- Automation & Robotics

- Security Screening Equipment Market

Security Screening Equipment Market Size, Share, and Growth Forecast 2026 – 2033

Security Screening Equipment Market by Equipment Type (X-ray Screening Systems, Metal Detectors, Others), Technology (Electromagnetic Technology, Computed Tomography (CT), Others), Application, End-user (Airports, Others), and Regional Analysis for 2026-2033

Security Screening Equipment Market Size and Trends Analysis

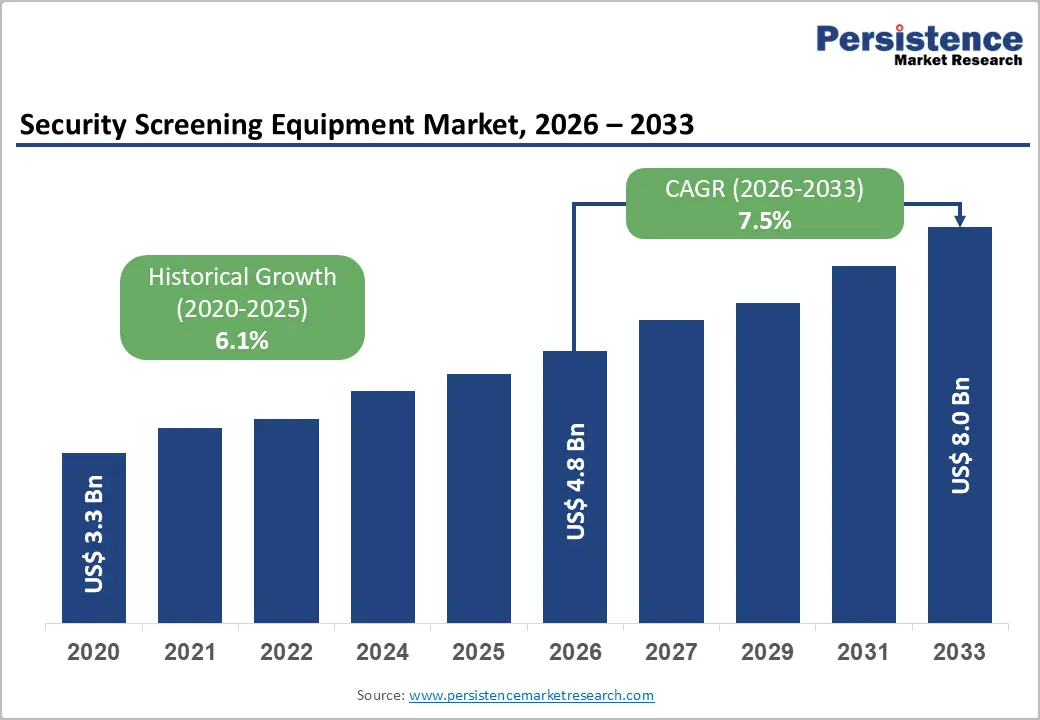

The global security screening equipment market size is likely to be valued at US$4.7 billion in 2026 and is expected to reach US$7.8 billion by 2033, growing at a CAGR of 7.5% during the forecast period from 2026 and 2033, driven by increasing concerns related to terrorism, illegal trafficking, and smuggling activities, which are compelling governments and private operators to strengthen security infrastructure. Stringent regulatory mandates across aviation, border control, and critical infrastructure are further accelerating the adoption of advanced screening systems. Technological advancements are significantly shaping market trends, with the rising integration of artificial intelligence (AI), computed tomography (CT), millimeter-wave imaging, and biometric-based screening solutions enhancing detection accuracy, throughput, and operational efficiency.

Key Industry Highlights:

