- Industrial Machinery

- North and Latin America Water Pump Market

North and Latin America Water Pump Market Size, Share, and Growth Forecast, 2026 - 2033

North and Latin America Water Pump Market by Power Source (Electric Pumps, Engine-Driven Pumps.), Pump Outlet Size (Up to 1 Inch, 1-2 Inches, 2-4 Inches, 4-6 Inches, Above 6 Inches.), Volume Flow Rate (Up to 500 GPM, 500-1000 GPM, 1000-3000 GPM, Above 3000 GPM.), Pump Type (Centrifugal Pump, Positive Displacement Water Pump), Sales Channel (OEM, Aftermarket), End-user (Construction, Agriculture, Oil & Gas, Wastewater Treatment, Chemical, Mining, Power Generation, Food & Beverage) and Regional Analysis for 2026 - 2033

North and Latin America Water Pump Market Size and Trends Analysis

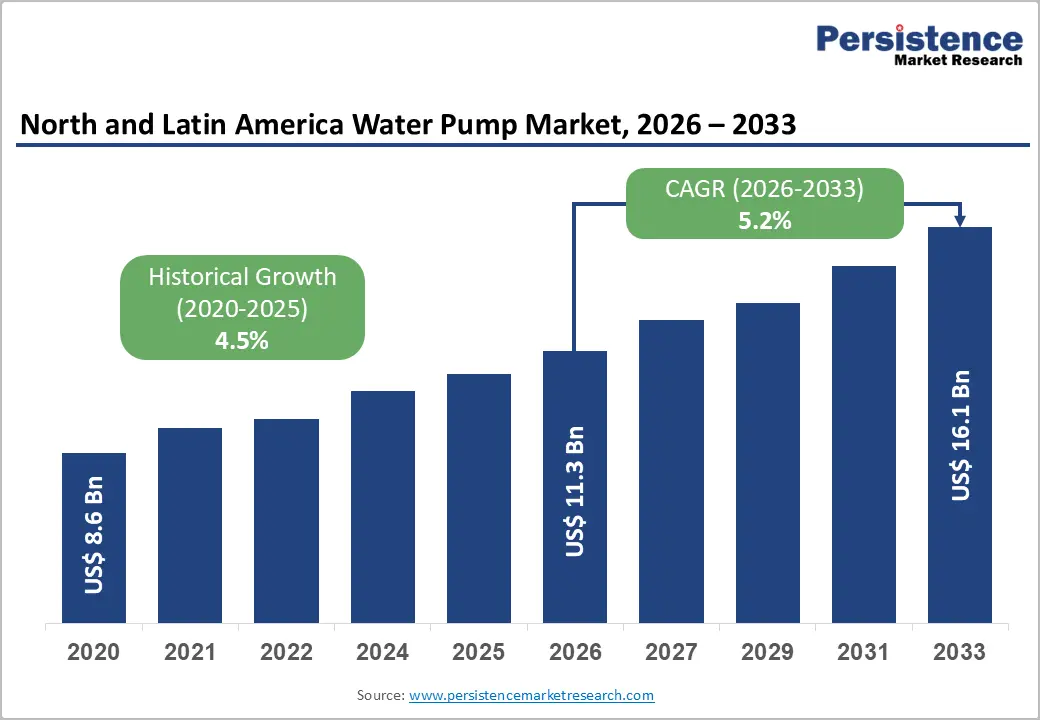

The North and Latin America water pump market is valued at US$11.3 billion in 2026 and is projected to reach US$ 16.1 billion by 2033, expanding at a CAGR of 5.2% during this forecast period. This accelerating growth trajectory, from a historical CAGR of 4.5% reflects structural demand tailwinds across municipal infrastructure modernisation, agricultural efficiency demands, and regulatory compliance imperatives.

