- Pharmaceuticals

- Human Immunodeficiency Virus Therapeutics Market

Human Immunodeficiency Virus Therapeutics Market Size, Share, and Growth Forecast 2026 - 2033

Human Immunodeficiency Virus Therapeutics Market by Drug Class (Nucleoside Reverse Transcriptase Inhibitors, Non-Nucleoside Reverse Transcriptase Inhibitors, Protease Inhibitors, Integrase Inhibitors, Entry & Fusion Inhibitors), Therapy Type (Antiretroviral Therapy, Pre-Exposure Prophylaxis, Post-Exposure Prophylaxis, Long-acting Injectable Therapies), Drug Type (Branded Drugs, Generic Drugs), by Distribution Channel (Hospital Pharmacies, Retail Pharmacies, Online Pharmacies), and Regional Analysis, 2026-2033

Human Immunodeficiency Virus Therapeutics Market Share and Trends Analysis

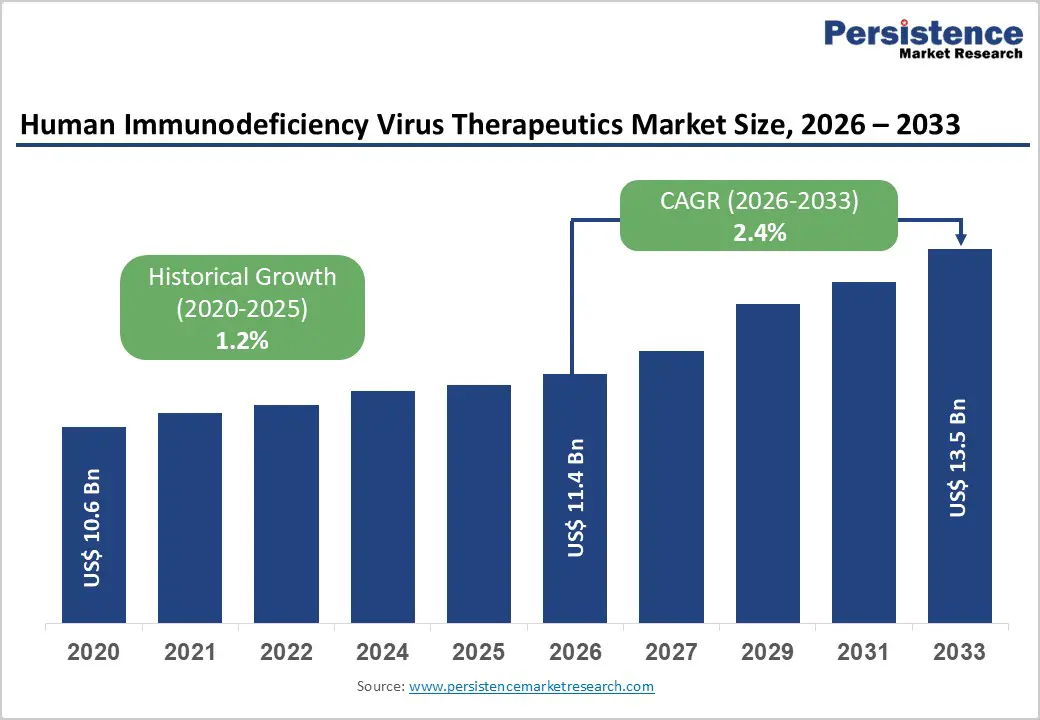

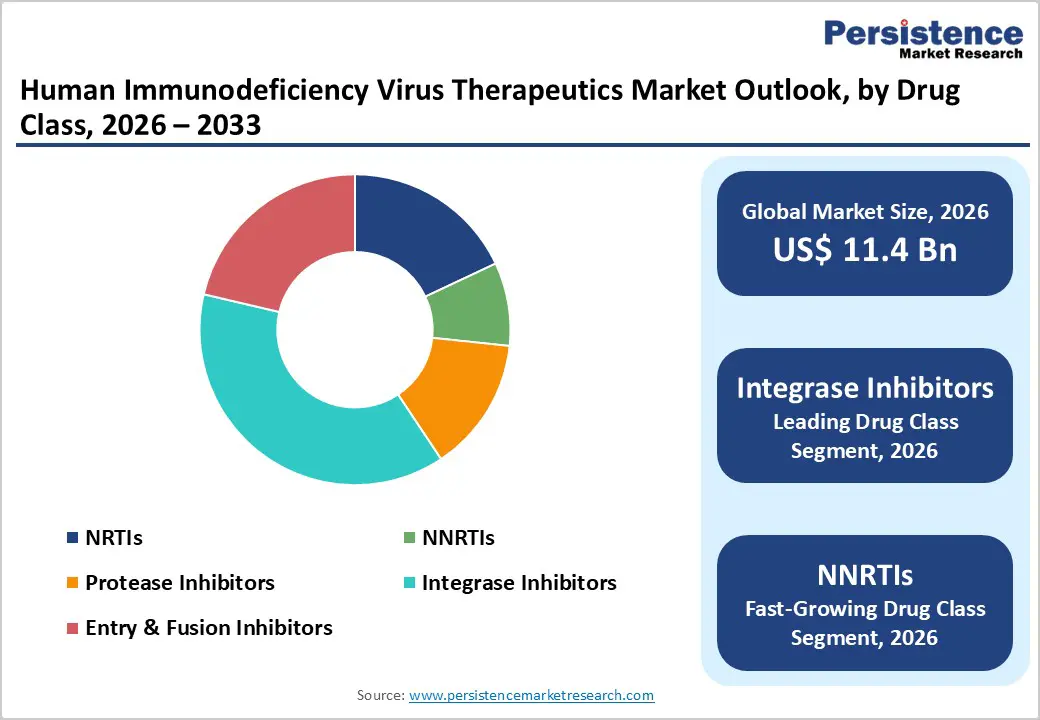

The global human immunodeficiency virus therapeutics market size is expected to be valued at US$ 11.4 billion in 2026 and projected to reach US$ 13.5 billion by 2033, growing at a CAGR of 2.4% between 2026 and 2033. The market