- Food Ingredients & Additives

- Gelatin and Gelatin Derivatives Market

Gelatin and Gelatin Derivatives Market Size, Share, and Growth Forecast, 2025 - 2032

Gelatin and Gelatin Derivatives Market by Source Type (Animal-based Gelatin, Plant-based Gelatin, Microbial Gelatin, Others), Form Type (Powder, Sheet, Granules, Capsules, Others), Function Type (Gelling Agent, Stabilizing Agent, Thickening Agent, Emulsifier, Others), Application Type, and Regional Analysis for 2025 - 2032

Gelatin and Gelatin Derivatives Market Size and Trend Analysis

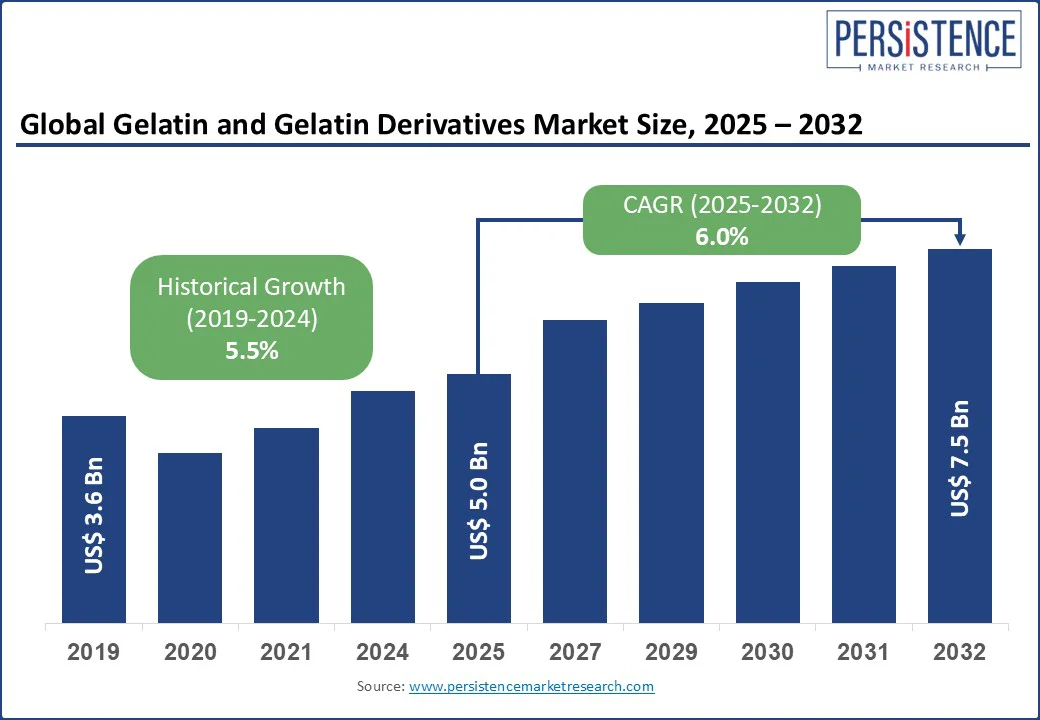

The global Gelatin and Gelatin Derivatives Market is likely to be valued at US$ 5.0 Bn in 2025 and is estimated to reach US$ 7.5 Bn in 2032, growing at a CAGR of 6.0% during the forecast period from 2025 to 2032.

