- Marine

- Integrated Marine Automation System Size, Share, and Growth Forecast 2026 - 2033

Integrated Marine Automation System Size, Share, and Growth Forecast 2026 - 2033

Integrated Marine Automation System Market by Component (Hardware, Software, Services), by System (Power Management Systems, Vessel Management Systems, Process Control Systems, Others), End-user (Commercial, Defence, Others), and Regional Analysis, 2026 - 2033

Integrated Marine Automation System Market Size and Trend Analysis

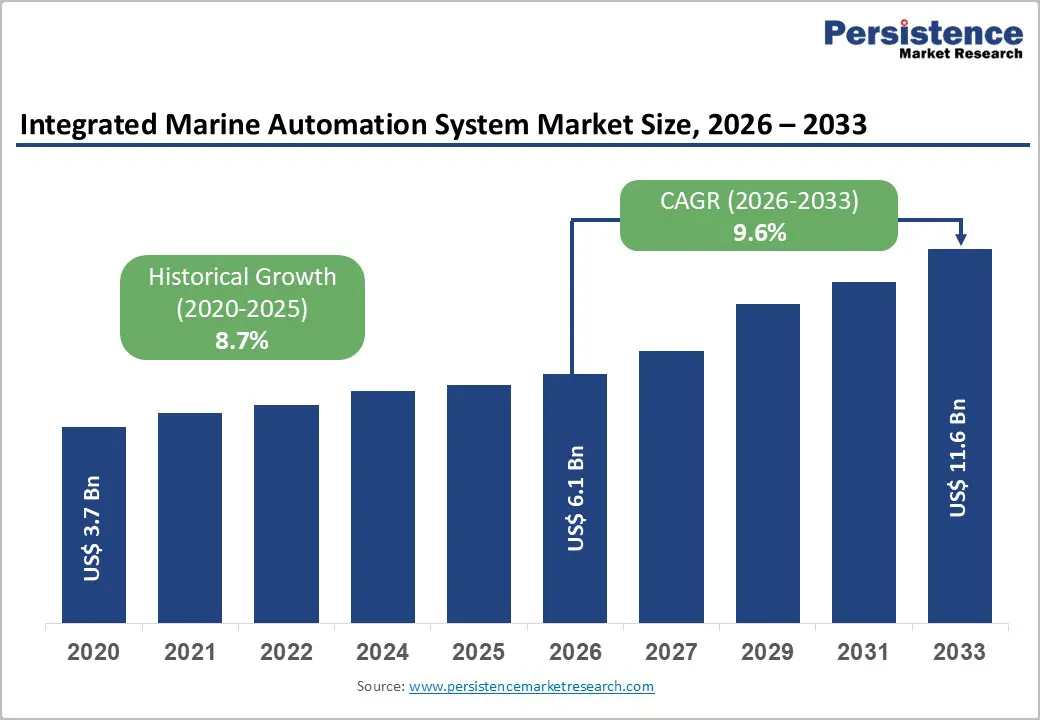

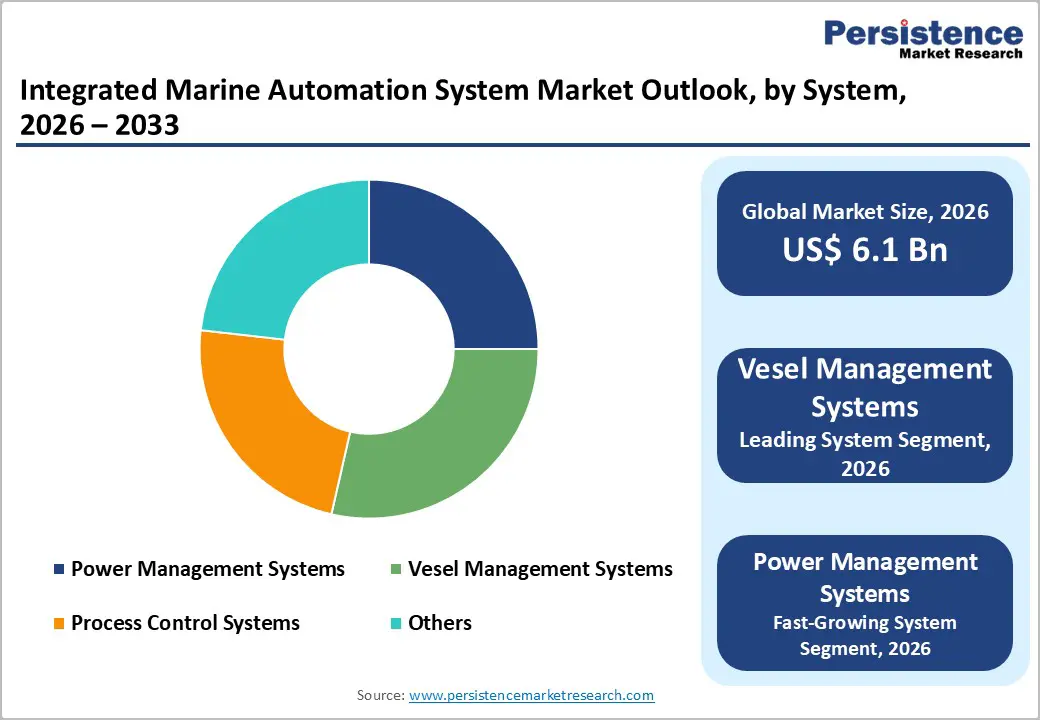

The global Integrated Marine Automation System market size is expected to be valued at US$ 6.1 billion in 2026 and projected to reach US$ 11.6 billion by 2033, growing at a CAGR of 9.6% between 2026 and 2033.