is driven by expanding treatment access globally, with approximately 31.6 million people (77% of all people living with HIV) now accessing antiretroviral therapy as of 2024, representing a significant increase from 7.7 million in 2010.

Additionally, the approval and commercialization of innovative long-acting injectable therapies, such as cabotegravir and the twice-yearly injectable lenacapavir, have revolutionized treatment options and prevention strategies. The rising prevalence of HIV, coupled with increased government initiatives and public health programs to expand treatment coverage, continues to create sustained demand for HIV therapeutics across all regions.

Key Industry Highlights:

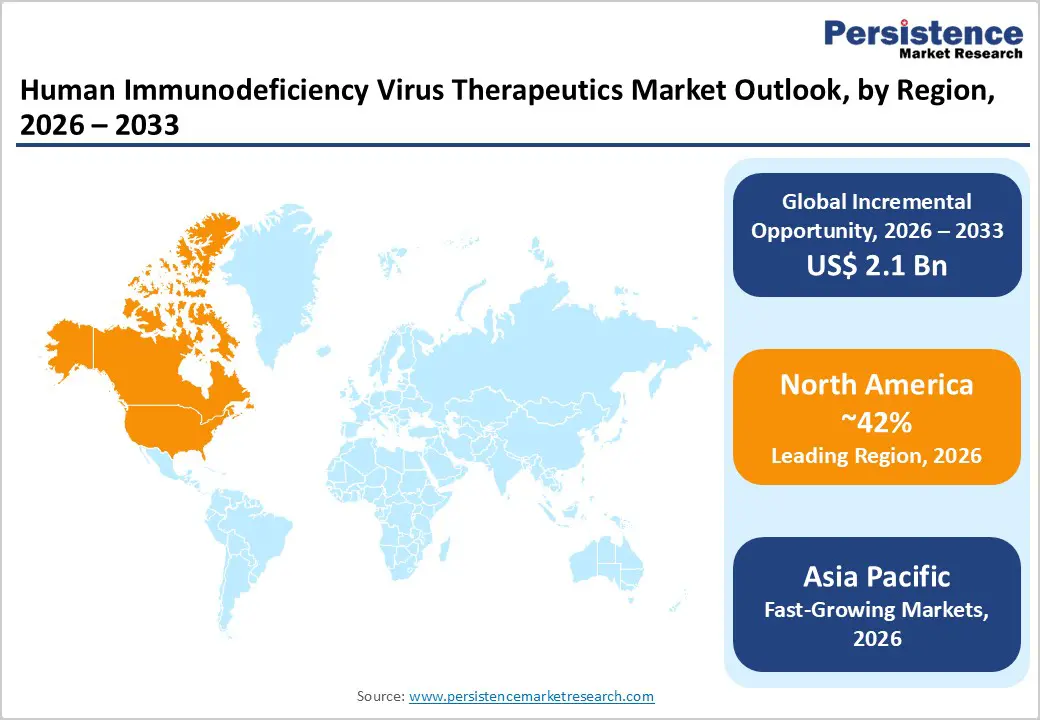

- The North American region dominates the HIV therapeutics market, accounting for 42% of the market in 2025, driven by advanced healthcare infrastructure, robust pharmaceutical innovation capacity, comprehensive treatment access programs, and the highest global disease treatment coverage rates among developed nations.

