- Executive Summary

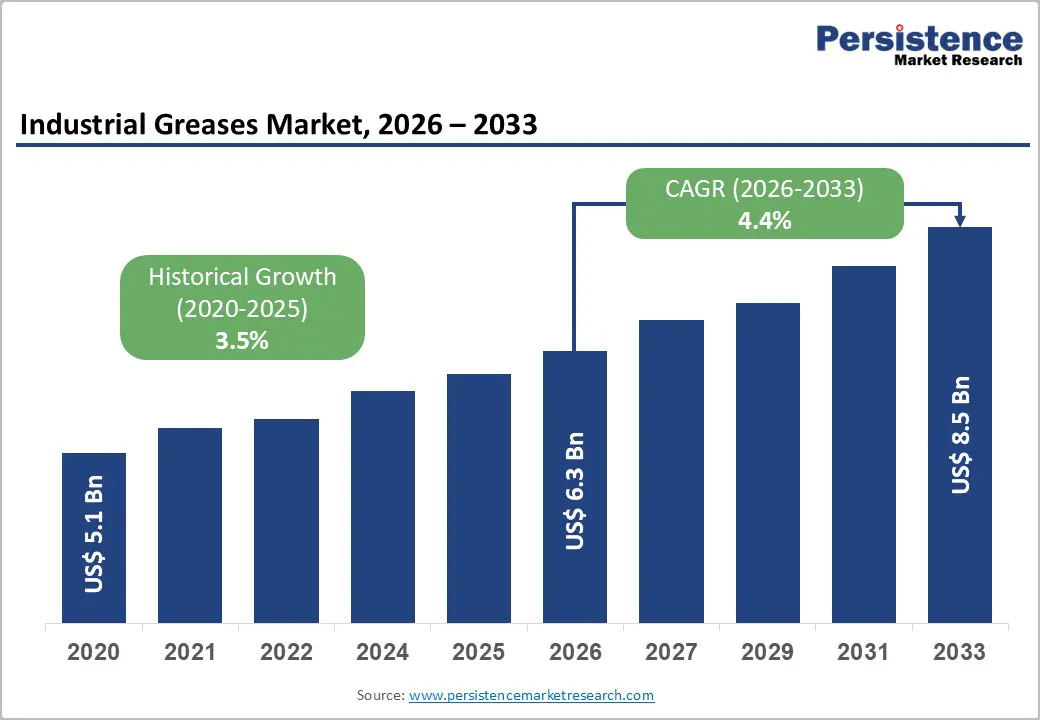

- Global Industrial Greases Market Snapshot 2026 and 2033

- Market Opportunity Assessment, 2026-2033, US$ Bn

- Key Market Trends

- Industry Developments and Key Market Events

- Demand Side and Supply Side Analysis

- PMR Analysis and Recommendations

- Market Overview

- Market Scope and Definitions

- Value Chain Analysis

- Macro-Economic Factors

- Global GDP Outlook

- Global Automotive Industry Overview

- Global Mining Industry Overview

- Forecast Factors – Relevance and Impact

- COVID-19 Impact Assessment

- PESTLE Analysis

- Porter's Five Forces Analysis

- Geopolitical Tensions: Market Impact

- Regulatory and Technology Landscape

- Market Dynamics

- Drivers

- Restraints

- Opportunities

- Trends

- Price Trend Analysis, 2020 – 2033

- Region-wise Price Analysis

- Price by Segments

- Price Impact Factors

- Global Industrial Greases Market Outlook: Historical (2020 – 2025) and Forecast (2026 – 2033)

