- Power Generation, Transmission, & Distribution

- Middle East & Africa Generator Market

Middle East & Africa Generator Market Size, Share, and Growth Forecast, 2026 – 2033

Middle East & Africa Generator Market by Fuel Type (Natural Gas, Diesel), Power Ratings (0–75 kVA, 75–375 kVA, Above 375 kVA), Application (Prime Power, Backup Power, Peak Shaving) for 2026 – 2033

Middle East & Africa Generator Market Size and Trends Analysis

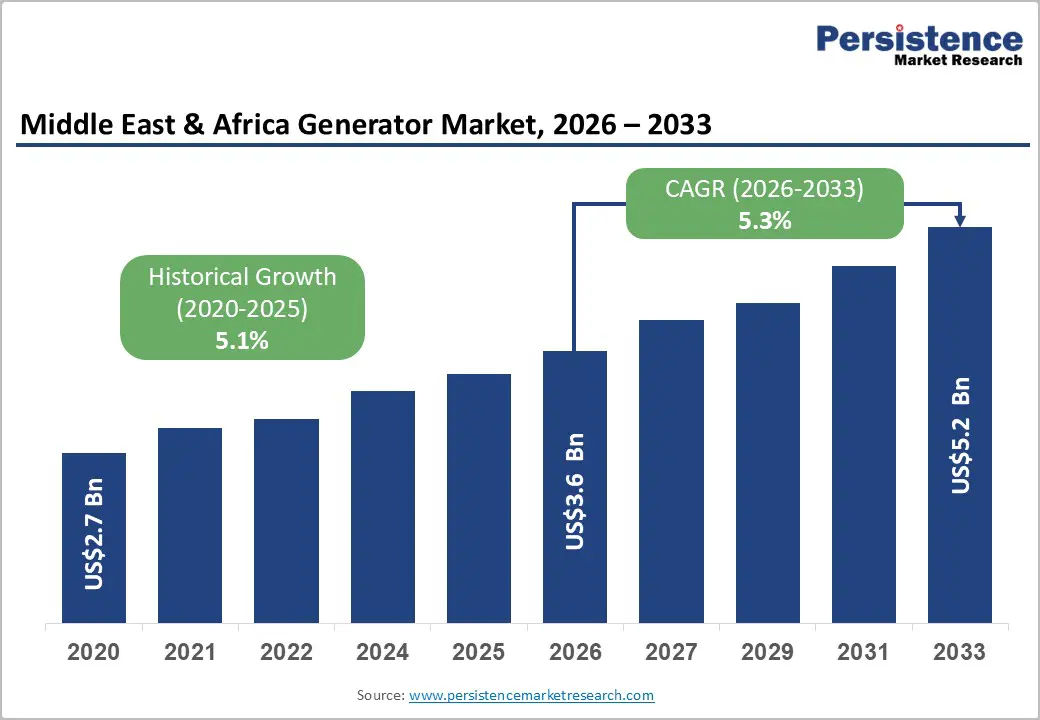

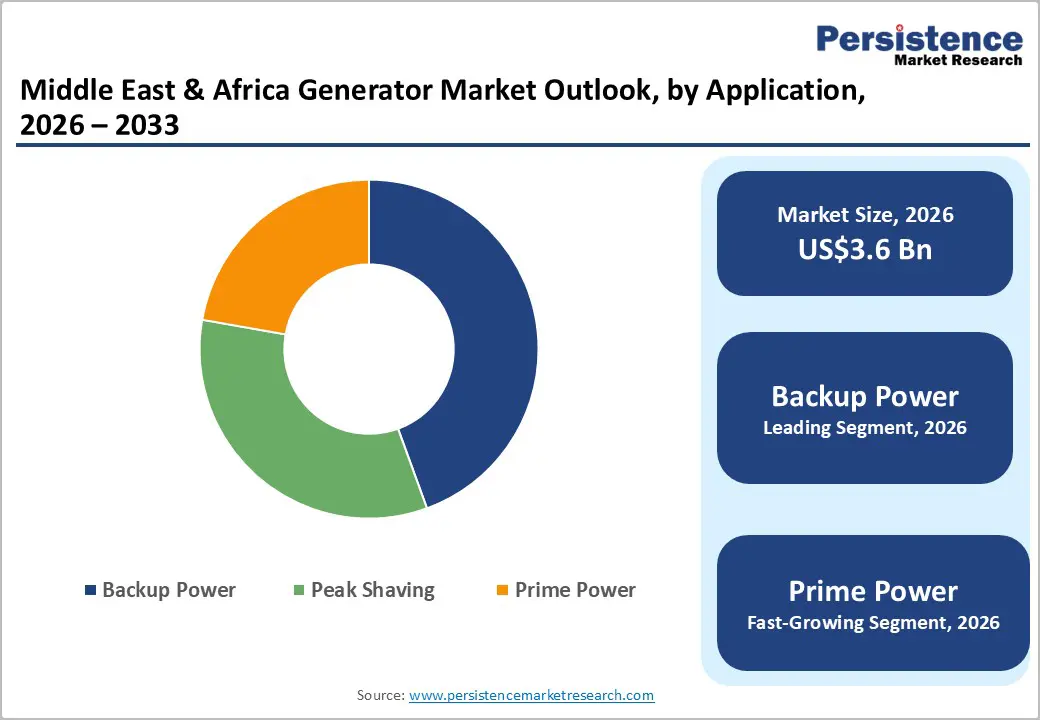

The Middle East & Africa generator market size is likely to be valued at US$3.6 billion in 2026 and is expected to reach US$5.2 billion by 2033, growing at a CAGR of 5.3% during the forecast period from 2026 to 2033, driven by persistent grid unreliability, rising electricity demand in off-grid and remote regions, and large-scale infrastructure and construction investments across both the Middle East and Africa.

Rapid urbanization, population growth, and industrial expansion in African economies, coupled with oil & gas activities, mega infrastructure projects, and smart city developments in GCC countries, continue to strengthen demand for reliable power generation solutions. Diesel generators dominate the market due to their durability, fuel availability, and efficiency under extreme climatic conditions, whereas natural gas generators are gaining traction in gas-rich Middle Eastern countries owing to lower emissions and operating costs.

Key Industry Highlights:

- Leading Fuel Type: Diesel is projected to account for 65% of the market in 2026, driven by its reliability, fuel availability, and suitability for harsh operating conditions across the MEA region.