- Asia Pacific represents the fastest-growing regional market, projected to expand at approximately 3.2% compound annual growth rate between 2025 and 2032, driven by expanding disease prevalence, increasing treatment access initiatives, and a dominant position in generic drug manufacturing and export capacity.

- Integrase inhibitors dominate the drug class segment, commanding a 38% market share in 2025 through superior efficacy profiles, high barriers to viral resistance, and favorable safety profiles, establishing them as the preferred first-line treatment across developed and emerging healthcare systems.

- Non-nucleoside reverse transcriptase inhibitors are the fastest-growing drug class, driven by ongoing research and development that has yielded novel agents with enhanced efficacy and substantially reduced adverse-effect profiles compared with earlier-generation agents.

| Key Insights | Details |

|---|---|

| Human Immunodeficiency Virus Therapeutics Market Size (2026E) | US$ 11.4 billion |

| Market Value Forecast (2033F) | US$ 13.5 billion |

| Projected Growth CAGR (2026-2033) | 2.4% |

| Historical Market Growth (2020-2025) | 1.2% |

Market Dynamics

Drivers - Ongoing Progress and Novel Developments in the Development of Antiretroviral Drugs

Ongoing progress and novel developments in antiretroviral drug development substantially drive the exponential expansion of the global HIV therapeutics market. In the ever-changing realm of pharmaceutical research, the development and effectiveness of medications intended for the management and treatment of HIV/AIDS have undergone a significant transformation. Antiretroviral therapy (ART) has been a fundamental component in the global battle against HIV; continuous scientific investigations strive to improve the drugs' efficacy, toleration, and availability.

Over the past few years, significant advances have been made in developing innovative antiretroviral medications that address issues such as drug resistance, adverse effects, and administration protocols. Scientists are developing drugs with enhanced bioavailability, prolonged half-lives, and reduced toxicity to increase treatment adherence and reduce the likelihood of resistance. A noteworthy advancement pertains to the creation of integrase inhibitors, which are a category of antiretroviral medications designed to obstruct the integration of viral DNA into the genome of the host cell by selectively targeting the viral integrase enzyme. Viral replication suppression has been remarkably facilitated by this class of medications, which also have a favorable profile of adverse effects.

Innovation in Long-Acting Injectable Formulations

The emergence of long-acting injectable therapies represents a transformative growth driver reshaping the HIV therapeutics landscape. In June 2025, Gilead Sciences received FDA approval for Yeztugo (lenacapavir), a twice-yearly subcutaneous injectable that demonstrated 100% efficacy in preventing HIV infections among 2,134 participants in clinical trials. ViiV Healthcare's cabotegravir-based therapies, including Apretude for pre-exposure prophylaxis and Cabenuva for treatment, have also gained significant traction. These formulations address critical patient adherence challenges by reducing pill burden and requiring only 6-12 injections annually, compared to daily oral regimens. Data from clinical studies demonstrate that 89% of treatment-naïve individuals prefer switching to long-acting injectable cabotegravir from daily oral medications.

Restraints - Drug Resistance and Viral Mutation Challenges

HIV's ability to develop resistance to antiretroviral medications remains a significant market restraint. According to the World Health Organization's 2024 HIV drug resistance report, resistance rates among individuals receiving dolutegravir-based therapy with detectable viremia range from 3.9% in people without viral suppression for at least nine months to 19.6% in people with heavy prior treatment experience. This resistance barrier necessitates continuous development of new drug classes and combination therapies, imposing substantial research and development costs on manufacturers. Additionally, the emergence of resistant viral strains complicates treatment strategies and limits the longevity of existing therapeutic agents, potentially reducing market predictability for pharmaceutical companies.

Limited Access in Low and Middle-Income Countries

Despite significant progress, equitable access to HIV therapeutics remains severely constrained in resource-limited regions. The UNAIDS reports that while 77% of people living with HIV access treatment globally, coverage varies dramatically by region, with certain Asian and African countries maintaining treatment access below 50%. Central and Eastern European countries face particular challenges, with treatment coverage targets substantially below the 95% WHO goal. Generic drug availability and affordability issues persist despite licensing agreements between companies like ViiV Healthcare, GSK, and the Medicines Patent Pool. Manufacturing timelines for generic formulations can extend 3-5 years, delaying cost-reduction benefits in low-income nations and constraining overall market growth in developing regions.