- Key Highlights

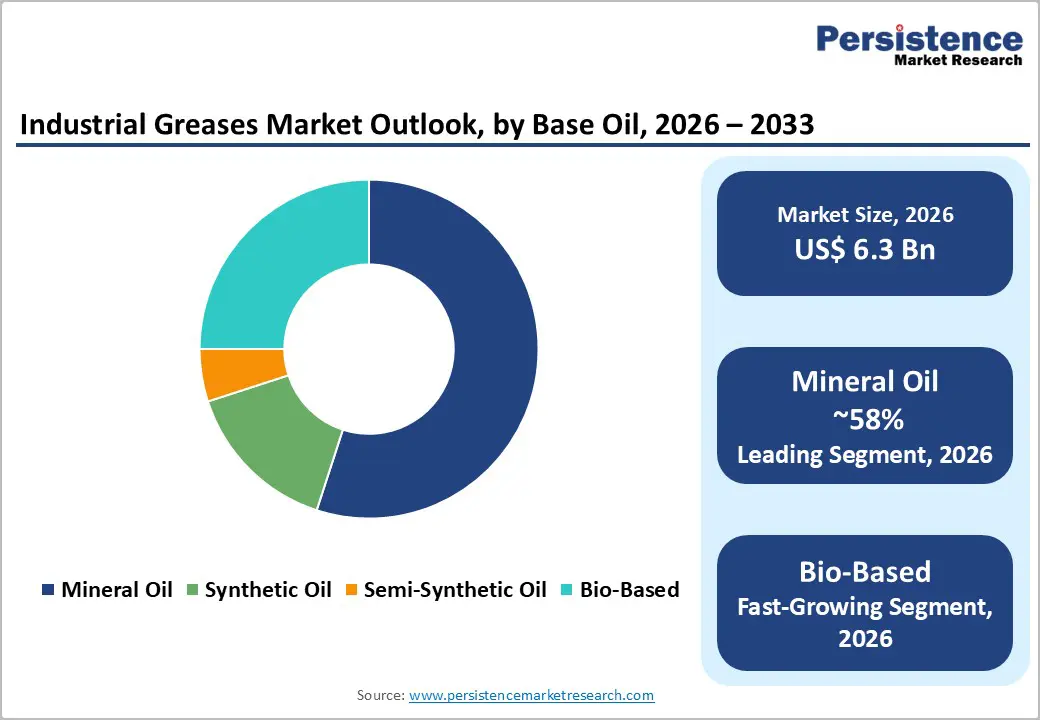

- Global Industrial Greases Market Outlook: Base Oil

- Introduction/Key Findings

- Historical Market Size (US$ Bn) and Volume (Units) Analysis by Base Oil, 2020-2025

- Current Market Size (US$ Bn) and Volume (Units) Forecast, by Base Oil, 2026-2033

- Mineral Oil

- Synthetic Oil

- Semi-Synthetic Oil

- Bio-Based

- Market Attractiveness Analysis: Base Oil

- Global Industrial Greases Market Outlook: Thickener Type

- Introduction/Key Findings

- Historical Market Size (US$ Bn) and Volume (Units) Analysis by Thickener Type, 2020-2025

- Current Market Size (US$ Bn) and Volume (Units) Forecast, by Thickener Type, 2026-2033

- Simple Metal Soaps

- Non-Soap Thickener

- Complex Metal Soaps

- Market Attractiveness Analysis: Thickener Type

- Global Industrial Greases Market Outlook: End- Users

- Introduction/Key Findings

- Historical Market Size (US$ Bn) and Volume (Units) Analysis by End- Users, 2020-2025

- Current Market Size (US$ Bn) and Volume (Units) Forecast, by End- Users, 2026-2033