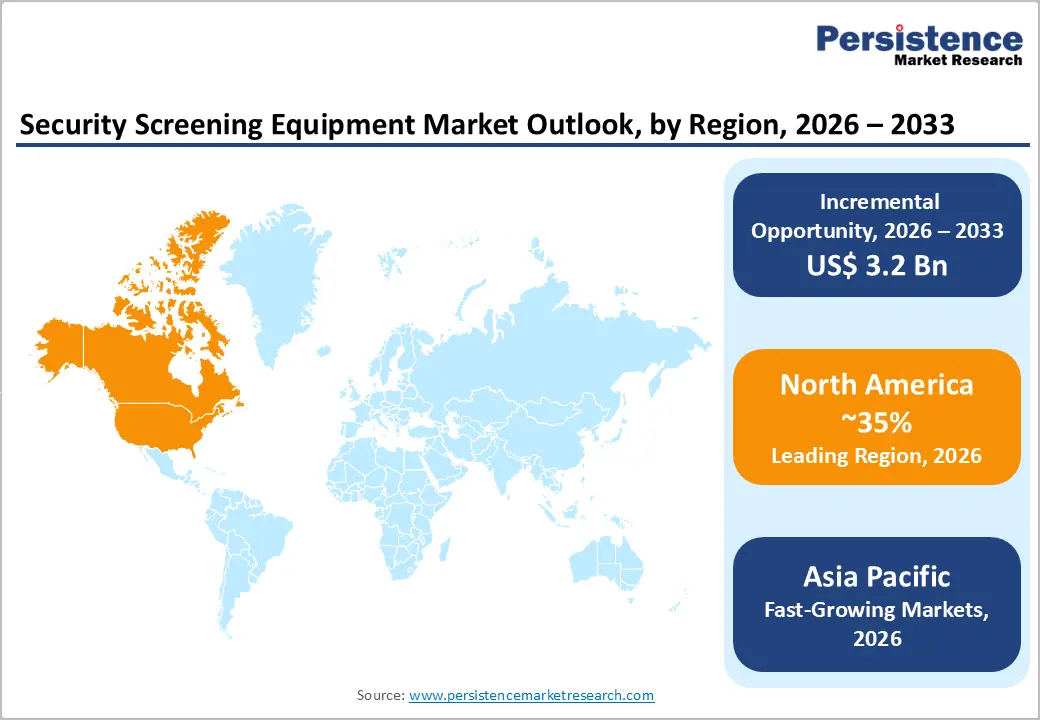

- Leading Region: North America leads with around 35% share, driven by stringent TSA regulations, substantial government investments, and rapid adoption of advanced screening technologies.

- Fastest-growing Region: Asia Pacific is the fastest-growing region, driven by rising security concerns, rapid urbanization, and large-scale infrastructure expansions across China, India, Japan, and ASEAN countries, supported by a strong manufacturing base and government incentives.

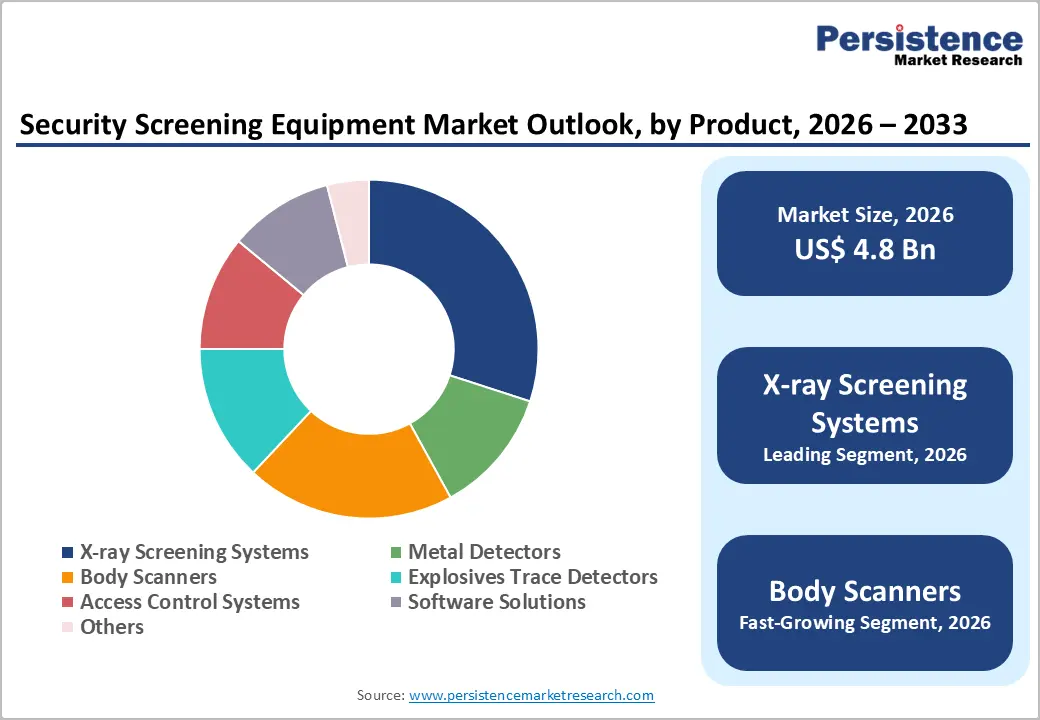

- Leading Equipment Type: X-ray screening systems lead with nearly 30% share, driven by their vital role in baggage and cargo inspection for high throughput and reliability.