The market's expansion is underpinned by substantial federal infrastructure investments in North America, climate-driven agricultural water demands across Latin America, and heightened regulatory requirements for water treatment and quality management. Centrifugal pumps maintain leadership through their versatility in municipal and industrial applications, whereas positive-displacement pumps exhibit the fastest growth trajectory, supported by specialised demands in chemical processing, oil & gas, and wastewater treatment. Electric pump-driven systems, reflecting electrification trends and energy efficiency mandates, are positioning energy-optimised solutions as critical competitive differentiators.

Key Industry Highlights:

- Leading Regional Market: The U.S. dominates the North and Latin America Water Pump Market, supported by federal infrastructure spending under IIJA and WIFIA, while Brazil, Mexico, and Argentina drive growth in Latin America through municipal, agricultural, and industrial projects.

- High-Value Leading Power Source: Electric pumps lead with 69.7% market share, backed by DOE efficiency mandates, declining electricity costs, and increasing adoption of VFD-based smart pumping solutions across municipal, agricultural, and industrial applications.

- Leading Pump Type: Centrifugal pumps remain dominant, with a 63.8% market share, driven by their versatility, reliability, and compatibility with municipal water and wastewater treatment systems and large-scale irrigation systems.

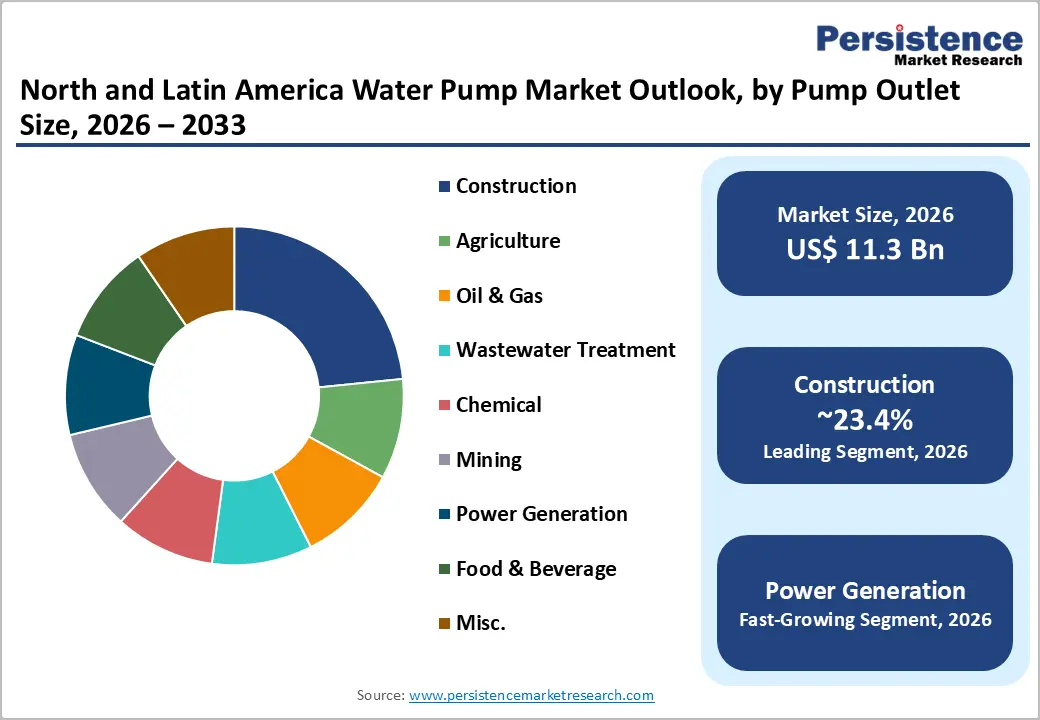

- Leading End-user: Construction is the largest end-use segment, accounting for 23.4% of the market, driven by residential and commercial building projects, infrastructure modernisation, and nearshoring investments in Latin America.

