- Specialty & Fine Chemicals

- Latin America Ammunition Market

Latin America Ammunition Market Size, Share, Trends, Growth, Regional Forecasts, 2026 to 2033

Latin America Ammunition Market by Ammunition Type (Small Caliber, Medium Caliber, Large Caliber, Mortar & Artillery Ammunition), End-User (Military, Civilians), Technology (Smart, Conventional, Reduced-Ricochet), and Regional Analysis for 2026-2033

Latin America Ammunition Market Share and Trends Analysis

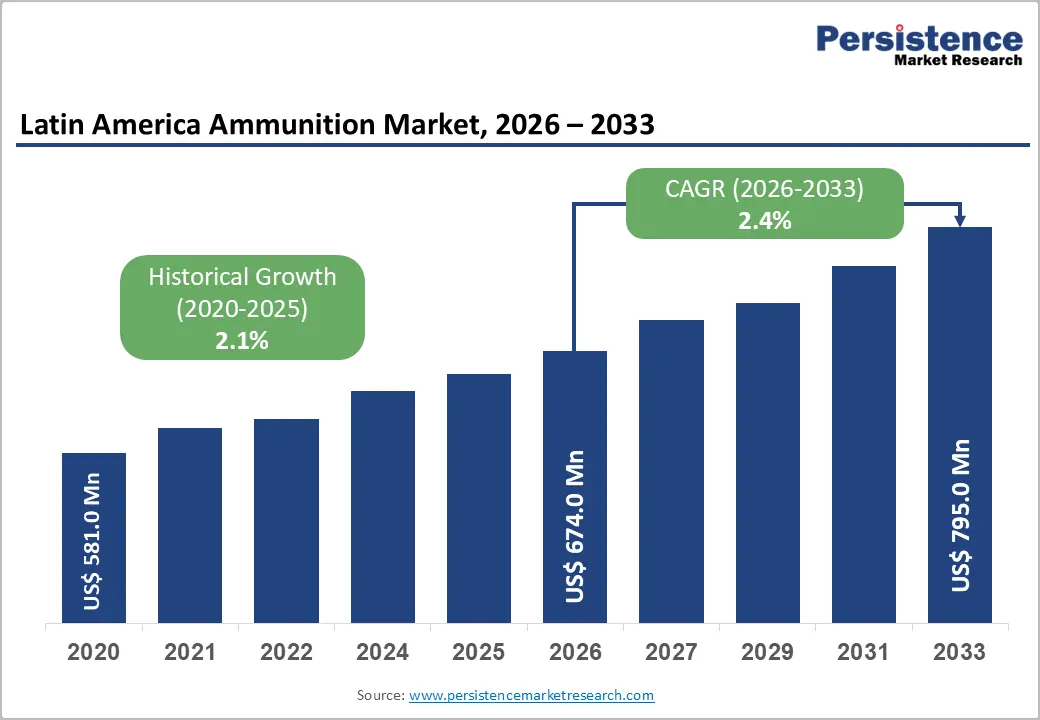

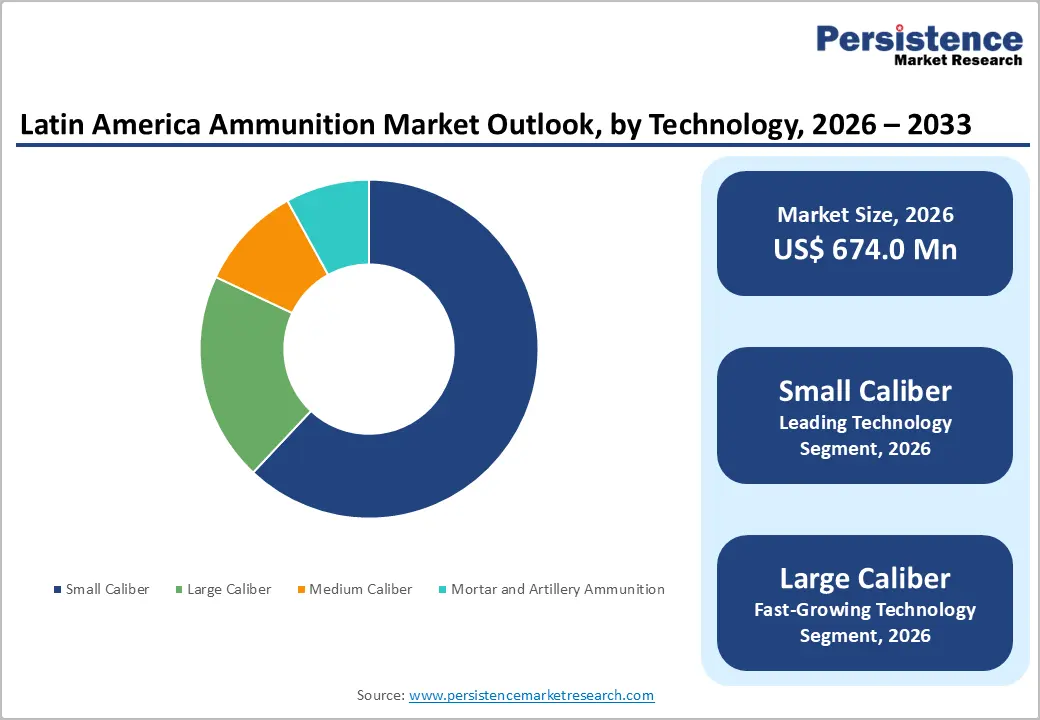

The Latin America ammunition market size is likely to be valued at US$ 674.0 million in 2026, and is projected to reach US$ 795.0 million by 2033, growing at a CAGR of 2.4% during the forecast period 2026−2033.

This expansion is underpinned by rising defense budget allocations across the region, escalating law enforcement procurement activity, and accelerating modernization of national security infrastructure. Brazil and Mexico collectively anchor regional demand, accounting for the majority of total consumption. Strategic procurement contracts, ongoing counter-narcotics operations, and border security imperatives continue to shape purchasing patterns, while regulatory frameworks governing civilian access influence market segmentation dynamics across countries.