- Leading Technology: Electromagnetic technology leads with over 40% share, primarily used in metal detection and access control systems.

- Leading Application: Aviation security dominates with about 40% share, driven by stringent regulatory requirements and rising global passenger traffic.

- Leading End-user: Airports lead with about 45% share, supported by rising air travel and stringent government security mandates.

| Key Insights | Details |

|---|---|

| Security Screening Equipment Market Size (2026E) | US$4.7 Bn |

| Market Value Forecast (2033F) | US$7.8 Bn |

| Projected Growth CAGR (2026-2033) | 7.5% |

| Historical Market Growth (2020-2025) | 6.1% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Government Security Investments and Regulatory Mandates

Governments worldwide are making substantial investments in security screening infrastructure across airports, railway stations, border checkpoints, and major public spaces to combat terrorism, smuggling, and organized crime. Rising geopolitical tensions and cross-border threats have prompted authorities to enhance national security frameworks through the deployment of advanced screening technologies. Increased defense and homeland security budgets are accelerating large-scale procurement of next-generation screening systems, particularly in high-risk transportation and border zones. Mandatory compliance audits and security certifications further reinforce continuous equipment upgrades across regions.

Agencies such as the TSA, ECAC, and regional bodies in Asia Pacific enforce strict screening standards mandating certified X-ray scanners, explosives detectors, and body screening systems. These initiatives not only strengthen public safety but also create a steady demand for advanced, reliable, and high-throughput security screening equipment. Regulatory mandates ensure that airports, public transport systems, and government facilities regularly upgrade to the latest technology for higher accuracy and efficiency. Such regulations are also driving the adoption of AI-enabled and automated screening solutions to improve throughput and reduce human error, while standardized security norms support cross-border technology adoption.

High Capital Expenditure and Maintenance Costs

The security screening equipment market faces restraints due to the substantial upfront investment required for advanced systems such as computed tomography (CT) scanners, millimeter-wave body scanners, and explosives trace detectors, along with the high costs of installation and integration into existing infrastructures. This cost burden can be challenging for smaller airports, public facilities, and developing economies with limited budgets, slowing down technology adoption. Legacy infrastructure limitations increase retrofit complexity and deployment timelines, while long procurement cycles delay modernization efforts in cost-sensitive regions.

High initial costs are further compounded by ongoing expenses for maintenance, calibration, software upgrades, and personnel training, which continue to strain operational budgets. As screening systems become more sophisticated with AI and automation, the cost of technical support and spare parts continues to rise. These financial barriers often lead to extended replacement cycles and dependence on outdated technologies, impacting overall screening efficiency. Budget constraints also limit the adoption of multi-layered security solutions, and smaller operators often prioritize basic compliance over advanced performance capabilities.

Emerging Markets and Infrastructure Expansion

Emerging markets and large-scale infrastructure expansion present significant opportunities for the market. Rapid urbanization, increasing air travel, and growing investments in transportation hubs across Asia Pacific, the Middle East, and Africa are driving the need for advanced security systems. Governments in these regions are prioritizing modernization of airports, seaports, and public transit networks, creating strong demand for X-ray scanners, body screening systems, and explosives detection technologies. Mega airport projects and cross-border transport corridors are amplifying long-term equipment demand, while rising passenger volumes require high-throughput and scalable screening solutions.

Expanding smart city initiatives and rising public safety concerns are encouraging the deployment of integrated, technology-driven screening solutions. Local manufacturing incentives and public-private partnerships are also enabling cost-effective implementation of advanced screening infrastructure. As emerging economies invest in critical infrastructure and adopt global security standards, vendors with innovative and affordable screening solutions are poised to capture strong growth opportunities. Growing preference for modular and portable screening systems is supporting flexible deployment, and regional policy support is accelerating market entry for domestic manufacturers.

