- Inks, Coatings, Adhesives & Sealants (ICAS)

- Marine Coatings Market

Marine Coatings Market Size, Share, and Growth Forecast 2026 - 2033

Marine coatings market by Product Type (Anti-fouling, Anti-corrosion, Foul release, Anti-slip, Others), Resin (Epoxy, Alkyd, Others), Application (Ships, Shipyards, Offshore Civil Structure, Yachts, Container Vessels, Others), and Regional Analysis, 2026-2033

Marine Coatings Market Size and Trends Analysis

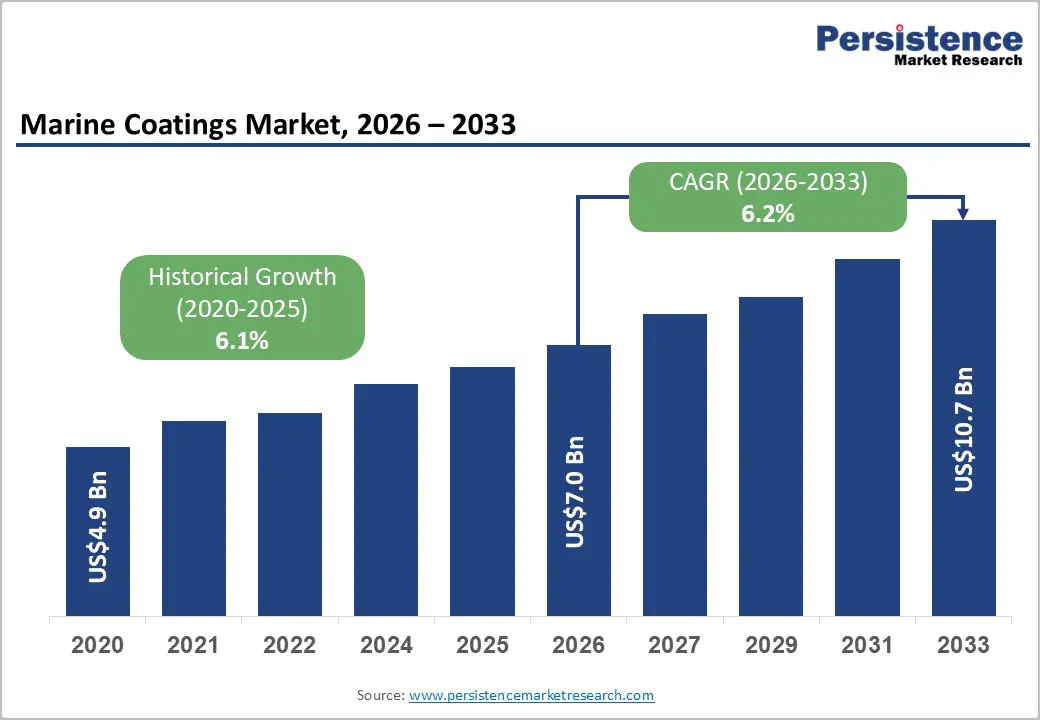

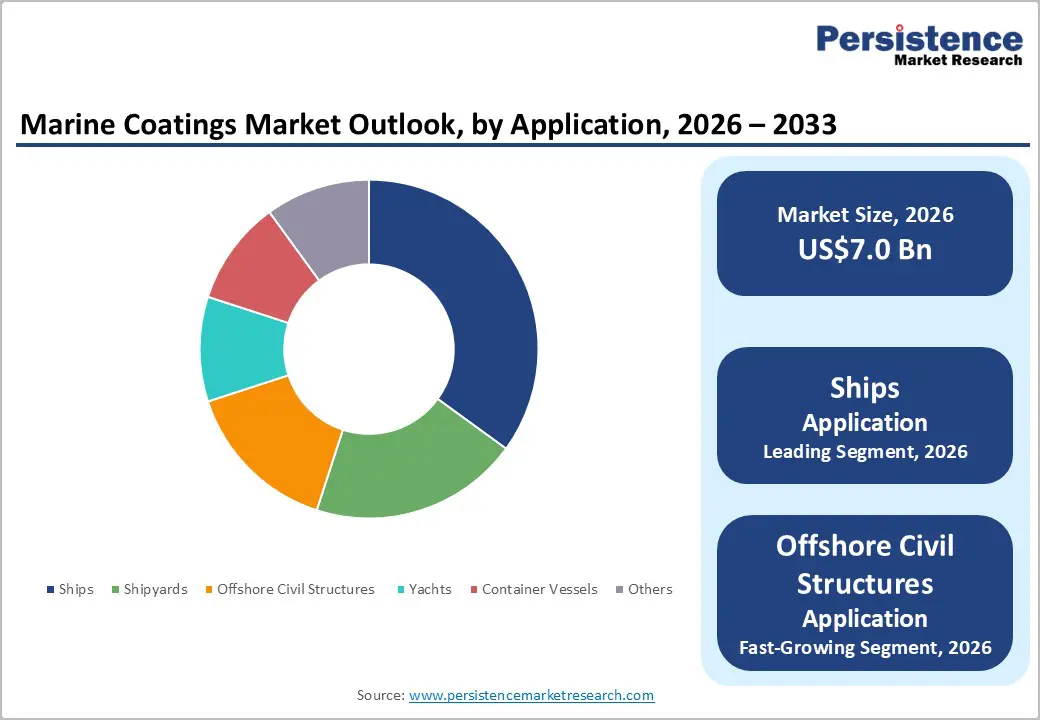

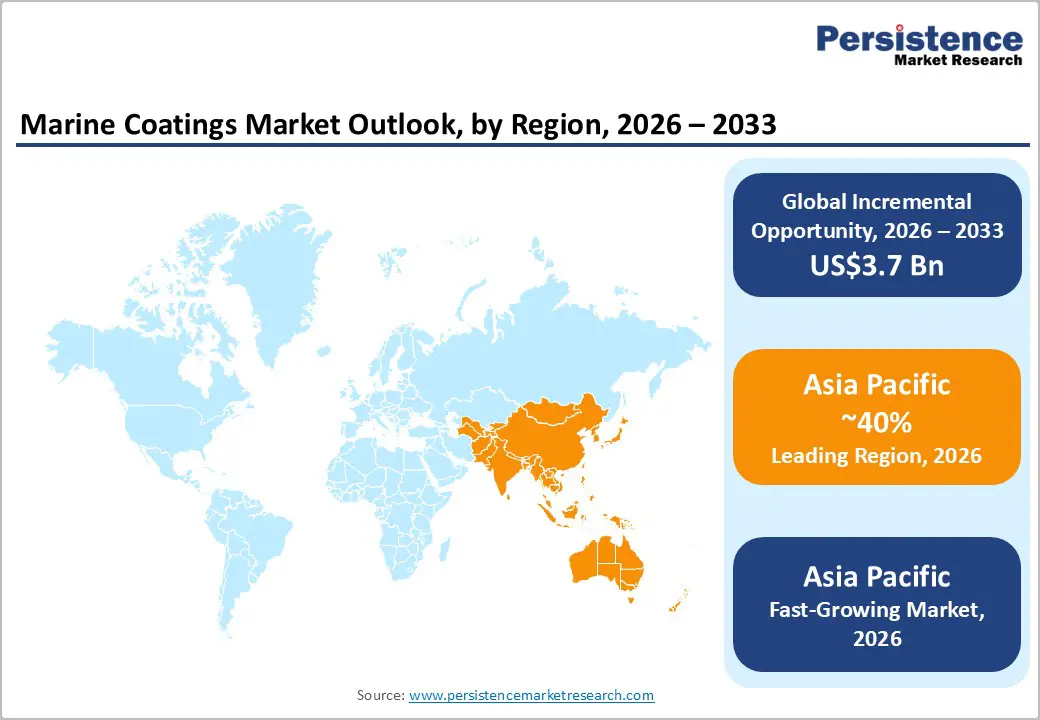

The global marine coatings market size is expected to be valued at US$7.0 billion in 2026 and projected to reach US$10.7 billion by 2033, growing at a CAGR of 6.2% during the forecast period from 2026 to 2033, driven by surging global maritime trade and stringent environmental regulations promoting eco-friendly protective solutions.

