- Pharmaceuticals

- Middle Ear Infections Treatment Market

Middle Ear Infections Treatment Market Size, Share, and Growth Forecast, 2026-2033

Middle Ear Infections Treatment Market by Cause (Bacterial, Viral, Allergic, Others), Treatment Modality (Surgery, Drugs, Others), Demography (Infants (0-2 yrs), Children (3–12 yrs), Adolescents (13–17 yrs), Adults (18–64 yrs)), and Regional Analysis for 2026-2033

Middle Ear Infections Treatment Market Share and Trends Analysis

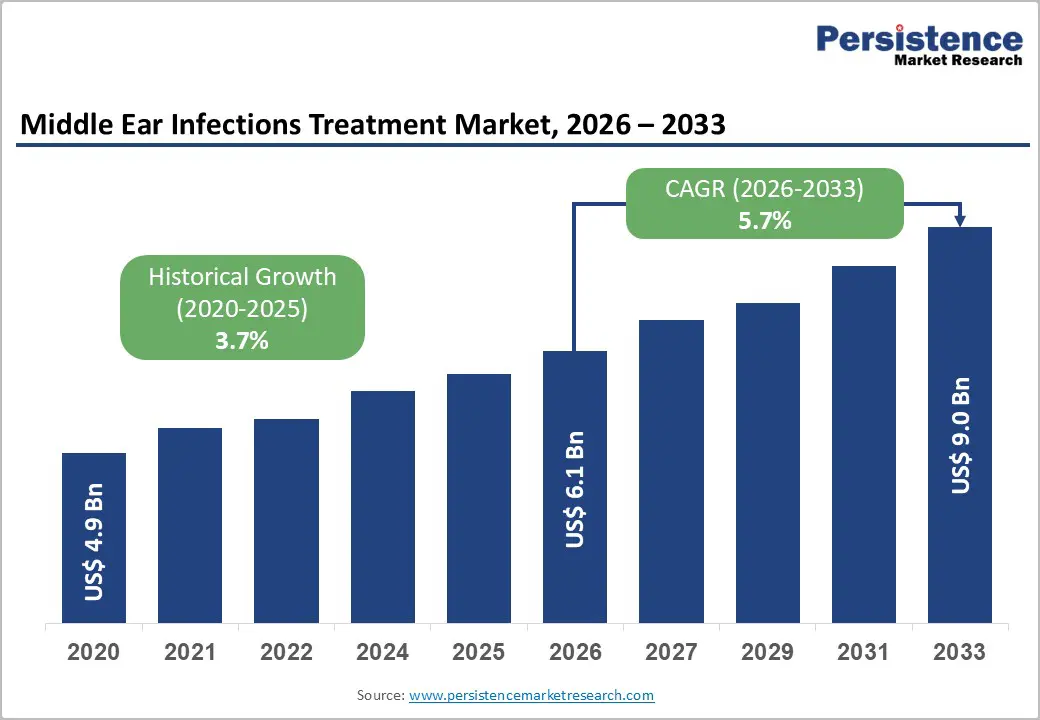

The global middle ear infections treatment market size is likely to be valued at US$ 6.1 billion in 2026, and is projected to reach US$ 9.0 billion by 2033, growing at a CAGR of 5.7% during the forecast period 2026–2033.

Market expansion is primarily driven by the high global prevalence of otitis media, rising pediatric populations in emerging economies, and expanding access to antibiotic therapy and surgical interventions. According to the World Health Organization (WHO), middle ear infections affect over 700 million people annually, with children accounting for more than half of reported cases, making it one of the most common childhood infectious diseases worldwide. Rapid urbanization, increased exposure to respiratory infections, and higher daycare enrollment rates further elevate disease incidence. In parallel, strengthening primary healthcare infrastructure, wider availability of ear-nose-throat (ENT) specialists, and the adoption of updated clinical treatment guidelines issued by global and national health authorities are improving early diagnosis and treatment adherence. These combined factors are accelerating the uptake of standardized middle ear infection treatment solutions across countries, supporting sustained long-term market growth.