Category-wise Analysis

Equipment Type Insights

X-ray screening systems lead, capturing nearly 30% revenue share in 2025, driven by their critical role in baggage and cargo inspection across airports, transportation hubs, and border checkpoints. These systems are preferred for their high throughput, reliability, and precise threat detection, ensuring efficient and safe passenger and cargo screening. For example, Rapiscan Systems’ baggage X-ray scanners are widely deployed at major international airports to meet global aviation security standards.

The body scanners segment represents the fastest-growing category in the market, driven by increasing deployment at airports, public venues, and government facilities to enhance passenger screening accuracy while maintaining privacy standards. The deployment of millimeter-wave and computed tomography (CT) technologies allows for quicker and more accurate identification of concealed items, minimizing false alarms and enhancing operational efficiency. For instance, major airports in the U.S. and Europe have implemented millimeter-wave body scanners to accelerate and optimize passenger screening procedures.

Technology Type Insights

Electromagnetic technology holds the largest share, accounting for around 40% revenue share in 2025, primarily due to its extensive use in metal detection and access control systems across airports, public venues, and government facilities. Its reliability, cost efficiency, and ease of integration into existing infrastructure make it a preferred choice for large-scale security operations. Widespread use of walk-through and handheld metal detectors across sectors further strengthens its market dominance. For example, walk-through metal detectors supplied by CEIA are extensively deployed at airports, government buildings, and event venues across North America and Europe.

Computed Tomography (CT) technology represents the fastest-growing segment, driven by rising demand for high-precision imaging in aviation security, border checkpoints, and critical infrastructure. CT-based systems provide 3D visualization and automated threat recognition, allowing faster and more accurate detection of concealed items while reducing false alarms. Regulatory support for CT screening upgrades is accelerating its global adoption for enhanced safety and efficiency. For example, Smith’s Detection’s CT-based baggage screening solutions are increasingly deployed at airports to comply with next-generation aviation security regulations.

Application Type Insights

Aviation security is projected to account for approximately 40% of revenue in 2025, fueled by strict international regulations and growing global passenger traffic. Continuous airport expansions and modernization projects further strengthen its leading position, as authorities prioritize advanced screening systems for enhanced safety and operational efficiency. For example, Hong Kong International Airport has implemented smart CT-based screening lanes to improve throughput and security performance.

Government and military facilities represent a rapidly expanding application segment, fueled by growing counter-terrorism efforts, defense modernization programs, and infrastructure upgrades. The increasing need to secure sensitive locations and critical assets is prompting higher adoption of advanced X-ray, explosives detection, and biometric screening technologies across defense and government installations. For example, Defense installations increasingly rely on explosives trace detectors supplied by companies such as Smiths Detection to secure restricted zones.

End-user Type Insights

Airports remain the largest end-user segment in the security screening equipment market, capturing around 45% revenue share, driven by the surge in air travel, coupled with stringent government security mandates that require advanced baggage and passenger screening systems. Continuous investments in airport expansions, modernization projects, and automated checkpoint solutions further reinforce the strong demand for reliable and high-throughput screening technologies. For example, Major hubs such as London Heathrow have upgraded to CT baggage scanners to enhance screening efficiency and passenger experience.

The stadiums and events segment is witnessing rapid growth, propelled by the increasing frequency of large public gatherings, concerts, and sports events. Rising emphasis on crowd safety and efficient access control is driving the deployment of portable and scalable screening systems capable of managing high visitor volumes. As public event security becomes a priority, this segment is expected to contribute significantly to future market expansion. For example, Metal detectors and handheld screening devices are now routinely deployed at international sporting events such as the FIFA World Cup to manage high visitor volumes securely.

Regional Insights

North America Security Screening Equipment Market Trends

North America leads the security screening equipment market, holding approximately 35% of the regional share. This growth is fueled by rising security threats, ongoing infrastructure upgrades, and the increasing adoption of advanced screening technologies. The U.S. and Canada drive this expansion through stringent TSA and DHS regulations that prioritize enhanced screening at airports, border crossings, and public venues. Rapid advancements in CT, millimeter-wave, and AI-based detection systems further propel market growth.

The rising demand for efficient, high-throughput security solutions across aviation, logistics, and critical infrastructure sectors is spurring continuous investment in modernization projects. The integration of automation and digital technologies is enabling faster, more accurate threat detection, reshaping the regional landscape. For instance, Rapiscan Systems provides advanced CT baggage screening and checkpoint solutions at major U.S. airports under TSA certification programs, reinforcing North America’s position as a hub for security screening innovation—driven by strong government initiatives and leading technology providers.