Rising shipbuilding activities, particularly in Asia, and the need for fuel-efficient hull coatings to combat biofouling are the key boosters. According to UNCTAD, global seaborne trade grew by 3.2% in 2024, driving the demand for durable anti-corrosion and anti-fouling products that reduce drag and emissions.

Key Industry Highlights:

- Dominant Region: Asia Pacific is expected to command 40% share, powered by shipbuilding giants such as China and Japan.

- Fastest-growing Region: Asia Pacific grows the fastest at 6.5% CAGR, driven by trade and offshore boom.

- Dominant Product Type: Anti-fouling, to dominate with 45% share for biofouling prevention.

- Dominant Application: Ships, to dominate applications with a 50% share in 2026, as cargo and passenger vessels over 51,000 cargo ships globally demand extensive hull protection.

| Key Insights | Details |

|---|---|

|

Marine Coatings Size (2026E) |

US$7.0 Bn |

|

Market Value Forecast (2033F) |

US$10.7 Bn |

|

Projected Growth CAGR (2026-2033) |

6.2% |

|

Historical Market Growth (2020-2025) |

6.1% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Growth Analysis - Rising Seaborne Trade and Shipbuilding Expansion

Increasing international maritime trade is creating a significant demand for durable marine coatings that can protect vessels from the harsh conditions of open oceans, including saltwater corrosion, biofouling, and extreme weather. As ships carry larger volumes of cargo over longer distances, maintaining hull integrity and operational efficiency becomes essential. High-performance marine coatings help reduce friction and prevent the accumulation of marine organisms, directly improving fuel efficiency and lowering maintenance costs.

The International Maritime Organization (IMO) has intensified its focus on sustainability, introducing measures such as the Energy Efficiency Existing Ship Index (EEXI) and Carbon Intensity Indicator (CII). These regulations push shipping operators to reduce greenhouse gas emissions, which has accelerated the adoption of coatings that improve hydrodynamics and minimize biofouling. By reducing drag, these coatings help vessels consume less fuel and comply with stricter environmental standards.

Stringent Environmental Regulations and Fuel Efficiency Imperatives

The IMO guidelines on biofouling management and emissions are reshaping the marine coatings landscape, driving shipowners and operators to adopt advanced anti-fouling and foul-release solutions. Biofouling, the accumulation of marine organisms on a vessel’s hull, increases drag, which in turn raises fuel consumption and greenhouse gas emissions. To meet regulatory requirements, vessels must maintain smoother hull surfaces, making high-performance coatings essential for compliance with international standards.

The marine coatings industry has developed biocide-free and low-emission technologies that prevent organism growth without harming marine ecosystems. These innovations not only align with global sustainability objectives but also enhance operational efficiency by reducing fuel use and minimizing CO output. By mitigating friction and improving hydrodynamics, modern coatings allow ships to achieve better speed, lower operational costs, and longer intervals between maintenance. Merchant fleets and offshore vessels benefit from these technologies, as they extend service life, reduce dry-docking frequency, and offer predictable maintenance schedules.

Barrier Analysis - Regulatory Restrictions on Biocides and Environmental Concerns

The phasing out of harmful biocides, including restrictions on copper-based compounds, is significantly reshaping the marine coatings industry. Traditionally, copper and similar biocides were central to anti-fouling coatings because of their proven ability to prevent biofouling effectively. Growing environmental concerns and stricter IMO and regional regulations have forced manufacturers to develop alternative, eco-friendly solutions. These regulatory pressures complicate formulation development, as new coatings must balance environmental compliance with performance requirements, such as durability, fouling resistance, and fuel efficiency.

Developing biocide-free or low-impact alternatives requires substantial R&D investment, advanced testing, and innovation in materials science. This can increase production costs, limit traditional formulation options, and potentially delay product launches. Some eco-alternatives may not perform as effectively under extreme marine conditions, creating challenges for fleet operators who rely on coatings to maintain efficiency and minimize maintenance. Manufacturers must carefully optimize formulations to meet both regulatory standards and operational expectations, while customers face higher prices and cautious adoption.

