- HVAC

- Industrial Burner Market

Industrial Burner Market Size, Share and Growth Forecast for 2025 - 2032

Industrial Burner Market by Burner Type (Regenerative, High Velocity, Thermal Radiation, Radiant, Customized (Burner Boilers), Flat Flame, Line, Others), Burner Design (Mono Blocks, Duo-Block), Application (Boilers, Furnaces/Forges, Air Heating/Drying, Incineration, Others), Fuel Type, End-use Industry, and Regional Analysis from 2025 - 2032

Market Size and Share Analysis

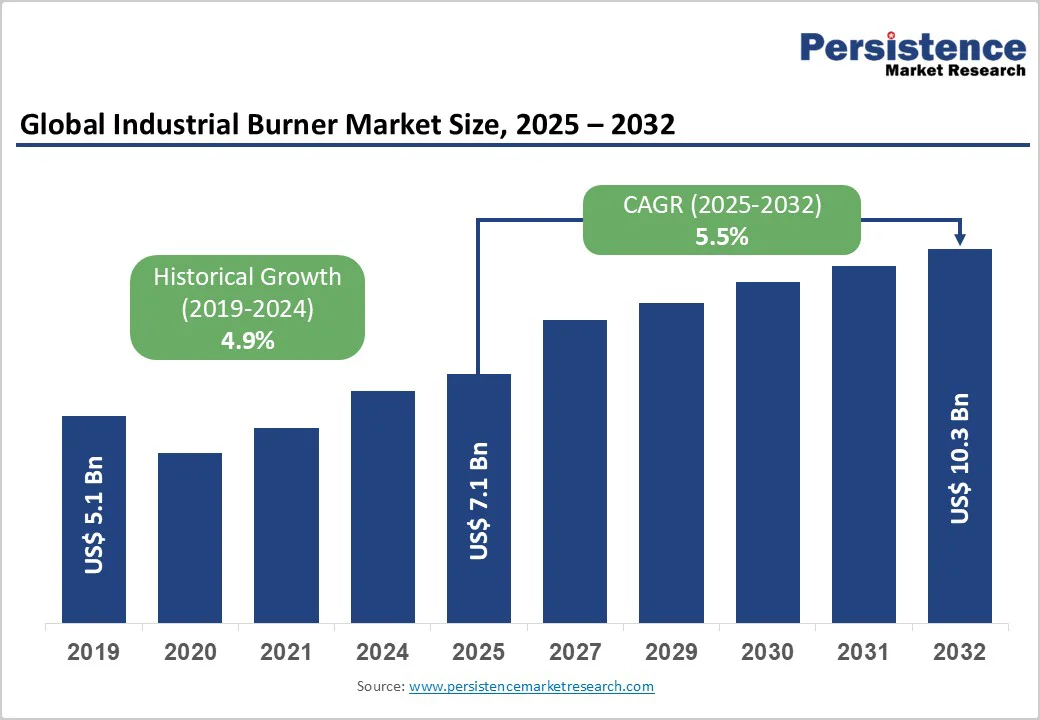

The industrial burner market size is likely to value US$ 7,089.4 million in 2025 and is projected to reach US$ 10,294.1 million at a CAGR of 5.5% during the period from 2025 to 2032. The market for industrial burners is expected to grow due to industrialization, mining, and petrochemical activities. Leading companies are also investing in burner capabilities to reduce pollution and carbon footprints.

Key Industry Highlights:

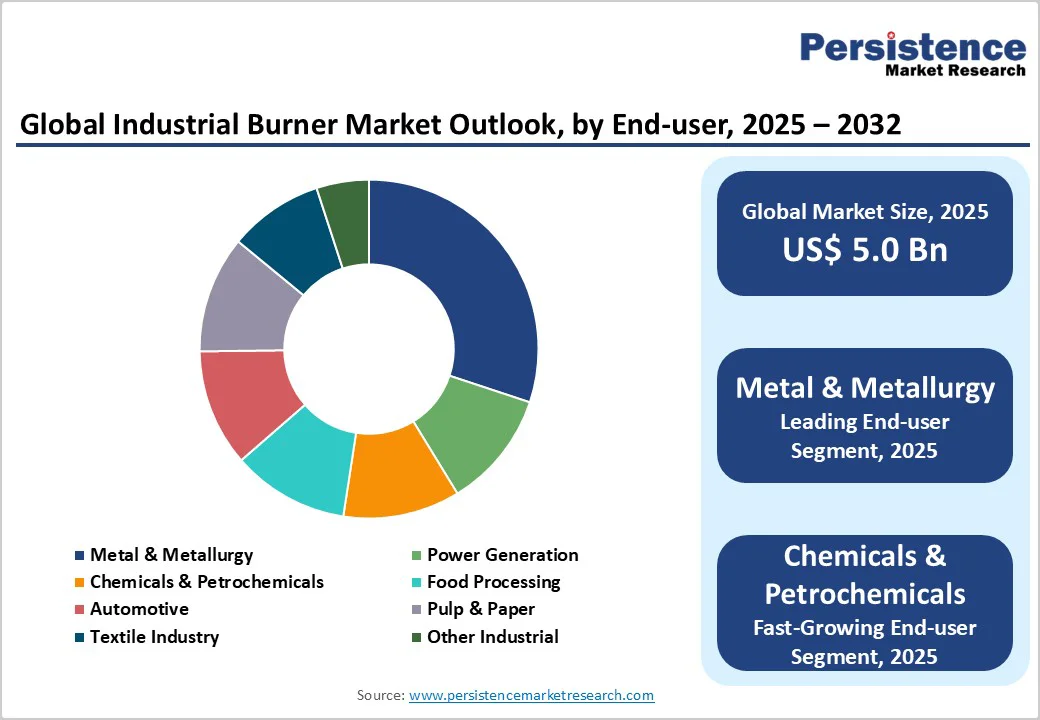

- Industry Leadership: Metal and Metallurgy segment dominates with over 25.3% projected market share by 2032, driven by extensive use of industrial burners in smelting, casting, and heat treatment processes requiring precise temperature control and energy efficiency.

- Burner Technology Dynamics: High-Velocity Burners lead the market with an anticipated CAGR of 5.8% through 2032, supported by their superior flame stability, high thermal efficiency, and ability to reduce emissions in demanding industrial environments.

- Manufacturing Innovation Trends: The advent of 3D printing technology is transforming burner production, enabling lightweight designs, improved combustion efficiency, and customized burner geometries that enhance performance and reduce material waste.