This growth is fueled by its versatile applications in food processing, pharmaceutical formulations, and cosmetic products within the gelatin market trends. Gelatin, a protein derived primarily from collagen in animal tissues, serves as a gelling, stabilizing, and thickening agent, while its derivatives enhance functionality in specialized uses in the gelatin and gelatin derivatives market

Key Industry Highlights

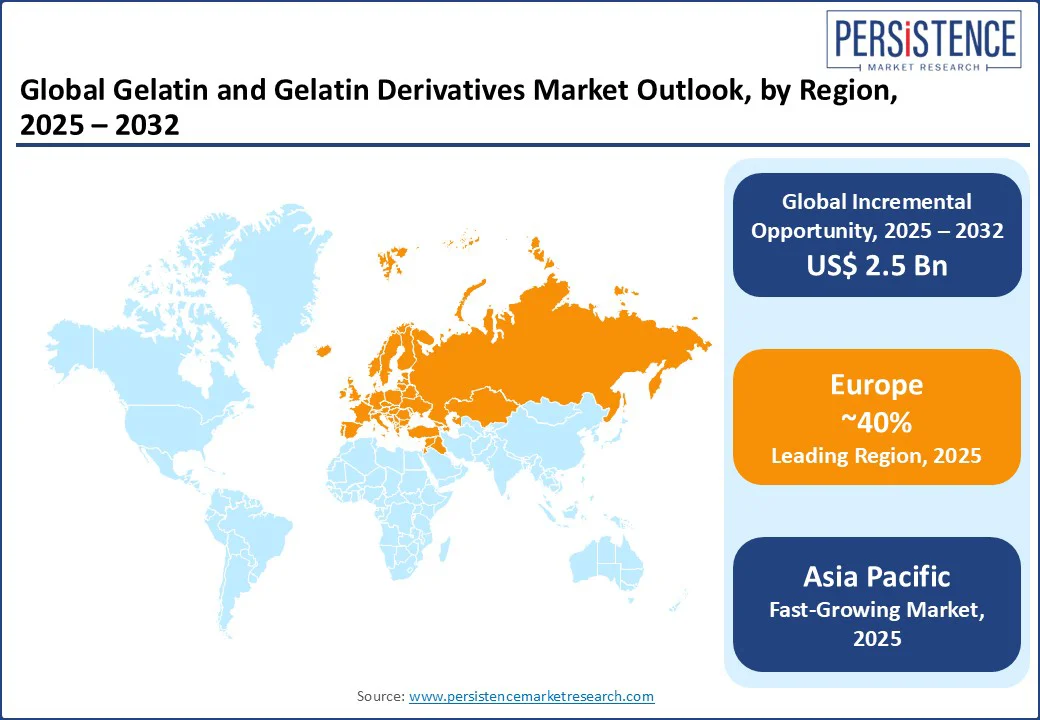

- Leading Region: Europe dominates the gelatin and gelatin derivatives market with a 35% share in 2025, driven by strict food safety regulations such as the EU Novel Foods Regulation and significant demand from the confectionery sector. In this industry, gelatin helps major manufacturers reduce production costs by 15-20%, strengthening its market position.

- Fastest-Growing Region: The Asia Pacific region is expected to grow at a robust CAGR through 2032, propelled by rapid urbanization, increasing disposable incomes in countries such as India and China, and government programs promoting nutritional fortification. Gelatin plays a crucial role in addressing protein deficiencies affecting nearly 20% of the population, boosting market growth.

- Dominant Source Type: Animal-based gelatin holds over 70% market share due to its excellent gelling properties and cost-effectiveness, with prices typically below $5/kg for bovine gelatin. This makes it the preferred choice for large-scale food production in the gelatin derivatives industry.