Volatility in Raw Material Prices and Supply Chain Challenges

Fluctuations in resin and pigment costs have become a critical challenge for marine coatings manufacturers, as these materials form the backbone of high-performance formulations. Price volatility can stem from raw material scarcity, energy cost variations, or changing demand in related industries like plastics and chemicals. Such instability directly increases production expenses, forcing manufacturers to adjust pricing, absorb costs, or modify formulations, all of which can affect profit margins.

Adding to the complexity are geopolitical disruptions, trade restrictions, regional conflicts, and port delays that can interrupt the supply of essential resins, pigments, and specialty additives. Many marine coatings rely on specialized materials with limited suppliers, meaning any disruption can create bottlenecks, delay production, and lead to shortages in the market. These challenges are especially pronounced for manufacturers serving commercial and offshore fleets, where reliability and performance are critical. The combined effect of rising raw material costs and supply chain vulnerabilities pressures companies to explore alternative sourcing, secure long-term supplier agreements, and optimize formulations for efficiency.

Opportunity Analysis - Shift to Eco-Friendly and Foul-Release Technologies

The growing emphasis on biocide-free foul-release coatings is transforming the marine coatings market, offering both environmental and operational benefits. Driven by the IMO’s biofouling management guidelines, which encourage the adoption of non-toxic, sustainable solutions, these coatings are designed to prevent the accumulation of marine organisms without relying on harmful chemical biocides. By reducing friction and improving hydrodynamics, foul-release coatings enhance vessel efficiency, lower fuel consumption, and contribute to greenhouse gas emissions reduction, aligning with global maritime sustainability targets.

Beyond regulatory compliance, these coatings also extend service life and minimize the frequency of dry-docking, lowering maintenance costs and operational downtime for shipowners. The fastest-growing segment within marine coatings foul-release technologies has seen rising demand in both newbuilds and retrofit applications, reflecting a broader industry shift toward environmentally responsible solutions. For manufacturers, this trend presents opportunities to capture premium market value, as shipping operators are willing to invest in high-performance, sustainable coatings that combine regulatory compliance with tangible cost and efficiency advantages.

Expansion in Offshore and Renewable Energy Applications

The expansion of offshore and renewable energy applications is driving increased demand for specialized marine coatings. Offshore platforms, wind farms, and tidal energy installations operate in highly corrosive and dynamic marine environments, where exposure to saltwater, waves, and biofouling can significantly reduce structural integrity and operational efficiency. Advanced coatings are essential to protect these assets, ensuring durability, minimizing maintenance requirements, and extending service life.

As the global shift toward renewable energy accelerates, particularly in offshore wind and tidal projects, operators are prioritizing high-performance coatings that resist corrosion and fouling while supporting regulatory compliance and environmental sustainability. These coatings often incorporate biocide-free or low-impact technologies to meet environmental standards and reduce ecological impact, reflecting the industry’s commitment to green operations. The growth of offshore and renewable energy sectors also encourages innovation in application techniques and material formulations, tailored to large-scale structures and long-term exposure.

Category-wise Insights

Product Type Analysis

Anti-fouling is expected to lead, with a 45% market share in 2026, due to its critical role in maintaining vessel efficiency and longevity. These coatings prevent the accumulation of marine organisms on hulls, reducing drag, fuel consumption, and greenhouse gas emissions, which is increasingly important under IMO regulations and global sustainability targets. Anti-fouling solutions are widely adopted across commercial shipping, offshore platforms, and newbuilds, offering both operational and regulatory benefits.

AkzoNobel’s International Paint brand has a leading position with its Intersleek antifouling and foul release coatings, which significantly reduce hull friction and improve vessel efficiency while aligning with environmental regulations, helping shipowners cut fuel consumption and emissions. This range has become a preferred choice for large commercial fleets and cruise ships globally due to its performance and sustainability credentials.

Foul release is likely to be the fastest-growing, fueled by increasing restrictions on copper-based biocides and rising demand for eco-friendly solutions. These coatings work by creating ultra-smooth surfaces that prevent marine organisms from adhering, effectively reducing hull drag by up to 10%, which lowers fuel consumption and greenhouse gas emissions. Their non-toxic, biocide-free composition aligns with IMO biofouling regulations and global sustainability goals, making them attractive for newbuilds and retrofits alike.