Rising demand for fuel-efficient vessel operations and improved operational safety is accelerating adoption across commercial and naval fleets. Increasing pressure to comply with international maritime safety and environmental standards is encouraging shipowners to upgrade automation platforms for navigation, propulsion, and engine monitoring. With more than 55,000 merchant vessels operating globally, shipping companies are investing in integrated automation to reduce fuel consumption, enable predictive maintenance, and support digital ship management systems.

Key Industry Highlights:

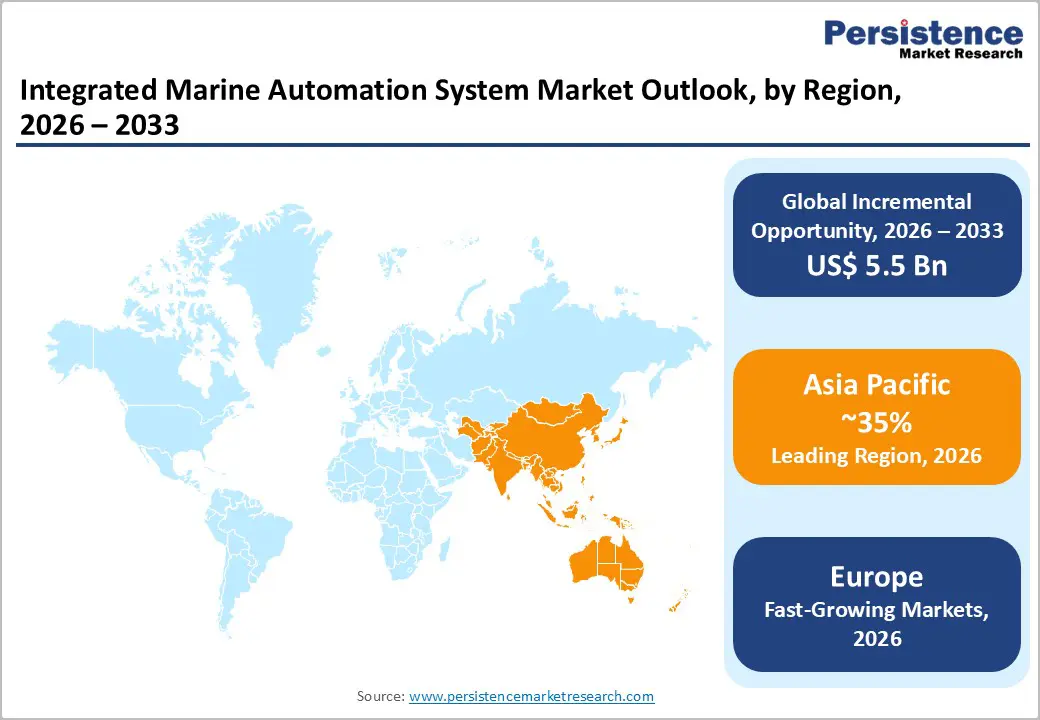

- Leading Region: Asia Pacific leads the market with 35% share in 2025, driven by strong shipbuilding capabilities and government-backed maritime initiatives.