- Leading Power Ratings: The 75–375 kVA segment is projected to be the leading power rating segment, accounting for over 45% of revenue in 2026, supported by strong demand from commercial buildings, telecom towers, and small- to mid-sized industrial facilities.

- Leading Application: The backup power segment is projected to be the leading application type, accounting for over 55% of revenue in 2026, supported by frequent grid outages and the critical need for uninterrupted power in healthcare, telecommunications, and commercial sectors.

| Global Market Attributes | Key Insights |

|---|---|

| Middle East & Africa Generator Market Size (2026E) | US$3.6 Bn |

| Market Value Forecast (2033F) | US$5.2 Bn |

| Projected Growth (CAGR 2026 to 2033) | 5.3% |

| Historical Market Growth (CAGR 2020 to 2025) | 5.1% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Rising Energy Demand and Infrastructure Development

Many countries across Africa continue to face chronic electricity supply gaps, with grid infrastructure unable to keep pace with the increasing consumption from households, commercial buildings, and emerging manufacturing hubs. Generators remain a critical source of both primary and backup power. In the Middle East, growing energy consumption is closely linked to economic diversification efforts, expansion of oil & gas operations, desalination plants, data centers, and large commercial complexes. Frequent power fluctuations, peak load stress, and extreme climatic conditions reinforce the need for reliable on-site power generation. Diesel generators dominate demand due to their operational robustness and fuel availability, while natural gas generators are gaining adoption in gas-rich economies seeking cost-efficient and cleaner power solutions. This sustained rise in electricity demand directly translates into increased generator installations for residential, commercial, and industrial end users.

