- Specialty & Fine Chemicals

- Chelating Agents Market

Chelating Agents Market Size, Share, and Growth Forecast 2025 - 2032

Chelating Agents Market by Chemistry (Acetates, Phosphonates, Polyphosphates, Succinates, Sodium Gluconate, Citric Acid, Polyaspartic Acid, Catechol, Others), Product Type (Organic Chelating Agent, Inorganic Chelating Agent), Form (Powder/granules, Solution), Application (Cleaning & Detergents, Water Treatment, Pulp & Paper, Agrochemicals, Food & Beverage, Others), by Regional Analysis, 2025-2032

Chelating Agents Market Size and Trend Analysis

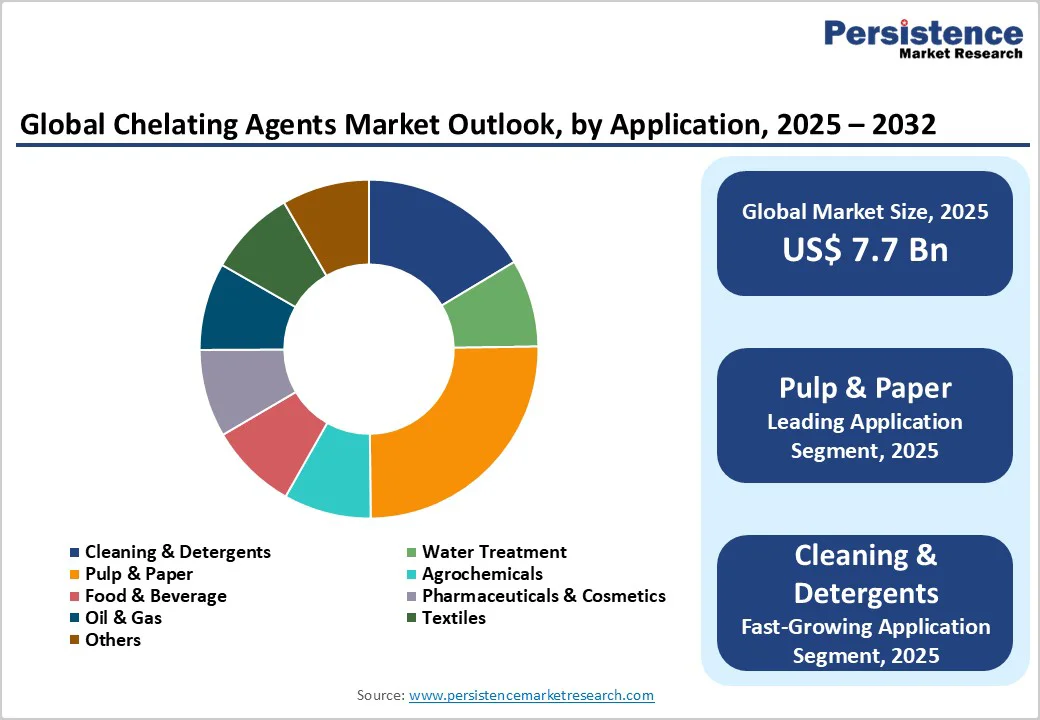

The global chelating agents market size is likely to be valued at US$ 7.7 Bn in 2025 and projected to reach US$ 11.7 Bn by 2032, growing at a CAGR of 6.1% between 2025 and 2032. This robust expansion is primarily attributed to the escalating demand for water treatment chemicals coupled with stringent environmental regulations mandating heavy metal removal from industrial effluents. The market is experiencing significant momentum from the pulp and paper industry where chelating agents enhance hydrogen peroxide bleaching efficiency, and from the cleaning and detergent sector where biodegradable formulations are replacing traditional phosphate-based products.