- Fastest-Growing End-user: Oil & gas applications represent the fastest-growing segment, driven by upstream exploration, midstream pipeline boosting, LNG facilities, and Latin American pre-salt and unconventional resource developments.

| Key Insights | Details |

|---|---|

| Water Pump Market Size (2026E) | US$ 11.3 Bn |

| Market Value Forecast (2033F) | US$ 14.0 Bn |

| Projected Growth (CAGR 2026 to 2033) | 5.2% |

| Historical Market Growth (CAGR 2020 to 2025) | 4.5% |

Market Dynamics

Drivers - Infrastructure Investment and Municipal Water System Modernization

The U.S. Bipartisan Infrastructure Investment and Jobs Act (IIJA) represents the most significant federal water infrastructure commitment in decades, allocating US$55 billion for water system rehabilitation and expansion. The American Society of Civil Engineers (ASCE) projects a water infrastructure investment gap of US$91 billion in 2024 alone, escalating to US$146 billion by 2043 if current spending levels remain constant. Within this context, the Water Pump Market serves as a critical capital equipment segment supporting the replacement and upgrade of ageing municipal water delivery and treatment networks.

The EPA's Water Infrastructure Finance and Innovation Act (WIFIA) programme complements direct appropriations by facilitating large-scale municipal projects across treatment plants, distribution systems, and pumping stations. In Latin America, major infrastructure initiatives underscore comparable demand momentum: Brazil's Ramal do Agreste water transmission project, delivering water to 70 municipalities and benefiting 2.2 million residents, deployed advanced centrifugal pump systems, while Argentina's Riachuelo wastewater treatment complex the largest pretreatment initiative in the region installed inlet and outlet pumping stations with capacities reaching 36 m³/s and 27 m³/s, serving over 4.3 million residents. These capital-intensive infrastructure programmes establish sustained demand for industrial-grade pumping solutions across municipal and regional water authorities.

Agricultural Water Demand and Climate-Driven Irrigation Requirement

Agricultural production consumes 70 percent of global freshwater withdrawal and 74 percent of total water extraction in Latin America and the Caribbean. Within this region, irrigation potential is estimated at 77.8 million hectares, with 66 percent concentrated in Argentina, Brazil, Mexico, and Peru, which experience pronounced water scarcity pressures. UNESCO's Platform on Climate Change, Agriculture and Water in Latin America and the Caribbean (PLACA) identifies the adoption of efficient irrigation technologies as a critical adaptation strategy, estimating that between 50 percent and 70 percent of extracted water is wasted through evaporation, leaks, and inefficient delivery systems.

The World Economic Forum and Inter-American Development Bank emphasise that water security represents a fundamental economic development constraint, as the region's 80 percent urban population and projected 784 million inhabitants by 2050 will intensify competition between agricultural and domestic water demands. Climate change amplifies this dynamic: Argentina, Peru, and northern Mexico face persistent drought conditions, exemplified by grassroots initiatives in December 2024 by Engineering Without Borders Argentina, which deployed manual pumps and 16,000-litre rainwater-harvesting systems in drought-affected villages. These conditions necessitate adopting energy-efficient irrigation pumping solutions, including centrifugal pumps for large-scale gravity-fed systems and positive-displacement pumps for precision drip-irrigation applications. This segment represents substantial incremental demand for the Water Pump Market across agricultural subsectors, including field irrigation, groundwater extraction, and water storage and distribution infrastructure.

Restraint- Regulatory Complexity and Compliance Cost Burden

Manufacturers and distributors within the North American Water Pump Market face escalating regulatory complexity stemming from federal EPA standards, state-level environmental regulations, and municipal-specific requirements. The U.S. Department of Energy pump efficiency standards, taking effect in 2020 and subsequently enhanced, mandate that all commercial pump designs exceed baseline efficiency thresholds, necessitating substantial R&D investments in hydraulic optimisation and advanced materials.