- Auto Manufacturing

- Off Highway and Construction

- Mining and Metallurgy

- Other Transportation

- On Road Vehicles

- Other Manufacturing

- Market Attractiveness Analysis: End- Users

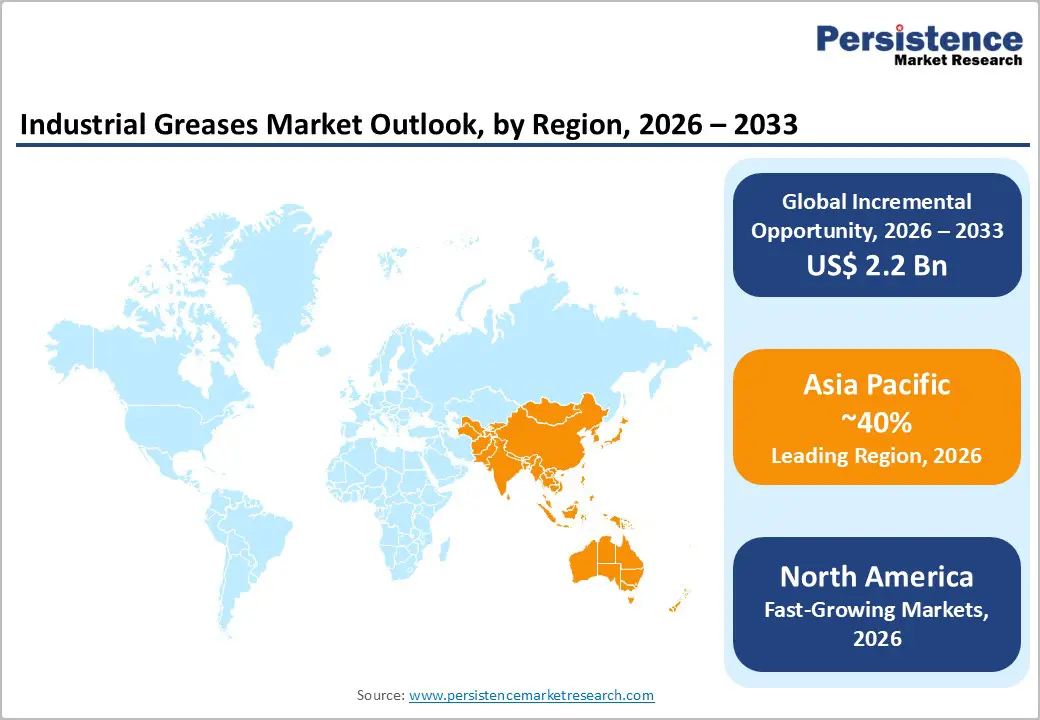

- Global Industrial Greases Market Outlook: Region

- Key Highlights

- Historical Market Size (US$ Bn) and Volume (Units) Analysis by Region, 2020-2025

- Current Market Size (US$ Bn) and Volume (Units) Forecast, by Region, 2026-2033

- North America

- Europe

- East Asia

- South Asia & Oceania

- Latin America

- Middle East & Africa

- Market Attractiveness Analysis: Region

- North America Industrial Greases Market Outlook: Historical (2020 – 2025) and Forecast (2026 – 2033)

- Key Highlights

- Pricing Analysis

- North America Market Size (US$ Bn) and Volume (Units) Forecast, by Country, 2026-2033

- U.S.

- Canada

- North America Market Size (US$ Bn) and Volume (Units) Forecast, by Base Oil, 2026-2033

- Mineral Oil

- Synthetic Oil

- Semi-Synthetic Oil

- Bio-Based

- North America Market Size (US$ Bn) and Volume (Units) Forecast, by Thickener Type, 2026-2033

- Simple Metal Soaps

- Non-Soap Thickener

- Complex Metal Soaps

- North America Market Size (US$ Bn) and Volume (Units) Forecast, by End- Users, 2026-2033

- Auto Manufacturing

- Off Highway and Construction

- Mining and Metallurgy

- Other Transportation

- On Road Vehicles

- Other Manufacturing

- Europe Industrial Greases Market Outlook: Historical (2020 – 2025) and Forecast (2026 – 2033)

- Key Highlights

- Pricing Analysis

- Europe Market Size (US$ Bn) and Volume (Units) Forecast, by Country, 2026-2033

- Germany

- Italy

- France

- U.K.

- Spain

- Russia

- Rest of Europe

- Europe Market Size (US$ Bn) and Volume (Units) Forecast, by Base Oil, 2026-2033

- Mineral Oil

- Synthetic Oil

- Semi-Synthetic Oil

- Bio-Based

- Europe Market Size (US$ Bn) and Volume (Units) Forecast, by Thickener Type, 2026-2033

- Simple Metal Soaps

- Non-Soap Thickener

- Complex Metal Soaps

- Europe Market Size (US$ Bn) and Volume (Units) Forecast, by End- Users, 2026-2033

- Auto Manufacturing

- Off Highway and Construction

- Mining and Metallurgy

- Other Transportation

- On Road Vehicles

- Other Manufacturing

- East Asia Industrial Greases Market Outlook: Historical (2020 – 2025) and Forecast (2026 – 2033)

- Key Highlights

- Pricing Analysis

- East Asia Market Size (US$ Bn) and Volume (Units) Forecast, by Country, 2026-2033

- China

- Japan

- South Korea

- East Asia Market Size (US$ Bn) and Volume (Units) Forecast, by Base Oil, 2026-2033

- Mineral Oil

- Synthetic Oil

- Semi-Synthetic Oil

- Bio-Based

- East Asia Market Size (US$ Bn) and Volume (Units) Forecast, by Thickener Type, 2026-2033