Propspeed® foul release systems from Propspeed International. Propspeed has long been recognized as an industry leading biocide free foul release coating solution that prevents marine organisms from attaching to underwater metals such as propellers, shafts, and rudders by creating an ultra smooth, non toxic surface. It improves vessel performance, reduces drag, lowers fuel use, and requires less maintenance compared with traditional antifouling paints.

Application Analysis

Ships are anticipated to dominate the market, with over a 50% share in 2026, driven by the extensive protection needs of cargo and passenger vessels. With more than 51,000 cargo ships globally, hulls require anti-fouling, anti-corrosion, and protective coatings to ensure durability, fuel efficiency, and regulatory compliance. New shipbuilding projects account for roughly 55% of anti-corrosion coating consumption, reflecting investment in fleet renewal and expansion to meet growing international trade.

Hempel A/S, another major marine coating supplier, has partnered with shipping operators to apply its Hempaguard X8 foul release and anti fouling coatings across fleets of cargo and passenger ships, helping reduce drag and fuel use in real operations.

Offshore civil structure is likely to be the fastest-growing, propelled by expanding oil and gas platforms and offshore wind farms. These structures face extreme marine conditions, including high salinity, strong currents, and constant wave action, which accelerate corrosion and material degradation. Advanced protective coatings are essential to ensure structural integrity, reduce maintenance frequency, and extend service life.

Rising investments in renewable energy, particularly offshore wind projects, along with continued oil and gas exploration, are increasing demand for durable, high-performance coatings. Jotun Group’s involvement in France’s EOLMED floating offshore wind project, where it provided over 60,000 liters of protective coatings for both exterior and interior surfaces of floating foundations. This highlights how high performance coatings are essential as offshore renewable energy expands into harsher and more challenging environments.

Regional Insights

North America Marine Coatings Market Trends

North America is led by the U.S., driven by its advanced naval, commercial shipping, and offshore energy sectors. Naval vessels, commercial ships, and offshore platforms across the region rely on high-performance marine coatings that meet strict durability, anti-corrosion, and biofouling resistance requirements. In the U.S., the Coast Guard enforces Protective System for Coatings (PSPC) standards to safeguard hull integrity and operational safety, pushing manufacturers to develop innovative solutions that extend service life and reduce maintenance costs.

In the offshore oil and gas sector, particularly in the Gulf of Mexico, anti-corrosion coatings are critical to withstand harsh marine conditions such as high salinity, constant wave action, and extreme weather. Regulatory pressure from agencies such as the EPA, including low-VOC limits, is accelerating the adoption of biocide-free and environmentally friendly coating technologies that protect marine assets while minimizing ecological impact. At the same time, the U.S. is investing in green shipping initiatives, including energy-efficient hull coatings and foul-release systems, which can reduce hydrodynamic drag and lower fuel consumption by approximately 10%, supporting both cost savings and long-term decarbonization goals.

Europe Marine Coatings Market Trends

Europe maintains a strong position in the marine coatings market, led by countries such as Germany, the U.K., and France, supported by an advanced shipbuilding industry and a strong emphasis on high-performance, environmentally compliant solutions. The region benefits from a robust mix of large commercial shipyards, naval construction, and offshore vessel production, driving demand for coatings that protect against corrosion, biofouling, and harsh marine environments.

IMO 2020 regulations limiting sulfur content in marine fuels have accelerated the adoption of silicone-based foul-release coatings that reduce hydrodynamic drag and improve fuel efficiency, aligning environmental compliance with operational performance.

In Spain, a thriving yacht and recreational boating sector is boosting demand for epoxy coatings that provide long-lasting protection and superior adhesion, while helping operators achieve high levels of emissions compliance. Across Europe, durability, anti-corrosion performance, and resistance to environmental stress remain key priorities, particularly under international frameworks such as the Ballast Water Management Convention, which regulates ballast water treatment to prevent the spread of invasive species. These regulatory and performance requirements have encouraged the development of R&D hubs across the region, with companies investing in advanced coating chemistries, biocide-free foul-release technologies, and hybrid systems that balance longevity, environmental compliance, and operational efficiency.