Infrastructure development is another major catalyst driving growth in the generator market across the MEA region. Governments are investing heavily in transport networks, smart cities, industrial corridors, hospitals, airports, and large housing projects to support economic growth and social development. During construction, generators provide essential temporary power, and post-completion they serve as critical backup systems to ensure operational continuity. In Africa, large-scale infrastructure programs aimed at improving healthcare, telecommunications, and mining activities rely extensively on generators due to limited grid reach in remote areas. The Middle Eastern mega-projects and industrial expansions require high-capacity generators to manage peak loads and prevent costly downtime. Public–private partnerships and foreign direct investments are accelerating infrastructure rollout, increasing demand for mid- and high-capacity generator sets.

Regulatory and Environmental Compliance Hurdles

Several Middle Eastern countries are gradually aligning with international environmental frameworks to reduce carbon emissions, placing tighter restrictions on diesel-powered generator operations. These regulations increase compliance costs for manufacturers and end users as advanced emission-control technologies, such as exhaust aftertreatment systems and low-sulfur fuel compatibility, become mandatory. Noise pollution regulations in urban and commercial zones limit generator operating hours and require acoustic enclosures, thereby increasing installation and maintenance costs. Inconsistent regulatory frameworks across countries create uncertainty for market participants, complicating cross-border equipment distribution and certification. Smaller enterprises often struggle to meet these evolving standards, delaying procurement decisions and slowing market penetration, particularly for older diesel generator models that do not meet updated environmental norms.

Environmental compliance hurdles are intensified by the growing policy emphasis on renewable energy and decarbonization across the MEA region. Governments are increasingly promoting solar, wind, and hybrid power systems to reduce dependence on fossil-fuel-based generation, thereby indirectly constraining long-term generator demand. Incentives for clean energy adoption, such as subsidies and preferential tariffs, make generators less attractive for continuous use, especially in urban areas. Environmental impact assessments and permitting requirements extend project timelines for large generator installations in industrial and infrastructure projects. For manufacturers, the need to redesign product portfolios toward low-emission and gas-based generators requires substantial investments in research and development, impacting profit margins. These regulatory pressures, combined with rising environmental awareness among end-users.

Expansion into Renewable-Hybrid Generator Systems

Hybrid systems that integrate diesel or gas generators with solar photovoltaic and battery storage are increasingly attractive in regions facing high fuel costs and grid instability. In Africa, where many areas remain off-grid or have weak grid coverage, solar-diesel hybrid generators significantly reduce fuel consumption while ensuring continuous power availability. Middle Eastern countries are adopting hybrid configurations to support sustainability goals without compromising reliability in extreme climatic conditions. These systems lower operational costs, reduce emissions, and extend generator lifecycles, making them appealing for telecom towers, healthcare facilities, commercial complexes, and remote industrial sites. As governments encourage energy diversification and efficiency, hybrid generators align well with policy objectives while preserving the dependable performance required across critical applications.

Growing investments in renewable energy infrastructure enhance the potential of hybrid generator systems across the MEA region. Solar capacity additions, declining battery costs, and advancements in energy management software are enabling seamless integration between generators and renewables. Hybrid systems are particularly suitable for mining, oil & gas camps, and construction projects where uninterrupted power is essential, and grid access is limited. For manufacturers, this transition opens opportunities to offer differentiated, high-value solutions and long-term service contracts, improving margins and customer retention. End users benefit from reduced fuel logistics costs, lower emissions compliance risks, and improved energy resilience.

Category-wise Analysis

Fuel Type Insights

Diesel is expected to lead the Middle East & Africa generator market, accounting for approximately 65% of revenue in 2026, driven by their proven reliability, durability, and ability to operate efficiently in extreme climatic conditions. Across oil & gas fields, mining sites, construction zones, and remote communities, diesel-based systems remain the preferred choice due to well-established fuel supply chains and ease of deployment where grid infrastructure is weak or unavailable. In many African economies, diesel fuel is more accessible than piped gas, reinforcing continued adoption for backup and prime power applications. For example, diesel generator sets of Caterpillar Inc. are widely deployed across GCC infrastructure projects and African mining operations owing to their rugged design and strong after-sales support network.