- Simple Metal Soaps

- Non-Soap Thickener

- Complex Metal Soaps

- East Asia Market Size (US$ Bn) and Volume (Units) Forecast, by End- Users, 2026-2033

- Auto Manufacturing

- Off Highway and Construction

- Mining and Metallurgy

- Other Transportation

- On Road Vehicles

- Other Manufacturing

- South Asia & Oceania Industrial Greases Market Outlook: Historical (2020 – 2025) and Forecast (2026 – 2033)

- Key Highlights

- Pricing Analysis

- South Asia & Oceania Market Size (US$ Bn) and Volume (Units) Forecast, by Country, 2026-2033

- India

- Southeast Asia

- ANZ

- Rest of SAO

- South Asia & Oceania Market Size (US$ Bn) and Volume (Units) Forecast, by Base Oil, 2026-2033

- Mineral Oil

- Synthetic Oil

- Semi-Synthetic Oil

- Bio-Based

- South Asia & Oceania Market Size (US$ Bn) and Volume (Units) Forecast, by Thickener Type, 2026-2033

- Simple Metal Soaps

- Non-Soap Thickener

- Complex Metal Soaps

- South Asia & Oceania Market Size (US$ Bn) and Volume (Units) Forecast, by End- Users, 2026-2033

- Auto Manufacturing

- Off Highway and Construction

- Mining and Metallurgy

- Other Transportation

- On Road Vehicles

- Other Manufacturing

- Latin America Industrial Greases Market Outlook: Historical (2020 – 2025) and Forecast (2026 – 2033)

- Key Highlights

- Pricing Analysis

- Latin America Market Size (US$ Bn) and Volume (Units) Forecast, by Country, 2026-2033

- Brazil

- Mexico

- Rest of LATAM

- Latin America Market Size (US$ Bn) and Volume (Units) Forecast, by Base Oil, 2026-2033

- Mineral Oil

- Synthetic Oil

- Semi-Synthetic Oil

- Bio-Based

- Latin America Market Size (US$ Bn) and Volume (Units) Forecast, by Thickener Type, 2026-2033

- Simple Metal Soaps

- Non-Soap Thickener

- Complex Metal Soaps

- Latin America Market Size (US$ Bn) and Volume (Units) Forecast, by End- Users, 2026-2033

- Auto Manufacturing

- Off Highway and Construction

- Mining and Metallurgy

- Other Transportation

- On Road Vehicles

- Other Manufacturing

- Middle East & Africa Industrial Greases Market Outlook: Historical (2020 – 2025) and Forecast (2026 – 2033)

- Key Highlights

- Pricing Analysis

- Middle East & Africa Market Size (US$ Bn) and Volume (Units) Forecast, by Country, 2026-2033

- GCC Countries

- South Africa

- Northern Africa

- Rest of MEA

- Middle East & Africa Market Size (US$ Bn) and Volume (Units) Forecast, by Base Oil, 2026-2033

- Mineral Oil

- Synthetic Oil

- Semi-Synthetic Oil

- Bio-Based

- Middle East & Africa Market Size (US$ Bn) and Volume (Units) Forecast, by Thickener Type, 2026-2033

- Simple Metal Soaps

- Non-Soap Thickener

- Complex Metal Soaps

- Middle East & Africa Market Size (US$ Bn) and Volume (Units) Forecast, by End- Users, 2026-2033

- Auto Manufacturing

- Off Highway and Construction

- Mining and Metallurgy

- Other Transportation

- On Road Vehicles

- Other Manufacturing

- Competition Landscape

- Market Share Analysis, 2025

- Market Structure

- Competition Intensity Mapping

- Competition Dashboard

- Company Profiles

- Belray Company LLC

- Company Overview

- Product Portfolio/Offerings

- Key Financials

- SWOT Analysis

- Company Strategy and Key Developments

- Texaco Inc

- Exxon Mobil Corporation

- Whitmore Manufacturing Company

- Axel Christiernsson International AB

- Dow Corning Corporation

- Sinopec Lubricant Company

- Royal Dutch Shell plc

- Royal High Performance Oil & Greases

- Industrial Oils Unlimited

- Primrose Oil Company, Inc.