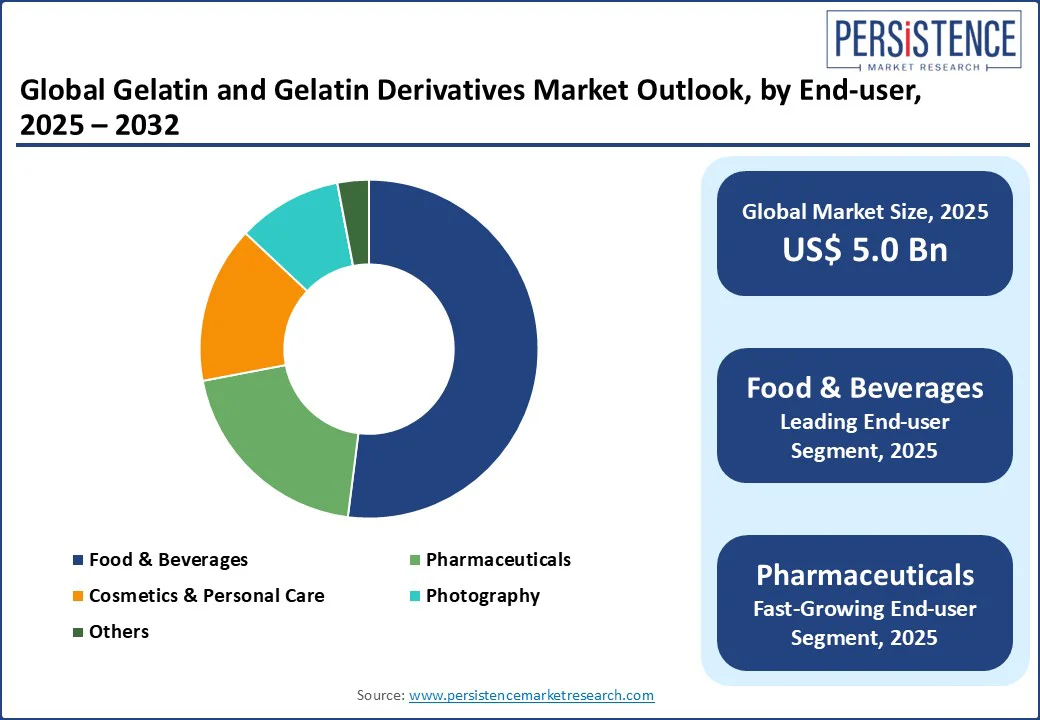

- Leading Application: The food and beverages segment accounts for 50% of the Gelatin and Gelatin Derivatives market revenue, as gelatin improves texture and stability in products such as gummies. This aligns with the global confectionery market, which generates over $200 Bn annually, underscoring gelatin’s critical role in this sector.

|

Global Market Attribute |

Key Insights |

|

Gelatin and Gelatin Derivatives Market Size (2025E) |

US$ 5.0 Bn |

|

Market Value Forecast (2032F) |

US$ 7.5 Bn |

|

Projected Growth (CAGR 2025 to 2032) |

6.0% |

|

Historical Market Growth (CAGR 2019 to 2024) |

5.5% |

Market Dynamics

Driver: Growing Demand for Convenient and Functional Foods

The global shift toward busy lifestyles and on-the-go consumption has significantly increased the demand for convenient and functional foods. Consumers are seeking products that combine ease of preparation with added health benefits, such as improved digestion, immunity support, or enhanced nutrition. Gelatin in functional foods plays a vital role as a gelling, stabilizing, and encapsulating agent in fortified snacks, protein gummies, and ready-to-eat desserts. This trend is accelerating as urbanization and higher disposable incomes fuel interest in packaged foods that deliver both taste and health benefits.

Government nutrition initiatives are also supporting this growth. For instance, the U.S. Department of Agriculture (USDA) highlights that functional foods enriched with protein, vitamins, and minerals help address nutrient gaps in the population, especially among children and the elderly. This alignment of consumer preferences with public health objectives is driving innovation and demand in gelatin-based functional food products.

Restraint: Cultural and Religious Restrictions

One of the significant barriers to the gelatin and gelatin derivatives market is the impact of cultural and religious restrictions. Traditional gelatin is primarily derived from bovine and porcine sources, making it unsuitable for certain religious groups, including Muslims, Jews, Hindus, and vegetarians. This limits its acceptance in key regions such as the Middle East, parts of Asia, and countries with large vegetarian populations. These restrictions affect applications across food & beverages, pharmaceuticals, and cosmetics, requiring manufacturers to seek alternative sources such as halal-certified gelatin, kosher gelatin, or plant-based gelatin.