Key Industry Highlights

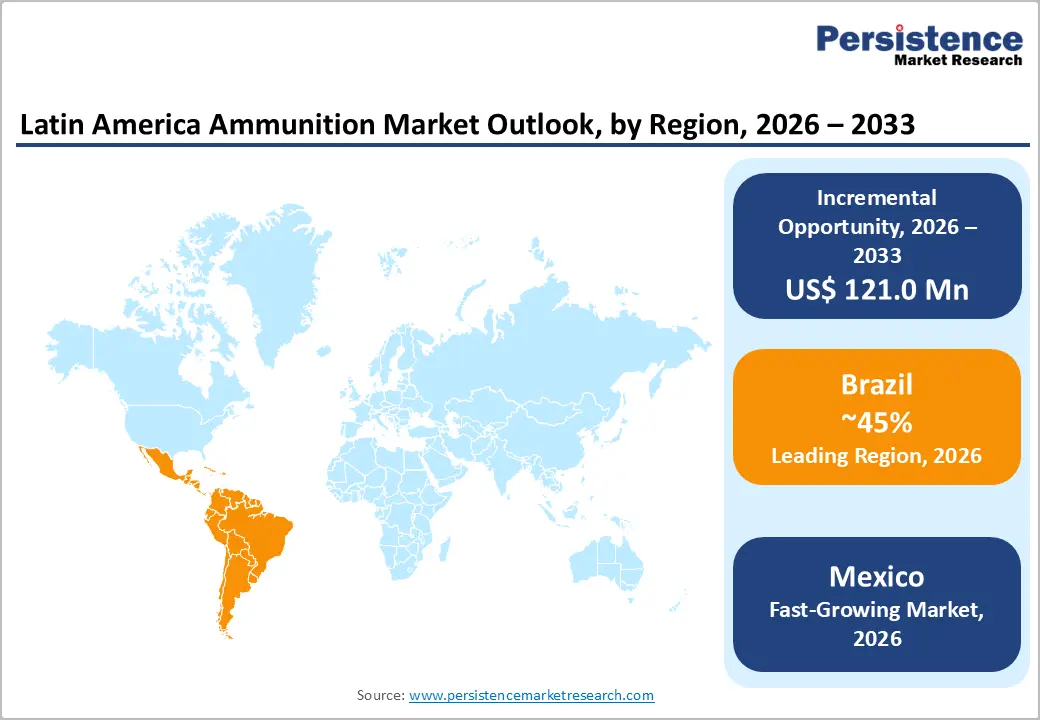

- Dominant Country: Brazil is anticipated to dominate with approximately 45% market share in 2026, owing to a strong combination of military, law enforcement, and civilian demand.

- Fastest-growing Country: Mexico is expected to be the fastest-growing country between 2026 and 2033, driven mainly by sustained demand from military and law enforcement operations.

- Leading & Fastest-growing Ammunition Types: Small caliber ammunition is likely to lead by holding around 62% market revenue share in 2026, whereas large caliber ammunition is expected to to be the fastest-growing segment during the 2026-2033 forecast period.

- Leading & Fastest-growing End-Users: Military is poised to capture approximately 60% of the market revenue share in 2026, with civilian experiencing the fastest growth over the 2026-2033 forecast period.

| Key Insights | Details |

|---|---|

|

Latin America Ammunition Market Size (2026E) |

US$ 674.0 Mn |

|

Market Value Forecast (2033F) |

US$ 795.0 Mn |

|

Projected Growth (CAGR 2026 to 2033) |

2.4% |

|

Historical Market Growth (CAGR 2020 to 2025) |

2.5% |

DRO Analysis

Rising Defense Budgets and Military Modernization

Latin American governments are increasingly raising their defense budgets in response to a combination of regional security challenges, territorial disagreements, and ongoing counter-insurgency operations. This strategic focus is driving the modernization of military forces and encouraging countries to secure reliable ammunition supplies. Nations such as Brazil, Colombia, and Mexico are actively investing in comprehensive programs that strengthen their domestic production and stockpiling of both small-caliber and large-caliber ammunition. By prioritizing self-sufficiency, these countries are ensuring that their armed forces remain prepared for a variety of operational scenarios, from border security to internal stability missions.

The emphasis on local production is also creating a steady and predictable demand for ammunition, which enables manufacturers to plan expansions and improve production capabilities with confidence. This proactive approach reflects a broader recognition that regional security pressures are ongoing and require long-term investment in military readiness and supply chain resilience. This trend is fostering a more stable environment for defense industry growth, with predictable demand allowing companies to innovate and develop specialized ammunition variants to meet diverse operational needs. As governments continue implementing modernization programs, manufacturers are incentivized to expand capacity, enhance technology, and optimize production processes.

Escalating Law Enforcement and Public Safety Procurement

Latin American countries are facing persistent challenges related to organized crime, drug trafficking, and rising urban violence, and governments are continuously strengthening their law enforcement systems to address these threats. Authorities are expanding police forces, improving training frameworks, and increasing operational budgets to ensure effective response capabilities. Institutions such as the United Nations Office on Drugs and Crime (UNODC) are highlighting the severity of these security concerns, which is prompting governments to treat public safety as a critical priority. Brazil, Mexico, Colombia, and Peru are actively reinforcing federal and state-level policing units to maintain order and deter criminal activity.

This ongoing focus is driving consistent procurement of ammunition to support daily operations, tactical missions, and emergency responses. Law enforcement agencies are ensuring that personnel remain well-equipped, which is strengthening their readiness and improving their ability to respond to evolving security risks across both urban and rural environments. Governments are entering long-term procurement agreements to secure a stable supply of ammunition and reduce the risk of shortages. These multi-year contracts are enabling better financial planning and ensuring uninterrupted operational support for law enforcement agencies. Even during periods of fiscal adjustment, spending on public safety is remaining protected, as governments are recognizing its direct impact on social stability and economic confidence.