The natural gas segment is likely to represent the fastest-growing segment in 2026, supported by abundant regional gas reserves, expanding LNG and pipeline infrastructure, and government policies promoting cleaner and lower-emission power generation solutions across the Middle East & Africa region. Governments across the GCC are encouraging gas-based power generation to reduce emissions while maintaining a reliable electricity supply, particularly in urban and industrial areas. Natural gas generators are increasingly favored for prime power and continuous-duty applications where lower operating costs and reduced environmental impact are critical decision factors. The transition toward gas is also supported by expanding LNG infrastructure and improved gas distribution networks, reducing dependence on diesel imports. For example, Wärtsilä Corporation supplies gas-fueled generator solutions for utility-scale and industrial customers in the Middle East, supporting national energy diversification strategies.

Power Ratings Insights

The 75–375 kVA power rating segment is projected to lead the market, accounting for around 45% of revenue in 2026, supported by its versatility across commercial, telecom, healthcare, and light-industrial applications. These generators strike an optimal balance between capacity, cost, and fuel efficiency, making them ideal for small and medium enterprises operating in rapidly urbanizing regions. Their adaptability supports both backup and limited prime power use, particularly in cities facing grid instability. Telecom operators rely heavily on this segment to ensure uninterrupted network operations, while commercial buildings favor it for emergency power coverage. For example, Cummins Inc. offers a broad portfolio of mid-range generators widely used in hospitals and telecom sites across Africa and the Middle East.

The 375 kVA segment is likely to be the fastest-growing in 2026, driven by rising demand from heavy industries, mega infrastructure projects, and data centers across the MEA region. Large-capacity generators are essential to ensure power continuity in oil & gas operations, mining facilities, airports, and industrial zones, where outages can cause severe financial losses. This segment benefits from increasing investments in smart cities and hyperscale data centers, particularly in the Gulf countries and South Africa. For instance, Rolls-Royce plc deploys its high-capacity generator systems in large industrial and utility-scale applications, offering exceptional reliability and efficiency. As governments prioritize economic diversification and industrial development, the demand for high-output generators is surging, presenting profitable opportunities for manufacturers targeting large-scale and mission-critical power projects.

Application Insights

Backup power is projected to dominate the Middle East & Africa generator market, accounting for around 55% of revenue by 2026, driven by ongoing grid instability and frequent power outages across the region. Key sectors such as healthcare, telecommunications, banking, and commercial real estate prioritize backup systems to safeguard operations, maintain data integrity, and ensure public safety. Backup generators are particularly essential in African economies, where grid reliability is inconsistent, and in Middle Eastern urban centers, where downtime can severely impact high-value services. For instance, Atlas Copco AB supplies backup generator solutions to hospitals and commercial facilities across the MEA region, supported by comprehensive service contracts. The prominence of backup power applications ensures consistent demand for equipment and ongoing maintenance revenues, making it a foundational segment for generator manufacturers and service providers.

Prime power is expected to be the fastest-growing segment in 2026, driven by the expansion of off-grid operations and limited grid access in rural Africa and remote areas of the Middle East. Industries such as mining, oil exploration, and large-scale construction are increasingly relying on generators as their primary power source. Prime power generators provide continuous electricity in regions where grid expansion is not economically feasible, thereby supporting industrial productivity and regional development. For instance, Perkins Engines Company Limited provides prime power solutions that are widely used in off-grid industrial and agricultural applications across Africa. As investments in resource extraction and remote infrastructure grow, prime power applications are gaining momentum, presenting significant growth opportunities in underserved and emerging markets throughout the MEA region.