The Pew Research Center reports that Muslims make up nearly 25% of the global population, highlighting the scale of dietary compliance needs. Similarly, India has over 500 Mn vegetarians, creating substantial demand for non-animal-derived gelatin. These factors are pushing the industry toward plant-based, fish-based, and microbial gelatin solutions, but such alternatives often come with higher production costs and functional challenges.

Opportunity: Plant-Based Alternatives and Sustainable

The rising consumer preference for ethical, eco-friendly, and dietary-compliant products is creating a strong growth opportunity for plant-based gelatin alternatives. Derived from sources such as agar-agar, carrageenan, and pectin, these options cater to vegan, vegetarian, halal, and kosher markets while addressing environmental concerns tied to livestock production. Growing awareness of sustainable sourcing in the gelatin market is also influencing purchasing decisions, with brands investing in traceable, low-carbon supply chains.

Industry demand is reinforced by changing regulations and market demographics. According to the United Nations, the global vegetarian and vegan population is steadily increasing, with plant-based food sales growing in double digits annually in several countries. In parallel, sustainable sourcing initiatives align with corporate ESG goals, reducing environmental impact and improving brand reputation. As production technologies improve, plant-based gelatin is closing the functionality gap with animal-based options, making it a high-potential segment in the global gelatin market.

Category-wise Insights

Source Type Insights

Animal-based gelatin dominates the gelatin and gelatin derivatives market, capturing approximately 72% market share. Derived mainly from bovine, porcine, and poultry sources, animal-based gelatin is extensively used due to its excellent gelling, stabilizing, and thickening properties. Its affordability and versatile applications across food & beverages, pharmaceuticals, and cosmetics reinforce its market dominance. The robust demand for animal gelatin is driven by its superior functional performance and widespread availability, making it the preferred choice for manufacturers globally.

Plant-based gelatin alternatives, such as agar-agar and carrageenan, are rapidly gaining traction amid rising veganism and clean-label trends. Though currently smaller in market share compared to animal gelatin, plant-based options are favored for their ethical appeal and suitability in specialized food and pharmaceutical applications. Increasing consumer preference for plant-derived ingredients is expected to boost their adoption and expand their market footprint over the coming years.

Form Type Insights

Powdered gelatin accounts for about 60% of the gelatin market, valued for its ease of use, long shelf life, and versatility. Powder form gelatin dissolves quickly and blends seamlessly in applications spanning confectionery, bakery, pharmaceuticals, and cosmetics. Its convenience in processing and dosage flexibility make it highly popular among manufacturers, solidifying its position as the dominant gelatin form in the global market.

Sheet gelatin holds a leading position in niche applications, especially in gourmet food industries such as confectionery and desserts. Sheets provide consistent gel strength and texture, favored by premium food producers for specialized recipes. Despite lower overall market share, sheet gelatin remains critical for applications demanding precision and uniformity in gel formation.

Function Type Insights

Gelling agents represent the largest function segment in the gelatin market, commanding roughly 40% market share. Gelatin’s unique ability to form thermo-reversible gels makes it indispensable in food products such as gummies, marshmallows, and dairy desserts. This functional property is also leveraged in pharmaceuticals and cosmetics to create stable, appealing textures. The gelling function continues to drive gelatin demand globally due to its essential role in product formulation.

Stabilizing agents are increasingly important as consumers demand improved texture and product shelf life. Gelatin’s stabilizing properties help maintain consistency in food and beverage products, preventing ingredient separation and enhancing mouthfeel. This function’s growing relevance positions stabilizing agents as a key leading segment alongside gelling in the gelatin derivatives market.

Application Type Insights

The food and beverages sector leads the gelatin market with a dominant 52% share, fueled by its widespread use in confectionery, dairy products, and processed foods. Gelatin imparts desirable texture, mouthfeel, and stability to a wide variety of consumables. Rising demand for convenience foods and functional ingredients further accelerates growth in this segment, making food and beverages the cornerstone application for gelatin and its derivatives.

