- Mining & Services

- Industrial Noise Control Market

Industrial Noise Control Market Size, Share, and Growth Forecast, 2026 - 2033

Industrial Noise Control Market by Product Type (Flexible, Rigid, Vibration Isolation), Material Type (Polymer & Composites, Metal, Others), End-user Industry (Manufacturing & Heavy Industry, Power Generation & Utility, Others), and Regional Analysis for 2026 - 2033

Industrial Noise Control Market Size and Trends Analysis

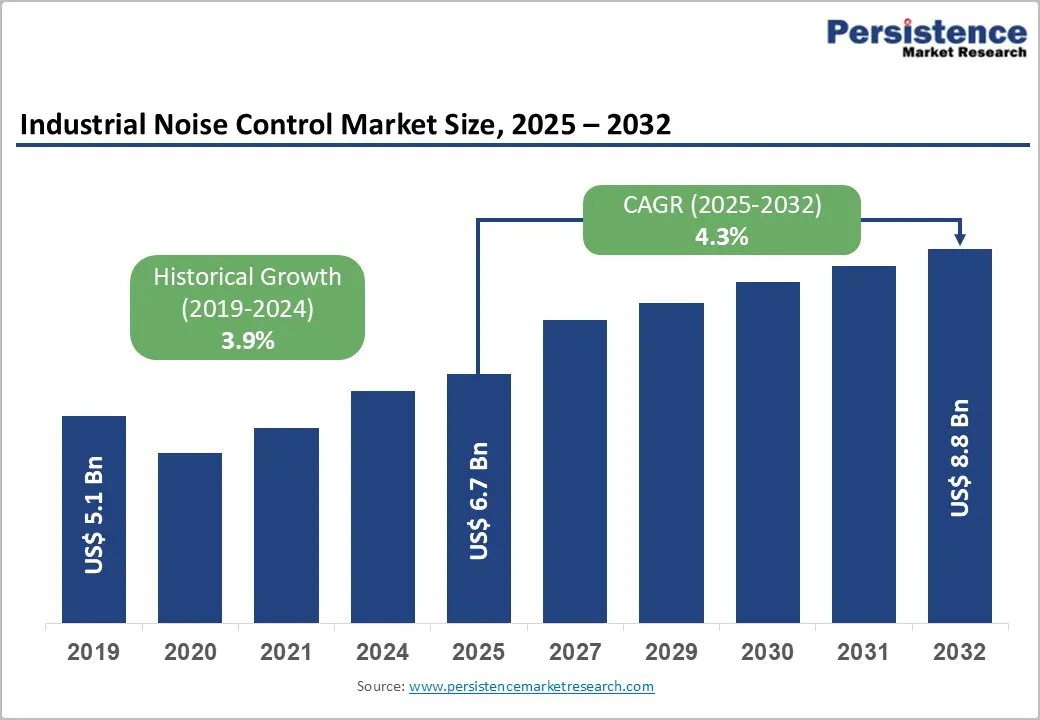

The global industrial noise control market size is projected to be valued at US$6.5 billion in 2026 and is projected to reach US$8.9 billion by 2033, growing at a CAGR of 4.6% during the forecast period from 2026 to 2033, driven by stricter enforcement of occupational health and safety regulations by organizations such as the Occupational Safety and Health Administration (OSHA) and the European Union.

The global revival of manufacturing under the Industry 4.0 framework is driving demand for advanced noise-control solutions. The growing emphasis on sustainability is also encouraging manufacturers to adopt acoustic materials that offer both effective sound insulation and thermal efficiency, thereby improving energy performance in industrial facilities.