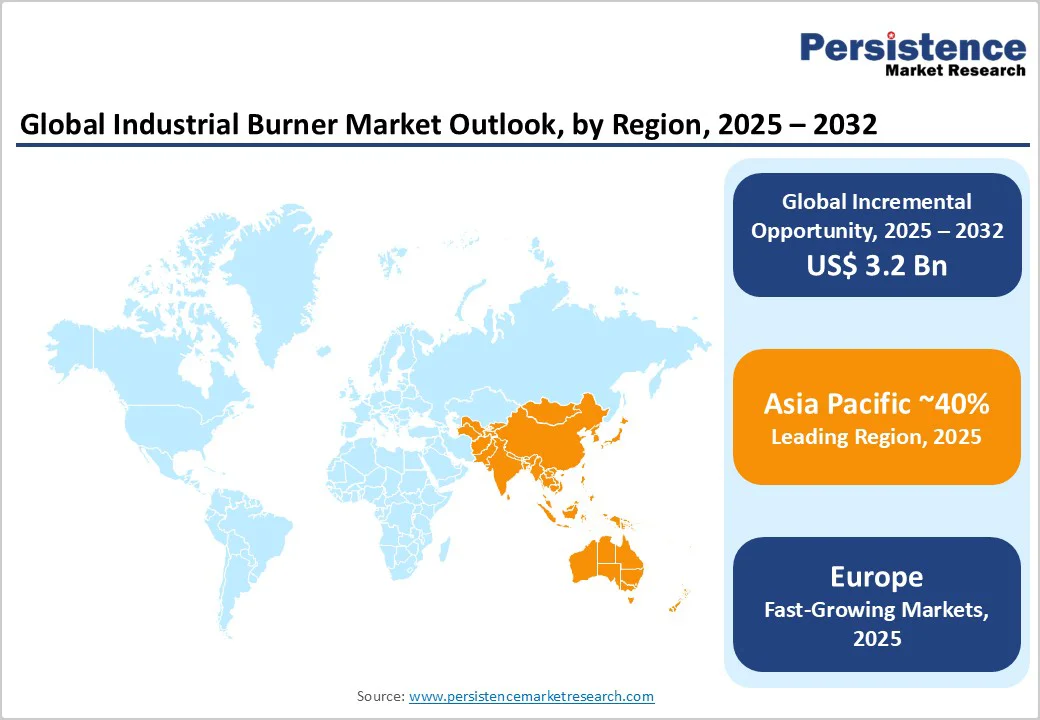

- Regional Market Dominance: Asia Pacific maintains substantial 73.4% market share in 2025, driven by rapid industrialization, mining expansion, and petrochemical activities, particularly in China and India, supported by large-scale manufacturing growth.

- Regional Growth Outlook: North America exhibits significant growth potential led by modernization of industrial facilities and adoption of low-NOx, energy-efficient burner technologies aligned with stringent emission norms.

- Country-Level Performance: China is projected to capture over 57.2% of East Asia’s industrial burner market by 2032, while the U.S. market expands at a robust CAGR of 5.6%, reflecting investment in advanced combustion solutions and clean energy transition initiatives.

| Key Insights | Details |

|---|---|

|

Market Size (2025E) |

US$ 7,089.4 Mn |

|

Projected Market Value (2032F) |

US$ 10,294.1 Mn |

|

Global Market Growth Rate (CAGR 2025 to 2032) |

5.5% |

|

Historical Market Growth Rate (CAGR 2019 to 2023) |

4.9% |

Rapid Industrialization Sets Apart Asia Pacific Industrial Burner Market to Grow Substantially

Asia Pacific is poised to dominate the industrial burner market and anticipated to hold a substantial 73.4% market share in 2025. This surge is driven by growing industrialization, mining, and petrochemical activities, particularly in China and India.

Asia Pacific market is projected to achieve a remarkable CAGR of 5.6% in 2025, driven by increased applications in steam boilers, heat exchangers, and hot water systems showcasing the region's expanding industrial capabilities.

China is expected to account for over 57.2% of East Asia market by 2032. With an industry value added exceeding $6.92 trillion, China is one of the world's largest consumers of industrial burners. The global manufacturers are investing more in product innovation to expand their market reach globally. For instance,

- In March 2025, Oilon has introduced the LN30 ultra-low NO? burner, achieving emissions below 20 mg/Nm³ without external flue-gas recirculation. Utilizing partly-premixed combustion and CFD-optimized design, it ensures high efficiency, low maintenance, and compliance with stringent EU emission standards. The burner sets a new benchmark for retrofits and new industrial heating systems.

North America Industrial Burner Market to Retain the Top Position

|

Country |

CAGR through 2032 |

|

U.S. |

5.6% |

North America is set to experience the significant growth in the market in the coming years, driven by rising demand across various sectors like power generation, chemicals, and food and beverages. The focus on sustainability and energy efficiency is accelerating the adoption of low-energy systems, with the U.S. industrial burner market growing substantially with a CAGR of 5.6% through 2032. The market players are also investing in the product development for better energy efficiency. For instance,

- In January 2025, Superior Boiler’s Cheyenne High-Efficiency Condensing Boiler and Weishaupt’s Ultra-Low NOx (ULN) burner package are transforming the heating industry with a focus on efficiency, flexibility and environmental responsibility.

Recent regulations from the U.S. Environmental Protection Agency have significantly improved burner design standards, encouraging manufacturers to develop low-emission and high-efficiency burners further boosting the market expansion.

Demand to Remain High for High Velocity Burners

|

Category |

CAGR through 2032 |

|

Burner Type - High Velocity Burners |

5.9% |

High-velocity burners are projected to lead the industrial burner market over the forecast period, with demand expected to grow at a CAGR of 5.9%. These burners are essential in applications requiring a high rate of recirculation of combustion products. They achieve excellent heat penetration by generating a high-velocity stream of hot gases within a furnace, resulting in enhanced efficiency and reduced fuel costs.