Opportunity - Expansion of Generic Long-Acting Injectable Manufacturing

The licensing of long-acting injectable cabotegravir manufacturing to generic producers represents a substantial market opportunity. In July 2025, the Medicines Patent Pool extended its licensing agreement with ViiV Healthcare to include generic production of long-acting cabotegravir and rilpivirine for treatment use across 133 low- and middle-income countries. Generic manufacturers Aurobindo Pharma Limited, Cipla Limited, and Viatris Inc. are now producing these formulations in India and South Africa, with manufacturing capacity expected to increase significantly through 2026-2028. This development is projected to expand treatment access to millions of patients across sub-Saharan Africa, Asia Pacific, and Latin America, creating substantial revenue opportunities for both multinational and generic manufacturers. The WHO's endorsement of long-acting cabotegravir-rilpivirine combinations as treatment options has further accelerated market expansion potential.

Growing Focus on Collaborative Endeavors and Public-Private Partnerships

An opportunistic factor propelling the worldwide HIV therapeutics market is the growing focus on collaborative endeavors and public-private partnerships as a means to tackle the complex challenges linked to HIV/AIDS. In light of the epidemic's complex characteristics and the imperative for comprehensive solutions, collaborative efforts have intensified among governments, pharmaceutical corporations, non-profit organizations, and international organizations. By leveraging the distinct capabilities of each sector, these partnerships promote innovation, expand treatment access, and advance the development of HIV therapeutics.

Research and development are significantly aided by public-private partnerships, which facilitate the discovery and manufacture of novel antiretroviral medications. These partnerships expedite the development of innovative therapies by leveraging the global reach and public health emphasis of governmental and non-profit organizations in conjunction with the resources and expertise of pharmaceutical companies. Collaborations frequently involve technology transfer, collaborative funding, and knowledge exchange; these elements facilitate a more streamlined and effective drug development process. Consequently, the market benefits from a wide array of pharmaceuticals that address evolving challenges, including drug resistance and the demand for streamlined treatment protocols.

Category-wise Analysis

Drug Class Insights

Integrase inhibitors represent the dominant drug class in the HIV therapeutics market, commanding approximately 38% of total market share in 2025. Second-generation integrase strand transfer inhibitors including dolutegravir and bictegravir have become the preferred first-line treatment agents due to their superior efficacy profiles, high resistance barriers, and favorable safety tolerability characteristics. Gilead Sciences' Biktarvy (bictegravir/emtricitabine/tenofovir alafenamide), a single-tablet integrase inhibitor-based triple therapy regimen, has achieved dominant market positioning backed by extensive clinical trial data spanning five years. The class's dominance reflects healthcare provider preference for potent, convenient, and well-tolerated agents that can suppress viral replication and maintain long-term treatment efficacy in both treatment-naïve and treatment-experienced patients.

Therapy Type Insights

Antiretroviral therapy represents the leading therapy type, representing the fundamental treatment approach for managing HIV infection and maintaining long-term viral suppression in approximately 31.6 million people globally. Combination antiretroviral regimens utilizing two or three drug classes simultaneously have become the standard treatment paradigm, preventing viral resistance and maximizing treatment durability. The success of modern ART is demonstrated across the WHO European Region where more than 90% of treated individuals achieve viral suppression. Emerging therapy types, including long-acting injectable antiretroviral therapy and novel capsid inhibitors, are gaining momentum, but conventional oral ART regimens continue to dominate due to their established efficacy, extensive clinical experience, regulatory approval across all jurisdictions, and substantially lower cost compared to emerging long-acting formulations.

Distribution Channel Insights

Hospital pharmacies represent the leading distribution channel for HIV therapeutics, commanding the largest market share in 2025 due to favorable infrastructure, specialized clinical expertise, and ready availability of novel drugs. Patients prefer hospital-based treatment due to the presence of skilled infectious disease professionals, comprehensive multidisciplinary care teams, and immediate access to advanced therapeutic options. Hospital pharmacies maintain updated inventories of latest-generation antiretrovirals and long-acting injectables, enabling rapid treatment optimization and adherence support. Retail pharmacies are emerging as the fastest-growing distribution channel, expanding market penetration through specialized services including free home delivery, 24/7 accessibility, enhanced patient counseling, and competitive generic pricing. In the United States, retail pharmacy infrastructure ensures that at least one pharmacy is within 5 miles of most households, thereby improving medication access and adherence among geographically dispersed patient populations.