- Fastest Growing Region: Asia Pacific is also the fastest-growing region, supported by manufacturing expansion, port modernization, and adoption of smart ship technologies.

- Leading Component Category: Hardware dominates the component segment with 45% share in 2025, providing reliable and durable infrastructure for vessel monitoring and control.

- Leading System Category: Vessel Management Systems (VMS) lead the system segment with 38% share in 2025, ensuring centralized control and regulatory compliance across vessels.

- Key Opportunity: Maritime Autonomous Surface Ships (MASS) represent a major opportunity, enabling autonomous operations, reducing crew dependence, and enhancing operational efficiency and safety.

| Key Insights | Details |

|---|---|

|

Integrated Marine Automation System Size (2026E) |

US$ 6.1 billion |

|

Market Value Forecast (2033F) |

US$ 11.6 billion |

|

Projected Growth CAGR (2026-2033) |

9.6% |

|

Historical Market Growth (2020-2025) |

8.7% |

Market Dynamics

Drivers - Advancements in IoT and AI Technologies Accelerating Digital Transformation and Smart Vessel Operations

Advancements in Internet of Things (IoT) and artificial intelligence technologies are significantly accelerating the adoption of integrated marine automation systems across modern vessels. These technologies enable real-time data collection from onboard equipment, allowing operators to monitor propulsion systems, engines, and power distribution through centralized platforms. Connected sensors and analytics tools help detect operational anomalies early, improving overall vessel reliability and reducing unexpected technical disruptions.

The integration of AI-driven analytics and cloud-based monitoring further supports predictive maintenance and remote diagnostics for fleet operators. Automated insights help optimize fuel consumption, propulsion performance, and route efficiency while minimizing manual intervention. As global shipping companies focus on improving operational resilience and digital fleet management, smart automation platforms are becoming essential components of next-generation maritime infrastructure.

Stringent Environmental Compliance and Maritime Safety Regulations Driving Automation Adoption

Increasingly strict environmental and maritime safety regulations are playing a critical role in driving the adoption of integrated marine automation systems worldwide. Regulatory frameworks aimed at controlling ship emissions and ensuring vessel safety require continuous monitoring of propulsion systems, fuel usage, and environmental performance. Automation platforms help ship operators maintain compliance by providing accurate data tracking and automated reporting capabilities.

Advanced monitoring systems also improve onboard safety by enabling automated alerts, fault detection, and system diagnostics during vessel operations. By continuously tracking emissions, ballast water management, and engine performance, automation technologies reduce operational risks and help shipping companies avoid costly regulatory penalties. As maritime authorities tighten compliance standards, integrated automation solutions are becoming vital for sustainable and secure vessel operations.

Restraints - High Capital Investment Requirements and Technical Complexities in Retrofitting Existing Vessel Fleets

High initial investment requirements remain a significant barrier to the adoption of integrated marine automation systems, particularly for small and mid-sized shipping operators. Implementing advanced automation platforms requires substantial spending on hardware, software integration, and onboard control infrastructure. These costs can be challenging for operators with tight budgets or fleets operating on thin profit margins.

Retrofitting existing vessels also presents technical and operational challenges. A large share of global fleets still rely on legacy mechanical and electronic systems that were not designed for modern digital integration. Upgrading these vessels often involves complex installation processes, compatibility issues, and potential operational downtime, which discourages some shipowners from adopting automation technologies.

Growing Cybersecurity Risks in Digitally Connected Maritime Infrastructure

The increasing connectivity of modern vessels has raised serious concerns about cybersecurity vulnerabilities within maritime automation systems. Integrated platforms rely on networked sensors, cloud connectivity, and remote monitoring systems, which can become potential entry points for cyber threats if not properly secured. Unauthorized access or system manipulation could disrupt vessel operations and compromise onboard safety.

Maritime organizations are therefore required to invest heavily in cybersecurity frameworks, software updates, and network protection systems to safeguard automation platforms. While these security measures are necessary for protecting critical infrastructure, they also increase operational costs and implementation complexity. Concerns surrounding cyber risks may slow the pace of digital adoption among shipping operators and maritime stakeholders.