Stringent Regulatory Frameworks and Import Controls

The Latin America ammunition market is operating within strict and complex regulatory frameworks that are shaping how manufacturers and distributors conduct business. Governments across the region are enforcing detailed licensing systems, compliance requirements, and approval procedures for the import, export, and domestic distribution of ammunition. These processes are increasing administrative responsibilities and extending approval timelines, which is affecting operational efficiency. Companies are continuously aligning their operations with these evolving regulations to maintain legal compliance and avoid disruptions. This environment is encouraging firms to invest in compliance infrastructure and develop strong relationships with regulatory authorities to ensure smoother market participation.

Regulatory uncertainty is influencing demand patterns, particularly in relation to civilian access policies. Governments are frequently reviewing and adjusting regulations, which is creating fluctuations in market demand and complicating long-term planning for manufacturers. Policy changes are directly impacting the size of the accessible market and are forcing companies to remain flexible in their production and distribution strategies. Multinational firms are carefully evaluating these risks while planning regional expansion, as sudden regulatory shifts may affect supply chain continuity and investment decisions. Companies are prioritizing risk management, local partnerships, and adaptive business models to navigate this evolving regulatory landscape while sustaining growth opportunities.

Global Trade Barriers and Sanctions

Embargoes and arms control agreements are increasingly shaping the ammunition market by restricting cross-border trade and limiting access to international suppliers. Governments and international bodies are enforcing strict controls on the import and export of ammunition to prevent illicit trafficking and enhance regional security. These measures are requiring manufacturers and distributors to follow detailed approval processes and comply with evolving legal standards. Companies are facing delays in shipments and higher compliance costs, which are affecting their ability to operate efficiently. Export restrictions from supplier countries are also reducing the availability of certain ammunition types, which is pushing buyers to seek alternative sources or strengthen domestic production capabilities.

Diplomatic tensions and geopolitical developments are influencing trade stability across the region. Conflicts and shifting alliances are leading to sanctions and policy restrictions that are disrupting established trade routes. These disruptions are creating uncertainty for businesses that rely on consistent international supply networks. Companies are continuously adjusting procurement strategies to manage these risks and ensure uninterrupted access to critical materials. Governments are also reassessing their defense and security priorities, which is influencing procurement decisions and market demand.

Adoption of Non-Toxic and Technologically Advanced Ammunition

Environmental regulations and public health priorities are increasingly influencing ammunition preferences across Latin America. Governments and regulatory bodies are encouraging the use of safer alternatives to traditional lead-based products to reduce environmental contamination and health risks. This shift is prompting manufacturers to develop non-toxic ammunition that meets stricter safety standards while maintaining performance. Law enforcement agencies are actively evaluating these alternatives as they are aiming to align with global environmental practices and protect personnel from long-term exposure to harmful materials. The growing awareness of occupational health risks is strengthening the case for cleaner ammunition solutions across training and operational use.

This transition is creating new opportunities for innovation and premium product positioning. Manufacturers are investing in materials such as bismuth, tungsten, and polymer compounds to produce high-performance, non-toxic projectiles. These solutions are offering improved durability and reduced environmental impact, which is attracting interest from both public and private sector buyers. Companies are also focusing on technology differentiation to gain a competitive advantage in a market that is evolving under regulatory pressure. As adoption continues, suppliers that are prioritizing research and development are likely to strengthen their market presence and establish leadership in environmentally responsible ammunition solutions.