- Belray Company LLC

- Appendix

- Research Methodology

- Research Assumptions

- Acronyms and Abbreviations

- Specialty & Fine Chemicals

- Industrial Greases Market

Industrial Greases Market Size, Share, and Growth Forecast 2026 - 2033

Industrial Greases Market by Base Oil (Mineral Oil, Synthetic Oil, Semi-Synthetic Oil, Bio-Based), by Thickener Type (Simple Metal Soaps, Non-Soap Thickener, Complex Metal Soaps), by End-Users (Auto Manufacturing, Off Highway and Construction, Mining and Metallurgy, Other Transportation, On Road Vehicles, Other Manufacturing), and Regional Analysis, 2026 - 2033

Market Overview

The global Industrial Greases market size is likely to be valued at US$ 6.3 billion in 2026 and is projected to reach US$ 8.5 billion by 2033, growing at a CAGR of 4.4% between 2026 and 2033.

The industrial greases market is expanding rapidly due to escalating demand from the automotive, construction, and mining sectors, which require high-performance lubrication solutions for machinery operating under extreme conditions. Rising industrial production across emerging economies, particularly in the Asia-Pacific region, combined with technological advancements in synthetic and bio-based greases, continues to drive market growth.

Key Market Highlights

- Leading Region: Asia-Pacific dominates the global industrial greases market, accounting for approximately 40% of total consumption, driven by China's position as the world's largest automotive and heavy equipment manufacturer, coupled with rapid industrial expansion in India, Vietnam, and Southeast Asian economies, creating sustained demand for specialized lubrication solutions.

- Fastest Growing Region: Asia Pacific exhibits the fastest regional growth at approximately 4.8-5.2% CAGR, with China experiencing 4.0% CAGR through 2035 and India demonstrating accelerating demand growth exceeding 6% annually, fueled by manufacturing modernization initiatives, automotive production expansion, and infrastructure development projects requiring high-performance greases.

- Dominant Segment from Product Type Category: Mineral oil-based greases command 58% market share globally, maintaining leadership through cost-effectiveness, established supply infrastructure, broad customer familiarity, and proven performance across diverse industrial applications, despite gradual market share erosion to synthetic alternatives.

- Fastest Growing Segment from Base Oil Category: Synthetic oil-based greases represent the fastest-growing base oil segment, expanding at approximately 6.5% CAGR, driven by automotive electrification, electric vehicle bearing specifications, high-speed machinery applications, regulatory emphasis on improved thermal stability, and extended service intervals.

- Key Market Opportunity: Development and commercialization of alternative thickener formulations, including polyurea and calcium sulfonate, represent primary growth opportunities, addressing lithium supply constraints while delivering superior performance characteristics, including extended service life, enhanced water resistance, and improved thermal stability for automotive manufacturing, construction equipment, and mining applications.

| Key Insights | Details |

|---|---|

|

Industrial Greases Market Size (2026A) |

US$ 6.3 Bn |

|

Projected Year Value (2033F) |

US$ 8.5 Bn |

|

Value CAGR (2026-2033) |

4.4% |

|

Historical Market Growth Rate (CAGR 2019 to 2023) |

3.5% |

Market Dynamics

Drivers - Expansion of Automotive Manufacturing and Electric Vehicle Production

The automotive sector represents the largest end-user segment for industrial greases, accounting for approximately 40% of global consumption. Traditional internal combustion engine vehicles continue generating substantial demand for chassis greases, bearing lubricants, and engine-related applications. However, the electric vehicle market emergence is fundamentally reshaping grease demand patterns. Electric vehicle production in Europe is projected to reach 3 million units by 2026, requiring specialized bearing greases capable of withstanding higher rotational speeds and electrical currents without degradation. ExxonMobil's 2024 specialty products division generated US$ 3.1 billion in earnings, substantially driven by improved basestock and finished lubricants margins reflecting robust automotive sector demand. Synthetic and polyurea-thickened greases deliver superior thermal stability and extended service intervals that align with sealed-for-life bearing specifications increasingly mandated by electric vehicle manufacturers.