Key Industry Highlights

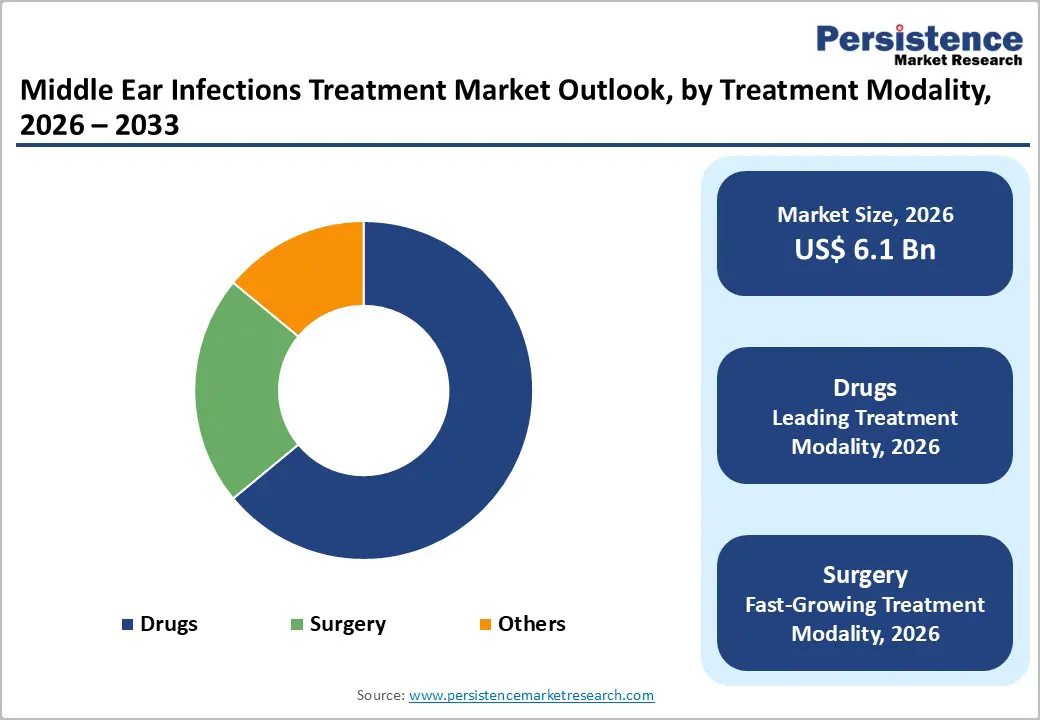

- Dominant Treatment Modality: Drug-based therapies are expected to account for around 64% of global revenue in 2026, while surgical interventions are projected to grow the fastest at about 6.8% CAGR through 2033, driven by rising recurrent otitis media cases.

- Leading Cause: Bacterial infections are expected to dominate with an estimated 62% share in 2026, while viral-origin otitis media is projected to be the fastest-growing through 2033, owing to improved diagnostic differentiation.

- Leading Patient Demographics: Children are projected to represent approximately 57% of the patient base in 2026, while adults are expected to register the fastest 2026-2033 growth due to increasing chronic ENT conditions.