Key Market Highlights

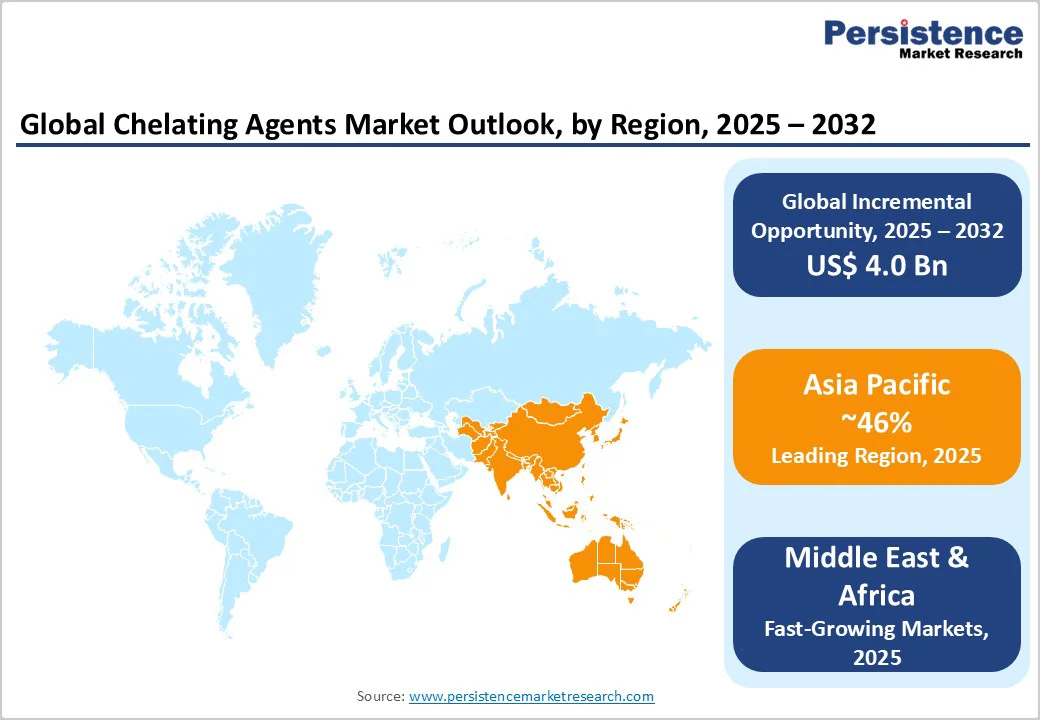

- Leading Region: Asia Pacific leads the global chelating agents market with 46% share in 2025, driven by China’s manufacturing, India’s agricultural growth, and Southeast Asia’s industrial and water treatment expansion.

- Fastest Growing Region: Middle East & Africa is forecasted to grow at a 7% CAGR through 2032, fueled by desalination, infrastructure development, localized cleaning production, and emerging pulp and paper investments.

- Dominant Segment: EDTA remains the most widely used chelating agent globally due to strong metal-binding, regulatory approvals, versatility across water treatment, cleaning, pulp and paper, agriculture, pharmaceuticals, and cosmetics.

- Fastest Growing Segment: Biodegradable organic chelating agents such as MGDA, GLDA, and EDDS are growing fastest, supported by environmental regulations, sustainability initiatives, eco-label preferences, and phosphate-free, low-toxicity formulation requirements.

- Key Market Opportunity: Agricultural chelated micronutrient fertilizers offer high growth potential as IDHA and HBED meet sustainability and regulatory standards, improving crop yields in alkaline soils across India, China, Middle East, and Latin America.

| Key Insights | Details |

|---|---|

|

Chelating Agents Market Size (2025E) |

US$ 7.7 Bn |

| Market Value Forecast (2032F) | US$ 11.7 Bn |

| Projected Growth CAGR (2025-2032) | 6.1% |

| Historical Market Growth (2019-2024) | 5.2% |

Market Dynamics

Market Growth Drivers

Stringent Water Treatment Regulations Driving Chelating Agent Adoption

Global initiatives to ensure water quality and manage industrial wastewater are significantly boosting chelating agent demand, supporting growth in the Water & Wastewater Treatment Chemicals Market. Regulatory authorities such as the U.S. EPA and China’s MEE have tightened discharge limits for heavy metals like lead, cadmium, copper, and mercury. China’s 2024 revised standards now require enhanced heavy metal removal in industrial wastewater, particularly in provinces such as Guangdong and Jiangsu, directly driving chelating agent consumption.

EDTA, DTPA, and biodegradable alternatives such as EDDS form stable water-soluble complexes, enabling removal through precipitation, ion exchange, and membrane filtration. Utilities depend on chelating agents to ensure compliance in aging pipelines and hard water zones, while the Middle East’s desalination sector increasingly incorporates these agents to prevent scaling and optimize membrane performance, sustaining demand for high-purity, environmentally compliant formulations.

Growing Demand for Biodegradable Chelating Agents in Cleaning Applications

Rising environmental awareness and regulatory measures in Europe and North America are fueling demand for biodegradable chelating agents in cleaning formulations, contributing to growth in the global detergent chemicals market, which is projected to reach US$ 83.8 billion at a CAGR of 4.8% by 2032.