Key Industry Highlights:

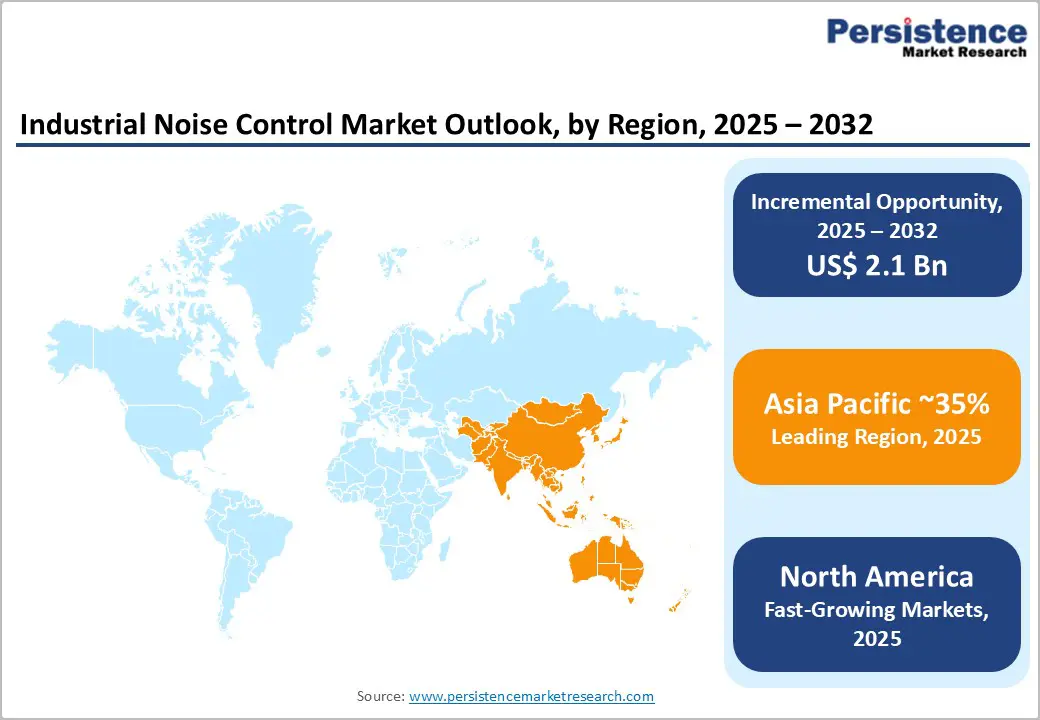

- Leading Region: Asia Pacific is projected to lead due to accelerated industrialization, accounting for 37% global market share, large-scale manufacturing expansion, and infrastructure investment supported by policy-led industrial upgrading.

- Fastest-growing Region: North America is anticipated to grow the fastest due to strong regulatory enforcement, policy-led incentives for domestic manufacturing, and rising investment across clean energy, advanced manufacturing, and infrastructure.