Asia Pacific Marine Coatings Market Trends

Asia Pacific is projected to dominant and fastest-growing region, capturing the 40% revenue in 2026, largely driven by China and Japan, which together account for nearly 90% of global shipbuilding capacity, according to UNCTAD. Their advanced shipyards produce a vast number of commercial vessels, naval ships, and offshore platforms, all requiring high-performance coatings for corrosion protection, anti-fouling, and fuel efficiency.

Emerging shipbuilding hubs in India and ASEAN countries are further accelerating growth, leveraging lower manufacturing costs and favorable labor economics to expand regional capacity. Large, modern ports across Asia Pacific, such as Shanghai, Singapore, and Busan, handle increasing trade volumes, creating strong demand for anti-fouling coatings to improve vessel speed, reduce fuel consumption, and enhance operational efficiency. Coastal infrastructure expansions, including dry docks, repair facilities, and offshore energy projects, contribute to a regional CAGR of 6.3%, supporting both newbuild and maintenance markets.

Asia Pacific’s combination of high-volume ship production, growing trade, cost advantages, and expanding port and offshore infrastructure makes it the center of innovation and adoption for marine coatings, particularly advanced anti-fouling, biocide-free, and energy-efficient solutions.

Competitive Landscape

The global marine coatings market is moderately consolidated, with the top players accounting for 60–70% of global market share through extensive supply chains, technological expertise, and ongoing R&D investments. Leading companies pursue strategic expansions via acquisitions, joint ventures, and partnerships with shipyards to strengthen market reach and enhance product portfolios. Emphasis is increasingly placed on sustainable formulations, including low-VOC epoxies, biocide-free foul-release coatings, and advanced anti-corrosion solutions that comply with IMO regulations and environmental standards. Key differentiators among market leaders include eco-compliant technologies, predictive maintenance models, and tailored solutions for newbuilds and retrofits.

The competitive landscape is dominated by major players such as AkzoNobel N.V., PPG Industries, Inc., The Sherwin-Williams Company, Axalta Coating Systems, LLC, and BASF, all of which leverage global networks and innovation to maintain leadership. AkzoNobel and PPG focus on advanced antifouling and foul-release technologies, while Sherwin-Williams and Axalta emphasize high-performance protective coatings for offshore and naval applications. BASF contributes specialty resins and coatings that improve durability and operational efficiency.

Key Industry Developments:

- In October 2025, the International Maritime Organization (IMO) introduced new regulations on the use of low-flashpoint marine fuels, which will increase the demand for high-performance marine coatings that can protect ships from the adverse effects of these fuels. This regulatory development is expected to drive growth in the market over the coming years (IMO.Org).

- In November 2024, PPG announced that its 50th order for the electrostatic application of marine fouling control coatings was received. The project was carried out on the VLCC SIDR, a 336-meter oil tanker operated by Bahri Ship Management, at the Asyad Drydock Company shipyard in Oman. The vessel’s hull was coated with PPG NEXEON™ 810 antifouling coating, marking a milestone for the application of advanced, copper-free marine coatings.

Companies Covered in Marine Coatings Market

- Akzo Nobel N.V

- PPG Industries, Inc.

- The Sherwin-Williams Company

- Axalta Coating Systems, LLC

- BASF

- KANSAI PAINT CO., Ltd.

- Nippon Paint Marine Coatings Co. Ltd.

- PPG Asian Paints Private Limited

- Jotun

- Hempel Foundation

- Mascoat

- Comex

- KCC corporation

- Chugoku Marine Paints, Ltd.

- National Paints Factories Co. Ltd.

Frequently Asked Questions

The global marine coatings market is expected to reach US$7.0 billion in 2026.

Demand is driven by IMO regulations on emissions and biofouling, alongside growth in seaborne trade requiring fuel-efficient protective solutions.

The marine coatings market is poised to witness a CAGR of 6.2% from 2026 to 2033.

Eco-friendly foul-release technologies present major potential amid shifts to sustainable, biocide-free options.

Major players include Akzo Nobel N.V., PPG Industries, Inc., Jotun, and Hempel.