Regulations such as EU REACH and Nordic Ecolabel standards prioritize eco-friendly, phosphate-free alternatives, prompting FMCG companies to reformulate products and replace conventional EDTA with MGDA and GLDA. BASF SE’s 2025 launch of Trilon G, with 56% renewable carbon content and over 60% biodegradation within 28 days, exemplifies this trend. Biodegradable chelating agents maintain metal-binding efficiency while supporting sustainability goals, enabling Ecolabel certifications, improving surfactant performance in hard water, preventing metal staining, and stabilizing bleaching compounds in detergents and industrial cleaners.

Market Restraints

Environmental Persistence and Ecotoxicological Concerns of Conventional Chelating Agents

Conventional chelating agents such as EDTA face market limitations due to environmental persistence and ecotoxicity. EDTA, widely used across industries, is poorly biodegradable and has been detected in European water bodies at up to 12 mg/L and in U.S. wastewater at 800 μg/L. It can remobilize heavy metals from sediments, posing risks to groundwater and aquatic ecosystems. High chelating agent concentrations interfere with metal removal processes, leaving toxic metals untreated. Regulatory scrutiny, especially in food, cosmetics, and agriculture, is increasing, and consumer resistance is growing. Developing biodegradable alternatives with comparable stability, metal-binding capacity, and cost-effectiveness remains challenging, creating barriers for new entrants and slowing the transition toward environmentally sustainable chelating solutions.

Declining Consumption of Phosphate-Based Builders Affecting Traditional Formulations

The shift away from phosphate-based detergent builders challenges the traditional chelating agent market. Historically, phosphates like STPP enhanced water softening, alkalinity, and soil suspension, complementing chelating agents. However, phosphate discharge causes eutrophication, prompting bans in the EU, Canada, and parts of the U.S. Manufacturers are switching to phosphate-free alternatives such as sodium carbonate, silicates, and zeolites, requiring reformulation of chelating systems. This transition introduces uncertainty in dosing, compatibility, and cleaning performance. R&D investment is needed for stability testing, validation, and regulatory approval, increasing costs and compressing margins. Coupled with declining per-capita detergent consumption in mature markets, these factors slow growth and constrain opportunities for conventional chelating agents.

Market Opportunities

Expanding Applications in Biodegradable Agricultural Chelated Micronutrients

The agricultural sector is emerging as a high?growth market for biodegradable chelating agents used in micronutrient fertilizers. Metals such as iron, zinc, copper, manganese, and magnesium often exist in soil forms inaccessible to crops. Chelating agents, including EDTA, DTPA, EDDHA, IDHA, HBED, and catechol, bind these metals to improve nutrient bioavailability across varying pH ranges, enhancing crop uptake and productivity. The catechol market is projected to grow to US$?0.2?bn by 2032, at a CAGR of 4.2% where agrochemicals account for 28.9% market share.

Environmental regulations and organic certification standards increasingly favor biodegradable alternatives like IDHA and HBED. Strategic moves, such as Nouryon’s acquisition of ADOB in Poland, expand manufacturing capacity and market reach. Government programs in India and trade requirements promoting bio?based inputs accelerate adoption. Growing awareness of micronutrient deficiencies, coupled with sustainability and regulatory alignment, positions biodegradable agricultural chelating agents, including catechol, as a premium, high?margin segment with long?term growth potential.

Technological Advancements in Pulp and Paper Bleaching Optimization

Chelating agents are critical in pulp and paper for enhancing bleaching efficiency, minimizing fiber damage, and reducing chemical consumption. Hydrogen peroxide bleaching is highly sensitive to transition metal contamination; metals like Fe²?, Mn²?, Cu²?, and Ni²? accelerate peroxide decomposition, leading to fiber weakening and chemical waste. EDTA, DTPA, and HEDTA sequester these ions, preserving peroxide efficacy, stabilizing brightness, and preventing oxalate scaling.

Modernization and sustainability initiatives are increasing chelating agent usage, especially in recycled fiber processing, which has higher metal ion content. Biodegradable and phosphonate-based alternatives compatible with closed-loop water systems are gaining traction. Suppliers like Kemira Oyj emphasize customized blends, technical services, and performance guarantees, creating opportunities for differentiation and premium product offerings in pulp and paper processing.