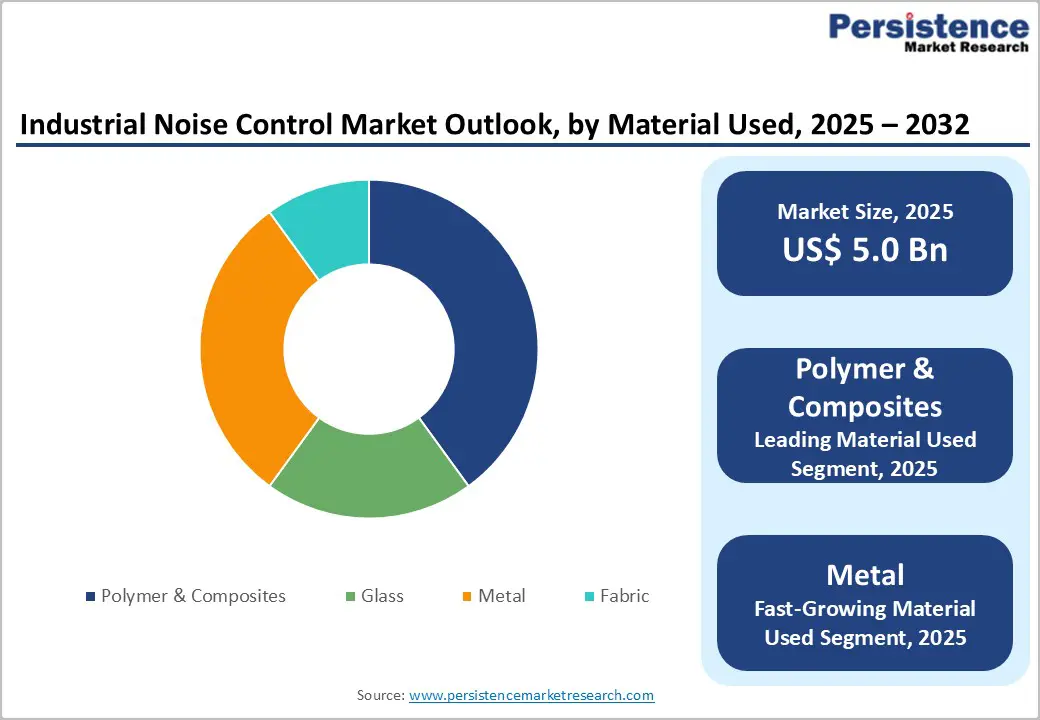

- Leading Material Type: Polymers and composites are projected to dominate, with approximately 35% share, for their favorable damping-to-weight performance, cost-efficiency, durability, and broad applicability across industrial environments.

- Leading End-user: Manufacturing and Heavy Industry is expected to lead the industrial noise control market, accounting for approximately 39% share, including AI-enabled smart monitoring, IoT integration, and sustainable sound-absorbing materials.

- Key Opportunity: Integration of active noise control (ANC) with IIoT-enabled acoustic intelligence offers growth potential. Real-time monitoring, adaptive cancellation, and predictive maintenance capabilities position noise control as both a compliance and operational efficiency solution.

| Key Insights | Details |

|---|---|

| Industrial Noise Control Market Size (2026E) | US$ 6.5 Bn |

| Market Value Forecast (2033F) | US$ 8.9 Bn |

| Projected Growth (CAGR 2026 to 2033) | 4.6% |

| Historical Market Growth (CAGR 2020 to 2025) | 4.1% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growth Analysis - Stringent Occupational Health & Safety Regulations

Stringent occupational health and environmental noise regulations remain the primary structural driver of the industrial noise control market. Regulatory agencies increasingly mandate enforceable exposure thresholds, shifting noise management from voluntary best practice to legal obligation. In the U.S., OSHA requirements on permissible exposure limits and mandatory hearing conservation programs push employers toward engineered noise mitigation rather than relying solely on administrative controls. Similarly, European directives establish lower action thresholds and emphasize preventive measures, compelling industrial operators to address noise at the source through enclosures, silencers, and acoustic barriers.

Beyond worker safety, environmental noise legislation expands demand across urban and infrastructure-linked industries. EU-wide noise mapping obligations require manufacturers, utilities, and transport operators to quantify and actively reduce sound emissions near population centers. The financial implications of non-compliance, including regulatory penalties, litigation risk, and compensation liabilities, materially outweigh upfront mitigation costs. As enforcement intensity increases, industries adopt permanent noise-control solutions to de-risk operations, thereby structurally supporting sustained market expansion in regulated regions. In Q4 2024, Brüel & Kjær launched a cloud-based noise monitoring platform. The firm introduced a new platform for industrial site compliance. This platform enables predictive maintenance and real-time monitoring, helping industries meet noise standards and minimize downtime. This indicates that increasing enforcement of occupational health and environmental noise standards is driving industries to adopt real-time monitoring systems to ensure regulatory compliance.

Barrier Analysis - Technical Trade-offs Affecting Machine Efficiency

Technical trade-offs between noise mitigation and machine performance represent a critical structural barrier for the industrial noise control market. High-performance acoustic enclosures often interfere directly with core equipment operation by restricting airflow, trapping heat, and limiting physical access for inspection and maintenance. In heat-intensive environments such as power generation, metal processing, and heavy manufacturing, inadequate thermal dissipation can accelerate component degradation, increase unplanned downtime, and shorten equipment lifespan. Operators therefore face a high-stakes dilemma in which achieving regulatory noise compliance may introduce new operational risks that are costlier than the original exposure.