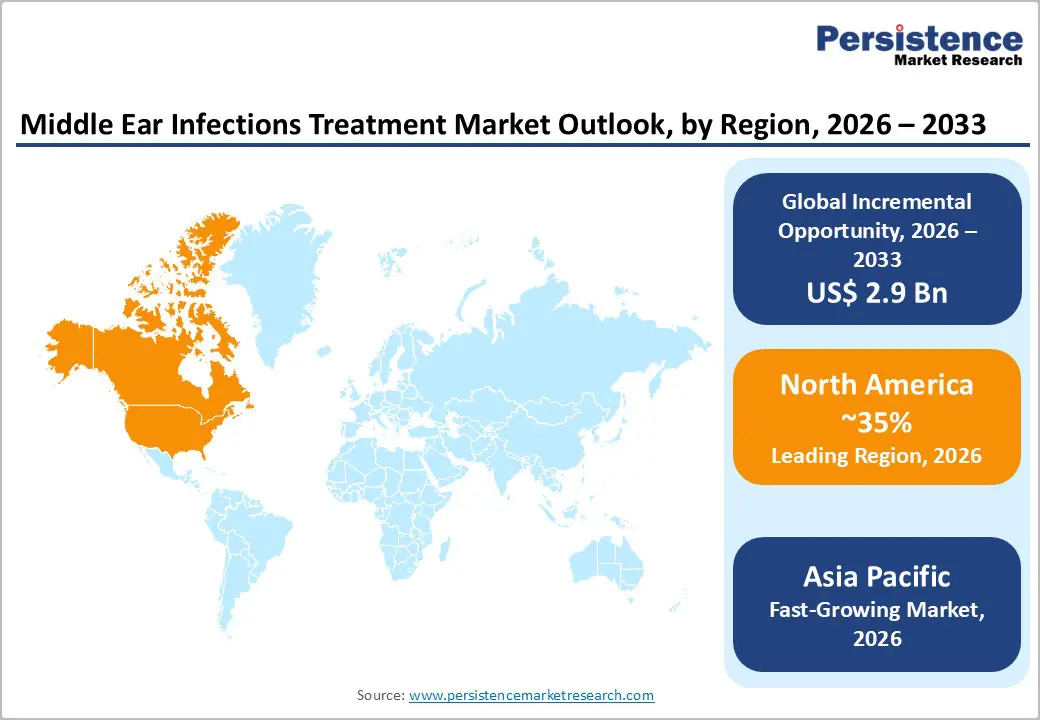

- Regional Leadership: North America is expected to lead with an estimated 35% share in 2026, while the Asia Pacific market is set to record the fastest growth at around 6.4% CAGR from 2026 to 2033, driven by widening access to primary healthcare.

- Competitive Dynamics: Competitive intensity is being increasingly shaped by innovation-led strategies, with pediatric drug launches and ENT portfolio expansions reinforcing differentiation and long-term market positioning.

| Key Insights | Details |

|---|---|

| Middle Ear Infections Treatment Market Size (2026E) | US$ 6.1 Bn |

| Market Value Forecast (2033F) | US$ 9.0 Bn |

| Projected Growth (CAGR 2026 to 2033) | 5.7% |

| Historical Market Growth (CAGR 2020 to 2025) | 3.7% |

Market Factors – Growth, Barriers, and Opportunity Analysis

High Clinical Prevalence Supported by Structured Treatment Adoption

The WHO estimates indicate that nearly 60% of children under five years of age experience at least one episode of middle ear infection annually, with recurrent infections reported in over 30% of pediatric cases, positioning otitis media among the most prevalent pediatric infectious diseases globally. In the United States, the Centers for Disease Control and Prevention (CDC) identifies otitis media as one of the leading causes of antibiotic prescriptions in children, underscoring the scale and consistency of therapeutic demand across primary and specialist care settings. This high diagnosis rate ensures continuous patient inflow across outpatient clinics, pediatric practices, and hospital-based ENT departments.

This clinical burden is increasingly reinforced by standardized treatment adoption, supported by public health actions in past years. During this period, the CDC expanded national antimicrobial stewardship programs, strengthening guidance on appropriate antibiotic use in pediatric infections, including otitis media. These initiatives aim to optimize prescribing accuracy rather than reduce access, thereby sustaining demand for drug-based therapies while improving clinical outcomes. As a result, healthcare providers benefit from clearer decision-making frameworks, reinforcing predictable utilization patterns across treatment modalities.

Demographic Expansion and Evidence-Based Clinical Guideline Evolution

The United Nations Population Division projects that children under 14 will account for over 25% of Asia Pacific’s population by 2030, significantly expanding the addressable patient pool in one of the world’s fastest-growing healthcare regions. Rising birth rates, increased exposure to respiratory infections in urban environments, and improving caregiver awareness are accelerating early diagnosis and treatment-seeking behavior, particularly across emerging economies where pediatric healthcare access is expanding. This demographic momentum structurally supports sustained growth in pediatric ENT service utilization.

In parallel, continuous improvements in evidence-based treatment guidelines issued by organizations such as the American Academy of Pediatrics (AAP) and the National Institute for Health and Care Excellence (NICE) have optimized therapeutic outcomes. In 2025, updated clinical guidance reinforced targeted antibiotic use, balancing resistance reduction with maintained clinical efficacy, while clarifying escalation pathways for procedural intervention. The refinements in surgical indications for tympanostomy tube placement, supported by otolaryngology consensus updates, have improved patient selection and procedural outcomes. These clinical advancements are strengthening physician confidence and accelerating adoption of standardized otitis media treatment solutions across both developed and emerging markets.

Antibiotic Resistance and Escalating Regulatory Oversight

The rising antimicrobial resistance presents a structural challenge for the middle ear infection treatment market, particularly for drug-based therapies that remain the primary line of care. WHO data shows that resistance to first-line antibiotics for respiratory and ear infections has exceeded 20% in several countries, undermining long-term treatment effectiveness. In October 2025, the WHO warned that antimicrobial resistance is accelerating globally, noting that one in six infections is now resistant to standard antibiotics, contributing to substantial mortality worldwide. This growing resistance burden complicates treatment decisions and increases reliance on monitoring and follow-up care.