Domestic Manufacturing Incentives and Import Substitution Policies

Several Latin American governments are actively strengthening their domestic defense industrial base as part of broader economic sovereignty strategies. Countries are prioritizing local manufacturing to reduce reliance on external suppliers and improve supply chain security. In Brazil, institutions such as Empresa Gerencial de Projetos Navais (EMGEPRON) are supporting this transition by promoting procurement policies that favor domestically produced ammunition. The Ministry of Defense (MoD) is also encouraging national production through structured policy frameworks and industrial support initiatives. These efforts are creating a more favorable environment for local manufacturers, as governments are aligning procurement decisions with long-term national interests.

Import substitution strategies are opening new growth opportunities for manufacturers willing to invest in regional production. Companies are establishing local facilities to benefit from government incentives, preferential tariffs, and stable supply agreements. These advantages are helping firms secure consistent demand and build long-term relationships with public sector buyers. By focusing on local capacity development, manufacturers are positioning themselves to replace imported products and capture a larger share of the market. This shift is also encouraging technology transfer, workforce development, and industrial innovation within the region.

Category-wise Analysis

Ammunition Type Insights

Small caliber is anticipated to dominate, commanding nearly 62% of the Latin America ammunition market revenue share in 2026. This dominance is resulting from the widespread use of ammunition across key weapon platforms such as handguns, rifles, and submachine guns, which are commonly deployed by military and law enforcement agencies across Latin America. Governments and security forces are continuously procuring large volumes to maintain operational readiness and ensure consistent supply. High-volume contracts from national police units, armed forces, and an expanding civilian firearms segment are sustaining recurring demand. Common calibers such as 9mm, .40 Smith & Wesson (S&W), 5.56x45mm, and 7.62x51mm are remaining essential due to their versatility and standardized use across multiple applications.

Large caliber ammunition is likely to be the fastest-growing segment during the 2026-2033 forecast period. This growth is being driven by ongoing military modernization programs in countries such as Brazil, Colombia, and Chile, where governments are upgrading armored vehicles, artillery systems, and naval platforms. These developments are increasing the need for compatible ammunition and strengthening demand for heavy munitions. Governments are also expanding strategic reserves in response to evolving geopolitical conditions. Investment in domestic production is improving supply security, while offering manufacturers higher margins and long-term defense partnerships despite high capital and compliance requirements.

End-User Insights

Military is projected to claim roughly 60% of the market revenue share in 2026, as armed forces are maintaining continuous requirements for training, operations, and reserve stockpiles. Countries such as Brazil, Mexico, and Colombia are driving major procurement activity through structured and long-term purchasing programs. These procurement cycles are creating stable demand and favoring established suppliers with proven capabilities. Governments are relying on direct contracts, state-owned enterprises, and competitive tenders to secure supply. The adoption of advanced weapons systems is increasing demand for specialized, higher-value ammunition, which is supporting sustained growth in military procurement.

Civilian is expected to be the fastest-growing segment over the 2026-2033 forecast period, driven by the rising popularity of recreational shooting sports, growing participation in hunting activities, and consistent requirements from private security and law enforcement support roles. Civilian users are increasingly engaging in sport shooting and firearm training, which is sustaining regular consumption of ammunition across common calibers. In several countries, regulatory frameworks are allowing controlled civilian ownership, which is further supporting market expansion. This trend is encouraging retailers and manufacturers to focus on accessible, reliable, and cost-effective ammunition solutions tailored to civilian needs.

Country Insights

Brazil Ammunition Market Trends

At approximately 45%, Brazil is anticipated to dominate the Latin America ammunition market share in 2026, powered by a strong combination of military, law enforcement, and civilian demand. The country is maintaining one of the region’s most extensive armed forces and a well-developed policing structure, which is continuously driving ammunition procurement. The civilian firearms segment is expanding, supported by increased participation in sport shooting and personal security activities. The government is allocating consistent resources toward defense readiness while also strengthening domestic manufacturing capabilities. This approach is ensuring steady demand across multiple user segments and reinforcing Brazil’s position as a central market within the region.