The barrier is further amplified by engineering and execution constraints. Effective solutions require highly customized acoustic modeling, integration of silencers or louvers that preserve airflow without compromising attenuation, and site-specific retrofitting in legacy plants that were never designed for enclosure-based controls. The absence of standardized designs prolongs deployment timelines and increases project uncertainty, while volatility in steel and specialty-material supply chains further inflates system costs and compresses supplier margins. Together, these factors create strong resistance among operators, slowing decision-making and materially constraining adoption despite regulatory pressure.

Opportunity Analysis - Integration of Active Noise Control and IIoT-Enabled Acoustic Intelligence

The convergence of active noise control and industrial digitalization creates a high-value opportunity beyond conventional passive mitigation solutions. Traditional barriers and absorptive materials lose effectiveness against low-frequency noise from turbines, compressors, and other rotating equipment, leaving a persistent compliance gap in heavy industries. As computational capabilities improve and sensor costs decline, ANC is transitioning from niche applications to viable industrial deployments, particularly where space constraints or thermal considerations limit the use of passive enclosures.

The integration of ANC with IIoT platforms further amplifies its strategic value. Networked acoustic sensors enable continuous noise mapping, adaptive cancellation, and real-time compliance assurance across dynamic operating conditions. More importantly, acoustic signatures act as early indicators of mechanical imbalance, bearing wear, or airflow disruptions, positioning smart noise systems as predictive maintenance tools rather than pure compliance assets. This dual functionality reframes noise control from a cost center into an operational intelligence layer, accelerating adoption among asset-intensive industries seeking to optimize uptime while meeting regulatory requirements. In December 2024, SoundPLAN launches version 6.0 of its noise mapping software. A software company released an updated version of its environmental noise calculation tool. Provides reliable visualization and documentation of noise from industrial sources, aiding in regulatory compliance and efficient project planning. This indicates a market transition toward data-centric and networked acoustic intelligence platforms that enable continuous noise mapping, compliance assurance, and integration with predictive maintenance workflows, laying the digital foundation for active noise control deployment in heavy industrial environments.

Category-wise Analysis

Material Type Insights

Polymer and composite materials are expected to account for approximately 35% of total market share in 2026, positioning them as the leading material category due to their structurally favorable damping-to-weight performance and broad industrial applicability. Their dominance is projected to persist as acoustic foams and loaded composite barriers deliver high sound absorption without imposing excessive structural load on facilities. Resistance to oil, chemicals, and fire further supports adoption in demanding manufacturing and construction environments. Ongoing advances in materials engineering are expected to enhance durability and lifecycle performance, reinforcing procurement preferences. In addition, polymers and composites continue to benefit from ease of customization and scalable deployment across diverse noise control configurations.

Metal-based acoustic materials are expected to be the fastest-growing segment in the industrial noise control market, driven by emerging needs for durable, high-performance solutions in extreme industrial environments where traditional foams and fabrics fail. Growth is being catalyzed by advancements in rigid metal products such as silencers, machinery enclosures, and soundproof panels, which provide superior structural integrity, heat resistance, and recyclability. Accelerating adoption is supported by modular designs, AI-assisted digital acoustic modeling, and IoT-enabled smart metal enclosures, lowering operational friction for first-time adopters, while improvements in industrial validation, lifecycle durability, and workforce familiarity position metal-based solutions to outpace overall market growth over the forecast period.