Competitive Landscape

The Middle East & Africa generator market exhibits a moderately fragmented structure, driven by the presence of numerous international and regional manufacturers competing to meet diverse power needs across sectors such as oil & gas, telecom, construction, healthcare, and commercial infrastructure. Major multinational players maintain strong footholds in the MEA region by leveraging extensive distribution networks, localized service support, and broad product portfolios that span diesel, gas, and hybrid generator solutions. The market’s competitive environment reflects a balance between well-established brands and agile regional suppliers offering tailored solutions for specific applications and power ratings.

With key leaders including Caterpillar Inc., Cummins Inc., Kohler Co., Generac Power Systems, Inc., Rolls-Royce plc, Mitsubishi Heavy Industries, Ltd., Wärtsilä Corporation, Yanmar Co., Ltd., Doosan Corporation, Atlas Copco AB, Himoinsa, Perkins Engines Company Limited, and Kirloskar Electric Company Limited, the market is shaped by broad geographic reach and diversified technology stacks. These players compete through a combination of product innovation, service excellence, and strategic market expansion to retain and grow their market share. Manufacturers are increasingly focusing on introducing advanced generator systems that integrate IoT capabilities, remote monitoring, and energy management features to appeal to end-users seeking reliability and efficiency.

Key Industry Developments:

- In January 2026, Bobcat launched a new and expanded range of generators for the Middle East & Africa market, significantly strengthening its presence in the region’s highly competitive power equipment landscape. The new portfolio includes over 20 generator models with prime power outputs ranging from 20 kVA to 1650 kVA, designed and manufactured within the MEA region to meet local operating conditions. These generators feature enhanced heat resistance, high airflow cooling systems, and robust components, ensuring reliable performance in extreme temperatures above 40°C. Local manufacturing enables shorter delivery times, lower transportation costs, and reduced customs duties, improving the total cost of ownership for customers. The expanded lineup targets key applications such as construction, rental, telecommunications, agriculture, industrial operations, and backup power for small and large businesses.

- In August 2025, Caterpillar Inc. launched the new Cat® D1500 diesel generator set, delivering 1.5 MW of reliable standby power with a compact, space-efficient design. Powered by a 32.1-liter Cat C32B engine, the D1500 offers best-in-class power density while occupying up to 13% less floor space and being up to 32% lighter than previous models in the same power category. This reduced footprint and weight lower transportation, installation, and structural support costs, making the generator ideal for data centers, hospitals, commercial facilities, and other space-constrained environments. The Cat D1500 meets ISO 8528-5 performance standards, complies with NFPA 110 Level 1 Type 10 requirements for fast power restoration, and is ULC 2200 listed for the US and Canada. It also conforms to U.S. EPA Tier 2 emission standards for stationary emergency use.

Companies Covered in Middle East & Africa Generator Market

- Caterpillar Inc.

- Cummins Inc.

- Kohler Co.

- Generac Power Systems, Inc.

- Rolls-Royce plc

- Mitsubishi Heavy Industries, Ltd.

- Wärtsilä Corporation

- Yanmar Co., Ltd.

- Doosan Corporation

- Atlas Copco AB

- Himoinsa

- Perkins Engines Company Limited

- Kirloskar Electric Company Limited

Frequently Asked Questions

The Middle East & Africa generator market is projected to reach US$3.6 billion in 2026.

The Middle East and Africa generator market is driven by factors such as ongoing grid instability, increasing energy demand, rapid infrastructure development, and the rising need for dependable backup and off-grid power solutions across industrial, commercial, and residential sectors.

The Middle East & Africa generator market is expected to grow at a CAGR of 5.3% from 2026 to 2033.

Key market opportunities include the growth of renewable-hybrid generator systems, increased demand for gas-powered and low-emission generators, rising investments in infrastructure and data centers, and the expanding use of prime power solutions in off-grid and remote regions across the Middle East and Africa.

Caterpillar Inc., Cummins Inc., Kohler Co., Generac Power Systems, Inc., Rolls-Royce plc, and Mitsubishi Heavy Industries are the leading players.