Intensifying Industrial Automation and Equipment Maintenance Demands

Global industrial automation markets are projected to reach €200 billion by 2026, with Europe as a key player driving substantial demand for precision lubrication solutions. Advanced manufacturing facilities increasingly incorporate conveyor systems, robotic equipment, and high-speed machinery requiring specialized greases that maintain performance consistency across wide temperature ranges and extended relubrication intervals. North America's manufacturing sector reported 5% growth in industrial production, coupled with continued infrastructure modernization initiatives, generating persistent demand for high-performance lubrication products. Construction and mining equipment operating under harsh environmental conditions, including extreme temperatures, moisture exposure, and abrasive contamination mandate grease formulations delivering superior water resistance, mechanical stability, and anti-wear protection. This dynamic creates differentiated demand for complex metal soap and calcium sulfonate-thickened greases that inherently offer enhanced load-carrying capacity without requiring extensive additive packages.

Restraints - Lithium Supply Chain Vulnerabilities and Rising Raw Material Costs

The grease industry historically relied on lithium complex thickeners commanding 69% of the global market share, but recent supply disruptions have fundamentally altered competitive dynamics. Lithium extraction capacity constraints and competing demand from battery manufacturing have elevated lithium hydroxide monohydrate prices substantially, forcing grease manufacturers to absorb cost increases or reformulate products using alternative thickeners. Calcium sulfonate and polyurea thickener adoption is accelerating, but these alternatives typically command cost premiums of 20-30% compared to conventional lithium complex formulations. Smaller regional manufacturers in emerging markets lack the financial resources to absorb elevated raw material costs, creating margin compression and competitive vulnerability. Switching to alternative thickeners introduces compatibility complexities; polyurea greases demonstrate incompatibility with conventional lithium complex formulations, requiring customers to conduct thorough equipment validation before transitioning products, thereby delaying adoption timelines.

Environmental Regulations and Synthetic Oil Production Complexities

Stringent regulatory frameworks targeting volatile organic compound emissions have prompted transitions toward synthetic and bio-based greases, but manufacturing these advanced formulations demands specialized facilities and sophisticated process controls. Synthetic base oils including polyalphaolefins (PAO), polyalkylene glycols (PAG), and esters originate from limited global suppliers with constrained production capacity. Energy-intensive synthetic oil production creates vulnerability to electricity price volatility; the 2021 global shipping crisis demonstrated logistical fragility, with freight costs for chemical shipments surging over 500% year-on-year. Regulatory approval requirements for food-contact and aerospace-certified greases impose substantial documentation and testing burdens, restricting market entry for manufacturers lacking international certifications. California Air Resources Board regulations and analogous European standards accelerate synthetic grease adoption in regulated regions, creating regulatory fragmentation that disadvantages manufacturers operating across multiple jurisdictions with inconsistent requirements.

Opportunities - Polyurea and Calcium Sulfonate Thickener Substitution for Performance-Demanding Applications

Polyurea-thickened greases demonstrate service life extending 3-5 times longer than conventional lithium formulations, creating compelling value propositions for long-interval maintenance applications and sealed-bearing systems. These advanced thickeners possess inherently superior oxidation stability stemming from their non-metallic composition, delivering high-temperature performance equivalent to lithium complex greases without requiring extensive oxidation inhibitor additives. Calcium sulfonate complex thickeners exhibit inherent extreme-pressure and load-carrying performance, reducing additive requirements while simultaneously improving water resistance through enhanced moisture absorption capacity. Industrial applications including off-highway construction equipment, mining machinery, and heavy-duty vehicles, increasingly specify polyurea and calcium sulfonate formulations. European automotive production exceeding 15 million vehicles annually creates sustained demand for performance-differentiated greases that support extended maintenance intervals and reduced total cost of ownership calculations for fleet operators.

Emerging Demand from Renewable Energy and High-Speed Bearing Applications

Wind energy installations and photovoltaic systems generate substantial demand for specialized bearing greases operating reliably under continuous high-speed rotation in harsh environmental conditions. High-speed grease applications are expanding at approximately 12.7% annually, driven by generator bearing lubrication requirements in renewable energy installations and precision machinery in advanced manufacturing. Polyurea-formulated high-speed greases deliver superior heat dissipation, minimal oxidation degradation, and extended relubrication intervals essential for sealed bearing systems in remote wind installations where maintenance access proves costly. Mining and metallurgical operations continue generating significant grease demand, with equipment manufacturers specifying calcium sulfonate and aluminum complex thickener systems for extreme-temperature environments exceeding lithium formulation capabilities.