Opportunities - Emerging Adoption of Maritime Autonomous Surface Ships Creating New Opportunities for Advanced Automation Systems

The growing development of Maritime Autonomous Surface Ships (MASS) is opening significant opportunities for integrated marine automation technologies. Autonomous vessel initiatives are gaining momentum as maritime authorities and research organizations explore new frameworks to support remotely operated and partially autonomous ships. These developments are encouraging shipbuilders and technology providers to integrate advanced automation, navigation, and monitoring capabilities into future vessel designs.

Autonomous operations offer substantial benefits, including improved operational efficiency, enhanced safety, and reduced dependence on onboard crew. Automation platforms enable real-time monitoring, intelligent navigation, and remote control of ship systems, supporting safer operations in complex maritime environments. As pilot projects and regulatory frameworks for autonomous shipping continue to evolve, demand for integrated automation solutions is expected to expand significantly.

Expansion of Offshore Energy Projects Increasing Demand for Advanced Marine Automation Solutions

The rapid expansion of offshore energy projects is creating strong demand for reliable marine automation systems across specialized vessels. Offshore wind installations, subsea infrastructure projects, and offshore oil and gas exploration require highly automated vessels capable of precise positioning, power management, and equipment monitoring. Automation technologies help operators maintain efficiency and safety in challenging offshore environments.

In addition to energy projects, defense modernization programs are increasing investments in advanced naval platforms and unmanned maritime systems. These vessels rely heavily on integrated automation for navigation, propulsion control, and mission system monitoring. As offshore infrastructure development and maritime security initiatives continue to expand, specialized automation solutions are becoming increasingly important for supporting complex marine operations.

Category-wise Analysis

Component Insights

Hardware dominates the Integrated Marine Automation System market by component, holding 45% share in 2025. Sensors, programmable logic controllers (PLCs), actuators, and control modules form the core infrastructure enabling vessel monitoring, propulsion control, and system communication. Their reliability and durability make them essential for harsh marine environments, while most compliant automation installations rely on robust hardware architecture to ensure stable operations and safety across commercial and naval vessels.

Software is emerging as the fastest-growing component as shipping companies adopt digital fleet management and predictive analytics. Advanced software platforms enable centralized vessel monitoring, remote diagnostics, and performance optimization through data-driven insights. Increasing adoption of cloud-based maritime platforms and AI-driven analytics is encouraging operators to integrate advanced software tools to improve operational efficiency and support smarter ship management.

System Insights

Vessel Management Systems (VMS) lead the system segment, capturing 38% share in 2025. These platforms integrate navigation, propulsion control, alarm systems, and machinery monitoring into a unified interface, enabling ship operators to manage multiple vessel functions simultaneously. Their ability to provide centralized operational visibility and ensure regulatory compliance makes VMS essential for modern vessels operating in complex maritime environments.

Power Management Systems represent the fastest-growing system category as ship operators prioritize efficient onboard energy distribution and fuel optimization. These systems regulate electricity generation, load balancing, and energy consumption across ship systems. Growing adoption of hybrid propulsion technologies and energy-efficient ship designs is accelerating the demand for advanced power management automation.

End-user Insights

The commercial segment dominates accounting for 52% share in 2025 due to widespread adoption across cargo vessels, tankers, container ships, and passenger vessels. Automation technologies help shipping companies optimize fuel consumption, improve navigation efficiency, and comply with international maritime environmental and safety regulations, supporting large-scale deployment across global merchant fleets.

The defence is the fastest-growing end-use category as naval forces increasingly adopt advanced automation systems for mission-critical operations. Integrated automation improves vessel monitoring, propulsion management, and operational safety in naval ships. Rising investments in technologically advanced naval fleets and autonomous maritime platforms are driving demand for automation solutions in defense applications.

Regional Insights

North America Integrated Marine Automation System Market Trends

North America holds a significant position in the Integrated Marine Automation System market, accounting for 28% share in 2025. The region benefits from strong maritime technology development, advanced naval infrastructure, and continuous investment in vessel modernization programs. The United States plays a central role in driving innovation in ship automation, digital navigation systems, and cybersecurity frameworks designed to protect connected maritime infrastructure.