The manufacturers are increasingly investing in the high velocity burners to expand their portfolio and market reach. For instance,

- In November 2023, Fives Group launched e-Ductflame™, a revolutionary electric/gas hybrid system intended for a wide range of applications, whether replacing existing duct burners or integrating into new installations. It has been designed to cut carbon emissions and improve the efficiency of industrial heating processes with minimum costs involved.

According to the U.S. Department of Energy, utilizing high-velocity burners can significantly improve industrial energy efficiency, further driving widespread adoption globally.

Metal & Metallurgy Segment to Take Control by Housing Metal Production Facilities

|

Category |

Market Share in 2025 |

|

End-use Industry - Metal & Metallurgy |

25.3% |

The metal and metallurgy sector is projected to capture over 25.3% of the industrial burner market by 2032. Industrial burners play a crucial role in steel, aluminum, and other metal production facilities, making this sector a significant contributor to the global market. For instance,

- In August 2023, Industrial leader Fives, with over 100 years of expertise in industrial combustion, launched its first 100% hydrogen duct burner. The Hy-Ductflam™ is a key step towards the decarbonization of heating and drying processes worldwide as hydrogen emits zero carbon when burnt. Designed for new installations or to replace standard duct burners, Fives’ solution can be easily implemented by manufacturers with very limited process modification.

The U.S. Department of Commerce reports that advancements in burner technology are essential for enhancing energy efficiency and reducing emissions in metal production further solidifying the industry's importance in the market landscape.

Market Introduction and Trend Analysis

The market is fueled by several industry trends and factors. Industrial burners are specialized devices designed to generate heat through the combustion of fuel. These burners are essential in sectors including food processing, metalworking, and petrochemicals, where high-temperature applications are required. Their efficiency and ability to operate in different capacities make them invaluable tools for enhancing productivity and reducing energy consumption in industrial processes.

The industrial burner market is showing a surge in demand, particularly in South Asia. This growth is driven by robust industrial growth in India and ASEAN countries. The region's increasing energy needs and rising activities in automotive production and mining are greatly contributing to market expansion.

Industrial burner sales currently account for 30% to 40% of the burner market share. As industries increasingly focus on sustainability, innovations in burner technology that promote energy efficiency and reduce emissions are becoming pivotal. This trend highlights the industry's adaptability to evolving regulatory standards and growing environmental concerns, positioning it for sustained growth in the coming years.

Historical Growth and Course Ahead

Between 2019 and 2023, the industrial burner market exhibited a 4.9% CAGR. This increase can be largely attributed to the rebound in manufacturing and industrial activities following the COVID-19 pandemic in 2020.

For years, managing the fuel-to-air ratio has been a crucial challenge in large-scale industrial applications. Today, nearly every industrial burner comes equipped with advanced electronic modules that facilitate precise control of this ratio. Leading companies are taking advantage of technologies to expand their product line. For example,

- Baltur revamped its TB series (600–3600?kW) with modernized mechanical and electrical systems, streamlined models, and improved installation. Enhancements include ultra-efficient motors, revised structure and manuals, and reduced NO? emissions (<50?mg/Nm³, aiming for <30?mg/Nm³). Gas, diesel, and mixed-fuel versions began rolling out in 2024, completing by mid?2025.

The demand for industrial burners is projected to expand at a CAGR of 5.5% from 2025 to 2032 with new advancements. Regenerative power generation emerges as a foundational element of the future energy system with industrial burners playing a pivotal role in energy efficiency and sustainability.

Market Growth Drivers

Growing Investments in Burners Strain to Lower Carbon Footprints

Leading companies in the industrial burner sector are ramping up investments to enhance burner capabilities. It focuses on reducing pollutant levels and minimizing carbon footprints. With increasing regulatory pressures and a push for sustainability, burners that can significantly lower greenhouse gas emissions, such as nitrogen oxides (NOx) present substantial opportunities for market players. For example,

- A recent innovation by General Electric, launched in early 2023, has demonstrated the ability to achieve NOx emissions as low as 6 ppm when adjusted for 3% O2. This breakthrough is particularly beneficial for applications like Once-Through Steam Generators (OTSGs) and Enhanced Oil Recovery (EOR). As the industry strives for cleaner technologies, such advancements are crucial for compliance and operational efficiency.