Regulatory and stewardship initiatives intensified, reinforcing constraints on antibiotic use across healthcare systems. In November 2025, the North Carolina Department of Health and Human Services declared Antibiotic Awareness Week, highlighting the importance of correct prescribing to slow resistance development. In parallel, the U.S. Centers for Disease Control and Prevention expanded its Antimicrobial Resistance Solutions Initiative in early 2026, investing in detection, surveillance, and prevention programs nationwide. While these actions strengthen public health outcomes, they also limit prescription volumes, tighten regulatory scrutiny, and increase development and compliance costs, slowing growth within antibiotic-based treatment segments.

High Surgical Costs and Structural Access Limitations in Emerging Economies

Although surgical interventions such as tympanostomy tube insertion are clinically effective for recurrent and chronic middle ear infections, cost remains a significant barrier in low- and middle-income regions. According to OECD health expenditure data, ENT surgical procedures cost three to five times the average monthly household income in many developing economies. This affordability gap delays timely intervention and sustains prolonged dependence on pharmacological therapies. As a result, disease recurrence and complication risks remain elevated in underserved populations.

Policy efforts sought to expand pediatric surgical capacity through public healthcare funding and hospital infrastructure upgrades in select markets. However, implementation remains uneven, with persistent shortages of trained ENT specialists and limited operating capacity outside major cities. Insurance coverage gaps and long surgical waiting times further restrict access, despite rising clinical need. These structural challenges continue to suppress procedural adoption rates, constraining market expansion in regions with high disease prevalence but limited healthcare resources.

Expansion of Pediatric Healthcare Programs and Outpatient Procedural Adoption

Government-led pediatric healthcare initiatives continue to create scalable growth opportunities for the middle ear infections treatment market, particularly by strengthening early diagnosis and standardized treatment pathways. UNICEF- and WHO-supported child health programs increasingly integrate routine ear screening and infection management into primary healthcare delivery. School-based screening initiatives across India, Indonesia, and Vietnam are expanding access to pediatric ENT care, translating into consistent demand for antibiotics, analgesics, and follow-up services. These programs support predictable, volume-driven treatment demand within public healthcare systems.

Regulatory and reimbursement developments are further lowering procedural barriers for recurrent otitis media management. In the U.S., the introduction of new CMS reimbursement pathways for in-office tympanostomy tube placement has accelerated adoption of minimally invasive procedures performed without general anesthesia. This shift expands access to surgical treatment in outpatient settings, reduces procedural costs, and improves parental acceptance. As similar outpatient care models gain traction globally, procedural intervention is expected to contribute meaningfully to market expansion, particularly in pediatric populations.

Innovation in Drug Delivery and Next-Generation Therapeutic Approaches

There is growing clinical demand for advanced drug formulations and localized delivery systems that improve efficacy while limiting systemic antibiotic exposure. Sustained-release ear drops and combination steroid-antibiotic therapies are increasingly favored for their ability to address inflammation and infection simultaneously. Ongoing government-funded clinical research is also exploring biofilm-targeting antibiotics, which could significantly reduce recurrence rates and treatment failure. Successful commercialization of these therapies would enable differentiation and support premium pricing within the pharmaceutical segment.

The early-stage regenerative and localized treatment innovations, highlight long-term therapeutic potential. Injectable gels designed to promote tympanic membrane healing and emerging trans-tympanic drug delivery technologies aim to improve outcomes in chronic and recurrent cases. While still in early development, these innovations align with broader healthcare priorities around precision treatment and antimicrobial stewardship. As regulatory validation progresses, such therapies could redefine treatment standards and create new revenue opportunities across both developed and emerging markets.

Category-wise Analysis

Treatment Modality Insights

Drug-based therapies are expected to maintain their leadership position, representing approximately 64% of the middle ear infections treatment market revenue share in 2026. Antibiotics, analgesics, and anti-inflammatory drugs remain the first-line treatment approach under widely adopted clinical protocols. Their accessibility, rapid symptom control, and suitability for outpatient care, particularly in pediatric populations, reinforce sustained utilization. High prescription frequency and repeat treatment cycles further strengthen this segment’s contribution to overall market revenues. As clinical guidelines continue to evolve, drug therapies are likely to remain the foundation of early-stage intervention.