Technological advancements in autonomous shipping and smart vessel operations are accelerating market development across the region. Government-supported research initiatives and defense modernization programs are encouraging the adoption of advanced automation systems in naval fleets and offshore vessels. Increasing focus on secure digital maritime operations is also driving demand for integrated automation platforms that ensure reliable monitoring and system protection.

Europe Integrated Marine Automation System Market Trends

Europe represents a technologically advanced market for integrated marine automation systems, supported by strong shipbuilding expertise and maritime engineering capabilities. Countries such as Germany, Norway, and the United Kingdom are key contributors to the development of advanced vessel management and automation platforms. Regional collaboration and unified maritime regulations are encouraging ship operators to upgrade existing fleets with modern automation technologies.

The region is projected to grow at a CAGR of 9.8% between 2026 and 2033, driven by increasing investments in digital shipping infrastructure and autonomous vessel research. European shipbuilders and technology providers are focusing on advanced control systems, intelligent navigation platforms, and environmentally compliant automation solutions to support sustainable maritime operations and next-generation vessel designs.

Asia Pacific Integrated Marine Automation System Market Trends

Asia Pacific dominates the Integrated Marine Automation System market with 35% share in 2025, supported by the region’s strong shipbuilding industry and expanding maritime trade activities. Countries such as China, Japan, and South Korea account for a significant share of global ship construction, creating strong demand for automation technologies integrated into new vessels during the manufacturing stage.

The region is also emerging as the fastest-growing market as governments invest in port modernization, digital shipping infrastructure, and advanced vessel technologies. Expanding maritime trade networks, growing offshore energy projects, and increasing adoption of smart ship technologies are accelerating demand for integrated marine automation solutions across major shipbuilding and shipping economies in Asia Pacific.

Competitive Landscape

The Integrated Marine Automation System market is highly consolidated, with leading players focusing on technological differentiation and strategic expansion. Companies are investing heavily in research and development, particularly in AI, predictive maintenance, and autonomous vessel capabilities. Certifications, modular system designs, and advanced integration features provide a competitive edge, enabling providers to meet stringent safety and environmental regulations while offering flexible solutions for diverse vessel types.

Emerging business models, such as as-a-service and subscription-based platforms, are gaining traction among small and medium-sized operators. These models reduce upfront costs, simplify deployment, and support broader adoption of automation technologies across commercial and defense fleets, enhancing market reach and scalability.

Key Developments:

- In June 2025, Kongsberg unveiled an upgraded K-Chief platform, merging multiple vessel systems for seamless integration. The enhancement improved operational efficiency, strengthened onboard safety, and provided centralized control, supporting smarter navigation, propulsion management, and real-time monitoring across commercial and naval fleets.

- In March 2024, Kongsberg supplied integrated marine automation systems to 10 Shell LNG carriers, ensuring compliance with stringent emission standards. The deployment enabled optimized fuel consumption, real-time engine monitoring, and environmental performance tracking, demonstrating advanced automation capabilities for large-scale maritime operations.

- In November 2023, Wärtsilä partnered with Maersk to implement hybrid automation systems on 15 vessels. The collaboration focused on energy-efficient propulsion, predictive maintenance, and centralized control, enhancing operational performance, reducing fuel consumption, and supporting sustainable shipping practices across commercial fleets.

Companies Covered in Integrated Marine Automation System Size, Share, and Growth Forecast 2026 - 2033

- ABB Ltd.

- Siemens AG

- Kongsberg Gruppen

- Wärtsilä Corporation

- Honeywell International Inc.

- Thales Group

- Northrop Grumman Corporation

- Emerson Electric Co.

- Rockwell Automation, Inc.

- Blue Ctrl AS

- Høglund AS

- Jason Marine Group

- Tokyo Keiki Inc.

- Consilium AB

- Ulstein Group ASA

Frequently Asked Questions

The market is expected to reach US$ 6.1 billion in 2026.

Rising demand is driven by IMO SOLAS and emission regulations requiring efficient vessel monitoring and control.

Asia Pacific leads the market with 35% share in 2025 due to shipbuilding strength and maritime initiatives.

Key opportunities include Maritime Autonomous Surface Ships (MASS) and offshore energy sector expansion.

Leading players include ABB Ltd., Siemens AG, Kongsberg Gruppen, Wärtsilä Corporation, and Honeywell International Inc.