Category-wise Analysis

Base Oil Insights

Mineral oil-based greases command approximately 58-62% market share, driven by cost-effectiveness, established supply infrastructure, and proven performance across diverse industrial applications. Mineral-oil-based lubricants market project valuation reaching US$ 20.3 billion by 2034 at 5.1% CAGR, reflecting persistent demand from price-sensitive end-user segments and conventional manufacturing operations. Mineral oil greases deliver acceptable performance across moderate-temperature operating ranges and derive a competitive advantage from significantly lower pricing compared to synthetic alternatives. However, market share erosion continues as synthetic oils capture premium applications demanding superior thermal stability, extended service intervals, and environmental compliance. Synthetic base oils, including PAO and polyester formulations, are experiencing accelerated adoption, with thermal stability and oxidation resistance delivering justified cost premiums for high-performance applications.

Thickener Type Analysis

Lithium complex thickeners dominate with approximately 55% market share, maintaining leadership through superior performance consistency, established manufacturing infrastructure, and broad end-user familiarity. Lithium complex greases possess high dropping points, excellent mechanical stability, and demonstrated water resistance, though lithium supply constraints are gradually eroding market dominance. Calcium sulfonate complex thickeners command growing market participation at approximately 20-25% share, with annual growth rates reaching 9.10% as alternative to lithium, driven by inherent extreme-pressure capacity, superior water resistance, and improved thermal stability. Polyurea thickened greases represent 8-12% market share with accelerating adoption in sealed-bearing and high-temperature applications, offering extended service life and superior oxidation stability. Simple metal soaps and non-soap thickeners combined account for approximately 10-15% share, maintaining niche applications where specific performance requirements justify utilization despite superior alternatives.

End-user Analysis

Automotive manufacturing and related transportation applications command 40-45% market share, encompassing bearing lubrication, chassis greasing, and engine component protection. Automotive OEMs increasingly specify performance-differentiated greases addressing electric vehicle requirements, traditional combustion engine demands, and off-highway vehicle specifications. Off-highway construction equipment and mining operations account for 25-30% market share, requiring heavy-duty greases delivering extreme-pressure performance, water resistance, and thermal stability. Commercial manufacturing and industrial machinery applications represent 20-25% market share, encompassing conveyor systems, pump bearings, and precision equipment requiring consistent lubrication performance across extended operating periods.

Regional Insights

North America Industrial Greases Market Share

North America maintains a strong market position driven by advanced automotive sector, established manufacturing infrastructure, and high equipment maintenance standards. The U.S. manufacturing sector generated US$ 2.937 trillion of GDP in Q4 2024, reflecting robust industrial activity supporting sustained grease demand across automotive, aerospace, and heavy equipment applications. American automotive manufacturers accelerated the adoption of specialized bearing greases for electric vehicle production, with major OEMs establishing technical specifications mandating enhanced thermal stability and extended service intervals.

Federal manufacturing modernization initiatives and infrastructure investment programs generate incremental demand for grease products, supporting equipment reliability and maintenance efficiency across industrial networks. FDA and EPA regulatory frameworks establish stringent performance standards compelling manufacturers to maintain advanced product portfolios addressing environmental concerns while delivering superior equipment protection.

Europe Industrial Greases Market Trends

Europe dominates as a mature, highly regulated market with advanced environmental standards and specialized industrial requirements driving premium grease adoption. The European grease market is estimated at US$ 4.41 billion in 2026, growing at 3.11% CAGR toward US$ 5.63 billion by 2033, reflecting steady but moderate expansion driven by automotive sector modernization and industrial equipment maintenance demands. Germany maintains 23% European market share at US$ 1.5 billion in 2026, supported by an extensive specialized manufacturing infrastructure serving major European industrial operations. United Kingdom commands 17% share at US$ 1.1 billion, driven by comprehensive manufacturing programs implementing advanced grease management systems across industrial facilities. France holds 13.5% share at US$ 0.9 billion through specialized industrial facilities and advanced lubrication networks.

Electric vehicle production expanding toward 3 million units annually by 2026 creates differentiated demand for sealed-bearing greases meeting thermal and electrical isolation specifications. Renewable energy sector expansion, including wind turbine installations and high-speed generator systems, generates incremental demand for polyurea and calcium sulfonate-thickened formulations. Regulatory emphasis on sustainability drives adoption of bio-based and environmentally compliant greases, creating market segmentation favoring manufacturers with advanced formulation capabilities addressing both performance and environmental objectives.