Pharmaceutical applications are emerging as a significant growth driver, particularly in capsule and tablet manufacturing. Gelatin’s biocompatibility and excellent film-forming properties make it ideal for encapsulation and controlled release of drugs. Stringent quality requirements in pharmaceuticals ensure consistent gelatin demand, positioning this application as a leading segment in the evolving gelatin market landscape.

Regional Insights

North America Gelatin and Gelatin Derivatives Market Trends

North America holds a significant share of the gelatin and gelatin derivatives market, driven by the strong pharmaceutical industry and high consumption of processed and functional foods. The U.S. and Canada are major consumers of gelatin for drug delivery, nutraceuticals, and personal care products. Increasing consumer focus on health and wellness, coupled with strict regulatory compliance, promotes product innovation. Advanced research and development activities in gelatin applications further strengthen North America’s position as the leading regional market.

Europe Gelatin and Gelatin Derivatives Market Trends

Europe dominates the gelatin and gelatin derivatives market, holding around 40% share due to its well-established food processing, pharmaceutical, and cosmetics industries. Countries such as Germany, France, and Italy drive strong demand for gelatin in confectionery, dairy products, and pharmaceutical capsules. Europe’s stringent regulatory standards and rising consumer preference for clean-label, high-quality gelatin products further boost market growth. The presence of leading gelatin manufacturers and ongoing innovation in gelatin derivatives position Europe as a key region for gelatin market expansion.

Asia Pacific Gelatin and Gelatin Derivatives Market Trends

The Asia Pacific gelatin market is the fastest-growing globally, accounting for approximately 25% market share. Rapid urbanization, increasing disposable incomes, and expanding food and pharmaceutical sectors in China, India, Japan, and Southeast Asia fuel this growth. Rising demand for convenience foods, health supplements, and cosmetics is accelerating gelatin consumption. Additionally, growing awareness of plant-based gelatin alternatives and vegan-friendly products in the Asia Pacific supports market diversification, making it a hotspot for gelatin market growth and investment.

Competitive Landscape

The global gelatin and gelatin derivatives market is highly competitive, with both global leaders and regional players focusing on innovation, sustainability, and optimizing supply chains. Gelita AG and Rousselot dominate the industry with their extensive scale, while Nitta Gelatin Inc. holds a strong position in the Asian market. Other notable companies include PB Gelatins, Weishardt Group, Sterling Biotech, and India Gelatine & Chemicals Ltd.

Key Developments

- In May 2024, GELITA launched OptiBar, a collagen peptide for protein bars, targeting health-conscious consumers in Europe and North America.

- In March 2023, Darling Ingredients acquired Gelnex, enhancing gelatin production capacity in South America for global exports.

Companies Covered in Gelatin and Gelatin Derivatives Market

- Gelita AG (Germany)

- Rousselot

- PB Leiner (Tessenderlo Group, Belgium)

- Weishardt (SAS Gelatines Weishardt, France)

- Nitta Gelatin Inc. (Japan)

- Darling Ingredients Inc. (US)

- Lapi Gelatine S.p.a. (Italy)

- India Gelatine & Chemicals Ltd. (India)

- Narmada Gelatines Limited (India)

- Nippi Inc. (Japan)

- Trobas Gelatine B.V. (Netherlands)

- Sterling Biotech Ltd. (India)

- Others

Frequently Asked Questions

The gelatin market size is projected to reach US$ 5.0 Bn in 2025.

Rising pharmaceutical demand, increased health awareness, and a preference for natural ingredients are key drivers of growth in the gelatin market.

The gelatin market forecast is poised for a CAGR of 6.0% from 2025 to 2032.

Plant-based gelatin and microbial innovations for sustainable and vegan products.

Gelita AG, Rousselot, Nitta Gelatin Inc., and others are leading players.