Europe Security Screening Equipment Market Trends

Europe represents a mature and steadily expanding market for security screening equipment, fueled by strict regulatory frameworks and heightened security concerns across airports, transportation networks, and public venues. The European Civil Aviation Conference (ECAC) plays a pivotal role in harmonizing screening standards, encouraging widespread adoption of certified X-ray scanners, explosives detectors, and body scanners among member states.

The region is increasingly embracing advanced technologies such as computed tomography (CT) and millimeter-wave systems to improve detection accuracy and streamline passenger throughput. Growing focus on data privacy and adherence to the EU’s General Data Protection Regulation (GDPR) is shaping the development of privacy-conscious screening solutions. For instance, Smiths Detection has been a key player in Europe, providing ECAC-certified CT screening systems for airports in Germany and the U.K. Ongoing infrastructure upgrades, smart border initiatives, and security requirements for large public events are further driving demand for equipment across both public and private sectors.

Asia Pacific Security Screening Equipment Market Trends

The Asia Pacific region is the fastest-growing, driven by rapid urbanization, escalating security concerns, and extensive infrastructure development. Countries including China, India, Japan, and those in Southeast Asia are heavily investing in airport expansions, smart city initiatives, and modernization of border security. Government programs aimed at enhancing national security and regulatory compliance are fueling strong demand for advanced screening systems across transportation hubs and public spaces.

The region’s robust manufacturing capabilities support the production of cost-effective and innovative screening technologies. Rising passenger volumes, combined with the need for efficient operations at airports and railway stations, are accelerating the adoption of computed tomography (CT) and AI-powered detection systems. For example, Nuctech supplies X-ray and CT-based security screening solutions to airports, rail stations, and border checkpoints across China and Southeast Asia. The growing investments in defense, logistics, and event security, supported by favorable policies, are driving sustained growth throughout the Asia Pacific market.

Competitive Landscape

The global security screening equipment market is moderately competitive, with several leading companies prioritizing technological innovation, regulatory compliance, and international expansion to enhance their market positions. Major players such as Smiths Detection, Rapiscan Systems, Analogic Corporation, Adani Systems, and Teledyne DALSA are investing in CT technology, AI-powered analytics, and millimeter-wave scanners to boost the accuracy and efficiency of threat detection.

These companies are also focusing on integrating cybersecurity measures and ensuring interoperability with cloud-based monitoring systems to support smart infrastructure security. Strategic partnerships, mergers, and government contracts are key to sustaining competitiveness. For example, collaborations between manufacturers and airport authorities are facilitating large-scale deployments of next-generation scanners and explosive trace detection solutions.

Key Industry Developments:

- In October 2025, Smiths Detection launched the SDX 10080 SCT, a modular hold baggage and air cargo screening system built on its explosives detection (EDS) platform. The system features dual-energy computed tomography (CT) with an optional high-resolution dual-view line scanner, designed to meet current standards such as ECAC Standard 3.2 and TSA 7.3, while offering readiness for future regulations, including ECAC Standard 4.0 and TSA 9.0. Engineered as a drop-in replacement, the SDX 10080 SCT maintains full network compatibility and the same physical footprint as existing scanners.

- In September 2025, Athena Security announced the launch of its centralized "Second Look" AI X-ray screening platform to enhance multi-site security operations. The system combines on-premise AI analysis with cloud-based oversight, allowing human operators to review flagged items across multiple locations. This enterprise solution is designed to improve the speed, accuracy, and reliability of X-ray screening by providing a second layer of expert review, reducing errors caused by fatigue, distraction, or complex object overlap.

Frequently Asked Questions

The global security screening equipment market is valued at US$4.7 billion in 2026 and expected to reach US$7.8 billion by 2033, reflecting robust growth.

The primary demand drivers for the market include increased government spending on security, stringent regulatory requirements, and technological advancements such as artificial intelligence (AI) and computed tomography (CT) technologies.

X-ray screening systems lead with a 30% share, due to their critical role in airports and border security.

North America dominates, capturing over 35% driven by regulatory frameworks and technological innovation.

A major opportunity in the security screening equipment market lies in the expanding markets across the Asia Pacific region and the increasing demand for AI-driven automated screening solutions.