The proliferation of emerging regulations, including PFAS drinking water standards, revised Lead and Copper Rule compliance thresholds, stormwater management mandates, and state-specific contaminant monitoring requirements, fragments the market into specialised application niches requiring customised pump solutions. Utilities and industrial operators must navigate multi-layered compliance frameworks that vary by jurisdiction, delaying capital procurement timelines and creating uncertainty in demand forecasting. These regulatory burdens particularly impact smaller manufacturers lacking resources for extensive product certification and testing, concentrating market share among multinational corporations capable of absorbing compliance costs.

Opportunities - Energy-Efficient Pump Technology and IoT Integration

Regulatory mandates for energy efficiency, coupled with rising electricity costs, create substantial market opportunities for variable-frequency drive (VFD)-equipped centrifugal pumps and smart pump solutions that offer real-time performance monitoring. The U.S. Department of Energy efficiency standards implemented in 2020 exceed baseline hydraulic performance requirements, incentivizing adoption of advanced pump geometries and materials engineering. Pentair's September 2024 launch of upgraded Aurora and Fairbanks Nijhuis end-suction and vertical in-line pump series exemplifies this innovation trajectory, combining DOE-compliant hydraulics with shared component architectures, stainless steel impellers, and ductile iron castings to reduce lifecycle costs and maintenance complexity.

IoT-enabled monitoring solutions that offer predictive maintenance, energy consumption analytics, and remote performance diagnostics create opportunities for differentiation for Original Equipment Manufacturers and aftermarket service providers. Municipal water authorities seeking to optimise energy expenditures amid budget constraints represent a substantial customer segment for these technology-enabled solutions.

Brazilian and Mexican water utilities, under modernisation pressures and facing electricity cost inflation, demonstrate particular receptivity to smart pump deployments offering 15 to 30 percent energy consumption reductions compared to conventional systems. Grundfos' August 2024 expansion of its SP 18 submersible pump across the India, Middle East, Africa, and Central Asia (IMEA) region addresses these efficiency and reliability requirements, positioning optimised hydraulics and lower long-term operational costs as core value propositions for agricultural and municipal end-users.

Geographic Expansion in Emerging Markets and Nearshoring Dynamics

Strategic facility investments and regional representative appointments by multinational pump manufacturers signal accelerating market penetration across underserved Latin American geographies. SIMFLO's July 2025 Latin American expansion, which appoints a dedicated sales manager for Mining and Oil & Gas applications across Chile, Argentina, and Peru, reflects the momentum of rising commodity production and infrastructure development in the Andean region. Concurrently, Pleuger's November 2025 partnership with Tecnium, as an authorised representative for Brazil, enhances access to submersible pump and motor solutions for energy, water, and mining applications, strengthening localised engineering support and reducing delivery timelines for industrial customers. Sulzer's June 2025 opening of a third service facility in Ezeiza, Argentina, expanding existing operations in La Plata and complementing Brazilian operations in Jundiaí establishes Latin America as a strategic manufacturing and service hub for the organisation's global pump and turbomachinery portfolio.

These geographic expansions capitalise on rising capital formation and infrastructure investment across Latin America. Argentina, despite recent macroeconomic volatility, continues to face substantial requirements for modernising water and sanitation infrastructure. Brazil's agricultural sector expansion and municipal water security initiatives continue to drive multibillion-dollar capital allocation.

Mexico's nearshoring momentum, which is attracting data center investments requiring advanced liquid-cooling systems, creates incremental demand for specialised submersible and sealed-cavity pump designs. Peru and Chile's recovery of the mining sector, coupled with stringent environmental compliance regimes, necessitates advanced dewatering and fluid-handling pump solutions. The Water Pump Market within this geographic expansion context represents a core enabling technology for infrastructure modernisation and industrial development strategies, positioning manufacturers with established regional presence and localised manufacturing capacity as preferred partners for capital-intensive municipal and industrial projects.