End-user Insights

Manufacturing and heavy industry is expected to lead the market, accounting for approximately 39% share in 2026, underpinned by the extensive deployment of high-decibel machinery and intensive acoustic environments in sectors such as metal processing, mining, and large-scale manufacturing. Adoption remains anchored by operational efficiency, workforce protection, and asset longevity, with enterprises prioritizing modular integration and flexible acoustic solutions in sprawling facilities. Ongoing platform evolution, including AI-enabled smart monitoring, IoT integration, and sustainable sound-absorbing materials, continues to reinforce replacement cycles and utilization intensity. Brands like IAC Acoustics, Kinetics Noise Control, The Durr Group, Sound Seal Inc., and BBM Akustik Technologie provide comprehensive enclosures, silencers, and vibration-isolation systems that integrate into industrial workflows. This combination of mature infrastructure, ecosystem lock-in, and predictable demand sustains the segment’s dominance across structured deployment models.

Power generation and utilities are expected to be the fastest-growing segment, driven by the rapid expansion of renewable energy infrastructure and the modernization of legacy power plants, which introduce new low-frequency noise and vibration challenges. Growth is being catalyzed by hybrid active-passive noise systems, modular plug-and-play barriers, and cloud-based monitoring platforms that improve compliance, predictive maintenance, and operational efficiency. Accelerating adoption is supported by advanced gear units, high-performance silencers, and vibration-isolation solutions from brands such as IAC Acoustics, The Durr Group, BBM Akustik Technologie, and SEW-EURODRIVE, thereby lowering implementation friction for new installations. As urban-proximate power facilities and regulatory enforcement increase, this segment is expected to outpace overall market growth over the forecast period.

Regional Insights

Asia Pacific Industrial Noise Control Market Size

Asia Pacific is expected to lead the global market as the dominant region, accounting for approximately 37% share in 2026, driven by accelerated industrialization across China and India. The region benefits from large-scale manufacturing expansion, rising infrastructure investments, and policy-led industrial upgrading that supports early-stage integration of control solutions. Unlike mature Western markets that rely on retrofitting, Asia Pacific increasingly adopts greenfield development models, enabling prevention-through-design approaches. Strengthening regulatory oversight and tighter enforcement of environmental and industrial standards are expected to accelerate compliance-driven adoption, positioning the region ahead of Europe and North America in volume-led demand and structural growth momentum.

The region is likely to remain structurally advantaged as China advances national industrial modernization programs and India expands large-scale manufacturing under government-led initiatives. These policy frameworks support integrated infrastructure planning and cost-efficient supply chains, reinforcing adoption across heavy industry and precision manufacturing. Price sensitivity continues to shape demand, favoring flexible and polymer-based solutions suited to large-volume deployment.

Europe Industrial Noise Control Market Size

Europe is expected to account for approximately 30% of the global market, reflecting a mature and structurally stable regional position. Germany, the U.K., and France act as core hubs, supported by advanced industrial capabilities and strong regulatory alignment under the European Green Deal. Policymakers increasingly treat noise as a critical environmental pollutant, which reinforces compliance-driven adoption across industrial and infrastructure projects. The region benefits from high technical standards and early integration of sustainability requirements, positioning Europe ahead of emerging regions in technological sophistication but behind them in volume-driven expansion.

The region is likely to remain stable rather than high-growth, as demand centers on replacement cycles, regulatory upgrades, and premium applications. Advanced diagnostic approaches, such as noise source visualization before solution deployment, support precision-driven implementation. These structural factors are expected to preserve Europe’s mature market profile, balancing regulatory rigor and sustainability leadership with limited acceleration potential compared to Asia Pacific.

North America Noise Control Market Size

North America is expected to be the fastest-growing region, driven by strong regulatory enforcement and accelerating industrial investment. The U.S. anchors regional momentum through a mature compliance framework, with the OSHA Hearing Conservation Amendment acting as a continuous demand driver for industrial noise control solutions. Policy-led incentives supporting domestic manufacturing expansion strengthen demand across clean energy, advanced manufacturing, and infrastructure projects. This regulatory and policy alignment positions North America ahead of Europe in growth velocity while maintaining higher compliance intensity than Asia Pacific.