Surging Electricity Demand Fuels the Demand for Industrial Burners

The electricity demand is rising greatly worldwide, and China leads the world in electricity consumption with a staggering 9,445 terawatt-hours (TWh) in 2023. This figure is more than double that of the second largest consumer. The United States ranks second, with an electricity demand of around 4,268 TWh. Meanwhile, India ranks third and shows rapid electricity demand growth due to its expanding economy and population.

According to the International Energy Agency (IEA), global electricity demand is forecasted to grow at an annual rate of 2.1% through 2040, double the growth rate of primary energy demand. Rising incomes, expanding industrial production, and a growing services sector are key drivers behind this trend.

Power plants rely on various fuels to generate high-pressure steam, making industrial burners essential components in this process. For instance,

- Siemens launched their latest gas turbine, the SGT-8000H, in early 2022, designed to optimize efficiency and reduce emissions in power generation, further propelling the demand for industrial burners.

Factors Impeding the Market

The Capital-Intensive Production of Industrial Burners Hinders the Growth

Producing boiler-based industrial burners is a capital-intensive endeavor that demands meticulous planning. Companies must prioritize the identification of economically viable raw materials with a reliable long-term supply. This process involves significant research and development (R&D) investments, as well as securing auxiliary components for industrial boilers. For instance,

- In 2022, Bosch launched its new modular boiler system aimed at improving efficiency and reducing costs highlighting the need for innovation in this sectors.

The construction of industrial boiler plants incurs substantial expenses related to engineering, procurement, and construction (EPC) services, alongside technology investments and fuel procurement. Moreover, ongoing maintenance and after-sales services also require hefty capital.

The cost of industrial boilers can vary widely based on design and support levels, with budget options often leading to shorter lifespans and less customer support. These factors collectively drive up the overall procurement and maintenance costs of industrial burners.

Demand for Advanced Industrial Burners Impacts Strain Producers

Industrial burners come in a diverse range of capacities, from 40 kW to over 30,000 kW, catering to various operational needs. Once these burners are installed, plant operators are tasked with optimizing their efficiency. However, many operators need to recalibrate their heating requirements, often pushing the limits of their existing systems. In response to this challenge, manufacturers are innovating by developing industrial burners with multi-stage capacity regulation capabilities. For instance,

- In January 2025, Superior Boiler’s Cheyenne High-Efficiency Condensing Boiler and Weishaupt’s Ultra-Low NOx (ULN) burner package are transforming the heating industry with a focus on efficiency, flexibility and environmental responsibility.

As the need for flexible capacity management grows, producers face increasing pressure to deliver advanced solutions that meet these evolving requirements ensuring they remain competitive in a dynamic market.

Future Opportunities for the Market Players

3D Printing Technology Revolutionizes Industrial Burners

The advent of 3D printing technology is transforming the production of industrial burners, significantly reducing costs while enabling the creation of complex designs. For instance,

- Companies like Euro-K GmbH, headquartered in Germany, have harnessed this technology since its launch of advanced micro-burners. These compact burners enhance fuel consumption and offer remarkable performance flexibility by efficiently mixing fuel and air, allowing them to combust both gas and liquid fuels.

3D-printed burners are increasingly utilized in the marine sector, where they play a crucial role in injecting diesel or oil into furnaces that ignite ship boilers. This process generates steam to power turbines that propel vessels. As industries continue to adopt innovative manufacturing techniques, the demand for sophisticated burners developed through 3D printing is expected to grow, opening up exciting opportunities in various sectors.

Environmental Regulations Influence the Industrial Burner Market Growth

Environmental concerns and stringent emissions regulations are significantly shaping the global industrial burner market.

Governments and international organizations are increasingly focused on reducing air pollutants and greenhouse gas (GHG) emissions from industrial operations. For instance, The U.S. Environmental Protection Agency (EPA) has set ambitious targets to cut GHG emissions by 50% by 2030, prompting industries to invest in cleaner combustion technologies. As a result, burners with low nitrogen oxide (NOx) and carbon emissions have become essential for regulatory compliance.