Regional Insights

North America Human Immunodeficiency Virus Therapeutics Market Trends and Insights

North America dominates the HIV therapeutics market with 42% market share in 2025, driven by the United States' substantial disease burden, advanced healthcare infrastructure, and robust pharmaceutical innovation ecosystem. The region is home to leading pharmaceutical companies including Gilead Sciences, Inc., Merck & Co., Inc., Johnson & Johnson (Janssen Pharmaceuticals), ViiV Healthcare, and Bristol-Myers Squibb Company, which collectively drive market innovation and maintain cutting-edge treatment development pipelines. The U.S. healthcare system demonstrates highest treatment coverage among developed nations, with government programs including Medicare, Medicaid, and the U.S. President's Emergency Plan for AIDS Relief (PEPFAR) facilitating broad access to antiretroviral therapy.

Asia Pacific Human Immunodeficiency Virus Therapeutics Market Trends and Insights

Asia Pacific emerges as the fastest-growing regional market, with projected CAGR of approximately 3.2% between 2025-2032, driven by expanding HIV treatment programs and increasing disease prevalence in nations including India, China, and Indonesia. The region represents home to 6.9 million people living with HIV as of 2024, with approximately 69% accessing antiretroviral therapy, creating substantial unmet treatment needs and market expansion opportunities. India dominates generic HIV drug manufacturing and export globally, with manufacturers Cipla Limited, Aurobindo Pharma Ltd., and Hetero Drugs Limited providing cost-effective alternatives that facilitate treatment access across sub-Saharan Africa, Asia Pacific, and Latin America.

Generic cabotegravir long-acting injectable manufacturing capacity is expanding rapidly in India through licensing agreements with Aurobindo, Cipla, and Viatris, supporting WHO's treatment recommendations for long-acting injectable combinations. Affordability remains a critical market access barrier in many Asia-Pacific countries, particularly among low-income and vulnerable populations. Manufacturing investments announced in 2025, including Blanver's R$592 million investment in constructing a third HIV medication production plant in Brazil (with similar expansion occurring across Asia), are expected to double production capacity by end of 2025, significantly reducing costs and expanding geographic accessibility through retail pharmacy channels.

Competitive Landscape

The human immunodeficiency virus (HIV) therapeutics market is highly competitive, driven by continuous innovation in treatment regimens and formulation improvements. Competition centers on efficacy, safety, tolerability, and convenience, with long-acting and combination therapies gaining traction over older treatments. Pricing pressures from generic entrants and evolving treatment guidelines intensify competitive dynamics, especially in mature markets. R&D investment focuses on next-generation agents, improved resistance profiles, and prevention strategies like PrEP and injectables.

Key Developments:

- In February 2025, Argobio and the Institut Pasteur launched Enodia Therapeutics, a groundbreaking French biotech company dedicated to blocking and degrading disease-causing proteins for the treatment of cancer, inflammatory diseases, and viral infections.

Companies Covered in Human Immunodeficiency Virus Therapeutics Market

- Gilead Sciences, Inc.

- ViiV Healthcare

- Merck & Co., Inc.

- Johnson & Johnson (Janssen Pharmaceuticals)

- AbbVie Inc.

- Bristol-Myers Squibb Company

- Cipla Limited

- Teva Pharmaceutical Industries Ltd.

- Viatris Inc.

- Aurobindo Pharma Ltd.

- Hetero Drugs Limited

- Sun Pharmaceutical Industries Ltd.

Frequently Asked Questions

The global Human Immunodeficiency Virus Therapeutics market is expected to be valued at US$ 11.4 billion in 2026, representing steady market expansion driven by expanding treatment access, innovative long-acting formulations, and increasing government health initiatives supporting antiretroviral therapy deployment across developing and developed nations.

The primary demand drivers include expanding global treatment access with 31.6 million people now accessing antiretroviral therapy (up from 7.7 million in 2010), revolutionary long-acting injectable therapies including Yeztugo and Apretude reducing pill burden and improving adherence, and government initiatives such as the CDC's 90-90-90 plan promoting treatment optimization and viral suppression across diverse patient populations.

North America dominates the HIV therapeutics market with 42% market share in 2025, driven by the United States' substantial disease burden, advanced healthcare infrastructure, leading pharmaceutical innovation capacity, comprehensive treatment access programs, and highest treatment coverage rates among developed nations globally.

Long-acting injectable PrEP and treatment expansion represents the most significant market opportunity, with twice-yearly lenacapavir (Yeztugo) demonstrating 100% efficacy prevention and twice-yearly cabotegravir reducing injection frequency to 12 times annually, dramatically improving patient adherence and enabling prevention of HIV infections across high-risk populations in developed and emerging markets.

Gilead Sciences, Inc., ViiV Healthcare, Merck & Co., Inc., Johnson & Johnson (Janssen Pharmaceuticals), etc.