The surgical treatment segment is projected to be the fastest-growing modality, registering a forecast CAGR of around 6.8% from 2026 to 2033. Growth is closely linked to rising diagnosis of recurrent and chronic otitis media cases that show limited response to pharmacological therapy. Evidence from 2025 clinical findings indicating reduced systemic antibiotic use following tympanostomy tube placement has strengthened confidence in procedural effectiveness. Advances in minimally invasive techniques and improved safety outcomes are further supporting adoption. Expanded reimbursement coverage continues to lower financial barriers, particularly in developed healthcare systems.

Demography Insights

Children between the ages of 3 and 12 are expected to remain the largest patient demographic, accounting for an estimated 57% of the middle ear infections treatment market share in 2026. High incidence rates among infants and young children, combined with routine pediatric screening and strong caregiver awareness, sustain consistent utilization of treatment services. Pediatric patients drive demand across both drug-based therapies and procedural interventions. Public health focus on early childhood disease management further reinforces the importance of this segment. As pediatric populations expand in emerging markets, this demographic is expected to remain central to market stability.

Adults (18-64 years) are anticipated to register the fastest growth, expanding at a CAGR of approximately 6.1% during the forecast period. Increasing prevalence of chronic respiratory disorders, smoking-related Eustachian tube dysfunction, and age-related immune changes are contributing to higher adult incidence rates. Updated clinical guidance emphasizing age-specific diagnostic and management strategies has improved detection and referral patterns among adults. Greater awareness of long-term complications is also encouraging earlier treatment seeking. These trends are collectively positioning adult otitis media treatment as a progressively important growth contributor.

Regional Insights

North America Middle Ear Infections Treatment Market Trends

North America is projected to remain the leading regional market for middle ear infection treatments, accounting for an estimated 35% of global revenue in 2026, supported by high diagnosis rates, strong reimbursement frameworks, and advanced clinical practice standards. The United States continues to anchor regional demand due to widespread access to ENT specialists and structured pediatric screening practices across primary care and hospital settings. Consistent guideline adherence and early intervention approaches sustain steady treatment volumes across both acute and recurrent otitis media cases. Improvements in digital diagnostic tools, including enhanced digital otoscopy and AI-assisted imaging, are beginning to influence clinical decision-making and referral accuracy. High treatment uptake reflects strong integration of clinical care pathways, insurance coverage, and patient awareness of ear health conditions.

Public health awareness initiatives further reinforce regional momentum. In March 2026, the World Hearing Day 2026 campaign emphasized “From communities to classrooms: hearing care for all children,” encouraging early identification and management of childhood ear and hearing disorders through school and community-based programs. This initiative aligns closely with pediatric otitis media prevention and treatment goals, supporting routine screening adoption and follow-up care. The campaign’s focus on early diagnosis and continuity of care is expected to indirectly strengthen demand for both pharmaceutical therapies and procedural interventions across North America.

Europe Middle Ear Infections Treatment Market Trends

Europe represents a mature yet resilient market for middle ear infection treatments, with Germany, the U.K., France, and Spain acting as the principal demand centers. Harmonized regulatory oversight through the European Medicines Agency (EMA) ensures consistent treatment standards and broad availability of approved drug and surgical options across member states. Public healthcare systems support equitable access to otitis media treatment, particularly within pediatric and elderly populations. Rising awareness of chronic otitis media complications and hearing-related quality-of-life outcomes sustains baseline demand across both outpatient and hospital care settings. While growth remains moderate, utilization remains stable due to entrenched clinical protocols and strong primary care referral systems.

In November 2025, European Antibiotic Awareness Day (EAAD) was observed across more than 40 countries, reinforcing region-wide focus on responsible antibiotic prescribing and antimicrobial stewardship. The campaign emphasized correct diagnosis, targeted antibiotic use, and patient education, all of which are highly relevant to bacterial otitis media management. By promoting prudent use rather than volume-driven prescribing, EAAD supports long-term clinical sustainability while shaping treatment pathways. These efforts contribute to a more structured and regulated treatment environment, influencing prescribing behavior and therapy selection across Europe.