Category-wise Analysis

Chemistry Insights

EDTA dominates the global chelating agent market, capturing around 38% of consumption in 2023 due to its high metal-binding efficiency, stability across pH and temperature ranges, and broad regulatory acceptance, including FDA approvals. Its six functional groups enable effective sequestration of divalent and trivalent metal ions, preventing unwanted reactions, precipitation, and degradation.

EDTA is widely used in water treatment, pulp and paper, detergents, pharmaceuticals, cosmetics, and agriculture. In detergents, tetrasodium and disodium EDTA enhance performance in hard water, prevent staining, and stabilize bleach. In agriculture, EDTA-chelated micronutrients correct deficiencies in iron, zinc, and copper. Despite environmental persistence concerns, EDTA’s versatility, cost-effectiveness, and ongoing innovations in recovery and recycling technologies maintain its leadership position globally.

Product Type Insights

Organic chelating agents account for roughly 85% of global market volume in 2025, including aminopolycarboxylates (EDTA, DTPA, NTA, HEDTA), biodegradable options (MGDA, GLDA, EDDS, IDS), and natural alternatives (citric acid, sodium gluconate). Biodegradable organic agents are growing fastest, with projected CAGR above 6.5% through 2032, driven by regulatory pressures and sustainability commitments. EU REACH and Nordic Ecolabel standards favor chelating agents achieving ≥60% biodegradation within 28 days. Market leaders such as BASF and Nouryon offer GLDA- and MGDA-based products with renewable carbon content and excellent metal-binding performance. Biodegradable agents maintain stability across pH ranges, temperature tolerance, and enzyme compatibility, enabling phosphate-free, low-toxicity applications in cleaning, personal care, agriculture, and industrial formulations. Their regulatory compliance, reduced environmental impact, and brand differentiation make them the fastest-growing product type segment.

Application Insights

Pulp and paper dominates global chelating agent consumption with about 26% share in 2025. Chelating agents like EDTA and DTPA optimize chemical and mechanical pulp bleaching by sequestering transition metals that degrade hydrogen peroxide, preventing fiber damage, yellowing, and over-oxidation. Their use improves brightness by 3% ISO, reduces peroxide consumption by 12%, and lowers COD in effluents by 24%. TMP and CTMP producers rely on chelating agents to maintain high fiber yield and strength, essential for newsprint and magazine papers. Recycled fibers require more intensive chelation due to higher metal content. Suppliers like Kemira Oyj offer specialized formulations for deinking, bleaching optimization, and scale prevention. Mill modernization in Asia Pacific and increased recycled fiber use in Europe and North America ensure stable, predictable chelating agent demand for pulp and paper manufacturers.

Regional Insights

North America Chelating Agents Market Trends

North America’s chelating agents market is driven by advanced industrial applications, regulatory rigor, and mature end-use sectors demanding high-performance and sustainable solutions. The United States leads consumption, fueled by pulp and paper operations, modern water treatment infrastructure, and agriculture requiring micronutrient fertilizers. Municipal utilities in aging pipeline networks rely on chelating agents to manage lead, copper, and iron levels. Pulp and paper mills in the Pacific Northwest, Southeast, and Great Lakes use chelating agents for bleaching, mechanical pulp brightening, and recycled fiber processing.

Dow Inc.’s Versene brand exemplifies product innovation, serving water treatment, industrial cleaning, and agricultural applications. Innovation hubs in Massachusetts, California, and North Carolina support bio-based synthesis, dual-function formulations, and recycling technologies. Regulatory oversight, including EPA and FDA approvals, encourages investment in biodegradable agents. Consumer preference for eco-friendly home care products drives adoption of MGDA and GLDA, enabling sustainability claims and Ecolabel certifications. These factors collectively sustain demand for advanced chelating solutions across the region.

Europe Chelating Agents Market Trends

Europe’s market is defined by strict chemical regulations, sustainable chemistry leadership, and industrial demand aligned with environmental stewardship. The EU REACH regulation imposes comprehensive testing, risk assessment, and documentation requirements, favoring established suppliers with regulatory expertise. Germany leads consumption due to its chemical, automotive, metal processing, and paper industries, adopting biodegradable chelates such as BASF’s Trilon M and Trilon G, which meet OECD biodegradability standards. The UK, France, and Spain generate demand from water treatment modernization, agricultural micronutrient use, and cosmetic formulations. Nordic countries maintain high sustainability standards under the Nordic Ecolabel, influencing detergent and industrial cleaning product formulations. Nouryon’s Netherlands facility produces ISCC PLUS-certified chelates with renewable carbon content, serving regional markets. Pulp and paper operations in Scandinavia, Germany, and France adopt chelating agents for bleaching efficiency while minimizing environmental impact. Harmonized EU regulations facilitate cross-border trade, standardize safety, and enable cost efficiencies, supporting innovation, competitive pricing, and stable market growth throughout Europe.

