2024-2032

- Metal Manufacturing and Fabrication

- Healthcare

- Automotive & Aerospace

- Electronics

- Energy, Oil & Gas

- Food & Beverages

- Pulp & Paper

- Chemicals

- Pharmaceuticals & Biotechnology

- Other Industrial Application

- Qatar Market Size (US$ Mn) and Volume (Tons) Analysis and Forecast, by Supply Mode, 2024-2032

- Pipeline

- Bulk Gas Delivery

- Cryogenic Tanks & Liquid Dewars

- Kuwait Industrial Gases Market Outlook:

- Key Highlights

- Pricing Analysis

- Kuwait Market Size (US$ Mn) and Volume (Tons) Analysis and Forecast, by Gas Type, 2024-2032

- Oxygen

- Nitrogen

- Helium

- Acetylene

- Argon

- Hydrogen

- Carbon Dioxide

- Methane

- Florine Gases

- Others

- Kuwait Market Size (US$ Mn) and Volume (Tons) Analysis and Forecast, by Application, 2024-2032

- Metal Manufacturing and Fabrication

- Healthcare

- Automotive & Aerospace

- Electronics

- Energy, Oil & Gas

- Food & Beverages

- Pulp & Paper

- Chemicals

- Pharmaceuticals & Biotechnology

- Other Industrial Application

- Kuwait Market Size (US$ Mn) and Volume (Tons) Analysis and Forecast, by Supply Mode, 2024-2032

- Pipeline

- Bulk Gas Delivery

- Cryogenic Tanks & Liquid Dewars

- Oman Industrial Gases Market Outlook:

- Key Highlights

- Pricing Analysis

- Oman Market Size (US$ Mn) and Volume (Tons) Analysis and Forecast, by Gas Type, 2024-2032

- Oxygen

- Nitrogen

- Helium

- Acetylene

- Argon

- Hydrogen

- Carbon Dioxide

- Methane

- Florine Gases

- Others

- Oman Market Size (US$ Mn) and Volume (Tons) Analysis and Forecast, by Application, 2024-2032

- Metal Manufacturing and Fabrication

- Healthcare

- Automotive & Aerospace

- Electronics

- Energy, Oil & Gas

- Food & Beverages

- Pulp & Paper

- Chemicals

- Pharmaceuticals & Biotechnology

- Other Industrial Application

- Oman Market Size (US$ Mn) and Volume (Tons) Analysis and Forecast, by Supply Mode, 2024-2032

- Pipeline

- Bulk Gas Delivery

- Cryogenic Tanks & Liquid Dewars

- Bahrain Industrial Gases Market Outlook:

- Key Highlights

- Pricing Analysis

- Bahrain Market Size (US$ Mn) and Volume (Tons) Analysis and Forecast, by Gas Type, 2024-2032

- Oxygen

- Nitrogen

- Helium

- Acetylene

- Argon

- Hydrogen

- Carbon Dioxide

- Methane

- Florine Gases

- Others

- Bahrain Market Size (US$ Mn) and Volume (Tons) Analysis and Forecast, by Application, 2024-2032

- Metal Manufacturing and Fabrication

- Healthcare

- Automotive & Aerospace

- Electronics

- Energy, Oil & Gas

- Food & Beverages

- Pulp & Paper

- Chemicals

- Pharmaceuticals & Biotechnology

- Other Industrial Application

- Bahrain Market Size (US$ Mn) and Volume (Tons) Analysis and Forecast, by Supply Mode, 2024-2032

- Pipeline

- Bulk Gas Delivery

- Cryogenic Tanks & Liquid Dewars

- Competition Landscape

- Market Share Analysis, 2024

- Market Structure

- Competition Intensity Mapping

- Competition Dashboard

- Company Profiles

- Linde plc

- Company Overview

- Product Portfolio/Offerings

- Key Financials

- SWOT Analysis

- Company Strategy and Key Developments

- Air Liquide S.A.

- Air Products and Chemicals Inc.

- ADNOC Industrial Gas

- Gulf Cryo Holding CSC

- Messer SE and Co. KGaA

- Praxair Technology Inc.

- Taiyo Nippon Sanso Corporation

- Air Water Inc.

- Iwatani Corporation

- Abdullah Hashim Industrial Gases (AHG)

- Buzwair Industrial Gases

- National Industrial Gas Plants (NIGP)

- Oman Gas Company

- Bahrain National Gas Company

- Linde plc

- Appendix

- Research Methodology

- Research Assumptions

- Acronyms and Abbreviations

Loading page data

Please wait a moment