Asia Pacific Middle Ear Infections Treatment Market Trends

Asia Pacific is expected to be the fastest-growing regional market, expanding at an estimated 6.4% CAGR from 2026 to 2033, driven by large pediatric populations, improving healthcare access, and expanding diagnostic coverage. China and India account for the majority of regional patient volume due to population scale and increasing penetration of primary and secondary care services. Japan leads the region in advanced ENT care adoption, supported by high specialist density and technological integration. The government healthcare reforms, combined with investments in hospital infrastructure and medical training, are gradually improving access beyond major metropolitan areas. These structural developments are enhancing early diagnosis rates and treatment continuity across the region.

Awareness-driven initiatives further strengthen regional growth potential. During World Antimicrobial Resistance Awareness Week (WAAW) 2025, held from 18–24 November, multiple Asia Pacific countries conducted educational programs focused on responsible antibiotic use and infection management. These initiatives highlighted the importance of accurate diagnosis and appropriate therapy selection, particularly in high-prevalence pediatric conditions such as otitis media. The emphasis on stewardship and surveillance supports more rational treatment adoption while reinforcing demand for effective, guideline-aligned therapies. Over time, such efforts are expected to improve clinical outcomes and support sustainable market expansion across Asia Pacific.

Competitive Landscape

The global middle ear infections treatment market structure is moderately consolidated, with leading pharmaceutical and medical device companies such as Pfizer, GlaxoSmithKline, Johnson & Johnson, Sanofi, and Novartis accounting for a significant share of global revenue. These players benefit from strong brand recognition, established antibiotic portfolios, and long-standing relationships with hospitals, pediatricians, and ENT specialists. Their competitive strength is reinforced by continuous investments in clinical trials, lifecycle management of existing drugs, and adherence to evolving regulatory standards governing antimicrobial use and pediatric safety.

Alongside global leaders, regional pharmaceutical manufacturers and specialized ENT device companies play an important role in serving local markets, particularly in Asia Pacific and Latin America. Entry barriers remain relatively high due to stringent regulatory approvals, antimicrobial stewardship requirements, and the need for extensive clinical evidence. However, innovation in drug delivery systems and minimally invasive surgical technologies is creating opportunities for smaller innovators to collaborate through licensing agreements and co-development partnerships. Over the forecast period, competitive intensity is expected to increase gradually, driven by portfolio diversification, geographic expansion into emerging markets, and selective acquisitions aimed at strengthening pediatric and chronic otitis media treatment capabilities.

Key Industry Developments

- In January 2026, GSK announced a definitive agreement to acquire RAPT Therapeutics for approximately US$ 2.2 billion, strengthening its immunology and inflammation pipeline. The acquisition centers on ozureprubart, a long-acting anti-IgE antibody in Phase IIb development, underscoring GSK’s strategic focus on high-unmet-need immune-mediated conditions with potential relevance to ENT-linked inflammatory pathways.

- In October 2025, AcuityMD revealed that Preceptis Medical selected its AI platform to support the expanded market launch of the Hummingbird® Tympanostomy Tube System. The collaboration aims to accelerate adoption of in-office pediatric ear tube procedures by improving physician targeting, sales strategy, and awareness through the Hummingbird Catalyst program.

- In June 2025, Elevate ENT Partners acquired Camellia ENT, expanding its clinical footprint in Louisiana and strengthening its Southeastern U.S. presence. Backed by Audax Private Equity, the deal enhances operational scale through centralized analytics and payer management while allowing Camellia ENT physicians to retain clinical independence.

Companies Covered in Middle Ear Infections Treatment Market

- Pfizer Inc.

- Johnson & Johnson

- GlaxoSmithKline plc

- Novartis AG

- Sanofi S.A.

- Merck & Co., Inc.

- Bayer AG

- AbbVie Inc.

- AstraZeneca plc

- Teva Pharmaceutical Industries

- Cipla Ltd.

- Sun Pharmaceutical Industries

Frequently Asked Questions

The global middle ear infections treatment market is projected to reach US$ 6.1 billion in 2026.

High otitis media prevalence, pediatric disease burden, and improved access to standardized drug and surgical treatments are driving market growth.

The market is poised to witness a CAGR of 5.7% from 2026 to 2033.

Expanding pediatric healthcare programs, drug innovation, and rising adoption in Asia Pacific offer strong growth opportunities.

Pfizer Inc., GlaxoSmithKline plc, Johnson & Johnson, Novartis AG, and Sanofi are among the key players operating in the market.