Asia Pacific Chelating Agents Market Trends

Asia Pacific dominates global chelating agent consumption, representing roughly 46% of the market in 2025 due to industrialization, infrastructure development, and extensive agricultural production. China is the primary producer and consumer, supported by integrated chemical complexes, ethylene amine capacity, and cost-effective manufacturing. Stricter 2024 environmental regulations targeting heavy metal discharge in provinces like Guangdong and Jiangsu have accelerated adoption in wastewater treatment, electroplating, textile, and metal processing sectors. India shows rapid growth driven by agricultural modernization, urban water treatment demand, and textile industry requirements for bleaching and dyeing, with government programs promoting soil health and balanced fertilization raising awareness of chelated micronutrients. Japan and South Korea demand high-quality biodegradable chelating agents for industrial cleaning, paper processing, water treatment, and semiconductor applications. Southeast Asia—including Indonesia, Thailand, and Vietnam—presents emerging opportunities tied to industrial growth, agriculture, and evolving environmental standards, incentivizing suppliers to establish regional networks and provide localized technical support.

Competitive Landscape

The global chelating agents market is moderately consolidated, dominated by multinational chemical companies with broad product portfolios, global manufacturing, and integrated supply chains, alongside specialized regional producers. Leading players leverage economies of scale, R&D capabilities, and technical service support to develop biodegradable chelating agents such as MGDA, GLDA, and EDDS, addressing regulatory pressures and sustainability trends. Strategic initiatives include capacity expansion, mergers and acquisitions, and portfolio optimization to capture environmentally conscious market segments.

Key differentiators include biobased content, biodegradability certifications, regulatory compliance, superior metal-binding performance, and collaborative customer engagement for formulation support. Emerging trends involve multifunctional chelating agents, high-performance chelating polymers, and digital chemistry tools accelerating innovation and novel product development across industrial, agricultural, and water treatment applications.

Key Market Developments

April 2025: BASF SE launched Trilon G, a GLDA-based chelating agent for home care and industrial cleaning, featuring 56% renewable carbon content and >60% biodegradability per OECD 301D, enhancing sustainable cleaning performance.

January 2023: Nouryon acquired ADOB, a Polish chelated micronutrient supplier with facilities in Pozna? and Wroc?aw, expanding its IDHA and HBED portfolio for eco-friendly crop nutrition and improved agricultural productivity.

February 2022: Nouryon commissioned a new Herkenbosch facility in the Netherlands to double green chelates production, including Dissolvine M (MGDA) and GL (GLDA), supporting sustainable detergent and industrial cleaning applications globally.

Companies Covered in Chelating Agents Market

- BASF SE

- Dow Inc.

- Kemira Oyj

- Mitsubishi Chemical Corporation

- Nippon Shokubai Co. Ltd.

- Nouryon

- Hexion Inc.

- Ascend Performance Materials

- Lanxess AG

- Akzo Nobel N.V.

- ADM (Archer Daniels Midland Company)

- Innospec Inc.

- Delamine

- Tate & Lyle PLC

- Jungbunzlauer Suisse AG

- AVA Chemicals Private Ltd.

- Zhonglan Industry Co. Ltd.

- Tosoh Corporation.

- Shandong IRO Chelating Chemical Co. Ltd.

Frequently Asked Questions

The market is valued at US$ 7.7 billion in 2025 and is projected to reach US$ 11.7 billion by 2032 at a 6.1% CAGR.

Key drivers include stringent water treatment regulations, biodegradable cleaning agents, chelated fertilizers in agriculture, and pulp and paper bleaching applications.

EDTA leads due to its strong metal-binding capacity, stability, cost-effectiveness, and regulatory approvals across multiple industries.

Asia Pacific dominates with 46% market share, driven by China’s production, India’s agricultural growth, Southeast Asia’s industrial expansion, and favorable manufacturing cost structures.

Agricultural chelated micronutrient fertilizers using biodegradable agents like IDHA and HBED offer high growth potential in regions with alkaline soils.

Major players include BASF SE, Dow Inc., Nouryon, Kemira Oyj, Mitsubishi Chemical, Nippon Shokubai, Lanxess AG, Akzo Nobel, Hexion, Ascend, ADM, Innospec, and Delamine.