The domestic production ecosystem is evolving under the leadership of Indústria de Material Bélico do Brasil (IMBEL) and Companhia Brasileira de Cartuchos (CBC), both of which are advancing local manufacturing strength and technological capability. Government policies are promoting import substitution and encouraging companies to expand production capacity within the country. Export opportunities are also increasing, as manufacturers are supplying neighboring markets and selected global destinations. Regulatory changes are shaping civilian demand, and although policies are shifting, the existing base of firearm users is continuing to sustain consumption. The competitive landscape is encouraging innovation, particularly in non-toxic ammunition and advanced production methods, which is supporting long-term industry growth.

Mexico Ammunition Market Trends

Mexico is expected to be the fastest-growing country in the Latin America ammunition market, driven mainly by sustained demand from military and law enforcement operations. The country is continuing to strengthen its internal security framework in response to organized crime, border control challenges, and national safety priorities. Institutions such as the Secretariat of National Defense (SEDENA) and the Guardia Nacional (GN) are leading large-scale procurement efforts through structured and multi-year contracts. These organizations are ensuring continuous supply to support counter-narcotics missions and public security operations. Government demand is remaining the primary force shaping market activity, while civilian participation is staying limited due to strict regulatory controls.

Mexico is relying heavily on imported ammunition due to limited domestic production capacity. Facilities such as Fábrica de Armas y Cartuchos (FAYCA) are supporting local manufacturing, but they are not fully meeting national requirements. This gap is creating opportunities for international suppliers, especially those with strong logistical networks and established defense relationships. The government is gradually encouraging local production through policy support, aiming to reduce external dependence and improve supply security. The competitive landscape is favoring experienced global manufacturers, particularly those from nearby regions, as they are benefiting from geographic proximity and long-standing partnerships with national defense institutions.

Competitive Landscape

The Latin America ammunition market structure is moderately consolidated, dominated by leading players such as CBC, IMBEL, Vista Outdoor Inc., and FAYCA. These players collectively capture 45-55% of the market share. The market reflecting a relatively concentrated competitive structure. These leading companies are leveraging strong production capabilities, established distribution networks, and long-term government contracts to maintain their positions.

The remaining market share is being distributed among mid-tier domestic manufacturers, specialized producers, and importers that are serving niche requirements. These smaller participants are focusing on specific calibers, customized solutions, and regional demand gaps, which is allowing them to compete effectively despite the dominance of larger, well-established industry leaders.

Key Industry Developments

- In March 2026, Brazilian ammunition manufacturer CBC signed an agreement with the Brazilian Navy to develop and test domestically produced ammunition for new Tamandaré-class frigates, aiming to reduce reliance on foreign suppliers. The collaboration supports national defense self-sufficiency by aligning locally built warships with indigenous ammunition production, strengthening Brazil’s military and strategic capabilities.

- In July 2025, Venezuela inaugurated Latin America's first Kalashnikov ammunition plant in Maracay, producing 7.62×39mm cartridges including steel-core, tracer, and blank rounds for AK-103 rifles used by its military and police. Built by Russia's Rosoboronexport on state-owned Cavim grounds despite Western sanctions and delays, the facility aims for 70 million cartridges annually to cut import reliance.

Companies Covered in Latin America Ammunition Market

- CBC

- IMBEL

- Vista Outdoor Inc.

- Northrop Grumman Corporation

- Nammo AS

- Rheinmetall AG

- FAYCA

- General Dynamics Ordnance & Tactical Systems

- BAE Systems plc

- Denel Munitions

- Poongsan Corporation

- Sellier & Bellot

- Indumil

- Fiocchi Munizioni SpA

Frequently Asked Questions

The Latin America ammunition market is projected to reach US$ 674.0 million in 2026.

Military modernization and rising civilian demand for sporting firearms are propelling market growth.

The market is poised to witness a CAGR of 2.4% from 2026 to 2033.

Key opportunities lie in domestic manufacturing expansion and the growing civilian sporting sector.

CBC, IMBEL, Vista Outdoor Inc., and FAYCA are some of the key players in the market.