Asia Pacific Industrial Greases Trends

Asia Pacific represents the fastest-growing regional market, driven by rapid industrialization, automotive manufacturing expansion, and emerging infrastructure development across China, India, and Southeast Asia. The region accounts for approximately 45-50% of global grease consumption by volume, reflecting its dominant position in global manufacturing networks and heavy equipment utilization. China emerges as the world's largest grease producer and consumer, with manufacturing modernization initiatives driving demand at approximately 4.0% CAGR through 2035.

India's rapidly expanding automotive and heavy equipment industries generate significant grease demand growth, with commercial integration of manufacturing facilities and construction equipment utilization accelerating synthetic and advanced thickener adoption. ASEAN member states including Vietnam, Indonesia, and Thailand demonstrate accelerating industrial production expansion, creating incremental demand for cost-effective greases balancing performance adequacy with price competitiveness. Regional manufacturing advantages including lower labor costs, abundant raw materials, and strategic geographic positioning, attract international manufacturers to establish regional production facilities and technical support networks.

Competitive Landscape

The industrial greases market exhibits a moderately consolidated competitive structure with major integrated oil companies and specialized lubricant manufacturers commanding significant market shares. BASF SE, Royal Dutch Shell plc, ExxonMobil Corporation, and Chevron Corporation maintain dominant positions through comprehensive product portfolios, advanced research capabilities, and global supply chain infrastructure enabling efficient distribution. ExxonMobil's Specialty Products division reported US$ 3.1 billion in 2024 earnings, substantially driven by improved basestock and finished lubricants margins, reflecting market leadership across automotive and industrial lubricant segments. Manufacturers compete through product differentiation emphasizing advanced thickener technologies, thermal stability performance, and extended service life capabilities. SKF, a major bearing and lubrication solutions provider, generated approximately €9.8 billion in annual revenue, leveraging integrated bearing-grease solutions, positioning where sealed-bearing systems increasingly demand compatible specialized lubricants.

Key Market Developments

- January 2025: ExxonMobil Corporation reported record specialty products earnings growth driven by improved basestock and finished lubricants margins, reflecting robust demand across automotive and industrial segments coupled with structural cost savings from operational efficiency initiatives.

- December 2024: Royal Dutch Shell plc expanded calcium sulfonate complex grease product portfolio, addressing market demand for alternatives to lithium-dependent formulations, targeting automotive and construction equipment applications requiring high-temperature and water-resistant performance.

Companies Covered in Industrial Greases Market

- Belray Company LLC

- Texaco Inc

- Exxon Mobil Corporation

- Whitmore Manufacturing Company

- Axel Christiernsson International AB

- Dow Corning Corporation

- Sinopec Lubricant Company

- Royal Dutch Shell plc

- Royal High-Performance Oil & Greases

- Industrial Oils Unlimited

- Other Market Players

Frequently Asked Questions

The global industrial greases market was valued at US$ 6.3 billion in 2026 and is projected to reach US$ 8.5 billion by 2033, representing a 4.4% CAGR during the forecast period.

Primary demand drivers include automotive manufacturing expansion, particularly electric vehicle production requiring specialized bearing lubricants, rapid industrial automation with €200 billion global market by 2025 necessitating precision lubrication solutions, construction and mining equipment operating under extreme conditions demanding high-performance greases, and regulatory emphasis on environmental compliance.

Lithium complex thickeners command approximately 55% market share due to proven performance consistency, established manufacturing infrastructure, and broad end-user familiarity, though market dominance is gradually eroding due to lithium supply constraints creating 9.10% annual growth in calcium sulfonate complex alternatives.

Asia Pacific dominates the global market, commanding 40% of total consumption, driven by China's position as the world's largest automotive and heavy equipment manufacturer, rapid industrialization across India and Southeast Asia, and accelerating infrastructure development projects requiring sustained lubrication solutions supporting equipment reliability.

Leading market participants include ExxonMobil Corporation, Royal Dutch Shell plc, BASF SE, Chevron Corporation, Sinopec Lubricant Company, FUCHS, BP p.l.c., SKF, Idemitsu Kosan, Petronas, TotalEnergies SE, and regional manufacturers including Belray Company LLC, Whitmore Manufacturing Company, and Axel Christiernsson International AB.