Category-wise Analysis

Power Source Insights

Electric pumps, accounting for 69.7% of the North and Latin American water pump market, dominate the market, reflecting regulatory electrification mandates, declining electricity costs in select markets, and the technological maturity of electric motor-pump integration. Electric pumps deliver superior energy efficiency compared to engine-driven alternatives, particularly when powered by renewable energy or grid electricity subject to energy-efficiency standards. Municipal water authorities increasingly mandate electric systems for new installations and infrastructure modernisation projects, supported by federal programmes and environmental compliance requirements.

Electric pump prevalence is particularly pronounced in wastewater treatment, where continuous operation and variable flow requirements optimise the total cost of ownership relative to engine-driven alternatives. North American utilities benefit from mature electrical grid infrastructure, predictable utility pricing, and established supply chains for electric pump components, solidifying electric pump market leadership across the region.

In Latin America, adoption of electric pumps is accelerating as agricultural producers and small municipalities gain access to reliable grid electricity or alternative energy sources. Brazil's hydroelectric capacity and Mexico's solar energy expansion improve electric pump economics relative to diesel alternatives, particularly for operational expense-sensitive applications including irrigation and municipal water supply. Franklin Electric's October 2024 facility realignment in Abernathy, Texas, consolidates engineered systems with electric-driven configured solutions, reflecting strategic capital allocation toward electric pump-based offerings and aftermarket services supporting commercial, industrial, and municipal customers.

Pump Type Insights

Centrifugal pumps remain dominant, accounting for 63.8% of the North and Latin America water pump market in 2026, driven by their versatility, reliability, and suitability for high-volume, moderate-to-low-pressure applications typical of municipal water supply, wastewater treatment, and large-scale irrigation systems. These pumps excel at handling clear fluids and moderate solids concentrations, making them ideal for treated water distribution and primary-stage wastewater applications.

The technology's maturity, coupled with standardised component architectures and robust aftermarket support infrastructure, establishes centrifugal pumps as the default technology for municipal water authorities conducting infrastructure modernisation. Sulzer's January 2022 launch of SES and Positive Displacement Pumps Water Pump segments market leader Sulzer's SES and SKS pump ranges, specifically designed for municipalities, water treatment facilities, and irrigation applications, exemplify centrifugal pump innovation supporting efficiency, reliability, and cost-effectiveness across the Water Pump Market. The North American municipal sector, characterised by mature water infrastructure requiring replacement and upgrade, creates stable, recurring centrifugal pump demand across distribution network expansions, treatment plant upgrades, and booster station installations.

End-user Insights

Construction applications represent the largest end-use category within the North and Latin America Water Pump Market, commanding 23.4% market share in 2026, driven by the U.S. construction industry's $2.2 trillion annual spending and 1.6 million new homes built in 2024, coupled with Latin America's surge in infrastructure, commercial development, and residential construction. Construction pumping applications include temporary site dewatering, concrete washout fluid management, and water supply for construction processes. The South American construction industry, while navigating political transitions and macroeconomic uncertainty, continues benefiting from nearshoring dynamics, attracting data center, life sciences manufacturing, and hospitality investments.

Construction cost inflation in South America, which declined from 4.3% in 2023 to a projected 3.9% in 2024, maintains the region's cost competitiveness and supports momentum for capital project initiation. The Water Pump Market benefits from this construction cycle through incremental demand for dewatering, dust control, and temporary water supply pump systems deployed across residential, commercial, and infrastructure projects.

The oil & gas sector emerges as the fastest-growing end-use segment within the Water Pump Market, driven by expanding exploration and production activities, unconventional resource development, and infrastructure modernisation across North America and select Latin American regions. Oil & gas pumping applications encompass upstream operations (well dewatering, artificial lift, injection), midstream (pipeline boosting, compression, liquefied natural gas terminals), and downstream