The region is likely to experience sustained acceleration as new gigafactories and semiconductor facilities integrate noise control into their designs rather than retrofitting. Industrial buyers prioritize custom-engineered solutions that integrate with HVAC and fire safety systems, reflecting high technical expectations and risk management standards. Expanding industrial capacity, combined with a strong safety culture and litigation-aware compliance practices, supports adoption across high-value applications. These structural factors are expected to reinforce North America’s fastest-growth profile while preserving its position as a high-specification, compliance-driven market.

Competitive Analysis

The global industrial noise control market exhibits a moderately consolidated structure, combining large multinational material science conglomerates with specialized acoustic engineering firms. Leading participants collectively account for an estimated 35 - 40% of overall market activity, indicating a competitive environment where scale advantages coexist with niche specialization. Global players such as Saint-Gobain, 3M, and Sika AG leverage extensive distribution networks and diversified material portfolios to address broad industrial requirements, while maintaining compliance with increasingly stringent environmental and occupational safety regulations.

Alongside these multinationals, specialist firms such as IAC Acoustics and Kinetics Noise Control compete through deep engineering expertise and project-specific capabilities. These players focus on complex, high-performance applications, including turbine enclosures and controlled testing environments, where customization and regulatory adherence are critical. Market differentiation increasingly centers on integrated service models that combine site assessment, acoustic modeling, manufacturing, installation, and post-installation compliance certification. This structure sustains moderate fragmentation, with innovation, sustainability alignment, and solution integration shaping competitive positioning rather than pure price competition.

Key Industry Developments:

- In June 2025, Kinetics Noise Control launched Econetic Core Acoustical Panels. Firm unveiled industry-first DECLARE Red List Free panels for noise control. Promoted health and sustainability by eliminating harmful chemicals, ideal for green building projects in industrial settings.

- In February 2025, BASF introduced Basotect EcoBalanced melamine foam. Chemical giant launched a new sustainable melamine resin foam with a reduced carbon footprint. The product lowers the product's carbon footprint by up to 50%, supporting greener noise absorption in the automotive and construction industries while maintaining high performance.

- In November 2024, Sound Seal launched colorful exterior-grade baffles and barriers. The company introduced a new line of visually appealing outdoor noise control products. Combined aesthetic improvements with superior acoustic performance, suitable for industrial outdoor applications, and enhancing workplace environments.

Industrial Noise Control Market

| Report Attribute | Details |

|---|---|

| Historical Data/Actuals | 2020 - 2025 |

| Forecast Period | 2026 - 2033 |

| Market Analysis | Value: US$ Bn |

| Geographical Coverage |

|

| Segmental Coverage |

|

| Competitive Analysis |

|

| Report Highlights |

|

Companies Covered in Industrial Noise Control Market

- Saint-Gobain S.A.

- Rockwool International A/S

- BASF SE

- Armstrong World Industries

- Kinetics Noise Control Inc.

- Pyrotek Inc.

- Sound Seal Inc.

- Ventac Co. Ltd.

- Merford Holding B.V.

- IAC Acoustics

- Sika AG

- Eckel Industries Inc.

- Owens Corning

- Honeywell International Inc.

- Knauf Insulation

- Dürr Universal Inc.

- Noise Barriers LLC

Frequently Asked Questions

The global industrial noise control market is projected to be valued at US$6.5 billion in 2026 and is expected to reach US$8.9 billion by 2033, supported by stringent occupational health regulations and a resurgence in global manufacturing activities.

Growth is fundamentally driven by the strict enforcement of occupational health and environmental noise standards by bodies such as OSHA and the EU Commission, which mandates noise mitigation to avoid financial penalties, litigation risks, and to ensure worker safety and regulatory compliance.

The industrial noise control market is forecast to grow at a CAGR of 4.6% from 2026 to 2033, reflecting sustained demand from industrial upgrading and compliance requirements.

North America is the fastest-growing regional market, fueled by strong regulatory enforcement, policy-led incentives for domestic manufacturing expansion, and the integration of noise control in new gigafactory and semiconductor facility designs.

Key players include Saint-Gobain, Rockwool International, BASF SE, Armstrong World Industries, Kinetics Noise Control, 3M, IAC Acoustics, and Owens Corning.