Companies like Honeywell, based in Morris Plains, New Jersey, launched their SMART Burner, designed to minimize emissions while maximizing efficiency. The market is also witnessing a shift toward eco-friendly solutions such as regenerative burners and flue gas recirculation systems. These are crucial for reducing the environmental impact of industrial processes and driving market growth.

Competitive Landscape for the Industrial Burner Market

Top industrial burner manufacturers are increasingly committed to developing high-performance, low-emission, and connected burners. The rise of automation and Industry 4.0 is driving these companies to incorporate cutting-edge technologies and features into their products. For example,

- The US Department of Energy has announced a $30 million funding opportunity to improve domestic manufacturing of materials for wind turbines. This funding could reduce wind energy costs and expand the US's wind energy portfolio, supporting goals for 100% clean electricity by 2035 and a net-zero-emissions economy by 2050.

Despite the focus on advanced solutions, the market comprises many small to medium-sized players dedicated to providing cost-effective industrial burners. These companies cater to businesses seeking reliable and budget-friendly options ensuring a diverse range of products is available to meet various customer needs.

Recent Developments in the Industrial Burner Market

- In October 2024, ClearSign Technologies Corporation completed the Ultra low NOx Burner Testing study by the California Gas Emerging Technologies (GET) Program, sponsored by Southern California Gas Company. The report concluded that the ClearSign ultra-low NOx burner demonstrated material fuel and electricity savings while producing ultra-low NOx levels. It was also capable of NOx levels lower than the baseline burner. The study translates into approximately $80k per year savings in California energy costs for a mid-size 500hp boiler compared to a comparable industry standard burner technology.

- In August 2024, Buhler India introduced two solutions for biscuit manufacturers to cater to growing demand in the region. The DirectBake Smart, a direct-fired oven, and the RotaMold Smart, a rotary molder, are part of the SmartLine series. Both use Buhler's recipe-controlled burner system technology and are reliable, versatile, and efficient. The DirectBake Smart is part of a global collaborative development program that was designed and produced in India.

Industrial Burner Industry Segmentation

By Burner Type

- Regenerative Burners

- High Velocity Burners

- Thermal Radiation

- Radiant Burners

- Customized (Burner Boilers)

- Flat Flame Burners

- Line Burners

- Others

By Burner Design

- Mono Blocks

- Single Stage

- Two Stage

- Duo-Block

By Application

- Boilers

- Furnaces/Forges

- Air Heating/Drying

- Incineration

- Others

By Fuel Type

- Gas Burners

- Oil Burners

- Duel Fuel Burners

By End-use Industry

- Metal & Metallurgy

- Power Generation

- Chemicals & Petrochemicals

- Food Processing

- Automotive

- Pulp & Paper

- Textile Industry

- Other Industrial

By Region

- North America

- Europe

- East Asia

- South Asia and Oceania

- Latin America

- The Middle East & Africa

Companies Covered in Industrial Burner Market

- John Zink Hamworthy Combustion

- Fives Group

- Maxon Corporation

- Eclipse, Inc.

- Weishaupt Group

- Baltur S.p.A.

- Oilon Group

- ANDRITZ AG

- Selas Heat Technology Company LLC

- Forbes Marshall

- Riello S.p.A.

- ESA Pyronics International

- Baelz Automatic GmbH

- Bloom Engineering

- HORN Glass Industries AG

- IBK Enzberg GmbH

- Ecoflam S.p.A.

- Tenova S.p.A.

- SAACKE GmbH

Frequently Asked Questions

The market is predicted to rise from US$ 6.4 Bn in 2024 to US$ 9.18 Bn by 2031.

Burners are employed in different sectors such as metal production, food processing, petrochemicals, and pharmaceuticals.

Maxon Corporation, Eclipse, Inc., Weishaupt Group, Oilon Group, and ANDRITZ AG are some leading manufacturers.

Industrial burners are used in different manufacturing industries such as automotive, food and beverage, petrochemical and more.

The high-velocity burner segment is estimated to lead the market exhibiting a CAGR of 3.9% through 2031.