In Latin America, Mexico's oil & gas sector modernisation, coupled with renewed exploration initiatives in the Gulf of Mexico and expanding natural gas infrastructure, is creating sustained pump demand. Brazil's pre-salt deepwater development and biofuels expansion require specialised submersible and high-pressure pump systems. Peru and Chile's mining sector recovery, while not strictly oil & gas, generates comparable demand for dewatering and water management pump solutions. SIMFLO's July 2025 appointment of a dedicated sales manager for Latin American Mining and Oil & Gas applications reflects the manufacturer's recognition of this accelerating segment. Flowserve's acquisition of cryogenic LNG pumps and ITT's US$11 million investment in testing facilities across Germany, India, and Saudi Arabia signal a strategic focus by multinational manufacturers on energy-sector pump innovations that address specialised pressure, temperature, and fluid-compatibility requirements.

Competitive Landscape

The North and Latin America water pump market exhibits a moderately consolidated competitive landscape, characterised by a mix of large North and Latin America OEMs with significant market share and numerous regional and niche specialists competing in specific end-use segments. Leading multinational players such as Xylem Inc., Flowserve Corporation, Grundfos, Ingersoll Rand Inc., Sulzer AG, and Wilo SE dominate the market through extensive distribution networks, broad product portfolios, and strong brand recognition across industrial, municipal, commercial, and residential water pumping applications. These established incumbents leverage strategic acquisitions, partnerships, and region-specific manufacturing investments to strengthen their market positions and respond to rising demand for energy-efficient, digitally enabled pumping solutions.

Smaller regional manufacturers and speciality technology providers retain meaningful presence in targeted niches such as dewatering, booster systems, wastewater handling, and submersible pumps, where local service responsiveness and customisation are valued. Competitive dynamics are also shaped by increasing regulatory emphasis on sustainability, water infrastructure modernisation, and energy usage standards, prompting players to innovate with smart, IoT-enabled, and high-efficiency products.

Key Developments:

- In July 2025, Sulzer has expanded its presence in Latin America with the opening of a third facility in Ezeiza, Argentina, strengthening its pump and turbomachinery service capabilities for key industries such as oil and gas, pulp and paper, power generation, and food and beverage. The 2,600 m² center enhances local engineering services and energy-efficient pump solutions, complementing Sulzer’s existing operations in La Plata, Buenos Aires, and Jundiaí, Brazil, while reflecting the company’s broader strategy to grow across Latin America.

- In June 2025, Fisia Italimpianti, in collaboration with the Webuild Group, commissioned Lot 2 of the Riachuelo wastewater treatment system in Buenos Aires, Argentina, marking the largest wastewater pretreatment project in Latin America. The lot features inlet and outlet pumping stations with capacities of 36 m³/s and 27 m³/s, enhancing sanitation services for over 4.3 million residents and contributing to the environmental recovery of the Río de la Plata.

Companies Covered in North and Latin America Water Pump Market

- Waste Management Inc.

- SUEZ Group

- Veolia Environment S.A.

- Biffa PLC

- Clean Harbors Inc.

- Covanta Holdings Corporation

- Hitachi Zosen Corporation

- Remondis AG & Co. Kg

- Republic Services Inc.

- Stericycle Inc.

- ALBA Group

Frequently Asked Questions

The North and Latin America Water Pump Market is projected to be valued at US$ 11.3 Bn in 2026.

The Electric Pump segment is expected to account for approximately 69.7% of the North and Latin America Water Pump Market by Processing Treatment in 2026.

The market is expected to witness a CAGR of 5.2% from 2026 to 2033.

The market growth in these regions is driven by large-scale infrastructure investment and municipal water system modernization in North America, coupled with rising agricultural water demand and climate-driven irrigation needs in Latin America.

Key market opportunities in the Water Pump Market lie in energy-efficient, IoT-enabled pump technologies for predictive maintenance and cost savings, alongside geographic expansion and nearshoring across underserved Latin American regions to support municipal, agricultural, and industrial infrastructure.

Key players in the Water Pump Market include Xylem Inc., Flowserve Corporation, Grundfos, Ingersoll Rand Inc., Sulzer AG, and Wilo SE.